Sample Category Title

Canada’s Economy Surged in January, But Near-Term Growth Poised to Cool

Canadian economic growth started 2025 on strong footing, growing by 0.4% month-on-month (m/m). This was a tick above Statistics Canada's and consensus expectations for a 0.3% m/m gain. In February, Statistics Canada estimates that the Canadian economy held flat.

January's reading was broad-based, with output expanding in 13 of 20 industries. Growth in goods industries (+1.1% m/m) led the charge, while the services sector advanced by a modest 0.1% m/m.

On the goods side, mining/quarrying/oil & gas contributed most to the gain, led by oil & gas extraction (2.6% m/m). Meanwhile, the manufacturing sector grew by 0.8% m/m after two consecutive months of declines, and utilities registered a solid 2.7% m/m. The construction industry is seeing some positive momentum, led by a 1.4% m/m gain in residential building construction.

On the services side, wholesale trade (0.8% m/m) and public admin (0.3% m/m) were the biggest contributors to overall growth. Offsetting some of the positive effects was a 0.9% m/m decline in retail trade as spending on motor vehicles and parts dropped by a sizeable 3.2% m/m.

Key Implications

Make no mistake, the economic momentum that started in the fourth-quarter has clearly carried into the early stages of 2025. With the information we have at hand, Q1-2025 growth is tracking around 2.0% and in line with the Bank of Canada's January MPR projections. Past this, the outlook is turbulent. There are clear downside risks to Canada's economy, especially as the threat of widespread tariffs seems imminent come April 2nd.

The BoC has its work cut out for them. Under reasonable assumptions, we would expect the Bank to cut its policy rate by 25 bps over their next two meetings to support economic growth ahead of a worsening trade conflict. That could change if the U.S. administration reverses course on their tariff plans, but it's something that appears unlikely at this point.

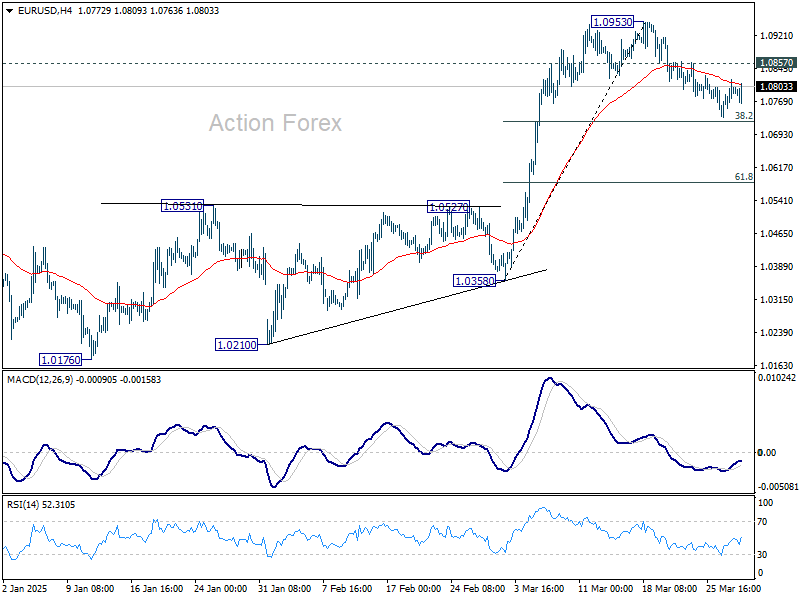

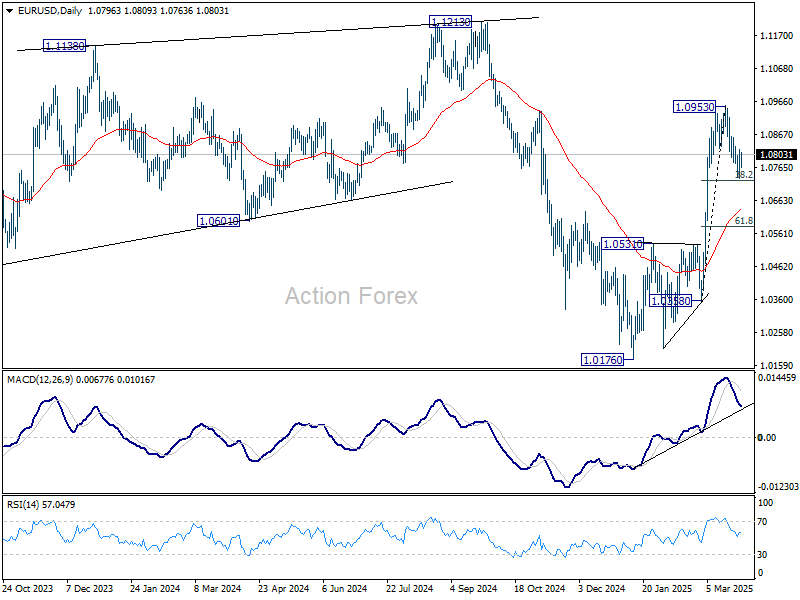

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0786; (R1) 1.0837; More...

