Sample Category Title

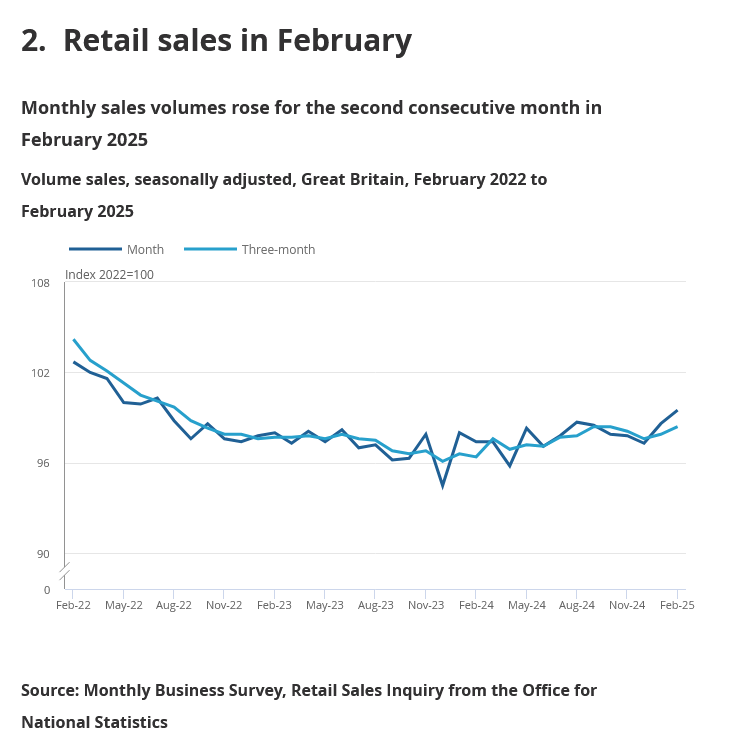

UK retail sales rise 1% mom in Feb with broad-based gains

UK retail sales volumes jumped 1.0% mom in February, far surpassing market expectations for -0.3% mom decline.

The gain was driven by strong performances across all non-food store categories, including department stores, clothing, and household goods, suggesting consumers were more willing to spend on discretionary items. The only notable drag came from supermarkets, where sales volumes dipped slightly following a solid increase in January.

Looking at the broader trend, sales volumes rose 0.3% in the three months to February compared to the previous three-month period, and were up 2.0% from the same period a year earlier.

