Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0783; (P) 1.0816; (R1) 1.0848; More...

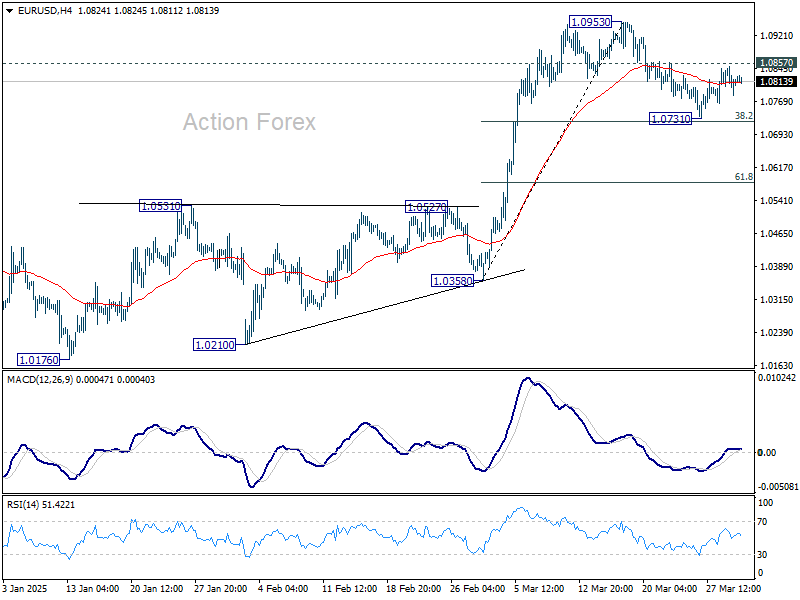

Intraday bias in EUR/USD remains neutral and outlook is unchanged. On the upside, break of 1.0857 resistance will indicate that correction from 1.0963 has completed already. Retest of 1.0953 should be seen first. Firm break there will resume the rally from 1.0176 towards 1.1274 key resistance. In any case, outlook will remain bullish as long as 38.2% retracement of 1.0358 to 1.0953 at 1.0726 holds.