No change in EUR/USD's outlook and intraday bias stays neutral. Strong support is expected from 38.2% retracement of 1.0358 to 1.0953 at 1.0726 to complete the correction from 1.0953. On the upside, break of 1.0857 will bring retest of 1.0953 first. Firm break there will resume larger rise from 1.0176. However, sustained break of 1.0726 will bring deeper correction to 55 D EMA (now at 1.0637).

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8818; (P) 0.8834; (R1) 0.8855; More…

Intraday bias in USD/CHF remains neutral for the moment. Consolidation from 0.8757 could extend. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

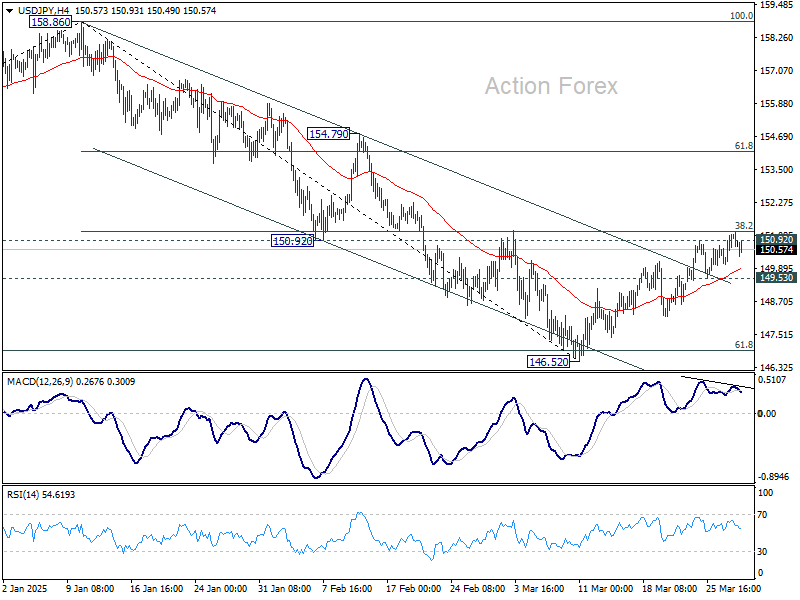

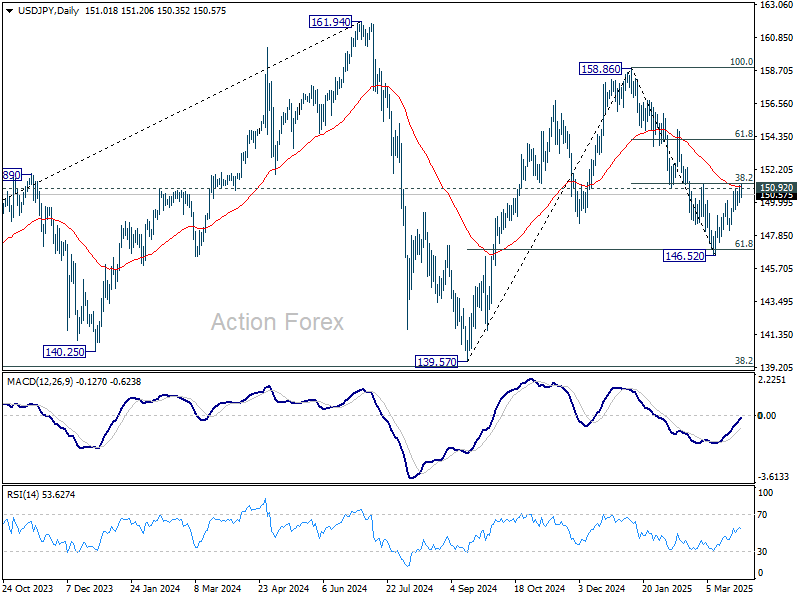

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.35; (P) 150.75; (R1) 151.45; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Strong resistance is still expected from 150.92 to complete the corrective recovery from 146.52. On the downside break of 149.53 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. However, firm break of 150.92 will argue that fall from 158.86 has completed and turn bias back to the upside for 154.79 resistance next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

