Sample Category Title

XAU/USD: Gold Rises Further on New US Tariffs

Gold price rose to one week high on Thursday after President Trump announced a new package of tariffs on imported cars.

New addition to the set of reciprocal tariffs from the world’s largest economy, due to become operational on Apr 2, sent fresh shockwaves through the world and boosted fears of further disruption in global trading, economic slowdown and rise in consumer inflation.

The latest news boosted safe haven demand and further lifted the yellow metal’s price, improving technical picture on daily chart, as fresh extension higher retraced over 61.8% of $3057/$3000 pullback, adding to signals that corrective phase from new record high is likely over.

Strong positive momentum and daily MA’s in full bullish configuration, contribute to bullish near-term outlook.

Bulls cracked Fibo 76.4% barrier at $3043, the last significant obstacle en-route to $3057 record high of last week, though anticipating strong headwinds here.

This may keep the price action in prolonged consolidation, but to remain bullishly aligned while holding above broken Fibo level at $3035 (61.8% retracement) and keep in play dip-buying scenario.

Caution on dips below $3035/30 and potential violation of 10DMA ($3022) which would sideline near-term bulls and risk retest of key $3000 support.

Res: 3057; 3071; 3079; 3093.

Sup: 3035; 3030; 3022; 3007.

XNG/USD Analysis: Natural Gas Price Drops to March Low

On 27 January, our analysis of the natural gas chart highlighted the formation of an ascending channel. Later, on 10 March, we noted that the sharp price increase had created technical conditions for a correction.

Since then, as indicated by the arrow on the XNG/USD chart, natural gas prices have declined by approximately 19%.

Why Is the Price of Natural Gas Falling?

- Unseasonably Warm Weather: Atmospheric G2 reported on Wednesday that forecasts now indicate significant warming across the eastern half of the U.S. from 31 March to 4 April. This could reduce demand for natural gas used in heating.

- Rising Inventories: According to the EIA’s forecast, weekly natural gas storage levels are expected to increase by +33 billion cubic feet over the past week.

Technical Analysis of XNG/USD Chart

Looking at the broader trend since the start of the year, the ascending channel (marked in blue) remains relevant. However, bears have pushed the price below its median line, shifting movement into a short-term downward channel (marked in red).

Currently, natural gas is trading near the $3.780/MMBtu level, a key price point that has previously acted as both support and resistance. Whether a bearish breakdown or a bullish rebound occurs largely depends on the upcoming EIA report, scheduled for release at 17:30 GMT+3.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Announcement of New Tariffs Boosts US Dollar

Yesterday, it was revealed that Donald Trump plans to introduce new 25% tariffs on cars not manufactured in the United States. This duty will be added to existing tariffs and is set to take effect on 2 April. The White House believes that these measures will support the US economy and, in the long term, create new jobs.

At the same time, critics warn that the new tariffs could trigger inflation and lead to a recession. Currently, markets are responding to the news with a strengthening of the US dollar.