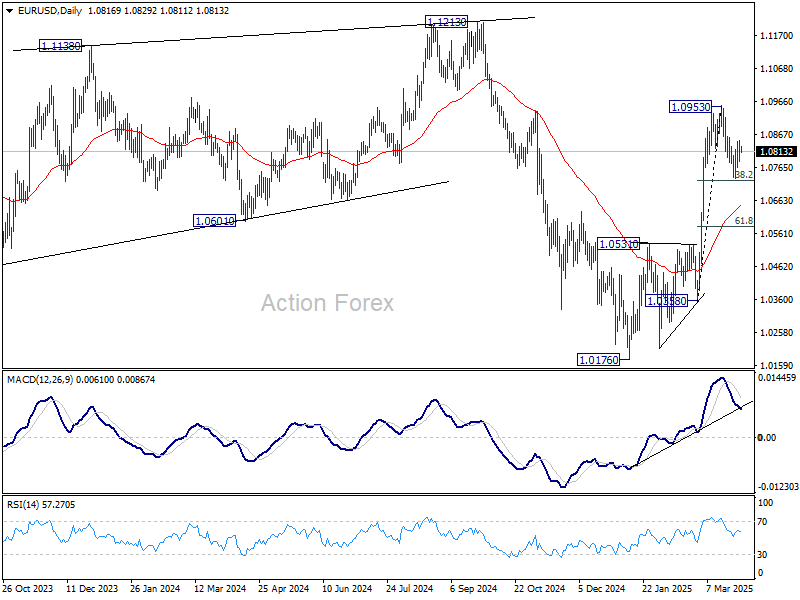

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

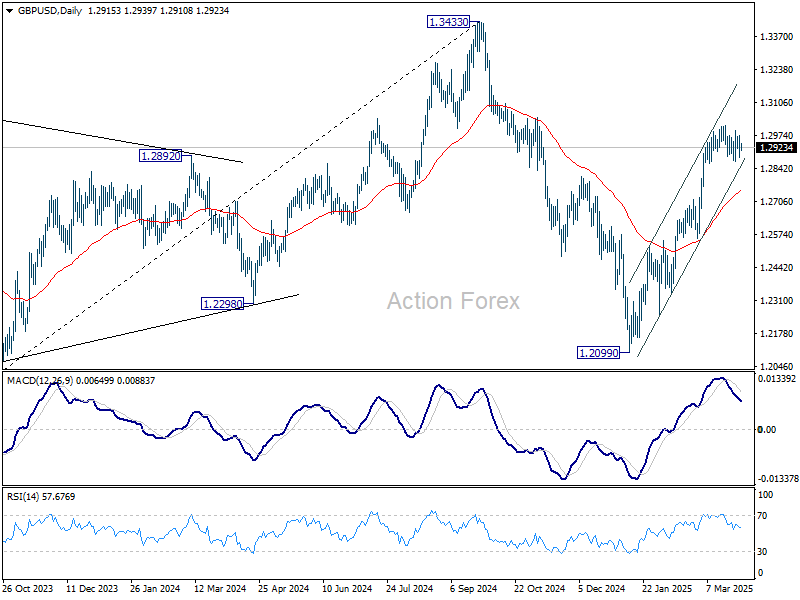

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2879; (P) 1.2925; (R1) 1.2964; More...

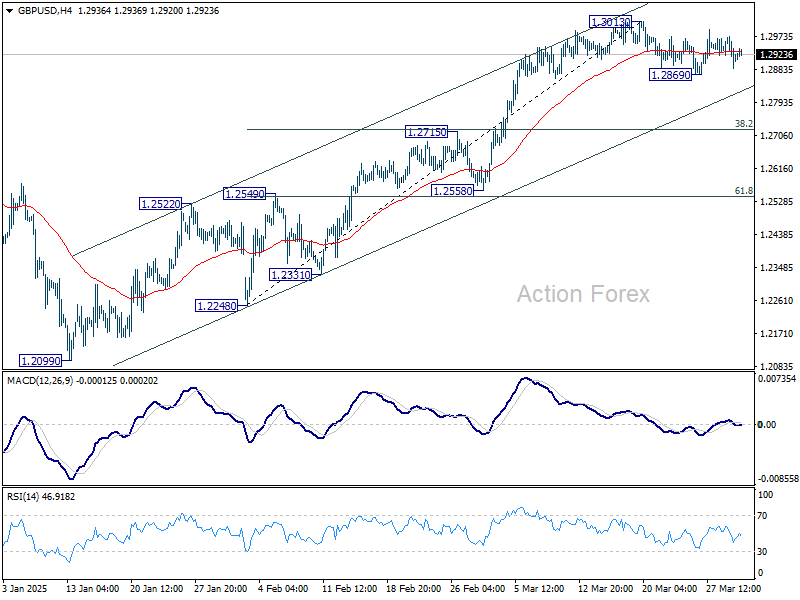

Intraday bias in GBP/USD remains neutral as consolidations continue below 1.3013. On the downside, below 1.2869 will bring deeper correction. But downside should be contained above 38.2% retracement of 1.2248 to 1.3013 at 1.2721. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