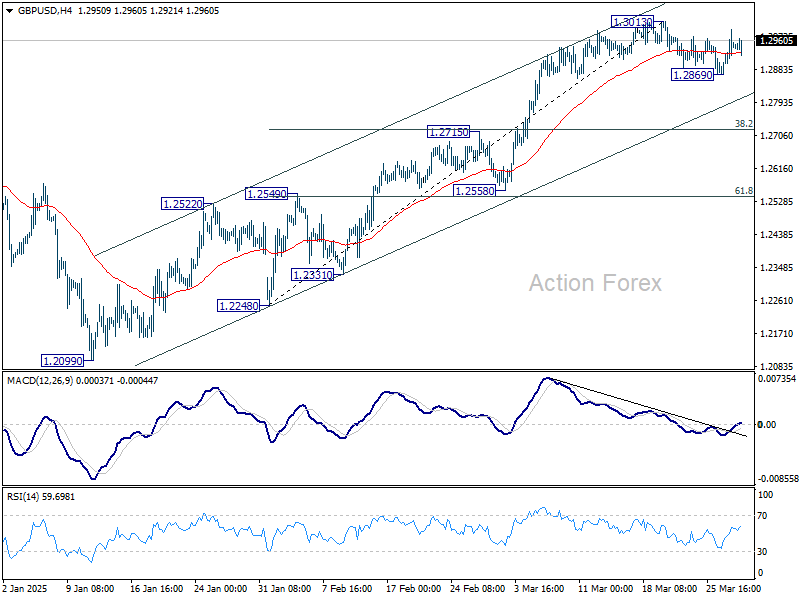

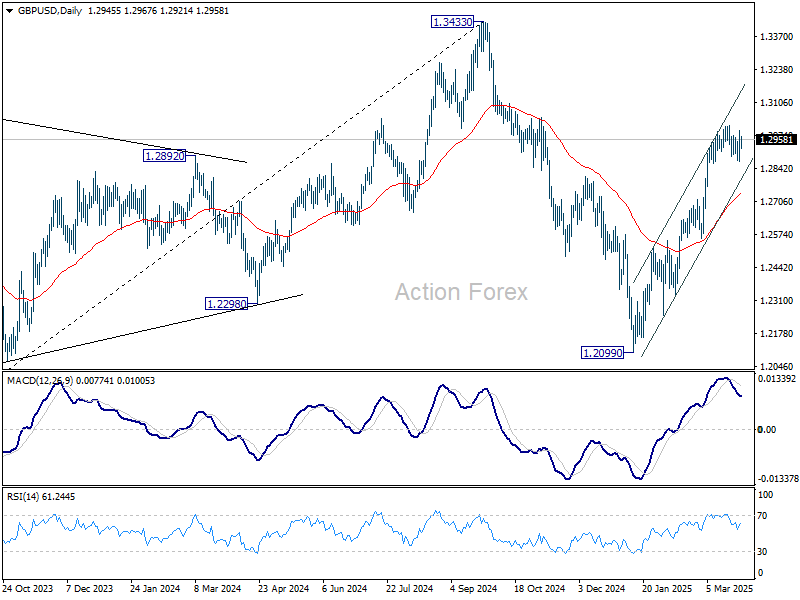

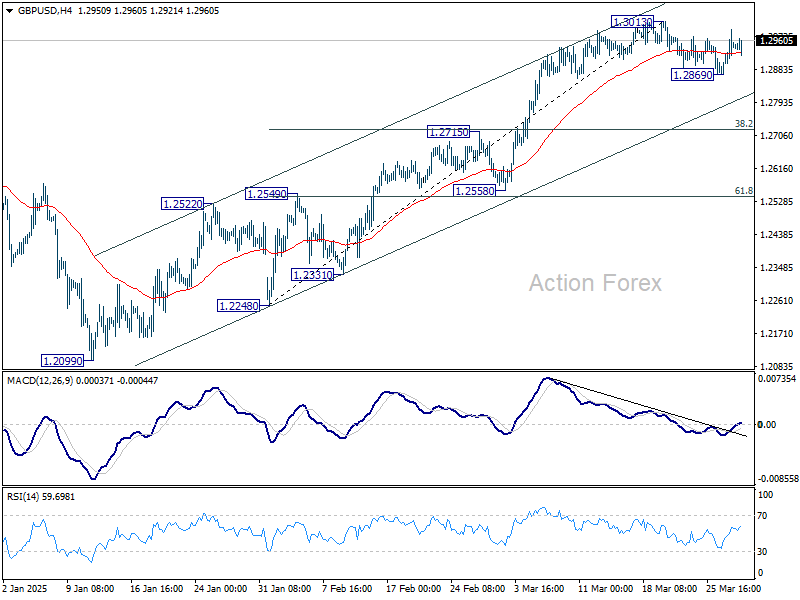

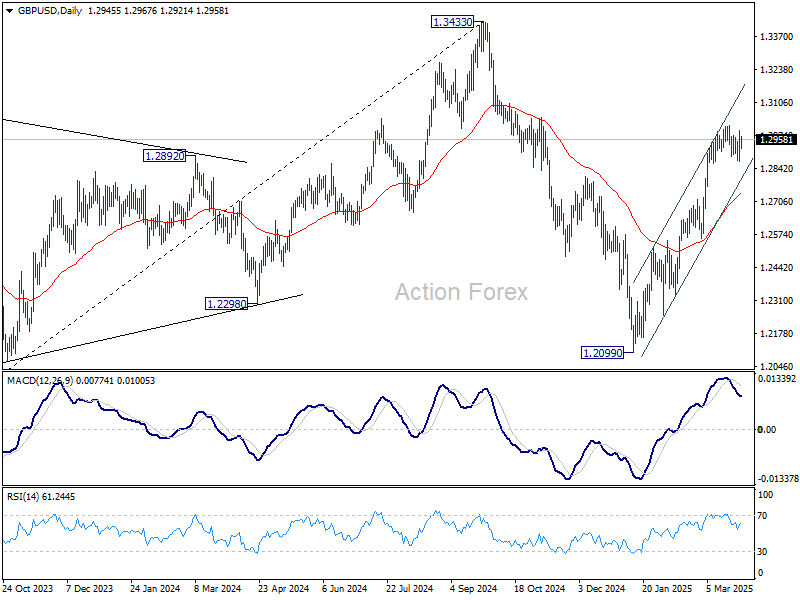

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2883; (P) 1.2937; (R1) 1.3004; More...

GBP/USD is still bounded in range below 1.3013 and intraday bias remains neutral. Consolidation from 1.3013 could extend. In case of another fall, downside should be contained by 38.2% retracement of 1.2248 to 1.3013 at 1.2721 to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

Markets Sluggish Despite Data Surprises, Caution Prevails Ahead of Tariff Unveil

The forex markets are ending the week in a sluggish and indecisive mood, despite a flurry of notable economic data releases. The highlight was the hotter-than-expected US core PCE inflation, which firmed expectations that Fed will hold rates steady in May, with market pricing now around 90% chance. However, expectations for a June rate cut remain relatively resilient at around 65%.

Yet, Dollar showed little appetite to capitalize on the data. It briefly lost ground against Euro and Sterling earlier in the session but quickly settled back into tight ranges. Similarly, stronger-than-expected Canadian GDP data failed to meaningfully support Loonie, which remains on the softer side for the day. Sterling, too, couldn’t hold onto gains despite upbeat retail sales figures, suggesting broader market hesitancy.

The overall restrained price action suggests that traders are simply not ready to make big moves ahead of next week's "reciprocal tariff" announcement from the US.

Looking at weekly performance, Australian Dollar leads the pack, while Canadian Dollar and British Pound follow. On the flip side, Japanese Yen remains the weakest, even after a brief bounce on Tokyo CPI figures, followed by Euro and New Zealand Dollar. Dollar and Swiss Franc are holding in the middle of the performance board.

In Europe, at the time of writing, FTSE is up 0.07%. DAX is down -0.83%. CAC is down -0.79%. UK 10-year yield is down -0.062 at 4.729. Germany 10-year yield is down -0.028 at 2.753. Earlier in Asia, Nikkei fell -1.80%. Hong Kong HSI fell -0.65%. China Shanghai SSE fell - 0.67%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield fell -0.038 to 1.554.