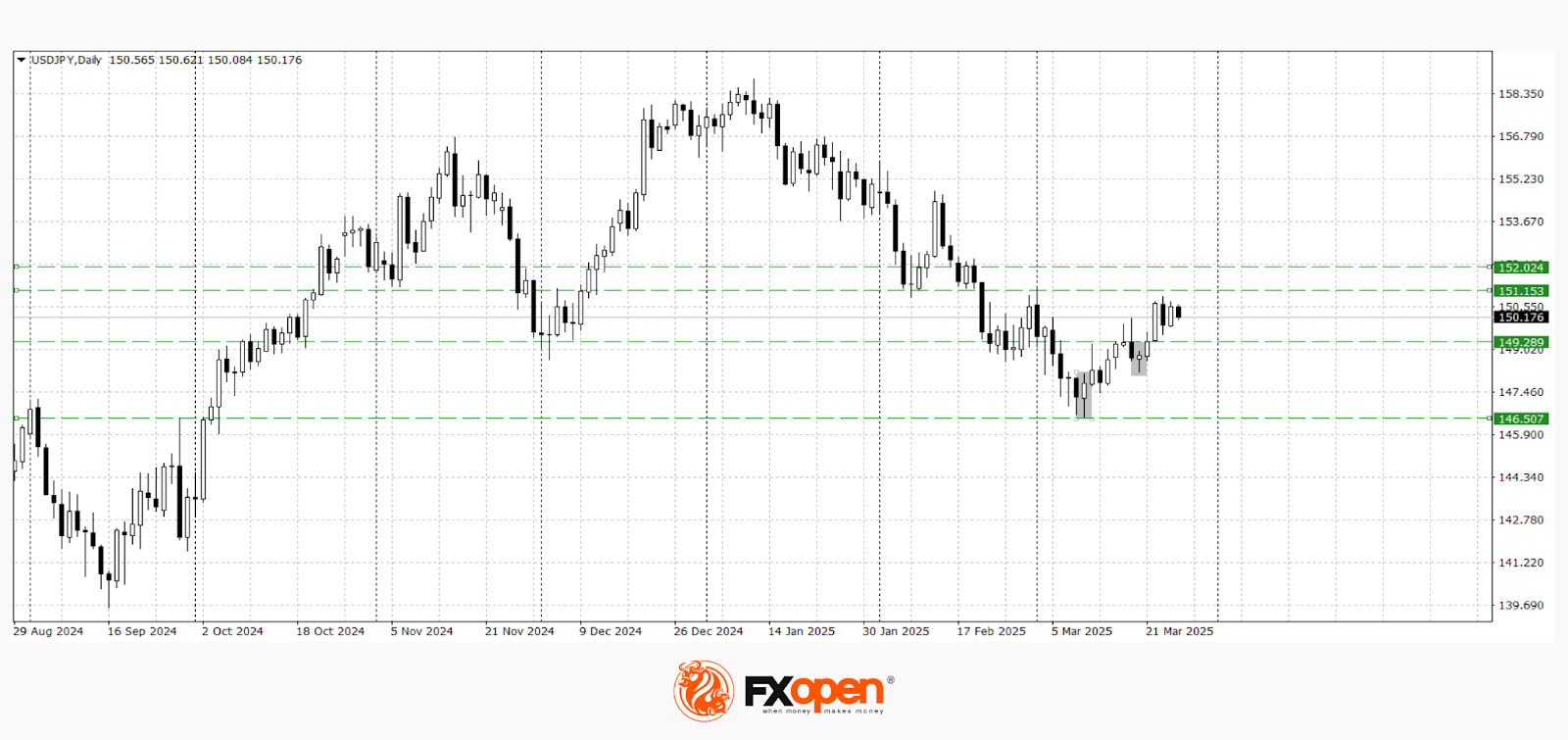

USD/JPY

Following the formation of a bullish engulfing pattern on 11 March, USD/JPY buyers have managed to hold above the key resistance level of 150.00.

Technical analysis suggests that if the pair continues trading above 149.30–149.00, further growth towards the 152.00–151.20 range is possible. A break below 149.00 could trigger a new downward move, potentially leading to a retest of the March lows at 146.60.

Key events that may influence USD/JPY today:

- 15:30 (GMT+2) – Core Personal Consumption Expenditures (PCE) Price Index (US)

- 15:30 (GMT+2) – US GDP

- 15:30 (GMT+2) – Initial Jobless Claims (US)

- 15:30 (GMT+2) – US Retail Inventories (excluding autos)

USD/CAD

The USD/CAD pair continues to trade within the medium-term range of 1.4540–1.4230.

A break below the lower boundary of 1.4230 may lead to a test of the January low at 1.4160. If USD buyers manage to push the price back above 1.4300, a recovery towards 1.4580–1.4500 could follow.