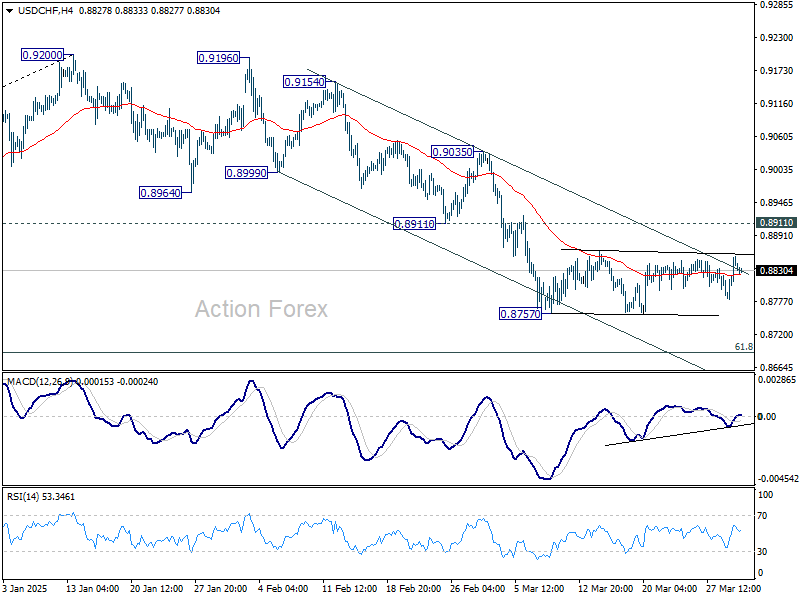

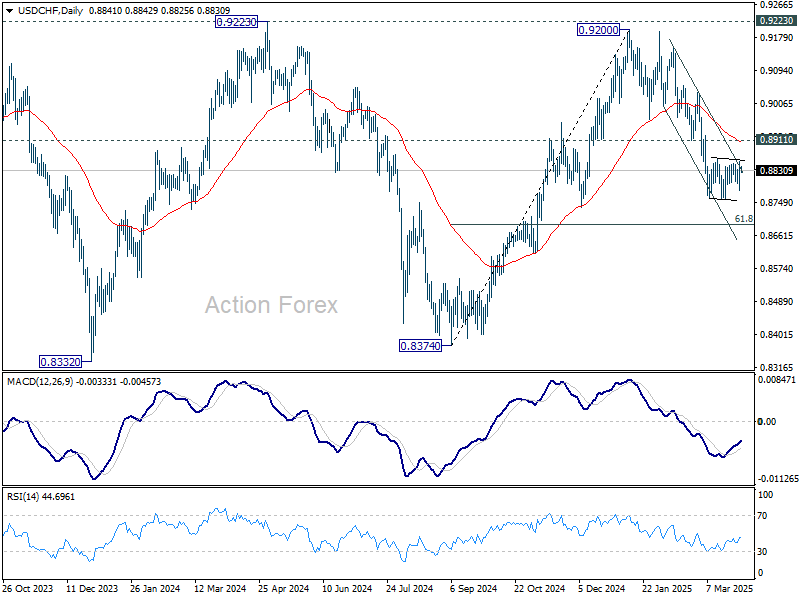

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8798; (P) 0.8827; (R1) 0.8873; More…

USD/CHF is still bounded in consolidation from 0.8757 and intraday bias stays neutral. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

