Sample Category Title

Dollar Index Outlook: Falls Almost 2% in Atypical Reaction on US Tariffs

The dollar was sharply down across the board on Thursday, smashed by the latest large package of import tariffs that President Trump announced on Wednesday.

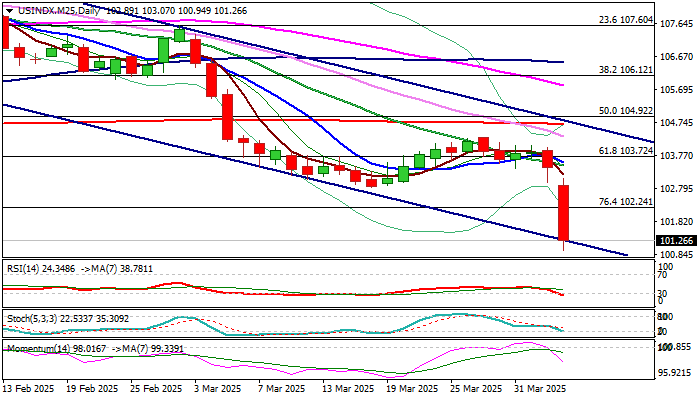

The dollar index fell to a six-month low following strong acceleration lower, in which the currency lost nearly 2% of its value, in the biggest daily fall in years.

Although the reaction was atypical as risk aversion should be likely scenario in such circumstances and inflate the greenback, fresh weakness helped in boosting the effect of tariffs for the US and make life much more complicated to US trading partners.

Technical picture has weakened further on daily chart (MA’s are in full bearish setup, 14-d momentum remains in a steep decline deeper into negative territory and the latest drop cracked the support line of bear channel) signaled continuation of larger downtrend, with loss of last significant support at 102.24 (Fibo 76.4% of 99.84/110.00 rally) opening way towards targets at 100.00 (psychological) and 99.84 (2024 low of Sep 27).

Partial profit taking should be anticipated after heavy losses, but strong negative sentiment is expected to keep dollar under increased pressure and limit upticks.

Broken Fibo level reverted to resistance (102.24) which should ideally cap and keep broader bears fully in play.

Res: 101.79; 102.24; 102.82; 103.07.

Sup: 100.94; 100.40; 100.00; 99.84.

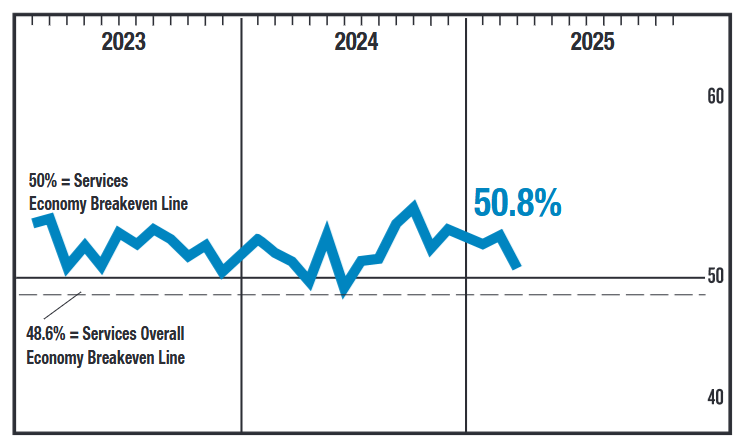

ISM Services Index Tumbles in March as New Orders and Employment Slump

The ISM Services index fell 2.7 points to 50.8 in March, short of the 52.9 consensus was expecting. Ten of eighteen industries reported growth in March, down from fourteen in February.

Business activity advanced, rising 1.5 points to 55.9. New orders fell to 50.4, extending its downward trajectory, and just above the 50 cut-off for growth. Notably, apart from the one-off contractions in June 2024, December 2022, and the shutdown months of April and May 2020, today's print is the softest new orders reading since July 2009.

The employment index sank sharply (46.2 vs. 53.9 in February), suggesting services payrolls turned lower in March. However, the employment index has signaled contraction several times in early 2024, while the labor market continued to expand.

