Sample Category Title

GBPCAD Finds Support in Blue Box, Buyers Achieve First Target

Hello traders. Welcome to another ‘blue box’ post where we discuss the recent trade setup that Elliottwave-forecast members traded. In this post, the spotlight will be on the GBPCAD currency pair.

In the long term, GBPCAD is developing as a bearish market within a proposed diagonal structure. The Supercycle degree wave (I) was completed in May 2010, followed by a bounce for wave (II), which ended in November 2015. From that point, wave (III) moved lower and completed in October 2022. Notably, waves (I), (II), and (III) are all 3/7 swing structures, supporting our proposed long-term diagonal structure for members. Diagonals are often composed of five sub-waves, with each wave subdivided into three waves.

Currently, the rally from October 2022, where wave (III) ended, is unfolding as another three-swing sequence. Therefore, we can classify this rally as wave (IV). However, it appears that wave (IV) is an incomplete corrective sequence. Based on projections, wave (IV) could extend to at least 1.96 – 2.08.

We prefer trading along the path of an incomplete sequence. With this in mind, we advised members to buy pullbacks in 3, 7, or 11 swings, while keeping invalidation levels intact at each stage. Let’s now discuss the latest setup we shared with members.

GBPCAD Elliott Wave Trade Setup – 27th March 2025

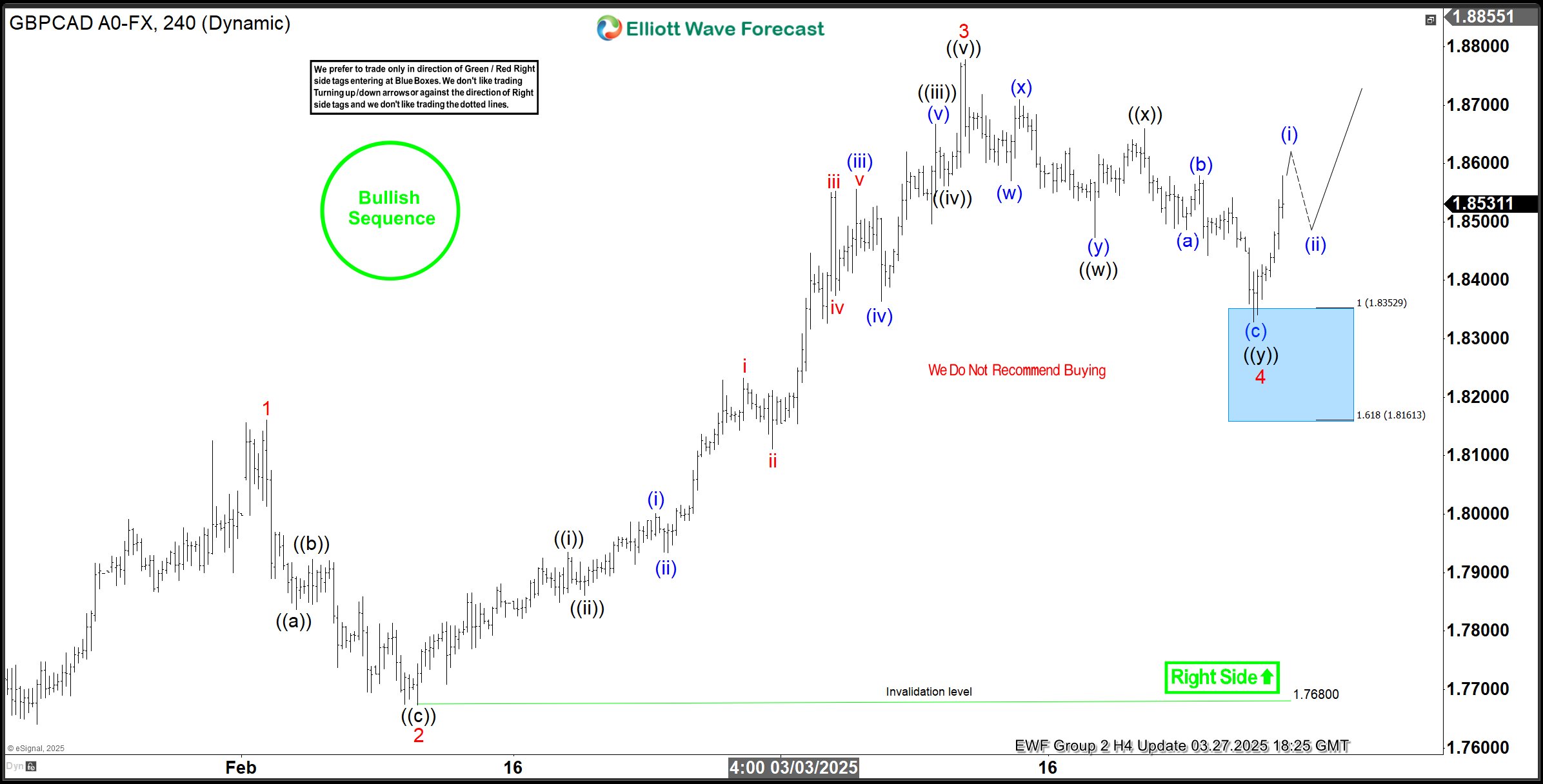