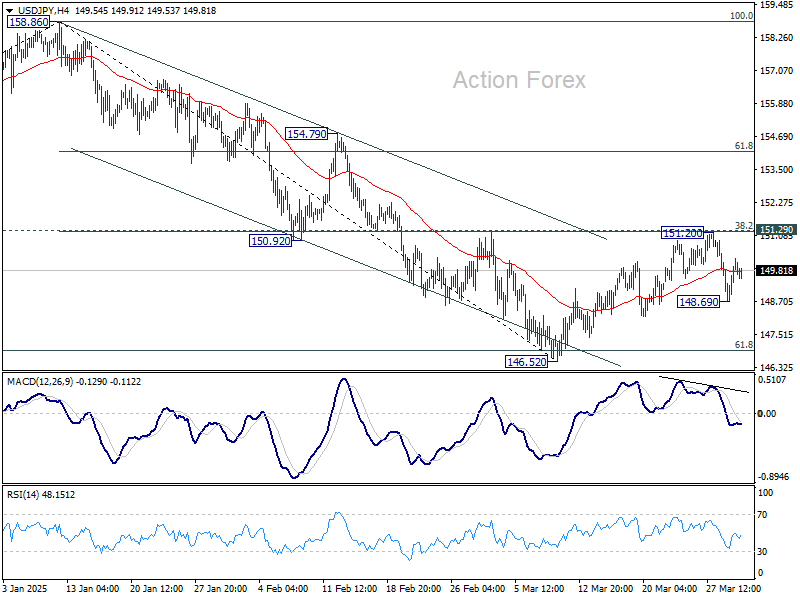

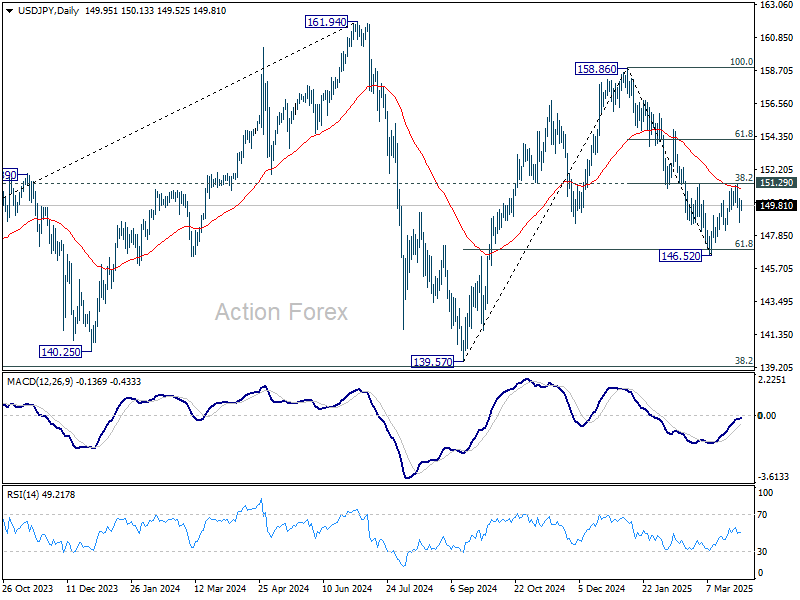

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.02; (P) 149.65; (R1) 150.59; More...

Intraday bias in USD/JPY is turned neutral with current recovery. Outlook is unchanged that corrective rise from 146.52 has completed at 151.20. Risk will stay on the downside as long as 151.29 resistance holds. Below 148.69 will bring retest of 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

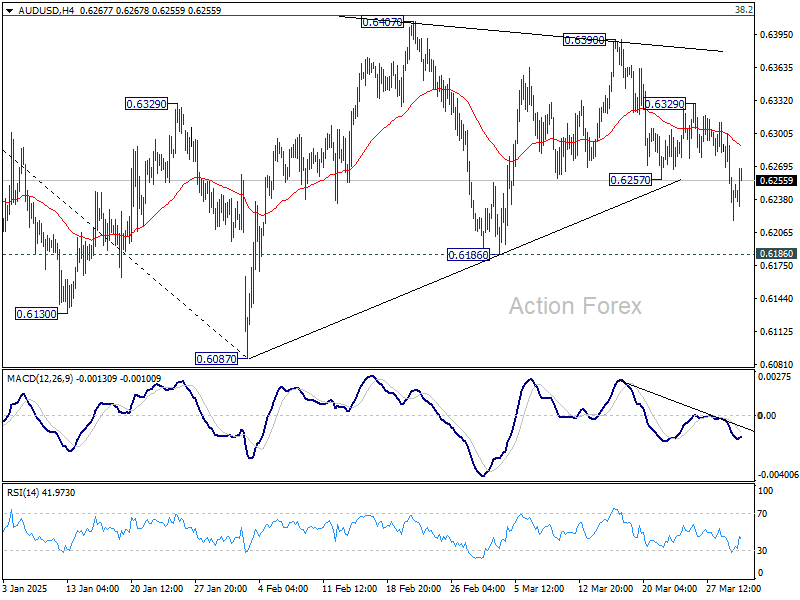

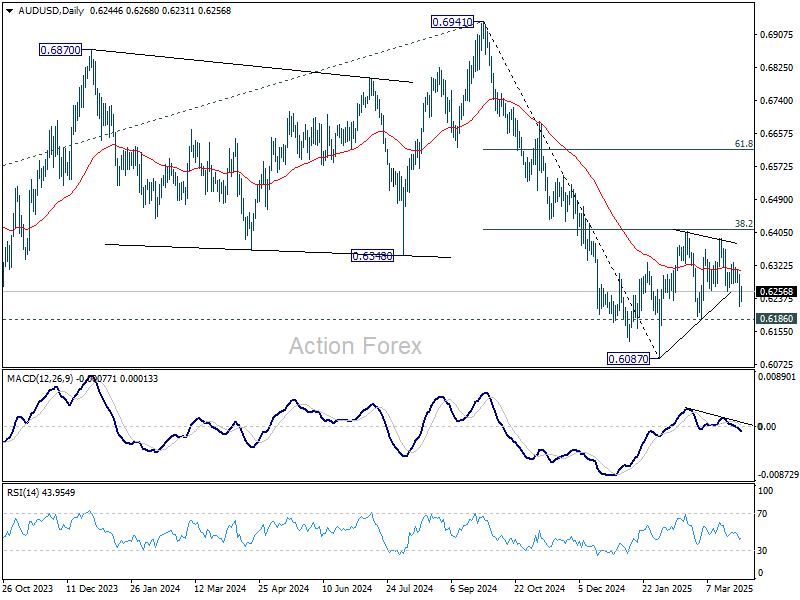

AUD/USD Daily Report

Daily Pivots: (S1) 0.6210; (P) 0.6256; (R1) 0.6292; More...