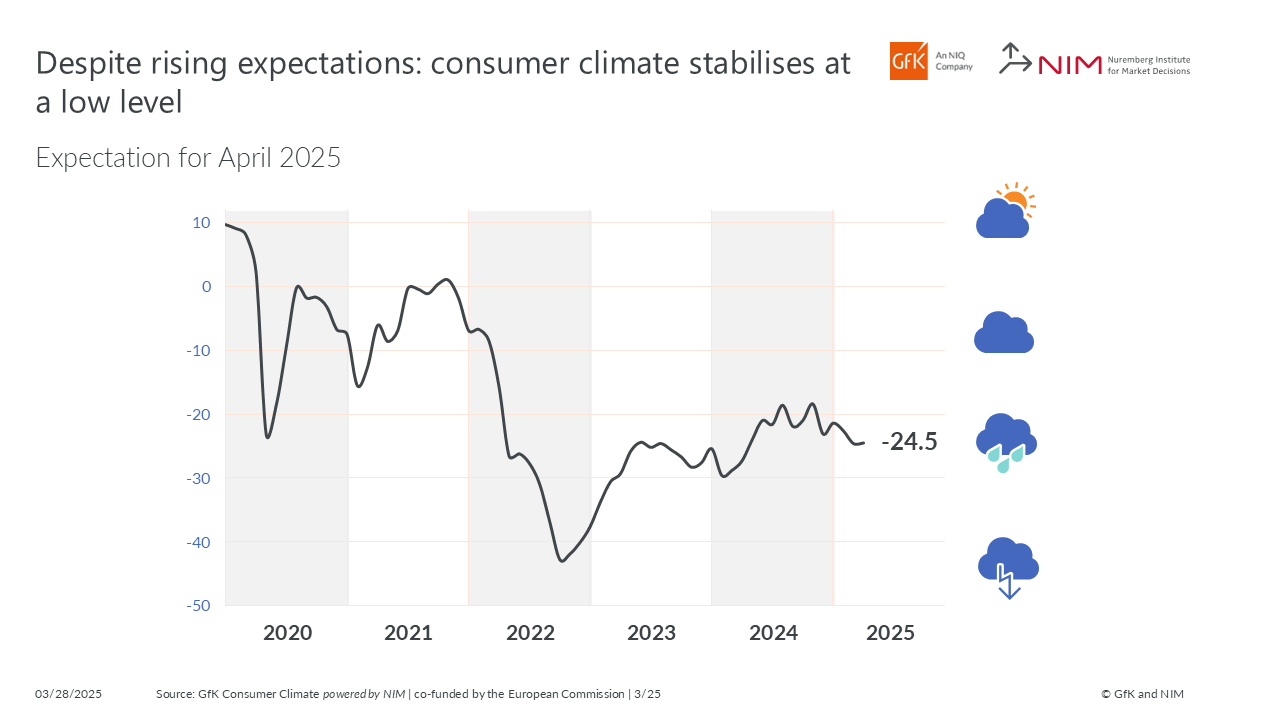

German Gfk consumer sentiment improves marginally to -24.5

Germany’s GfK Consumer Sentiment for April ticked up slightly from -24.6 to -24.5, falling short of expectations at -22.2.

According to Rolf Bürkl of the NIM, the minor improvement may reflect "lessened pessimism" following recent elections and the hope for a stable new government. However, willingness to save continues to signal significant uncertainty among German households.

Bürkl emphasized that "fast formation of a government and the early adoption" could play a key role in boosting consumer confidence and spending ahead.

Tariffs, Cars and CoreWeave IPO

Sentiment remains sour due to intensifying tariff talk. The carmakers around the world got hammered this week as the ones that produce their cars outside the US will cost 25% more if the levies go live – and nearly half of vehicles sold in the US are reportedly assembled elsewhere – and, the ones that are made in the US have at least 20% of their components coming from outside the US. Evercore ISI predicts that US car prices will likely increase by $3000-4000 on average while cars

Of course, the global ramifications are immense and the selloff is intense. GM lost more than 7% yesterday. The South Korean Kia Motors lost more than 7.5% from the peak of the week and the Japanese Honda lost more than 9% since the peak of the week. It is quite disquieting to see traditional carmakers lost that much of their value in a few hours. The European carmakers posted smaller losses because the tariff threats are already priced in since a while. iShares Stoxx 600 Automobiles & Parts ETF is down by almost 14% since the February peak, while the index saw a smaller pullback posterior to a remarkable rally on spending euphoria. Gold is unsurprisingly pushing higher into uncharted territories, and the overbought market conditions don’t matter when the geopolitical headlines are so aggressive. Investors buy gold each time they hear the word ‘tariff’.

And April 2nd – aka the Liberation Day – when the US is expected to announce its reciprocal tariffs is the next event to watch. It’s hard to be optimistic when we know that retaliation will emerge and uncertainties will continue with possible retaliation.

Retaliation and the extent of retaliation will determine the next direction of the US dollar. Trump naturally wants to limit response to his tariffs – he threatened Europe and Canada that he would impose higher tariffs if they teamed up to counter the US pressure. But the US dollar gave back a part of the recent gains yesterday hinting that the market favours the scenario of retaliation. Retaliation would hit the US exports in return, hit the US economic growth, boost inflation, hence boost the stagflation risks. The Federal Reserve (Fed) could step in and give support, but the tariffs – and the tariff uncertainty – will inevitably pressure earnings, impact capex plans and could further hurt the US equities before a potential Fed-backed relief.

Elsewhere, the Stoxx 600 has consumed the energy from government spending plans and is now facing earnings pressure from tariffs, as well. The Stoxx 600 index tipped a toe below its ytd ascending channel base yesterday and could well extend a correction into 520 – that would be another 4.5% retreat. The S&P500 could retest the 5500 level in the next wave of selloff, and Nasdaq 100 could break below the 19000 level in case of a worsening risk selloff. The rapid correction of the US Big Tech valuations has already caused up to 20% selloff from the November peak. Even encouraging and positive news from the tech and AI are unable to find a good spot on the international scene to turn the tables around.

Good luck, CoreWeave

So, it is in this difficult market setup that CoreWeave, the Nvidia-backed cloud computing specialized in AI, will start trading today on the Nasdaq stock exchange. The timing of the IPO is clearly not ideal as the AI-related stocks have experienced a significant pullback in their valuations on the back of various factors including tariff uncertainty, the rising Chinese competition, but also on rising fears of oversupply in AI versus the demand that didn’t grow as fast as previously forecasted. Investors have been sensitive to the idea that the AI spending went ahead of itself and demand is not following.

CoreWeave had to lower its IPO ambitions yesterday and pulled its expected valuation lower due to a weaker-than-expected reception during its roadshow. The company was planning to sell 49 million shares priced between $47 and $55 each, aiming to raise up to $2.7 billion and achieve a valuation of approximately $32 billion. But it will finally settle with a sale of 37.5 mio shares at $40 each and aim to raise around $1.5bn. That would value the company to $23bn instead of $32bn.