The prices paid sub-component took a step back to 60.9 from 62.9 in February. The trend in the index suggests services prices pressures are likely to persist over the near-term. The three-month moving average of the index is at 61.3, just below its April 2023 level of 61.4.

Key Implications

The services sector cooled a bit in March. Business activity ticked up showing firms continue to expand operations, but the details of the report left quite a bit to be desired. The downward trend in new orders growth is notable, while the employment subindex fell into contraction territory again. Moreover, several respondents cited tariffs in their comments as impacting current business conditions.

How economic uncertainty filters through to the services sector is now all-important. Yesterday's announcement on tariffs is likely to kick-start global negotiations, but in the meantime businesses and households are going to be in wait-and-see mode for where things eventually settle. The focus now shifts to tomorrow's payrolls report for, hopefully, some clarity on how market conditions could be impacting the labor market.

Sunset Market Commentary

Markets

Yesterday, optimists still hoped that the announcement of reciprocal US tariffs could bring some bad news, but at least also some clarity, providing a new reference framework. Even a worst case economic scenario could in this respect have helped find risk markets looking for a bottom. It’s a pity, but this proved to be the wrong assessment. Persistent uncertainty more than ever remains an integral part of the Trump roadmap. Announced tariffs only serve as a ‘friends price’ (halve what the US sees as the effective damage) and can be raised if trading partners retaliate (as e.g. China and the EU are preparing) and/or if negotiations fail. In addition, the tariffs for sure are higher than most expected, resulting in higher than feared economic damage both for the US and for its trading partners. An outright further risk sell-off was inevitable. Asian equity losses varied widely across markets (e.g. Nikkei -2.75%, China CSI 300 ‘only’ -0.59%). European equities opened with losses of about 2%, but after a brief pause deepened losses going into the US open (Eurostoxx currently -3%). The Nasdaq opened 4.5 % lower. For the US, stagflation risks are mounting sharply. For trading partners, risks might be more axed to growth. Bond markets clearly focused on the growth risks. Yields decline sharply with curves bull steepening. US yields decline between 17 bps (5-y) and 5 bps (30-y). Markets are discounting a 90% chance of a next Fed rate cut in June and a cumulative easing of 75+ bps this year. The 10-y yield fell below the 4% barrier for the first time since October. This implies the Fed giving up its primary focus on inflation. For now, there was no sign of the Fed amending its wait-and-see approach yet. Powell in a speech scheduled tomorrow might (or might not) provide some guidance on the Fed’s reaction function. German yields (off the intraday lows) decline between 11 bps (2 and 5-y) and 3 bps (30-y). Understandably, the March focus on a fiscally driven EU reflation evaporates further. Still we keep the idea in the back of our mind as a further fiscal response might still resurface. Spain announcing €14,1bn in aid to address the fall-out of the tariffs serves as a point in case. The country also advocates a similar initiative at a European level. Fiscal risk premia to return at some point?

On FX markets, a US stagflation narrative, underperformance of US assets, further loss of confidence in (the predictability of) US institutions and the Trump government for sure being happy with a weaker dollar all contribute to a broad-based USD sell-off. DXY tumbled from a 103.8 close yesterday to currently 101.6. Key support at 100.15/99.58 (2024/23 low) is approaching fast. EUR/USD jumps from 1.085 to 1.1125, with the 2024 top (1.1214) serving as next target. Cable also cleared the 1.3015 YTD top but despite a ‘mild’ UK 10% tariff, sterling isn’t able to match the euro’s performance. EUR/GBP almost gains a full big figure (0.8435). USD/JPY is falling off a cliff (145.6 from 149.25). The yen and the euro, admittedly in volatile intraday trading, are keeping each other in balance (EUR/JPY 161.75).