At the January 2025 low, wave ((2)) of (1) of c of (IV) was completed. From this low, an impulsive sequence began, forming wave (1) of ((3)). Within wave (1) of ((3)), a pullback for wave 4 of (1) started in March 2025 after the pair reached its highest price since July 2016.

We planned to buy from the extreme of wave 4 of (1), provided it completed a 3-swing or 7-swing pullback—also known as zigzag and double zigzag structures, respectively. As the pullback for wave 4 of (1) approached its extreme, we shared the H4 chart below with members

The chart above highlights the Blue Box where we expected members to enter long positions. We anticipated that wave 4 would complete in this zone, providing support for wave 5 of (1).

If the price rallied as expected, we advised members to take partial profit at 1.8530 and move the remaining position to breakeven. This strategy allowed for preparation in case wave 4 developed into a double correction. However, if an impulsive move emerged for wave 5, we planned to take the second profit at 1.9050.

GBPCAD Elliott Wave Trade Setup – 27th March 2025

Later, on March 27, 2025, GBPCAD rallied from the Blue Box, as anticipated. The price surpassed the first target at 1.8530, allowing traders to take partial profit and adjust the stop on the remaining position to breakeven.

With this risk-free setup, traders could shift their focus to other opportunities while still anticipating further profits on this pair. This was a high-confidence setup, carefully analyzed and executed. This approach exemplifies how we apply Elliott Wave theory in our service.