To justify the revised valuation, the company’s revenue should grow by more than 25% annually each year for a decade. That’s comparable to growth that Microsoft’s and Amazon’s data centers printed over the past years, but that growth also left investors with a doubt of oversupply.

As per Coreweave, the company printed an incredible performance last year; their revenue rose more than 700% to above $1.9bn, but reported a net loss of around $860mio last year. The huge debt that the company accumulated – almost $13bn over the past two years – should be partly paid back in the next years. As such, the way investors will welcome the company will tell a lot about whether they are still focused on impressive growth potential of AI enablers, or they are more concerned about slowing growth to avoid oversupply.

Inflation Releases Conclude the Week

In focus today

In the US, The Fed's preferred measure of inflation, the Personal Consumption Expenditures (PCE), will be released in February. In the afternoon, University of Michigan's revised March consumer sentiment survey is also due for release. While the revisions are not usually in focus for markets, we will pay more attention to consumer sentiment given the political uncertainty.

In the euro area, we will closely follow the March inflation data from Spain and France, that we get ahead of the euro area aggregate on Tuesday next week. We expect the euro area HICP inflation to decline from 2.3% y/y to 2.1% y/y due to energy and services inflation. We forecast core inflation to decline to 2.4% y/y from 2.6% y/y.

In Sweden, a new wage agreement might be announced any time from today, ahead of the 31 March deadline, due to significant pressure from expiring contracts. Last week's proposal included a three-year deal at 7.7%, with higher initial wage agreements and a decreasing profile - lower than expected and potentially indicating downward risks on wage forecasts. Additionally, Swedish retail sales for February will be published, with sales showing strong momentum last year, though January's decline and low consumer confidence could indicate downward trends continues into February.

In China, the official PMI for both manufacturing as well as services will be released for March early Monday. Consensus is a small increase in both indices, but we see a good chance of an even bigger increase based on a strong pick-up in the high-frequency Yicai index as well as the Emerging Industries PMI for March, which has already been released. A pick-up in metal prices in March also points to improvement in the manufacturing sector.

Economic and market news

What happened overnight

In the US, Susan Collins from Boston Federal Reserve said that it was inevitable that inflation would rise on the back of the tariffs, but unclear how long it would last, and that rates should be on hold. Fed's Barkin said the businesses could be "on hold" given the policy uncertainty and the Fed should be on hold as well.

In commodities space, gold prices have surged to $3,076.79 an ounce, as tariff plans from the US, together with fiscal policy, geopolitics and growth slowdown fuels uncertainty leading investors to adopt a risk-off approach seeking save havens.

In Japan, Tokyo CPI numbers for March were released. The print was on the strong side, with core CPI (CPI excl. fresh food) ticking up to 2.4% y/y (cons: 2.2%, prior: 2.2%), fueled by higher food prices. The release is typically a good indicator of the nationwide CPI measure, which is scheduled for release in the coming weeks. Overall, the reading supports the case of further rate hikes from the BoJ. We pencil in two 25bp rate hikes from the BoJ for the remainder of the year, with the next likely in July.

What happened yesterday

In the US, the final release of Q4 GDP 2.4% (cons: 2.3%) was revised slightly upwards, primarily due to a less negative contribution from inventories. Weekly jobless claims remained steady.

Yesterday's announcement of 25% car tariffs has created division among US trading partners. Notably in the opposing camp, Canadian Prime Minister, Carney, has declared the longstanding Canada-US relationship as over, advocating for a renegotiation of the trade agreement. Moreover, President of the European Commission, Von der Leyen, has announced negotiations of new measures to safeguard the economic interests of the bloc.

In the euro area, credit growth continued to increase in February in the euro area. Credit growth to households increased to 1.5% from 1.3% in January and for NFCs to 2.2% from 2.0%. Hence, the lower monetary policy rates are transmitting into the economy, which supports the arguments of the hawk camp in the ECB. Yet, the absolute revel of restrictiveness of monetary policy is better estimated by the "growth impulse" which measures the momentum in credit growth and is often a better predicter of GDP and the annual growth rate of credit. At a level of 1.17% of GDP, the credit impulse remains still quite low in a historical perspective when considering the 150bp cuts the ECB has delivered so far. Hence, we see this as an indication that monetary policy is still restrictive, also as the impulse has remained flat for the past year.

Regarding yesterday's ECB speeches, signals were a mixed bag, as widely expected. We note that members of the Governing Council have repeatedly flagged the topside risk to inflation from tariffs rather the dampening effect on growth. To us, this highlights a gradual shift in how the ECB views the balance of risk.