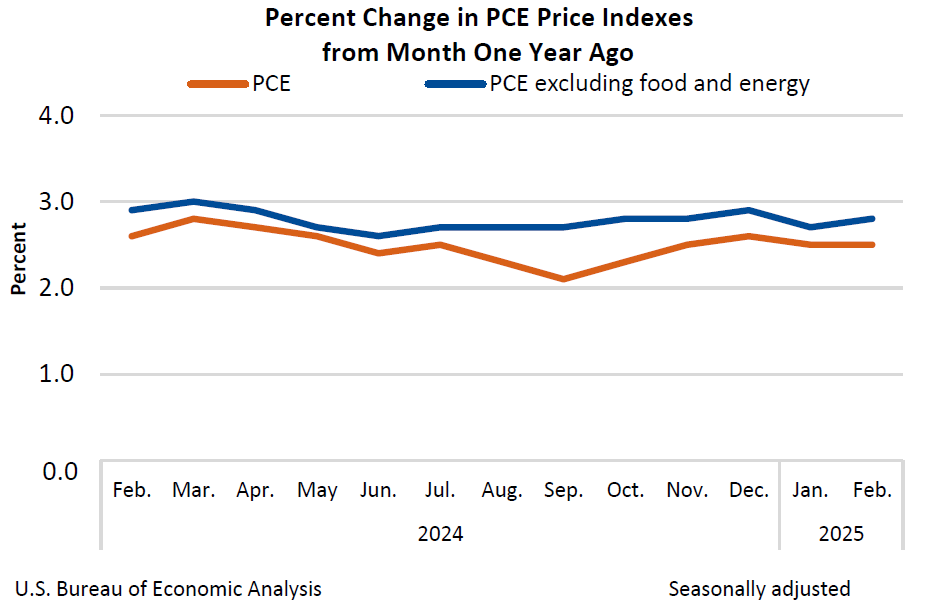

US core PCE accelerates to 2.8% in Feb, above expectations

US PCE inflation data for February came in largely in with notable surprises. Headline PCE rose 0.3% mom and held steady at 2.5% yoy, both matched expectations. However, core PCE, excluding food and energy, rose by 0.4% mom, slightly hotter than expected 0.3% mom. That pushed , pushing the annual core PCE rate up to 2.8% from 2.7%, also above forecasts.

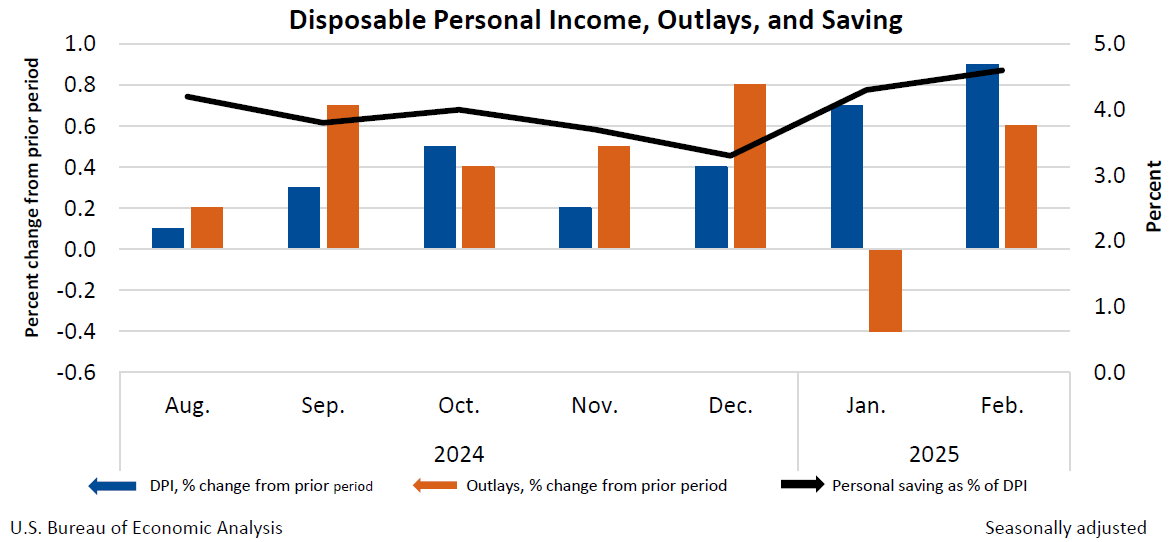

On the household side, personal income surged by 0.8% mom, significantly outpacing expectations of 0.4% mom, reflecting strong wage growth and robust labor market. But personal spending only rose 0.4% mom, slightly below forecasts of 0.5% mom, hinting at a more measured pace of consumption.