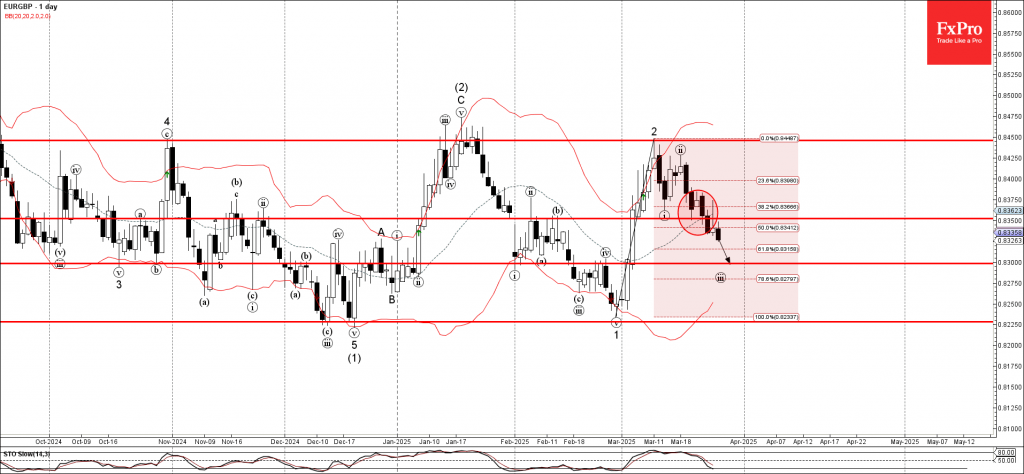

EURGBP Wave Analysis

EURGBP: ⬇️ Sell

- EURGBP broke support area

- Likely to fall to support level 0.8300

EURGBP currency pair recently broke the support area between the key support level 0.8350 (which has been reversing the price from the start of March) and the 38.2% Fibonacci correction of the upward wave 2 from the end of February.

The breakout of this support area accelerated the active impulse wave iii of the higher impulse waves 3 and (3).

Given the strongly bullish sterling sentiment, EURGBP currency pair can be expected to fall to the next support level 0.8300.

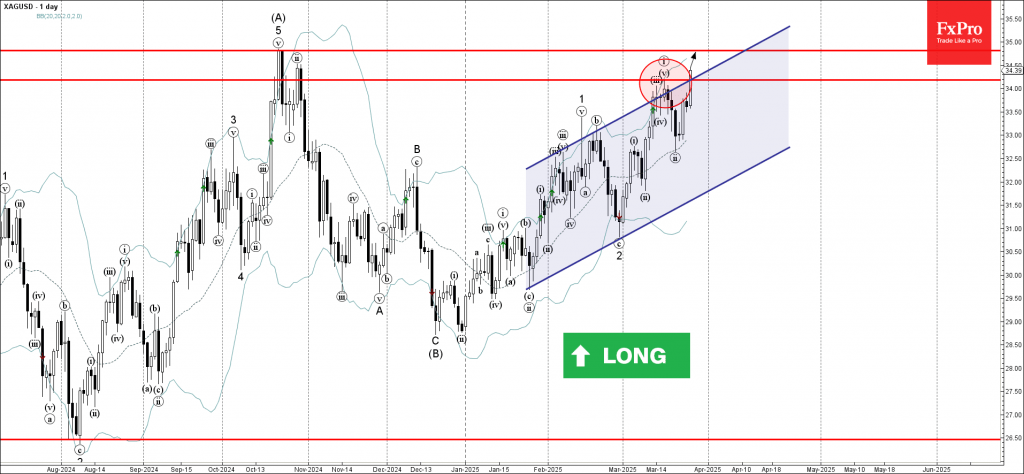

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver broke resistance area

- Likely to rise to resistance level 34.80

Silver recently broke the resistance area between the key resistance level 34.20 (top of the previous impulse wave i) and the resistance trendline of the daily up channel from January.

The breakout of this resistance area accelerated the active impulse wave iii of the higher impulse waves 3 and (C).

Given the clear daily uptrend, Silver can be expected to rise to the next resistance level 34.80 (former multi-month high from October) – from where the downward correction is likely.

GBP/JPY Forecast: Triangle Breakout Signals Potential Bullish Rally to 2007 Highs

- GBP/JPY has been trending upward since February 7, fueled by Yen weakness and GBP strength.

- A symmetrical triangle pattern on the daily chart suggests a potential breakout and bullish rally, possibly to 222.00.

- Key support levels are 194.00, 193.50, 192.00, while resistance levels are 197.50, 198.96, 200.00.

The GBP/JPY is one of the more volatile currency pairs and usually provides ample movement and potential opportunities.

In the past few weeks, Yen weakness and resurgent GBP have led the pair higher since bottoming out on February 7 at around the 187.00 handle.

This came about despite increased hopes of further Bank of Japan (BoJ) rate hikes later this year. Bank of Japan (BoJ) Governor Kazuo Ueda said on Wednesday that the central bank will keep raising interest rates if the economy and prices grow as expected. Additionally, strong wage increases for the third year in a row are fueling hopes for more rate hikes by the BoJ.