News & Views

Swiss inflation unexpectedly steadied in March. A flat monthly pace resulted in a 0.3% y/y print, equaling the February outcome compared to the 0.4% consensus forecast. Core inflation rose by the expected 0.9% y/y. The slight CPI miss had a near-negligible impact on the Swiss franc with the dominating theme today being trade-related risk off. The fallout for EUR/CHF (0.953) remains contained though. Swiss National Bank board member Tschudin was the first to comment on the US tariffs announced yesterday, saying the 31% slap was higher than anticipated. Based on calculations made by Switzerland’s State Secretariat for Economic Affairs, it could end up in a 1 ppt GDP hit. The SNB in March lowered the policy rate to 0.25% and money markets consider the possibility of another cut later this year. Tschudin refrained from commenting on the likelihood of returning to negative rates.

OPEC+ agreed to a larger than expected output hike next month and plan to add 411k barrels a day. That’s three times the 138k boost that kicked in this month, which was the first rollback of the production curbs in place for several years now. Delegates said it is intended to put pressure on members of the cartel that have been exceeding their production quotas as bigger supply forces the prices to go down. Brent oil, which was already slipping over tariff-triggered growth concerns, extended its daily slide on the news to $70.6/b. Since Trump’s presser yesterday, Brent stumbled almost 6%.

US ISM services falls to 50.8, employment tumbles into contraction at 46.2

US ISM Services PMI dropped sharply from 53.5 to 50.8 in March, falling well short of expectations (53.1).

While business activity improved to 55.9, the gain was overshadowed by deteriorating demand and labor market conditions. New orders fell from 52.2 to 50.4, barely holding above stagnation. Employment index plunged from 53.9 to 46.2—marking the first contraction since September 2024.

The steep drop in services employment is particularly concerning, as it may signal deeper caution among businesses in the face of growing uncertainty over trade and the broader economic outlook.

Meanwhile, prices paid for services eased slightly, with the index slipping from 62.6 to 60.9, though still reflecting elevated inflationary pressures in the sector.

According to ISM's historical correlations, the March reading aligns with an annualized GDP growth rate of just 0.7%.

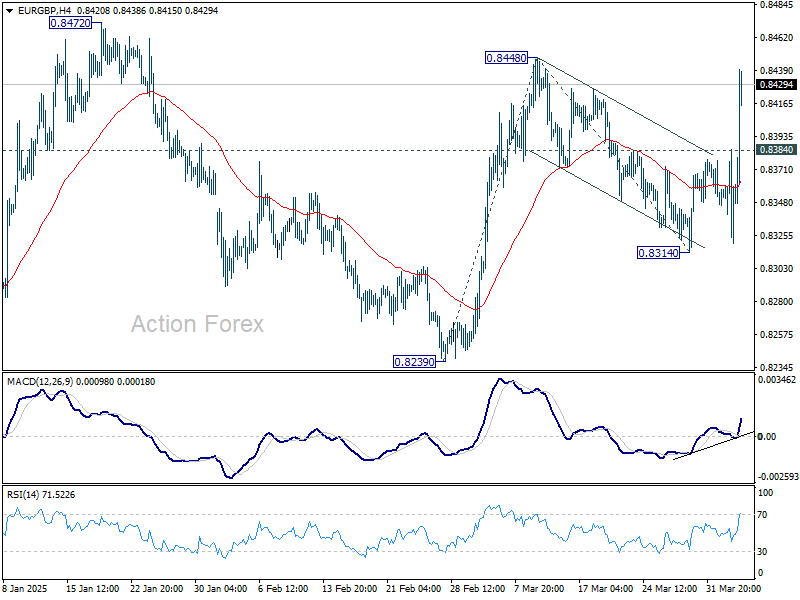

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8320; (P) 0.8354; (R1) 0.8380; More...

EUR/GBP's strong rally today suggests that fall from 0.8448 has completed at 0.8314 as a correction only. Intraday bias is back on the upside. Firm break of 0.8448 will target medium term channel resistance (now at 0.8490), and probably further to 100% projection of 0.8239 to 0.8448 from 0.8314 at 0.8523.