Key events that may affect USD/CAD in the upcoming sessions:

- Today at 15:30 (GMT+2) – Average Weekly Earnings (Canada)

- Today at 23:30 (GMT+2) – US Federal Reserve Balance Sheet

- Tomorrow at 15:30 (GMT+2) – Canadian GDP

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB’s Wunsch: April rate pause should be on the table

Belgian ECB Governing Council member Pierre Wunsch suggested that pausing rate cuts in April should at least be “on the table”, and highlighted how tariff-induced stagflation poses a policy dilemma.

Wunsch warned that tariffs would complicate ECB’s path forward: “To the extent that tariffs will impact the economy … this will have an impact on our decision-making,” he noted.

While downplaying the immediate importance of April's tariff development, Wunsch stressed that "It’s going to have an impact over the medium term.”

In contrast, Latvian Governing Council member Martins Kazaks suggested that if ECB’s baseline scenario holds, a “gradual reduction in rates in the future” could be expected.

Dollar Outperformed on (or is it Despite?) Risk-Off

Markets

Again no really congruent storyline to guide US and European markets yesterday. Equities on both sides of the Atlantic were captured in a risk-off modus as Trump’s Liberation Day tariff announcement was coming ever closer. The uncertainty, however, still resulted in a different performance between US and EMU interest rate markets. EMU (swap) yields declined further in a steepening move (2-y -4.1 bps, 30-y -2.2 bps). Money markets apparently are still embracing the idea of a ‘frontloaded’ April ECB interest rate cut (75% discounted). We join this view but are far more reluctant on the room for further steps later this year. In the US, bond markets despite the lingering risk-off, went in the other direction. Yields added between 0.3 bps (2-y) and 4.3 bps (30-y). Markets apparently assume that the Fed will stay in a wait-and-see approach. Even so, several Fed member including ST Louis Fed President Musalem are making reservations on Powell’s assessment last week that the inflationary impact of tariffs will likely be temporary. This debate, combined with CBO fiscal outlook might be important for yields in the (near?) future. If the Fed doesn’t respond decisively enough the market might. On FX markets, the dollar this time outperformed on (or is it despite?) the risk-off. DXY closed at 104.55. EUR/USD finished the session at 1.0754 (from 1.0791). The yen also weakened to USD/JPY 105.6. UK markets reacted rater constructive to softer than expected CPI data and to Fin Min Reeves’ spring budget update (and new OBR fiscal projections). UK yields eased between 1.1 bp (2-y) and 6.0 bps (30-y). Sterling declined after the CPI data, but regained most of the loss especially against the euro later (EUR/GBP 0.8345 close).

US President Trump announcing 25% tariffs on all cars imported in the US after the close of US markets is dominating the headlines this morning. Equity markets of the likes of Japan and South Korea are trading in red, but the reaction is very orderly. The EuroStoxx 50 future cedes 0.5%. US futures trade little changed. Trump also already warned on more tariffs on the EU and Canada if the work against the US. Even so, the orderly reaction suggests that an important part of this news was discounted. The intraday dynamics of EU equity markets might be telling. Also interesting, in FX EUR/USD (1.0775) trades off yesterday’s lows. DXY also eases (104.35). Later today, the eco calendar is thin (US weekly jobless claims), but several ECB policy makers will speak. Still, investors’ reaction to the tariffs announcement will set the tone for global trading. We especially keep a close eye at the reaction of US Treasuries. Will markets continue to accept Powell’s view at the press conference last week that the impact of tariffs on inflation/inflation expectations will probably remain temporary? If doubt is creeping in further, this might affect risk premia. In this respect, also keep a close look at the long term CBO US budget outlook to be updated today. Additional negative headlines on the sustainability of US debt might put pressure, especially at the long end of the US yield curve. For the dollar, the jury is still out. Even so, we look out for signs of a topping out process after recent rebound as quite some negative news on tariffs might gradually be discounted for the likes of the euro and the yen.