Meanwhile developments across the pond in the UK suggest further rate cuts may be in offing after the Office for National Statistics reported on Wednesday that the UK's main inflation rate (CPI) rose 2.8% in February compared to a year ago, down from 3.0% in January. This was lower than the 2.9% economists had predicted. Core inflation, which removes changes in food and energy prices, increased by 3.5% in February, less than the 3.7% seen in January and below the expected 3.6%.

All in all its supposed to read a weaker GBP as rate cuts are expected and JPY strength as rate hikes are planned. However this is not how price action has developed over the past few weeks.

Price action and chart patterns are hinting at a major bullish rally for GBP/JPY so let us see what the charts look like.

Technical Analysis - GBP/JPY

GBP/JPY Daily Chart, March 27, 2025

Source TradingView

From a technical standpoint, GBP/JPY on a daily timeframe has staircased its way higher since February 7.

The pair has been trading in a massive symmetrical triangle pattern with a breakout today looking likely.

Trading triangle patterns requires patience, however there is definitely a setup brewing.

A daily candle close above the triangle pattern will be the signal for triangle pattern setup based on the rules. However given the fickle nature of markets in recent times, there is a possibility of a short-term pullback and for that we need to take a look at the H4 chart for potential areas of interest to pay attention to.

GBP/USD Four Hour Chart, March 27, 2025

Source TradingView

Dropping down to a four-hour chart and we have just printed fresh highs which could lead to a potential pullback.

However, there is also the possibility that the pair rises further before any pullback comes to fruition.

The period 14 RSI is also just short of being in overbought territory.

OAU-PRS-236-MarketPulse-variant1-Square

A pullback to the March 26 low around the 193.50 handle may provide bulls with an even better entry following the triangle breakout. If this level fails to hold, a deeper pullback toward the swing low at 192 may be in the offing.

Either way if the triangle pattern does play out, the potential move could take GBP/JPY to highs of around 222.00, last reached before the global financial crisis in December 2007.

A mega move if there ever was one.

Support

- 194.00

- 193.50

- 192.00

- 190.00

Resistance

- 197.50

- 198.96

- 200.00

- 201.65

Brent Oil Market Update: Tariffs, Supply Concerns, and Price Analysis

- Brent oil prices rebounded but face headwinds from potential US tariffs and concerns about slowing US oil production.

- Market participants are closely watching global demand, potential US-Iran tensions, and the impact of trade wars on oil prices.

- Brent crude broke out of its previous range and above the descending trendline but significant resistance lies ahead.

Brent crude prices rebounded from a daily low of 73.00 to trade at 73.77 but looks likely to finish the day marginally in the red. Traders looked at shrinking crude supplies and the potential impact of new U.S. tariffs on the global economy.

Yesterday Oil prices rose 1% to its highest point since February. President Trump's announcements of tariffs on the automobile industry has ratcheted up trade war concerns.

This coupled with some concerns over supply are keeping oil prices supported for now. On Tuesday President Trump imposed new 25% tariffs on potential buyers of Venezuelan crude. The move has already led to reports that India's Reliance Industries, which runs the world's largest refining complex, will stop importing oil from Venezuela after the tariff announcement, sources said on Wednesday.

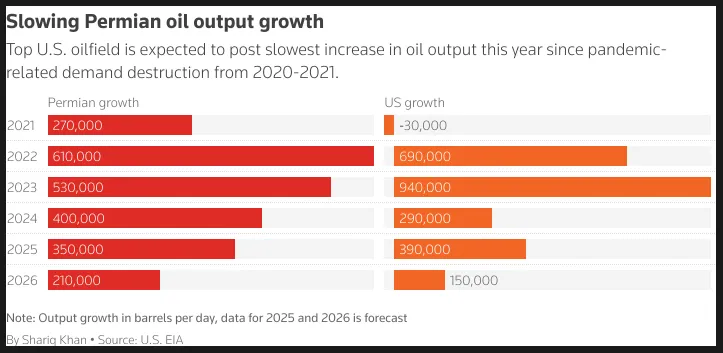

Another factor that could be adding to supply concerns comes from the US as President Trump looked to lessen the red tape to allow Oil producers to pump more oil. However, the challenges facing US oil producers are geological in nature as the country's top oilfield ages producing more water and gas, less oil, and could be close to reaching peak output.