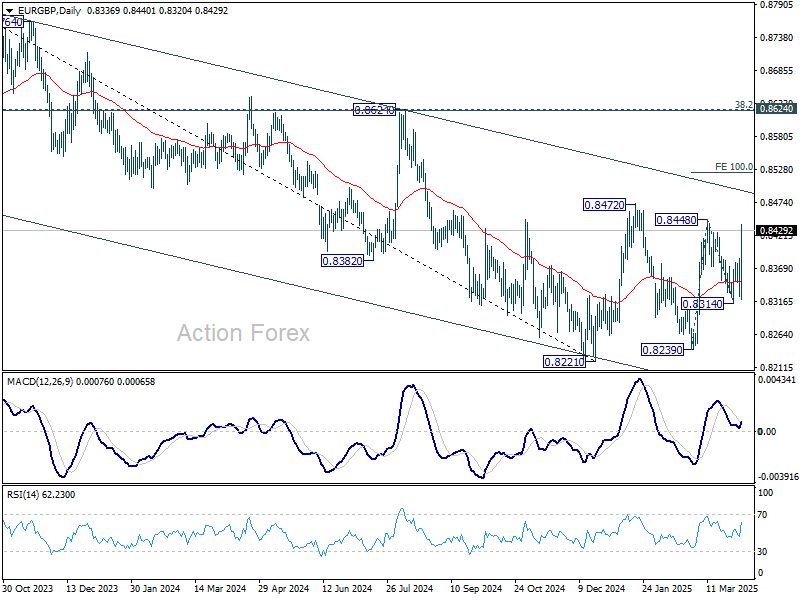

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8490).

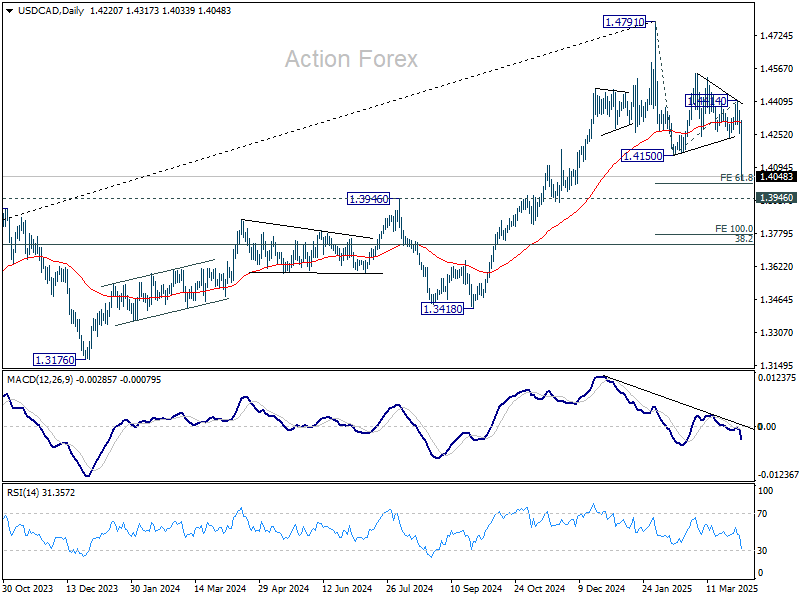

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4264; (P) 1.4339; (R1) 1.4380; More...

USD/CAD's fall from 1.4791 resumed by breaking through 1.4150 support and accelerated to as low as 1.4039 so far. Intraday bias remains on the downside for 61.8% projection of 1.4791 to 1.4150 from 1.4414 at 1.4018. Decisive break there would pave the way to 100% projection at 1.3773 next. On the upside, above 1.4158 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, focus is now on 1.3976 resistance turned support (2022 high), which is close to 55 W EMA (now at 1.3986). Sustained break there should confirm medium term topping at 1.4791. Deeper correction would be seen to 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727.