In Norway, the policy rate was kept unchanged at 4.50% by Norges Bank (NB). Importantly, NB maintained its easing bias with the rate path indicating two rate cuts in 2025 and a 25% probability of a cut in June. In light of the unchanged decision, we revise our NB call to two 2025 rate cuts (September and December), three cuts in 2026 and a final cut in 2027 bringing the sight deposit rate to 3.00%. We highlight the importance of the ongoing central wage negotiations. An outcome below 4.5% would open the door for a June cut. For a more in depth interpretation.

Equities: Equities were lower, but not as bad as one might think after the news on auto tariffs. S&P 500 -0.3% and Stoxx 600 index -0.5%. US stocks have outperformed European equities with two percentage points the last two weeks. We attribute this to oversold conditions and will not try to chase it. We recommend focusing on the fundamentals that keep favouring Europe. Derisking still taking place below the surface, with staples and health care outperforming while tech (Nvidia), industrials (cars) and energy lower. Pricing power is key when it comes to the new tariffs, hence Volkswagen only down 1.5% while Chrysler-parent Stellantis slumped 4.2% and BMW 2.5%. French automotive supplier Valeo sank 8%, after saying it could not absorb recent tariffs and would have to raise prices. On the other end, European real estate stocks 2% higher, on European yields dipping following Trump's auto tariff announcement. US futures are marginally higher this morning.

FI&FX: EUR/USD continues to hold around 1.08 and we expect further consolidation between 1.08-1.09, with predominately upside risks. EUR rates were little changed through yesterday's session, while EGB curves saw a bullish steepening. In a highly awaited monetary policy announcement, Norges Bank yesterday decided to keep rates unchanged at 4.50%, however they maintain their easing bias with the rate path indicating two cuts in 2025. Broad SEK remains supported, although we see near-term topside risks mounting in major SEK-crosses.

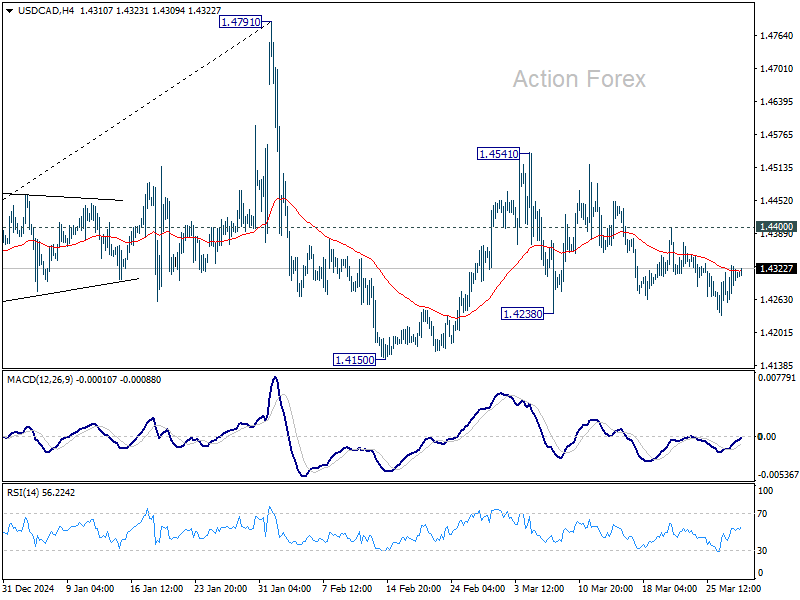

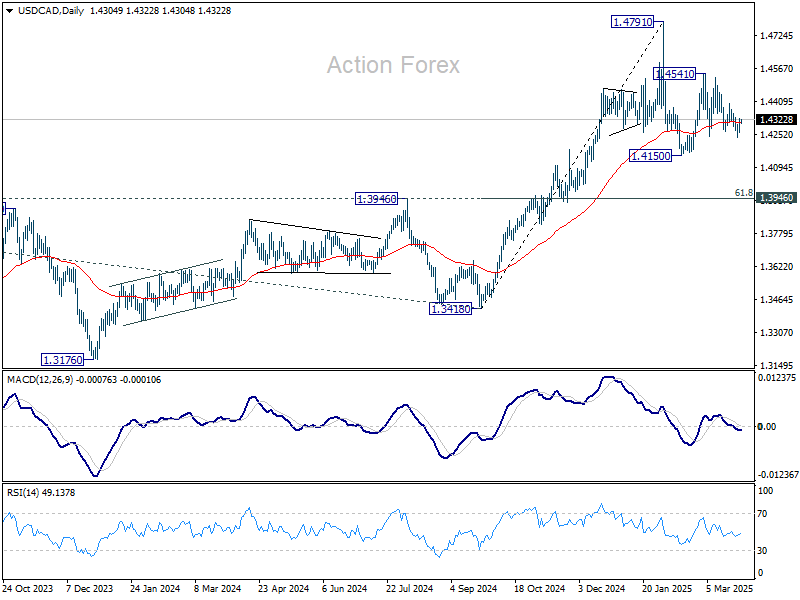

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4267; (P) 1.4298; (R1) 1.4336; More...