Permian Basin Facing Challenges

The Permian Basin was the heart of the U.S. shale boom, helping the nation become the world’s largest oil producer and challenging OPEC’s market share. It now produces 6.5 million barrels per day, nearly half of the U.S. record of 13.5 million in December.

However, growth is slowing. Years of drilling in the core areas of the Permian's top sub-basins, Midland and Delaware, have depleted much of the best reserves. Companies are now moving to lower-quality areas, leading to less oil, more water, and gas output. This has raised concerns in the industry, with analysts and executives warning about the challenges of sustaining production at current levels.

For now, output is still increasing.

Shale executives predict that oil production growth in the Permian will slow by about 25% this year, adding 250,000 to 300,000 barrels per day. The government expects a bigger increase of around 350,000 barrels per day, but even that would be the smallest growth in the basin's oil production since the COVID-19 pandemic.

Source: LSEG

These developments have no doubt given market participants food for thought and could in part explain the rise in Oil prices so far this week.Tariffs and a global economic slowdown still remain the biggest threat as does a potential US-Iran confrontation which seems to be growing more likely day by day.

US Airlines have already flagged a drop in demand and if this spreads globally then demand fears will no doubt rise once more and could put pressure on Oil prices.

Technical Analysis - Brent Crude

This is a follow-up analysis of my prior report “Brent Oil Price Update: Crude Reacts to Iran Sanctions & Potential US Tariffs” published on 20 March 2025.

From a technical analysis standpoint, Brent has finally broken free from the range it was confined to between 72.39 and 70.18 since March 20.

Brent has since broken above the range and the descending trendline which was in play.

However today's daily candle is set to close as a bearish inside bar candle which could be a sign that a pullback is imminent.

Support rests at 73.00 and 72.38 before the 71.33 comes into focus.

If bulls continue their charge then immediate resistance is provided by the 200-day MA at 74.45 before the 75.00 psychological level comes into focus.

Brent Crude Oil Daily Chart, March 27, 2025

Source: TradingView

Support

73.00

72.39

71.33

70.00 (psychological level)

Resistance

74.45

75.00

76.35

79.00

Trump’s ‘Liberation Day’ – What to Expect?

We take a look at tariffs enacted so far, what is expected to come into effect on April 2nd and what could be on the menu next. We provide an overview of the expected direct impact on US GDP without retaliation or sentiment effects.

While tariffs on individual countries or product groups have usually only limited effect on a macro level, small changes add up.

Fully enacting the expected tariffs on China, Canada, Mexico, cars & car parts as well as steel & aluminum could lift the effective average tariff rate above 13% and weigh on US GDP by 0.5%.

The reciprocal measures remain the most difficult to predict. We cannot rule out first EU-specific tariff announcements already next week.