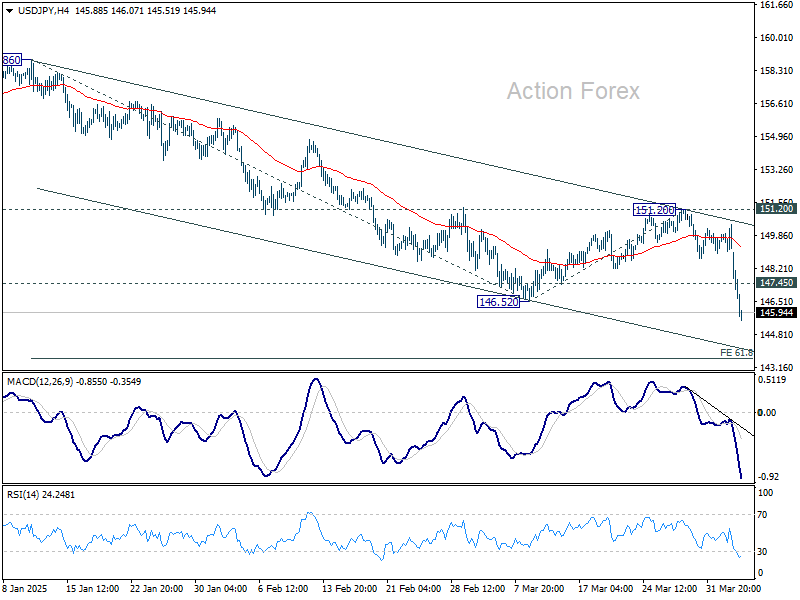

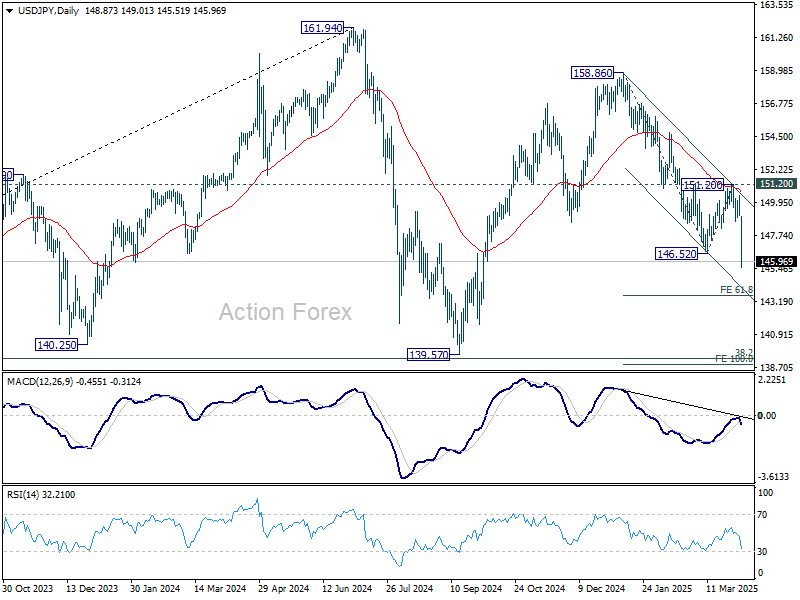

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.80; (P) 149.64; (R1) 150.19; More...

Break of 146.52 support confirms resumption of decline from 158.86. Intraday bias remains on the downside for s 61.8% projection of 158.86 to 146.52 from 151.20 at 143.57. On the upside, above 147.45 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