Intraday bias in USD/CAD is turned neutral again as it recovered ahead of 1.4238 support. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has already started the third leg. Deeper decline should be seen to 1.4150 support next. On the upside, though, break of 1.4400 resistance will argue that rebound from 1.4150 is possibly still in progress, and target 1.4541 resistance and possibly above.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

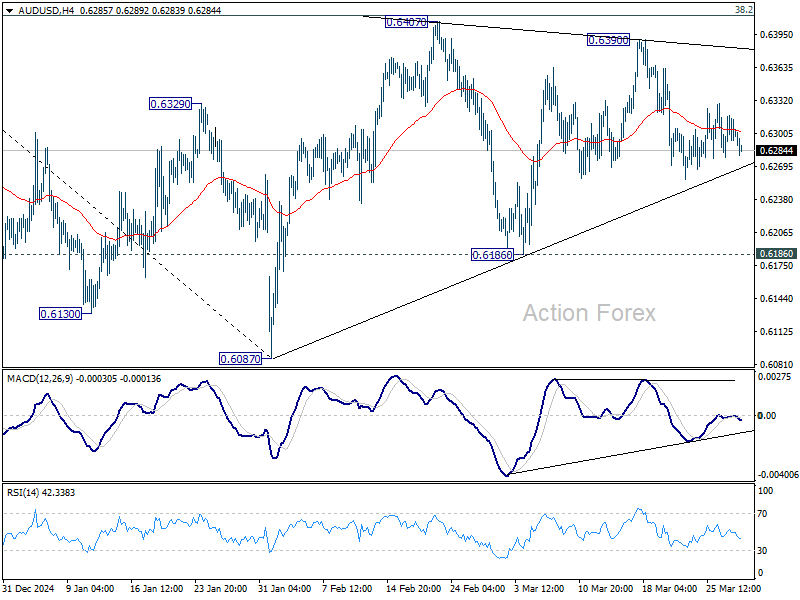

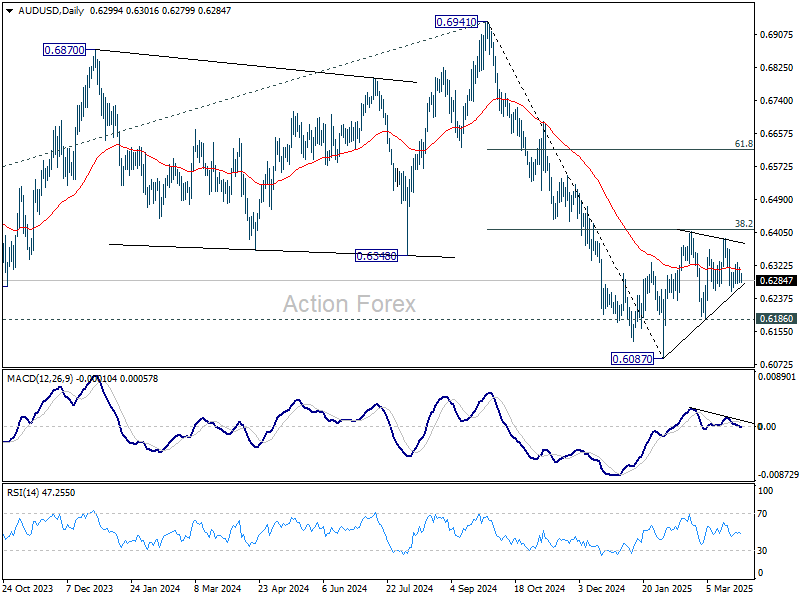

AUD/USD Daily Report

Daily Pivots: (S1) 0.6283; (P) 0.6301; (R1) 0.6322; More...

Intraday bias in AUD/USD remains neutral as consolidation from 0.6087 is still extending. On the downside, firm break of near term trend line support (now at 0.6270) will argue that the pattern has already completed. Intraday bias will be back on the downside for 0.6186 support. Further break there will solidify this bearish case and target 0.6087 low. For now, in case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6467) holds.