Canadian GDP grows 0.4% mom in Jan, but Feb flatline tempers momentum

Canada's GDP expanded by 0.4% mom in January, outpacing expectations of a 0.3% mom gain. Growth was broad-based, with 13 of 20 sectors contributing.

Goods-producing industries led the charge, rising 1.1% mom, the strongest monthly gain since October 2021, as all major components saw expansion. Services-producing industries posted a more modest 0.1% mom increase.

However, early estimates for February point to a flat reading, suggesting a pause in momentum. Strength in manufacturing and financial services was offset by pullbacks in real estate, oil and gas, and retail trade.

Swiss KOF rises to 103.9, robust economic outlook

Switzerland's KOF Economic Barometer rose to 103.9 in March, beating expectations of 102.6 and up from revised 102.6 in February. The index has remained above its medium-term average since the start of the year, reinforcing the view that the Swiss economy "remains robust".

KOF noted that improvements were broad-based, with stronger signals coming from manufacturing, services, and construction. Private consumption indicators also showed improvement while foreign demand remains unchanged.

UK retail rales rises 1% mom in Feb with broad-based gains

UK retail sales volumes jumped 1.0% mom in February, far surpassing market expectations for -0.3% mom decline.

The gain was driven by strong performances across all non-food store categories, including department stores, clothing, and household goods, suggesting consumers were more willing to spend on discretionary items. The only notable drag came from supermarkets, where sales volumes dipped slightly following a solid increase in January.

Looking at the broader trend, sales volumes rose 0.3% in the three months to February compared to the previous three-month period, and were up 2.0% from the same period a year earlier.

German Gfk consumer sentiment improves marginally to -24.5

Germany’s GfK Consumer Sentiment for April ticked up slightly from -24.6 to -24.5, falling short of expectations at -22.2.

According to Rolf Bürkl of the NIM, the minor improvement may reflect "lessened pessimism" following recent elections and the hope for a stable new government. However, willingness to save continues to signal significant uncertainty among German households.

Bürkl emphasized that "fast formation of a government and the early adoption" could play a key role in boosting consumer confidence and spending ahead.

Tokyo CPI core rises to 2.4%, driven by soaring food and rent prices

In Japan, Tokyo’s CPI core, which excludes fresh food, rose from 2.2% yoy to 2.4% yoy in March, surpassing expectations of 2.2% yoy. Even more notable was the rise in the core, core measure, which strips out both food and energy—climbing from 1.9% yoy to 2.2% yoy, signaling broader-based inflation. Headline inflation also ticked higher to 2.9% yoy from 2.8% yoy.

The key driver behind the spike was food prices, which surged 5.6% yoy, the fastest pace since January 2024. A standout was the massive 92.4% yoy jump in rice prices, the steepest rise since 1976.

Adding to the inflationary pressure was the services sector, where prices rose 0.8% yoy, up from 0.6% yoy in February. Rent prices, a key component, increased by 1.1% yoy, the sharpest rise since 1994.

BoJ opinions highlight tariff risks, but path to further hikes still intact

The Summary of Opinions from BoJ’s March monetary policy meeting revealed growing concerns over the fallout from US trade policy, particularly the risk that new tariffs could negatively impact Japan’s real economy.

One board member warned that downside risks from the US have “rapidly heightened". I f tariff issues worsen, it could have a "negative impact" on Japan's real economy. BoJ should be “particularly cautious” when considering further interest rate hikes if trade tensions escalate.

Other members echoed similar concerns, citing elevated uncertainty from tariff threats, global supply chain disruptions, and stiff competition from low-priced Chinese products.

The tone suggests policymakers are carefully monitoring how these factors affect inflation expectations, wage growth, and investment—particularly among SMEs.

A separate opinion suggested that as underlying CPI inflation edges closer to the 2% target, BoJ should prepare to shift from accommodative to "neutral" policy.

Overall, BoJ still sees a path toward rate normalization—contingent on its inflation outlook materializing—but recent developments in global trade and domestic firm performance will dictate the pace and timing of the next move.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2883; (P) 1.2937; (R1) 1.3004; More...

GBP/USD is still bounded in range below 1.3013 and intraday bias remains neutral. Consolidation from 1.3013 could extend. In case of another fall, downside should be contained by 38.2% retracement of 1.2248 to 1.3013 at 1.2721 to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

US core PCE accelerates to 2.8% in Feb, above expectations

US PCE inflation data for February came in largely in with notable surprises. Headline PCE rose 0.3% mom and held steady at 2.5% yoy, both matched expectations. However, core PCE, excluding food and energy, rose by 0.4% mom, slightly hotter than expected 0.3% mom. That pushed , pushing the annual core PCE rate up to 2.8% from 2.7%, also above forecasts.