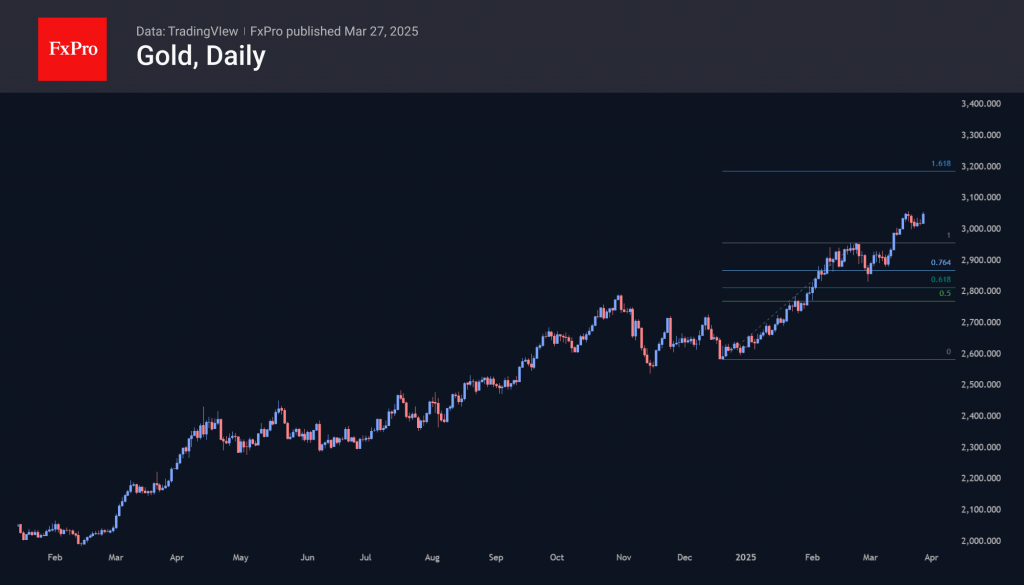

Gold and Silver About to Break the Ceiling

Gold returned to growth this week, re-entering the territory of historical highs after a brief correction at the end of last week. The reason for the new growth momentum is new bouts of tariff wars, which intensifies the pull to safe havens on the part of Central Banks. They continue to buy gold instead of US Treasury bonds.

The current growth is a logical development of the technical picture, which we have described many times before. Its logical development will be a growth to the area of $3180 in the perspective of a couple of weeks and a rise towards $3400 by the end of summer.

Silver also shone, climbing to levels above $34 per troy ounce. The last time we briefly saw such a price was last October. Before that, it wasn’t since 2012. Even then, it was a pivotal area. The bulls are clearly looking at the current situation with some trepidation. A foothold at this level or higher would take the upside potential to $50 an ounce, which is almost half the price of current levels. Compare that to gold’s 11% appreciation potential.

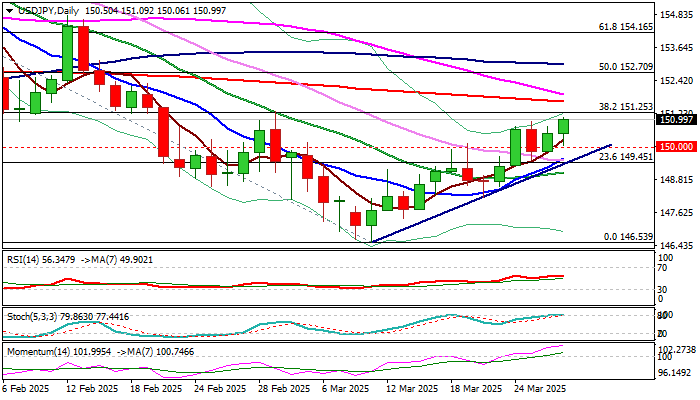

USD/JPY: Bulls Eye Key Technical Barriers at 151.25/30

USDJPY is establishing above 150 support as fresh gains extend into second consecutive day and fully reverse Tuesday’s 0.7% drop.

Bulls cracked 151.00 level on Thursday and pressure pivotal barriers at 151.25/30 (Fibo 38.2% of 150.87/146.53/March high).

Headwinds could be expected at this zone, which would pause recovery from 146.53 (March 11 low), although dips are likely to be limited and provide better levels for fresh longs.

Broken 150 level reverted to support which should hold extended dips and keep near term focus at the upside.

Violation of 151.25/30 and nearby 200DMA (151.66) to generate strong bullish signal for continuation of recovery leg from 146.53 towards 152.70 (50% retracement).

Res: 151.00; 151.25; 151.30; 151.66.

Sup: 150.25; 150.00; 149.50; 149.07.