News & Views

The non-partisan US Congressional Budget Office estimates the United States risk no longer being able to cover its obligations by August unless Congress acts to raise the debt ceiling. It warned that this so-called X-date could even be as soon as late May or somewhere in June should borrowing needs in coming months exceed CBO projections. The estimate is also complicated by shifts in timing and amount of revenue collection and spending. The CBO to that end noted several important dates, including the April 15 deadline for taxpayers to submit annual filings, a mid-June tax payment deadline and June 30, when additional extraordinary (accounting) measures for the US Treasury become available.

France’s budget deficit widened from 5.4% in 2023 to 5.8% last year, the country’s statistical office reported this morning. While huge and well-above the 3% EC limit, it was slightly less than the 6% the Finance Ministry had forecasted. It offers the government a slight reprieve and a better starting point for bringing down the gap to 5.4% again this year. That was already a hard-fought compromise by a minority government in a highly fractured parliament. The goal is to get back to the 3% cap by 2029 but didn’t get any easier by the plans to significantly increase military outlays over the coming years. Finance Minister Lombard, however, already said he won’t deviate from the current trajectory, meaning spending cuts will have to found elsewhere. France’s public debt rose to 113% of GDP end last year, up from 109.8% in 2023. The debt ratio prior to the pandemic stood at 97.9% (2019)

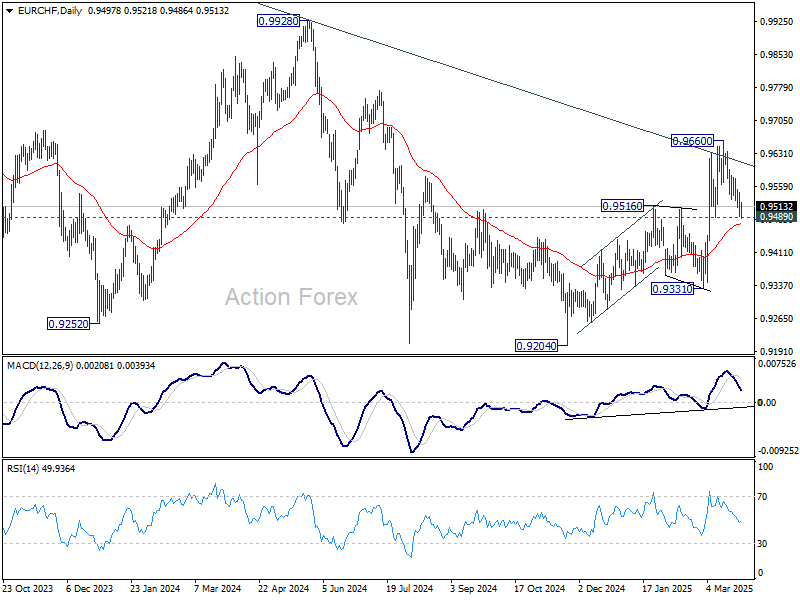

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9487; (P) 0.9516; (R1) 0.9532; More....

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. Strong support is expected fro 0.9489 to complete the correction from 0.9660. On the upside, above 0.9581 minor resistance will bring retest of 0.9660 first. However, sustained break of 0.9489 will dampen this view, and bring deeper fall back to 0.9331 support next.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9487) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9618) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be seen to 0.9928 key resistance at least.