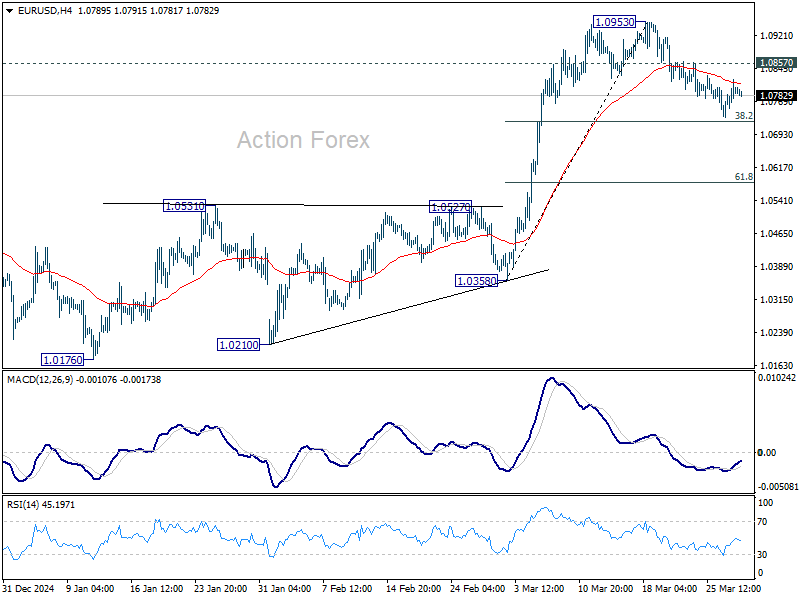

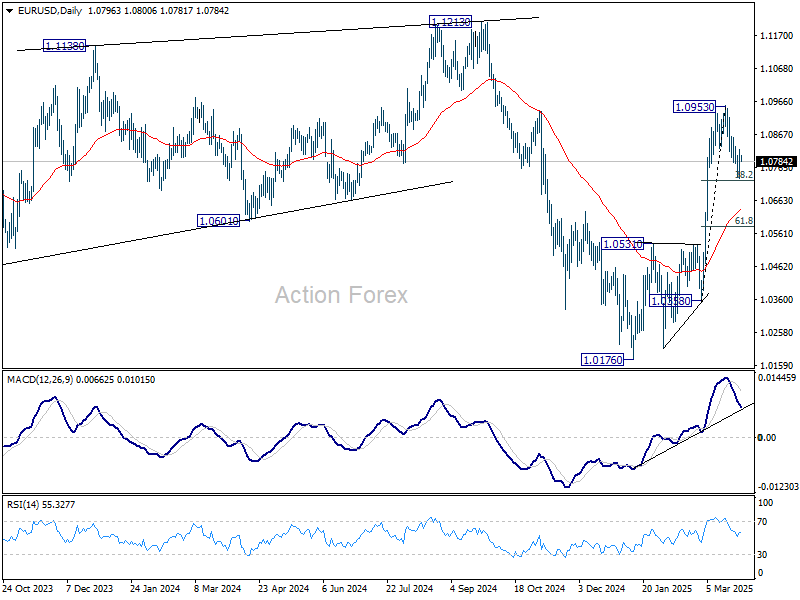

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0786; (R1) 1.0837; More...

Intraday bias in EUR/USD remains neutral for the moment. Strong support is expected from 38.2% retracement of 1.0358 to 1.0953 at 1.0726 to completion the correction from 1.0953. On the upside, break of 1.0857 will bring retest of 1.0953 first. Firm break there will resume larger rise from 1.0176. However, sustained break of 1.0726 will bring deeper correction to 55 D EMA (now at 1.0637).