Sunset Market Commentary

Markets

This week’s volatile and often erratic trading pattern continued today. European markets obviously started in a bad mood as US President Trump pushed through (the partly anticipated) 25% tariffs on the car sector after European close. Key European indices started with losses of around 1.5%, but avoided a steeper drop with the unknown known finally morphing into a known known and at least providing the advantage of clarity. EUR/USD dipped since yesterday’s tariff pre-lude from the 1.0795 area to 1.0740 in Asian trading, only to be back at start as we finish this report. The German Bund opened strong, but rapidly turned south in lockstep with UK Gilts and US Treasuries. UK Chancellor Reeves tried to defend her Spring budget, but the focus on future payback effects from structural reforms isn’t the one markets currently want to see. Stressing that it’s okayed by the UK Office for Budget Responsibility (OBR) isn’t the best sales argument given the OBR’s track record of painting a too rosy economic picture. It means either more economic pain in the Autumn update (tax hikes, spending cuts) or choosing for the “easy” way by giving up fiscal rules. Today’s Gilt sell-off suggests markets take the second route more and more into account. The UK 10-yr yield touched 4.8% for only the second time since 2008 following a brief period higher in January. US Treasuries followed the move south with tonight’s long-term budget outlook (2025-2055) from the Congressional Budget Office in mind. The US 10-yr yield tested first technical resistance at 4.4%, but a break higher in yields was blocked for now. A marginal downward revision to the Q4 PCE deflator (2.6% Q/Q from 2.7%) and continuously low weekly jobless claims (224k) might have marginally helped. Souring risk sentiment going as US dealings kicked off, played a role as well in balancing (long term) core bond losses from an intraday perspective. The front end of core bond curves outperformed, especially in Europe. ECB comments were mixed with Wunsch suggesting that a pause for April should at least be on the table given upside inflation risks. ECB Kazaks argues in favour of a gradual reduction in rates in the future if the ECB’s baseline scenario holds. However, geopolitical uncertainty is so high that it makes a difficult navigating. ECB vice-governor De Guindos leaves it out in the open for April, balancing all risks. Our base scenario is final 25 bps rate cut followed by a long pause.

News & Views

The Norges Bank (NB) today left its policy rate unchanged at 4.5%. In the respect, the NB ‘backtracked’ on guidance at the January 22 meeting that “the policy rate will likely be reduced in March”. Inflation picked up in recent months and has been markedly higher than expected (1.4% M/M and 3.6% Y/Y, core 1.0% M/M and 3.4% Y/Y in February). Wage growth in 2024 also turned out higher than projected. This could lead to higher inflation ahead than previously projected. Economic activity fell towards the end of last year and was lower than expected, but Norges Bank’s Regional Network Contacts reported increased activity over winter. In this context, the NB judges that a restrictive monetary policy is still needed to bring inflation down to target within a reasonable time horizon. The NB upwardly revised its expectations for the CPI-ATE for 2025 to 3.4% (from 2.7%) and to 2.9% from 2.7% for 2026, but still expects inflation to return to 2.1% in 2028. At the same time, the NB is aware that an overly tight policy could restrict the economy more than needed. Trade-offs make the MPC conclude that the current stance is warranted for somewhat longer than previously signaled. The new NB forecast is consistent with a decline in the policy rate to 4% by the end of the year (September & December rate cuts), followed by a very gradual further decline over the next years towards 3% by 2028. The krone briefly declined to EUR/NOK 11.39 at the time of the decision but currently trades little changed near EUR/NOK 11.34.

The Hungarian government announced additional requirements for investment funds today. From October, they must hold at least 3% of their assets in short-term government debt. There’s already a rule in place, obliging them to hold 5% in government bonds. Those minimum requirements increase to 4% and 6% respectively from April 2026 while those levels rise to 5% and 10% for bond funds. Hungarian bonds rallied after the announcement with the 10-yr government bond yield currently shedding up to 10 bps.