Intraday bias in AUD/USD remains mildly on the downside for 0.6186 support. Firm break there will indicate that corrective pattern from 0.6087 has completed and larger fall from 0.6941 is ready to resume. For now, risk will stay on the downside as long as 0.6329 resistance holds, in case of recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6467) holds.

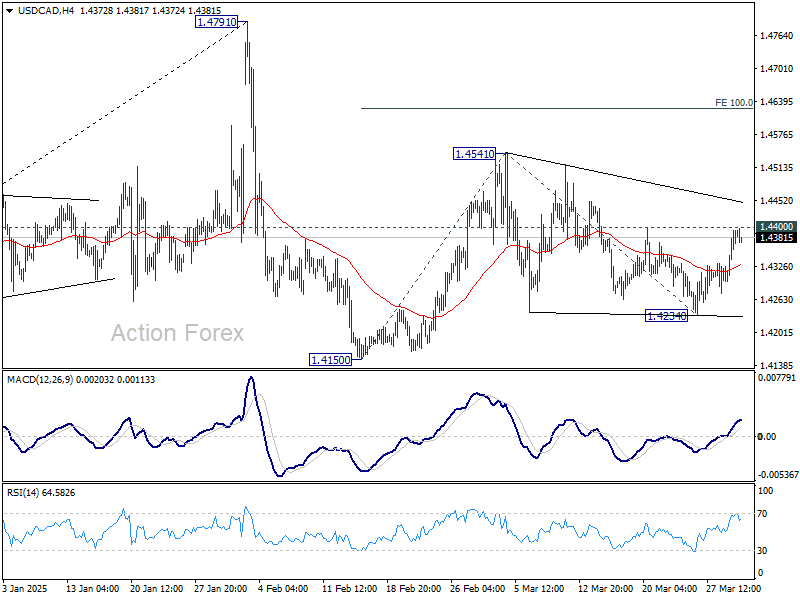

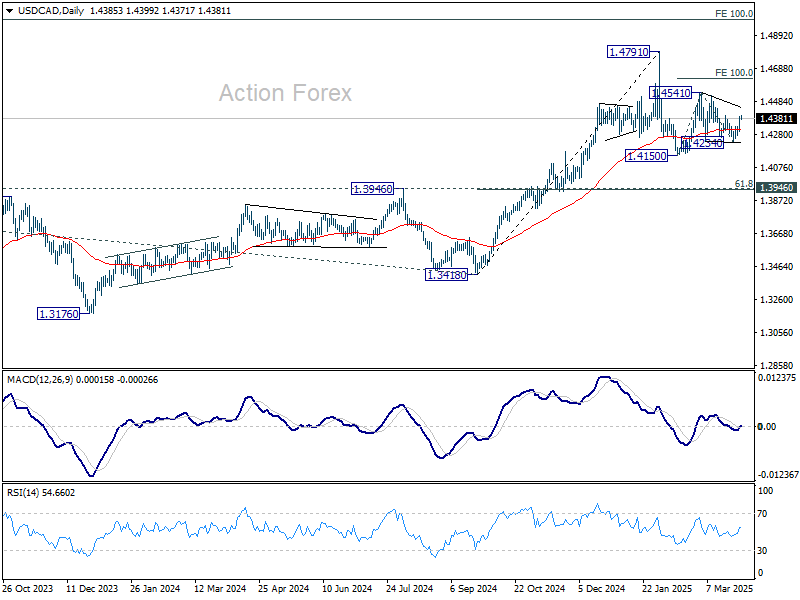

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4327; (P) 1.4361; (R1) 1.4424; More...