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

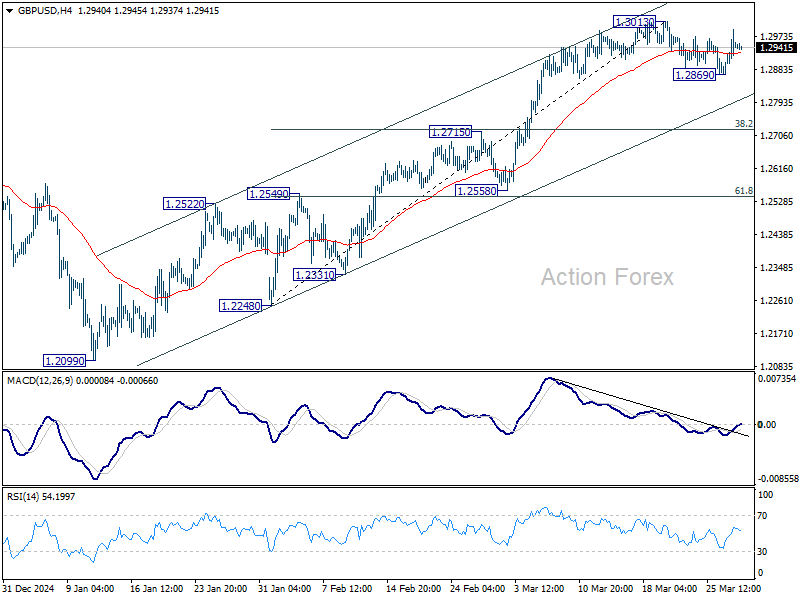

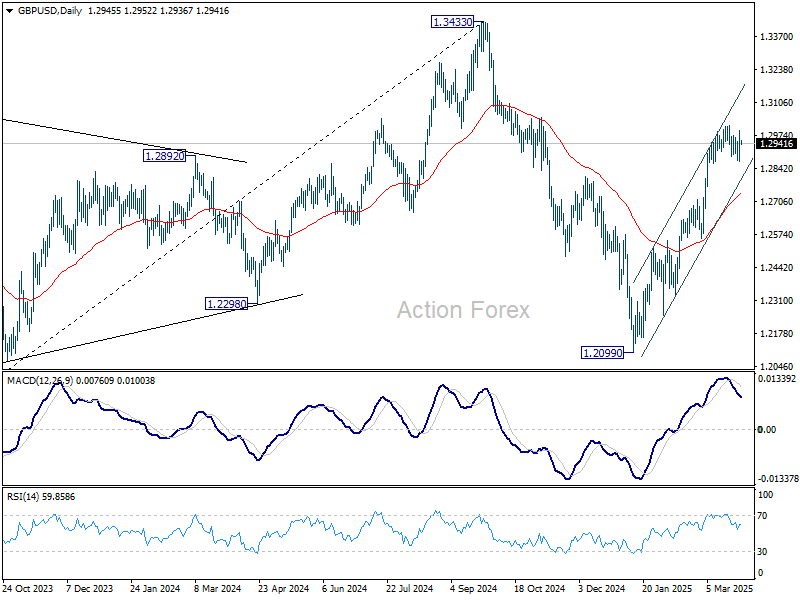

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2883; (P) 1.2937; (R1) 1.3004; More...

Intraday bias in GBP/USD remains neutral for the moment. Consolidation from 1.3013 could still extend. In case of another fall, downside should be contained by 38.2% retracement of 1.2248 to 1.3013 at 1.2721 to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high).