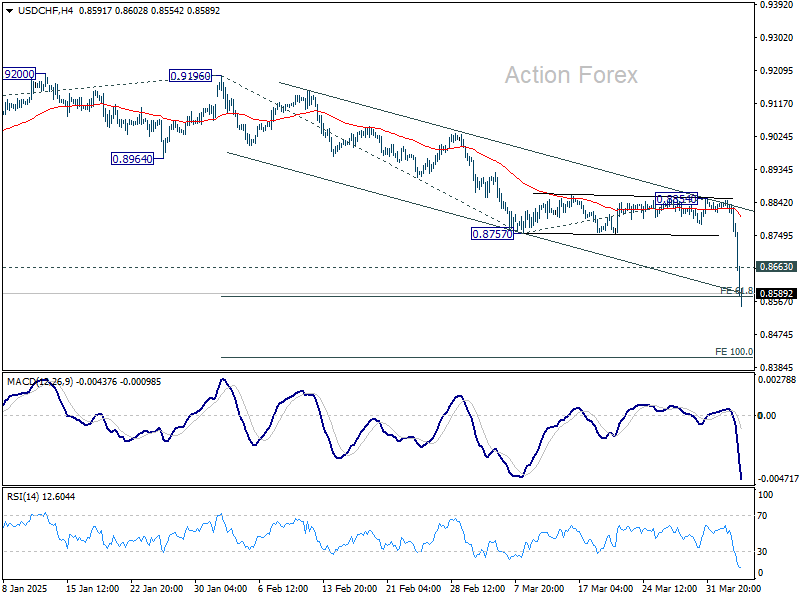

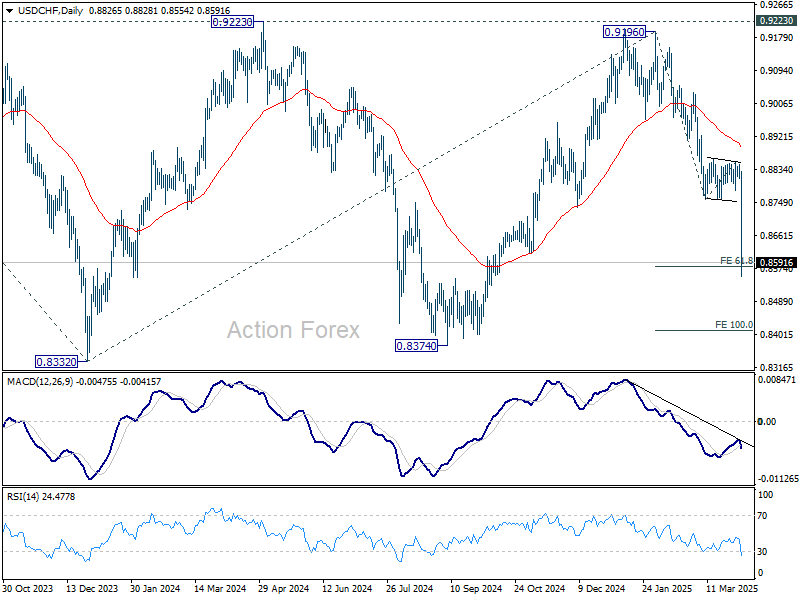

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8827; (R1) 0.8841; More…

USD/CHF's decline accelerated to as low as 0.8554 so far today and met 61.8% projection of 0.9196 to 0.8757 from 0.8854 at 0.8583 already. Intraday bias stays on the downside. Sustained trading below 0.8583 will pave the way to 100% projection at 0.8415. On the upside, above 0.8663 minor resistance will turn intraday bias neutral and bring consolidations first. Before staging another fall.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