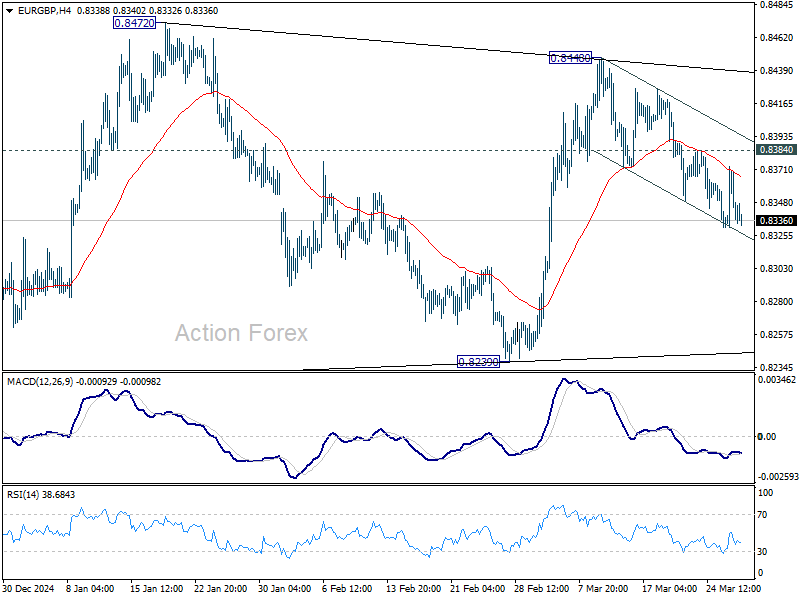

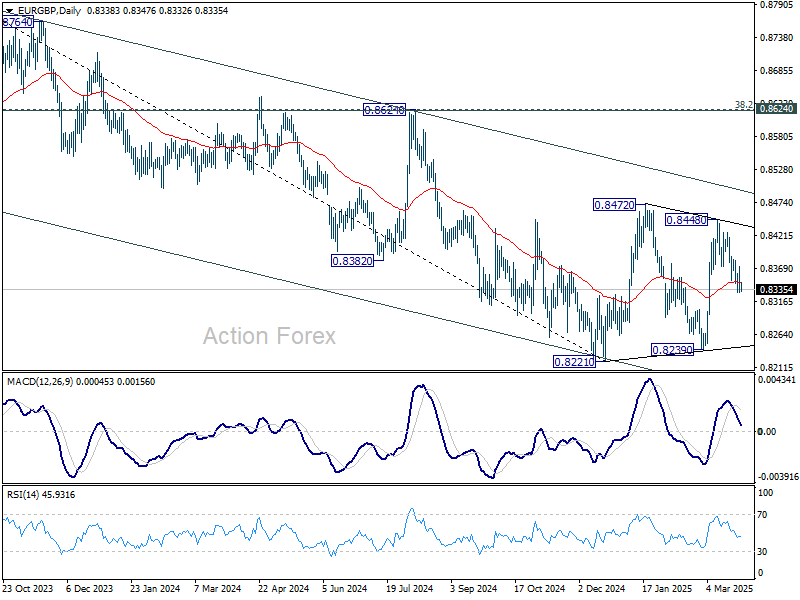

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8323; (P) 0.8349; (R1) 0.8369; More...

Intraday bias in EUR/GBP stays mildly on the downside for the moment. Rise from 0.8239 might have completed at 0.8448 already. Deeper fall would be seen back to 0.8239 support. On the upside, above 0.8384 minor resistance will turn bias back to the upside for 0.8448. Overall, consolidation pattern from 0.8221 is still in progress and could extend further.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8495).

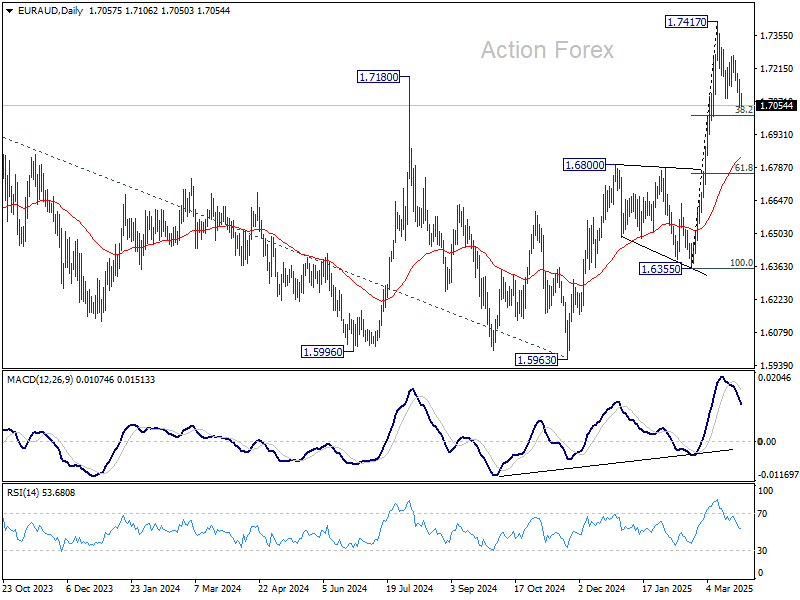

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7027; (P) 1.7097; (R1) 1.7144; More...