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

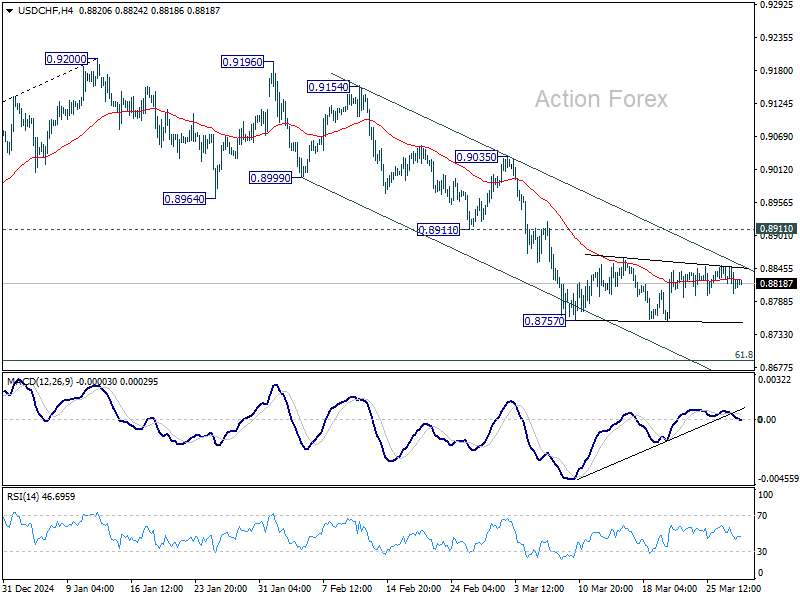

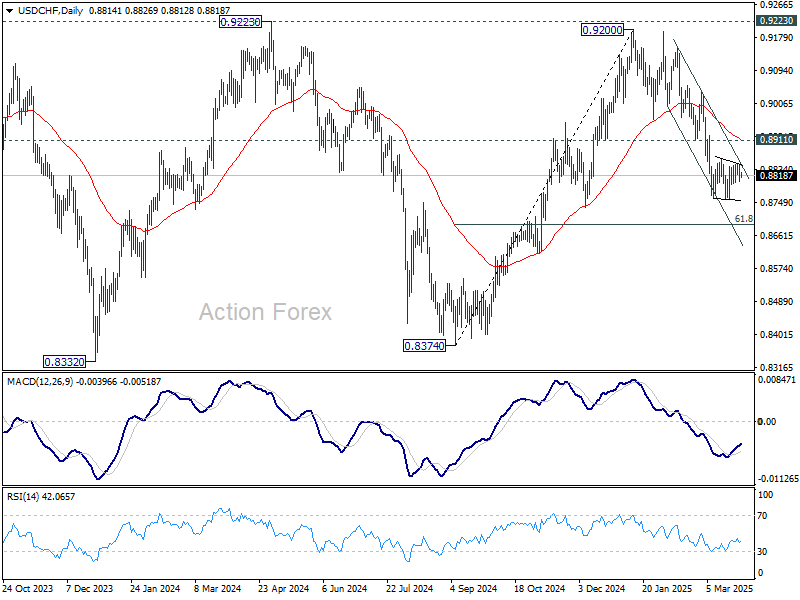

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8818; (P) 0.8834; (R1) 0.8855; More…

No change in USD/CHF's outlook and intraday bias remains neutral. Consolidation could extend above 0.8757. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

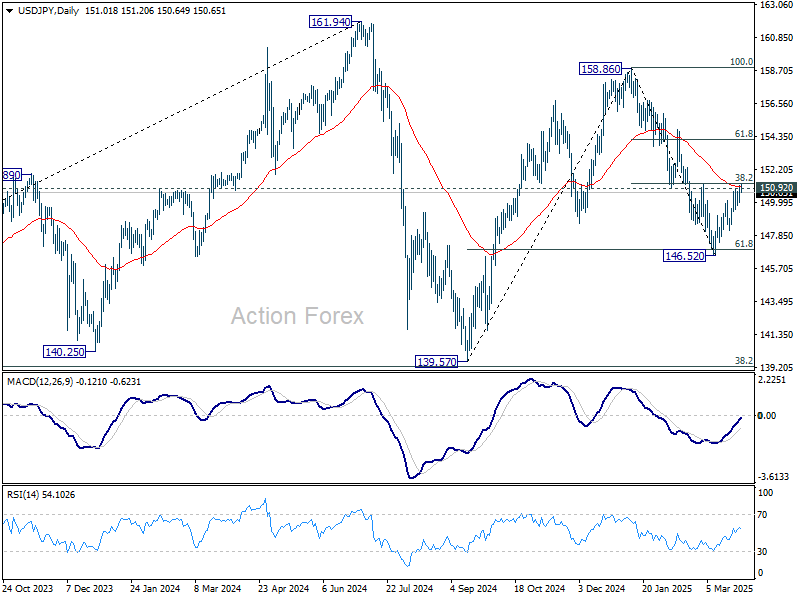

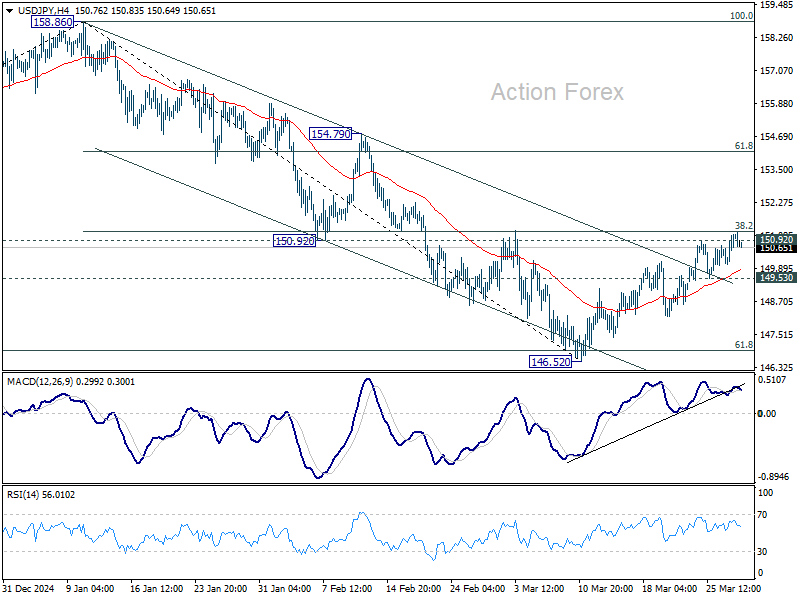

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.35; (P) 150.75; (R1) 151.45; More...

No change in USD/JPY's outlook and intraday bias remains neutral. Strong resistance is still expected from 150.92 to complete the corrective recovery from 146.52. On the downside break of 149.53 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. However, firm break of 150.92 will argue that fall from 158.86 has completed and turn bias back to the upside for 154.79 resistance next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.