On the household side, personal income surged by 0.8% mom, significantly outpacing expectations of 0.4% mom, reflecting strong wage growth and robust labor market. But personal spending only rose 0.4% mom, slightly below forecasts of 0.5% mom, hinting at a more measured pace of consumption.

Canadian GDP grows 0.4% mom in Jan, but Feb flatline tempers momentum

Canada's GDP expanded by 0.4% mom in January, outpacing expectations of a 0.3% mom gain. Growth was broad-based, with 13 of 20 sectors contributing.

Goods-producing industries led the charge, rising 1.1% mom, the strongest monthly gain since October 2021, as all major components saw expansion. Services-producing industries posted a more modest 0.1% mom increase.

However, early estimates for February point to a flat reading, suggesting a pause in momentum. Strength in manufacturing and financial services was offset by pullbacks in real estate, oil and gas, and retail trade.

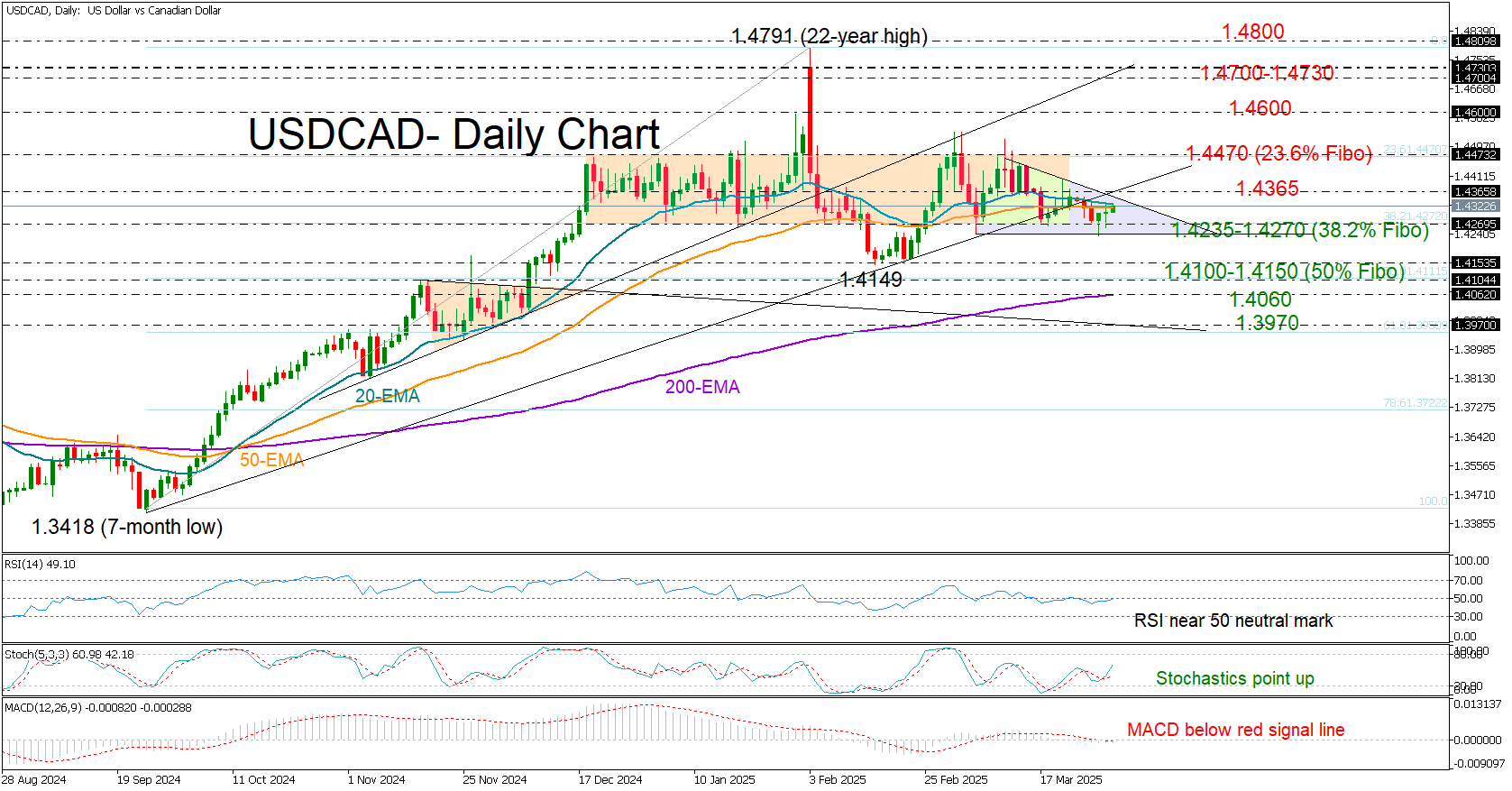

USD/CAD Indecisive Within Neutral Zone

- USD/CAD maintains sideways movement above 1.4270 support.