Intraday bias in EUR/AUD remains mildly on the downside as correction from 1.7417 is extending lower. But downside should be contained by 1.6990 support to bring rebound. On the upside, above 1.7270 will bring retest of 1.7417 first. Break there will resume whole rise from 1.6335.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

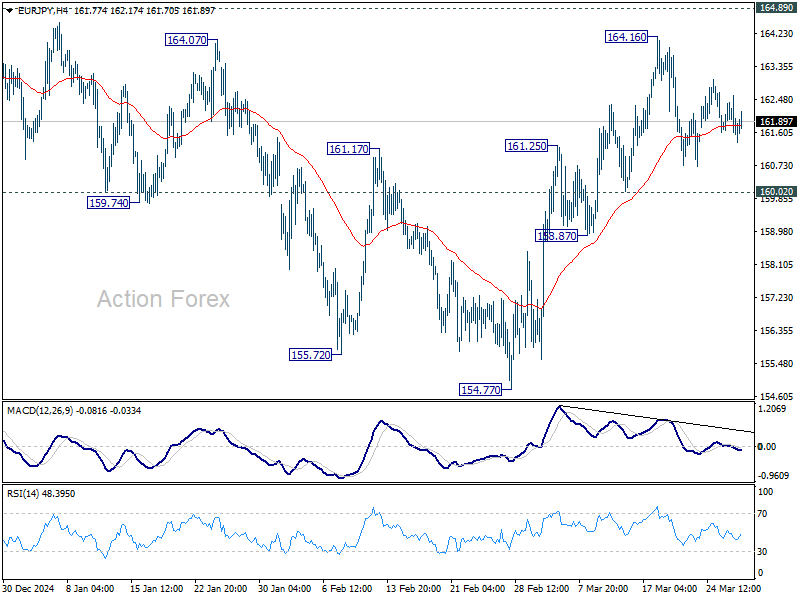

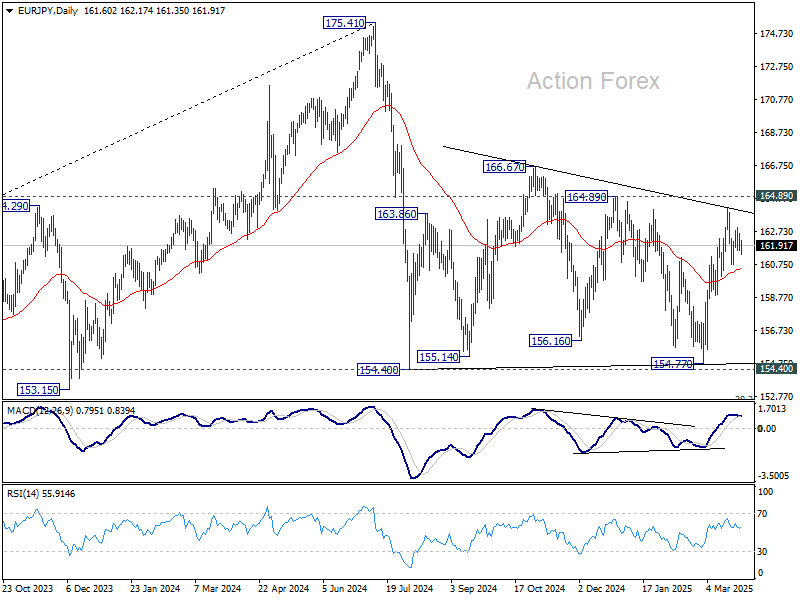

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.52; (P) 162.07; (R1) 162.49; More...