Intraday bias in in USD/CAD remains neutral at this point. Overall, corrective pattern from 1.4791 is still extending. On the upside, break of 1.4400 will argue that it's still in the second leg. Intraday bias will be turned back to the upside fro 1.4541 resistance first, and then 100% projection of 1.4150 to 1.4541 from 1.4234 at 1.4625. On the downside, though, break of 1.42324 support will suggest that the third leg has already started for 1.4150 and below.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Markets Stabilize Ahead of Tariff D-Day, Focus Turns to Eurozone CPI and ISM Manufacturing

The global equity selloff appears to have passed its peak—at least for now. After days of heavy risk-off moves driven by fears surrounding the upcoming US reciprocal tariffs announcement on Wednesday, traders have taken a cautious step back into a wait-and-see mode. US indexes clawed back most of their earlier losses overnight, closing mixed. Asian markets followed with mild gains in early Tuesday trading.

Currency markets, meanwhile, are staying largely range-bound in Asian session. Despite the calm surface, risk aversion remains evident in the performance breakdown. Kiwi, Aussie, and Loonie are still the worst performers for the week so far. On the flip side, Yen and Dollar are leading the pack, followed by Euro. Sterling and Swiss Franc are holding middle ground.

A major focus for today will be Eurozone’s flash CPI data. Recent media reports have revealed that some ECB officials are warming up to the idea of pausing rate cuts at the upcoming meeting on April 17. Odds now stand at around 65% for another 25bps reduction. While the doves remain committed to further easing, many appear willing to skip a meeting if hawks insist on more time to assess evolving risks. Any upside surprise in today's inflation print would strengthen the hawkish camp and make a pause more likely.

US ISM Manufacturing Index will also draw much attention. After briefly returning to expansion territory for just two months, the index is expected to slip back into contraction. Beyond headline activity, the price component will be scrutinized, especially in light of the impending tariffs. Prices index has surged from around 50 to over 60 this year—further acceleration could signal inflationary pressures re-emerging on the supply side.

Technically, EUR/CHF is worth a watch today, considering the impact of Eurozone inflation data. Rebound from 0.9486 is gathering some upside momentum. Break of 0.9581 resistance will argue that correction from 0.9660 has already completed, after drawing support from 0.9489. Further rise should then bee seen through 0.9660 to resume the whole rally from 0.9204.

In Asia, at the time of writing, Nikkei is up 0.29%. Hong Kong HSI is up 0.53%. China Shanghai SSE is up 0.36%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.015 at 1.503. Overnight, DOW rose 1.0%. S&P 500 rose 0.55%. NASDAQ fell -0.14%. 10-year yield fell -0.009 to 4.246.

RBA stands pat, inflation eases as expected, but outlook clouded

RBA kept the cash rate target unchanged at 4.10% today, in line with broad market expectations. While the central bank welcomed the continued decline in underlying inflation, it emphasized a "cautious" stance due "risks on both sides".

Recent data suggests inflation is easing in line with forecasts, but RBA reiterated that it needs greater confidence that this trend will continue sustainably toward the midpoint of the 2–3% target band.

RBA highlighted "notable uncertainties" around domestic consumption and labor market dynamics. Internationally, there are concerns over the escalating US tariff policy, noting that such developments are already affecting global confidence.

The risk of further tariff expansion or retaliatory measures from other countries could amplify the drag on global activity. Inflation could move in "either direction" depending on how households and firms react to the shifting macroeconomic environment.

Japan's Tankan survey flags manufacturing caution, services hit 33-year high

Japan’s Q1 Tankan survey revealed a mixed outlook for the economy, with sentiment among large manufacturers slipping for the first time in a year. The index fell from 14 to 12, in line with expectations, as steel and machinery producers grew more cautious amid weak global demand, rising input costs, and uncertainty surrounding US tariff policy.

However, manufacturing outlook ticked down just slightly to 12, beating expectations of a sharper decline to 9, indicating that businesses remain cautiously optimistic.

In contrast, Japan’s services sector showed remarkable resilience. The large non-manufacturing index rose from 33 to 35—marking the highest level since 1991. Still, the outlook component was flat at 28, slightly missing forecasts of 29.

Capital expenditure plans were also encouraging, with large firms expecting a 3.1% increase for fiscal 2025, ahead of consensus of 2.9%.

Japan PMI manufacturing finalized at 48.4, weaker domestic and international demand

Japan’s manufacturing sector contracted further in March, with final PMI reading falling to 48.4 from February’s 49.0, marking the lowest level in a year.