- Trend signals deteriorate; a break above 1.4635 could provide relief.

USDCAD extended its four-month sideways trajectory above the 1.4270 base for another week as the US tariffs deadline approached on April 2 and the Fed chairman reaffirmed economic stability.

Trend signals remain fragile. The pair slipped below the support trendline from September 2024 and remains capped below the 20- and 50-day exponential moving averages (EMAs) at 1.4330. Additionally, recent price action seems to be forming a descending triangle, which is usually a sign of a bearish breakout.

However, Wednesday’s green hammer candlestick and the rising stochastic oscillator suggest upside potential hasn’t vanished. The 20-day EMA is also holding resilient above the 50-day EMA for the fifth consecutive month. Still, bulls must reclaim 1.4365 and then break successfully above 1.4470 to exit the neutral zone.

A climb above 1.4470 could initially pause near 1.4600. If the bulls sustain power, a tougher obstacle could emerge within the 1.4700-1.4730 territory before the 1.4800 mark comes into play.

Conversely, a close below 1.4235-1.4270 may activate fresh selling orders toward 1.4100-1.4150. A drop past the 200-day EMA at 1.4065 could push prices toward 1.3970, aligning with the 61.8% Fibonacci retracement of the September-February rally.

Overall, USDCAD remains in limbo. A break above 1.4365 or below 1.4235 could set the next direction.

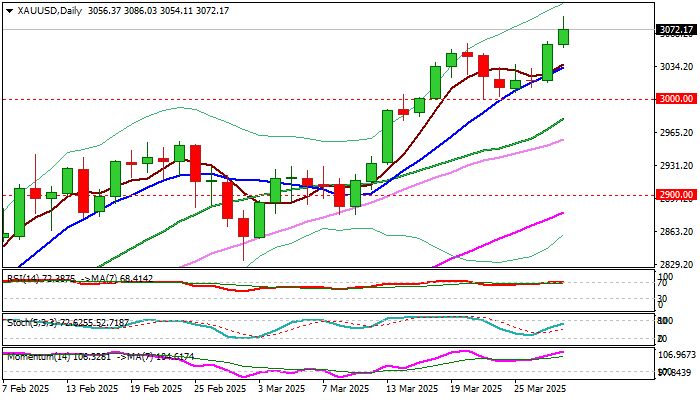

Gold Hits New Record High, on Track for Strong Weekly, Monthly and Quarterly Gains

Gold spiked to new record high ($3086) in early Friday trading, in extension of Thursday’s 1.2% advance.

The yellow metal is on track for the fourth consecutive weekly gain and also for the third straight bullish monthly close (over 7% up in March), with the price increasing by 17% in the first three months of 2025.

Gold price was lifted by rising safe have demand, driven by growing economic, and geopolitical uncertainty, signals or more rate cuts, as well as increased physical buying

The latest story with US reciprocal trade tariffs further fueled concerns of trade war escalation which could cause a colossal negative impact on global economy and further boost migration into safety.

Short term outlook is likely to remain very bullish, as there are no signs that situation in any of key fields would calm soon, but more likely to deteriorate further.

The notion is also supported by quick and easy break of $3000 milestone, where stronger headwinds were expected, due to significance of this psychological barrier, with fresh acceleration higher coming close to next round figure resistance at $3100.

Some easing could be anticipated here, due to week-end and month-end profit taking, though gold’s major drivers remain firmly in play, suggesting that dips are likely to be limited.

Technical picture is firmly bullish on daily chart, although stretched indicators warn that bulls may take a breather.

Previous top at $3057 offers immediate support, followed by rising 10DMA ($3033) where dips should ideally find a footstep and guard lower pivot at $3000 (former key barrier reverted to strong support).

Res: 3086; 3093; 3100; 3112.

Sup: 3057; 3033; 3012; 3000.