Intraday bias in EUR/JPY remains neutral first, as consolidation continues below 164.16. Further rally remains in favor as long as 160.02 support holds. Above 164.16 will target 164.89 and then 166.67. On the downside, however, break of 160.02 will argue that rise from 154.77 has completed and turn bias to the downside. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

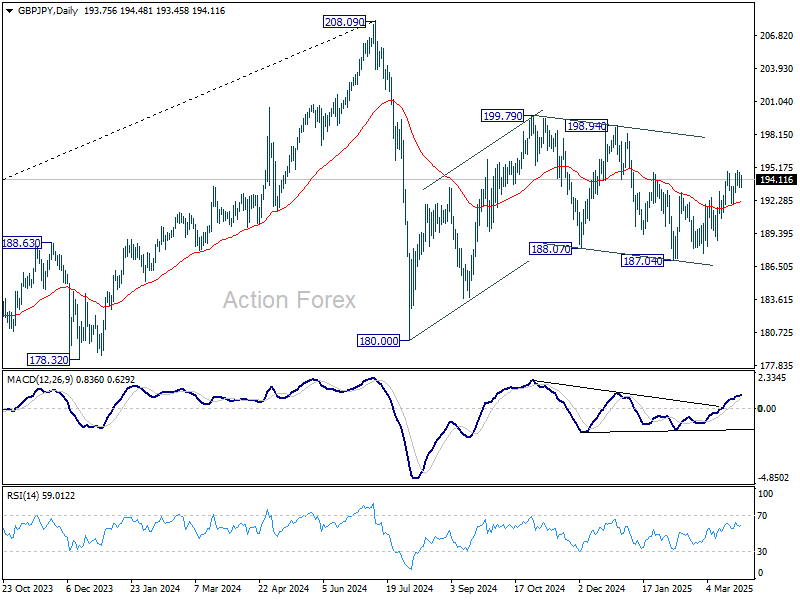

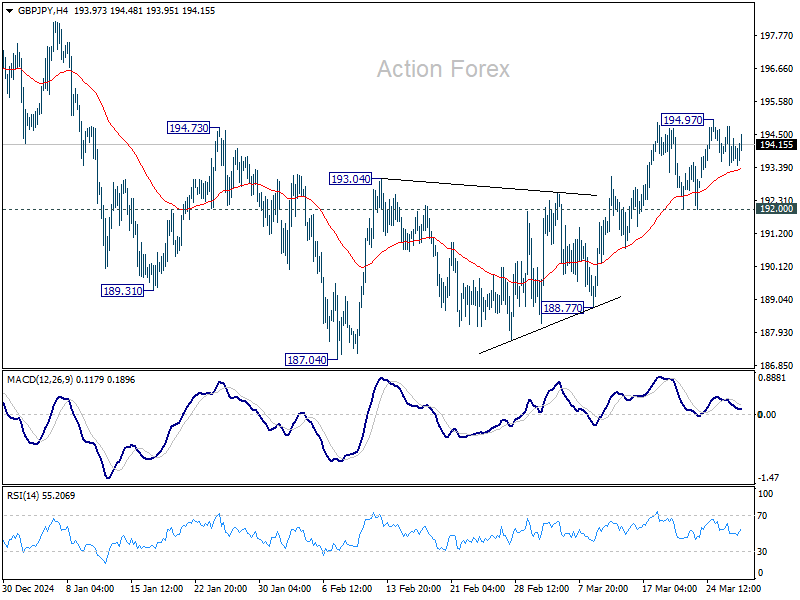

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.45; (P) 194.12; (R1) 194.77; More...

Intraday bias in GBP/JPY remains neutral at this point. On the upside, above 194.97 will resume the rebound from 187.04 towards 198.94 resistance. On the downside, break of 192.00 support will turn bias back to the downside for 188.77 support. Overall, corrective pattern from 180.00 is still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.