According to S&P Global, both output and new orders declined more sharply, reflecting "weaker demand from both domestic and international clients". Employment offered a rare bright spot, as firms increased hiring at the fastest rate in three months.

However, confidence remained muted and below the long-run average. Cost pressures also persisted, with strong increases in both input costs and selling prices, suggesting that "inflationary pressure across the sector remains acute".

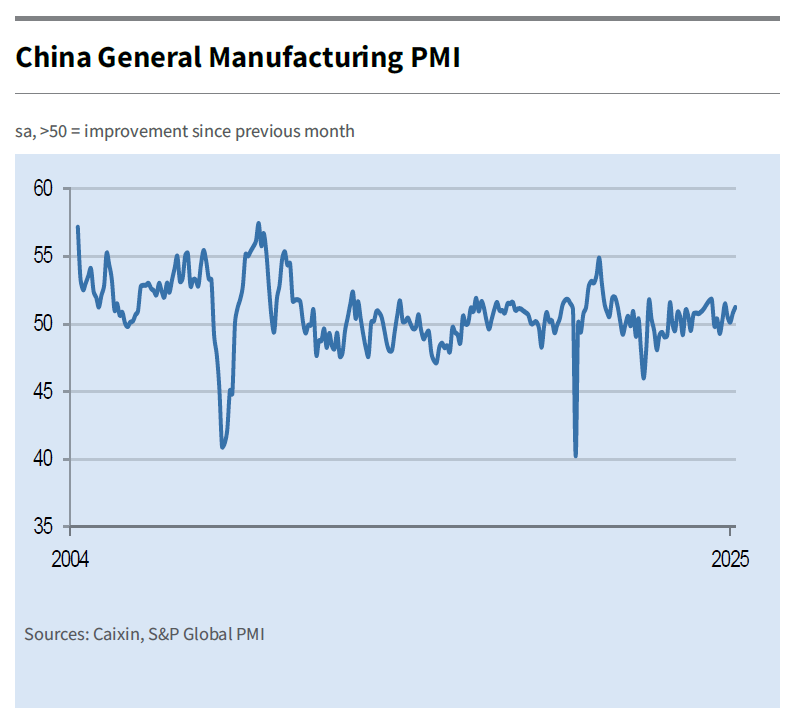

China Caixin manufacturing rises to 51.2, jobs and prices Lag

China’s Caixin PMI Manufacturing rose to 51.2 in March, up from 50.8 and marking a four-month high.

According to Wang Zhe of Caixin Insight Group, the upbeat print points to a steady start to the year, suggesting broader signs of recovery in the industrial sector.

Still, challenges remain beneath the surface. The labor market "remained relatively sluggish". In addition, "deflationary pressures persisted", driven by weak domestic demand and cautious sentiment among market participants.

Fed’s Williams: Tariff impacts on inflation could linger for years

New York Fed President John Williams cautioned that the inflationary effects of new US tariffs could be "more prolonged" than initially anticipated.

In an interview with Yahoo Finance, Williams emphasized that while the immediate price increases are expected, the true impact of tariffs “might not be fully felt for a couple of years."

He stressed the importance of monitoring not just the direct price changes, but also the “indirect effects” that ripple through the broader economy over time.

“It is still early days to be able to come to a concrete conclusion around this,” Williams said, noting that Fed will need to remain open-minded about "how long these last in terms of their effects on inflation and the economy.”

Fed’s Barkin: Tariffs create dual risks for inflation and jobs

Richmond Fed President Thomas Barkin highlighted growing concerns over the economic impact of the Trump administration’s upcoming tariffs. He told CNBC that the tariffs could both stoke inflation and weigh on the labor market.

“Call me nervous on both,” Barkin said, signaling that the path forward for monetary policy remains highly data-dependent.

Barkin emphasized "there's a lot of uncertainty right now, and I think that makes the case for wait and see how this plays out."

Looking ahead

Eurozone CPI flash is the main focus in European session. Eurozone will release unemployment rate and PMI manufacturing final. UK will release PMI manufacturing final. Swiss will release retail sales and PMI manufacturing. Later in the day, US ISM manufacturing is the main focus. Canada will also release PMI manufacturing.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4327; (P) 1.4361; (R1) 1.4424; More...