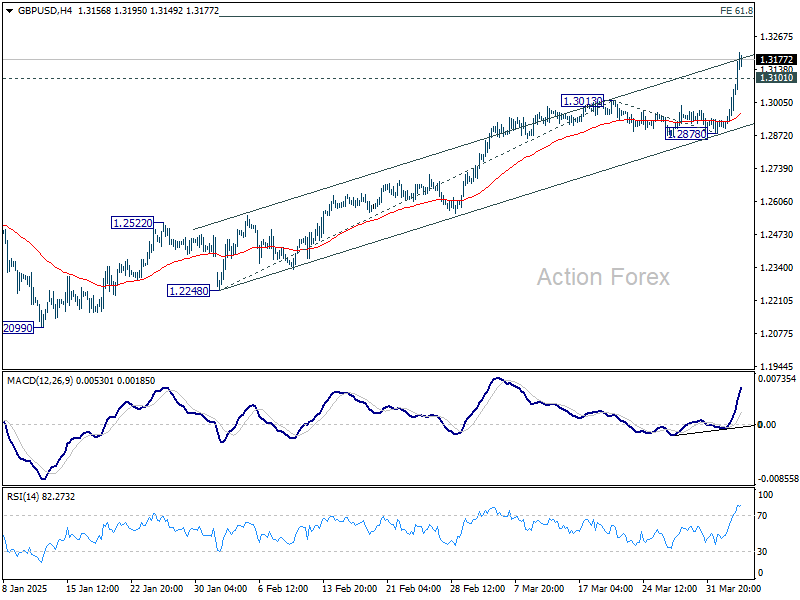

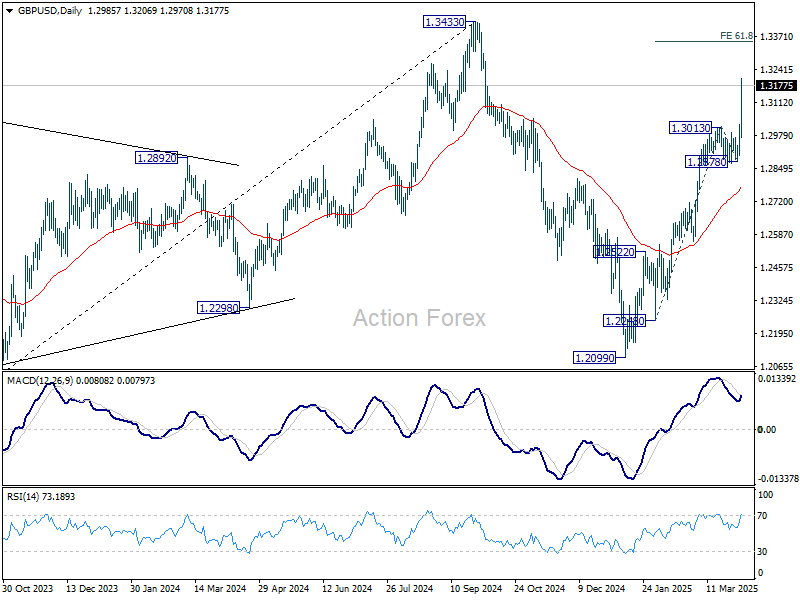

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2932; (P) 1.2979; (R1) 1.3056; More...

GBP/USD accelerates higher today and intraday bias stays on the upside. Current rally from 1.2099 will target 61.8% projection of 1.2248 to 1.3013 from 1.2878 at 1.3351. On the downside, below 1.3101 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

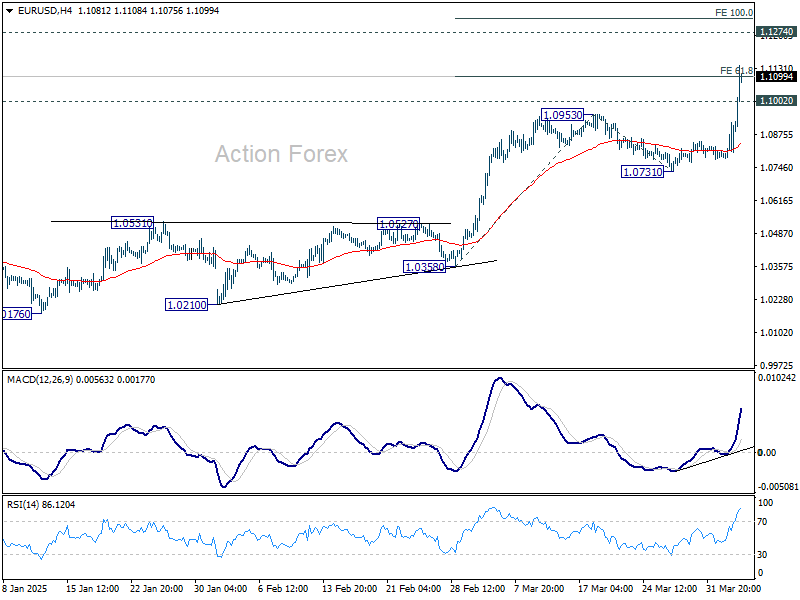

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0785; (P) 1.0855; (R1) 1.0929; More...

EUR/USD's rally accelerates to as high as 1.1145 so far, and met 61.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1099 already. Intraday bias stays on the upside. Sustained trading above 1.1099 will pave the way 1.1274 key resistance, and probably further to o 100% projection at 1.1326. On the downside, below 1.1002 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.