Intraday bias in in USD/CAD remains neutral at this point. Overall, corrective pattern from 1.4791 is still extending. On the upside, break of 1.4400 will argue that it's still in the second leg. Intraday bias will be turned back to the upside fro 1.4541 resistance first, and then 100% projection of 1.4150 to 1.4541 from 1.4234 at 1.4625. On the downside, though, break of 1.42324 support will suggest that the third leg has already started for 1.4150 and below.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

RBA stands pat, inflation eases as expected, but outlook clouded

RBA kept the cash rate target unchanged at 4.10% today, in line with broad market expectations. While the central bank welcomed the continued decline in underlying inflation, it emphasized a "cautious" stance due "risks on both sides".

Recent data suggests inflation is easing in line with forecasts, but RBA reiterated that it needs greater confidence that this trend will continue sustainably toward the midpoint of the 2–3% target band.

RBA highlighted "notable uncertainties" around domestic consumption and labor market dynamics. Internationally, there are concerns over the escalating US tariff policy, noting that such developments are already affecting global confidence.

The risk of further tariff expansion or retaliatory measures from other countries could amplify the drag on global activity. Inflation could move in "either direction" depending on how households and firms react to the shifting macroeconomic environment.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.10 per cent and the interest rate paid on Exchange Settlement balances at 4 per cent.

Underlying inflation is moderating.

Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. Recent information suggests that underlying inflation continues to ease in line with the most recent forecasts published in the February Statement on Monetary Policy. Nevertheless, the Board needs to be confident that this progress will continue so that inflation returns to the midpoint of the target band on a sustainable basis. It is therefore cautious about the outlook.

The Board noted that monetary policy is well placed to respond to international developments if they were to have material implications for Australian activity and inflation.

The outlook remains uncertain.

Private domestic demand appears to be recovering, real household incomes have picked up and there has been an easing in some measures of financial stress. However, businesses in some sectors continue to report that weakness in demand makes it difficult to pass on cost increases to final prices.

At the same time, a range of indicators suggest that labour market conditions remain tight. Despite a decline in employment in February, measures of labour underutilisation are at relatively low rates and business surveys and liaison suggest that availability of labour is still a constraint for a range of employers. Wage pressures have eased a little more than expected but productivity growth has not picked up and growth in unit labour costs remains high.

There are notable uncertainties about the outlook for domestic economic activity and inflation. The central projection is for growth in household consumption to continue to increase as income growth rises. But there is a risk that any pick-up in consumption is slower than expected, resulting in continued subdued output growth and a sharper deterioration in the labour market than currently expected. Alternatively, labour market outcomes may prove stronger than expected, given the signal from a range of leading indicators.

More broadly, there are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the demand environment and weak productivity outcomes while conditions in the labour market remain tight.

Uncertainty about the outlook abroad also remains significant. On the macroeconomic policy front, recent announcements from the United States on tariffs are having an impact on confidence globally and this would likely be amplified if the scope of tariffs widens, or other countries take retaliatory measures. Geopolitical uncertainties are also pronounced. These developments are expected to have an adverse effect on global activity, particularly if households and firms delay expenditures pending greater clarity on the outlook. Inflation, however, could move in either direction. Many central banks have eased monetary policy since the start of the year, but they have become increasingly attentive to the evolving risks from recent global policy developments.

Sustainably returning inflation to target is the priority.

Sustainably returning inflation to target within a reasonable timeframe is the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment. To date, longer term inflation expectations have been consistent with the inflation target and it is important that this remain the case.

The Board’s assessment is that monetary policy remains restrictive. The continued decline in underlying inflation is welcome, but there are nevertheless risks on both sides and the Board is cautious about the outlook.

The Board will rely upon the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is resolute in its determination to sustainably return inflation to target and will do what is necessary to achieve that outcome.

China Caixin manufacturing rises to 51.2, jobs and prices Lag

China’s Caixin PMI Manufacturing rose to 51.2 in March, up from 50.8 and marking a four-month high.

According to Wang Zhe of Caixin Insight Group, the upbeat print points to a steady start to the year, suggesting broader signs of recovery in the industrial sector.

Still, challenges remain beneath the surface. The labor market "remained relatively sluggish". In addition, "deflationary pressures persisted", driven by weak domestic demand and cautious sentiment among market participants.