Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0884; (P) 1.0906; (R1) 1.0945; More...

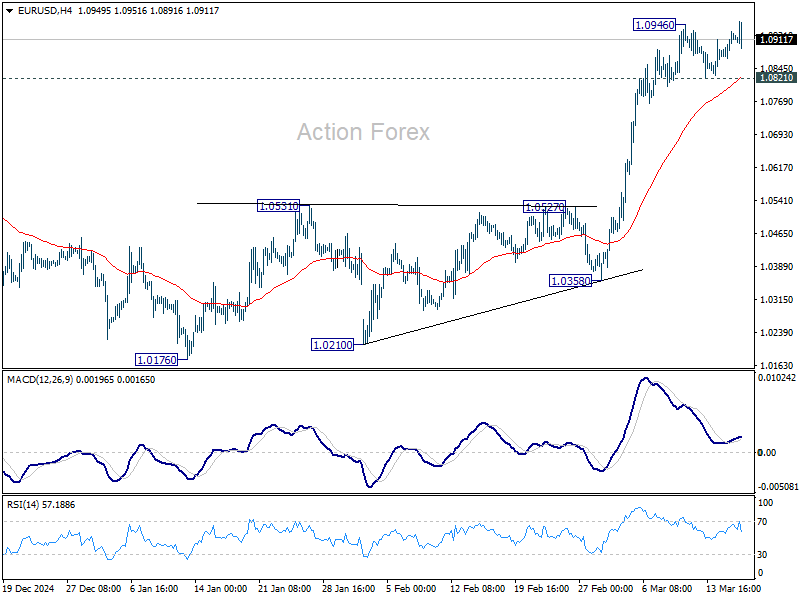

Intraday bias in EUR/USD is back on the upside with breach of 1.0946 resistance. Current rally from 1.0176 should target 1.1274 key resistance. On the downside, though, break of 1.0821 support will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2940; (P) 1.2970; (R1) 1.3020; More...

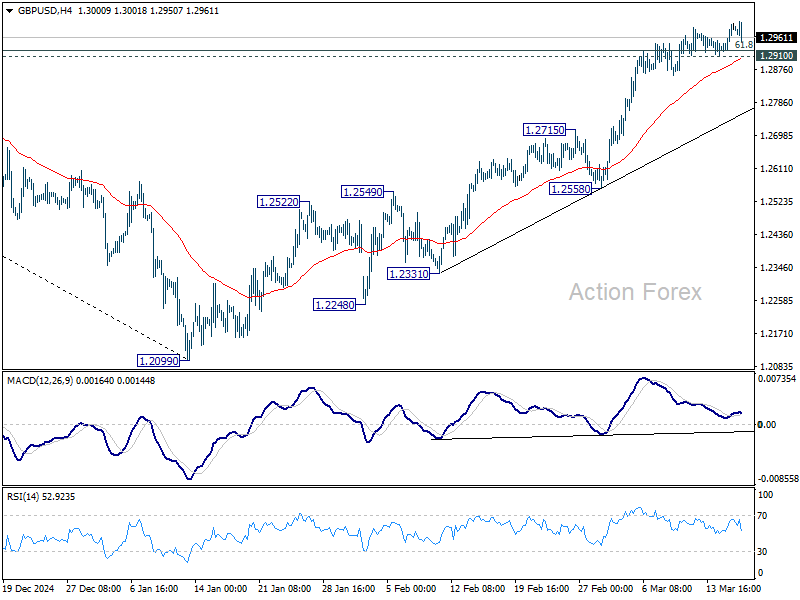

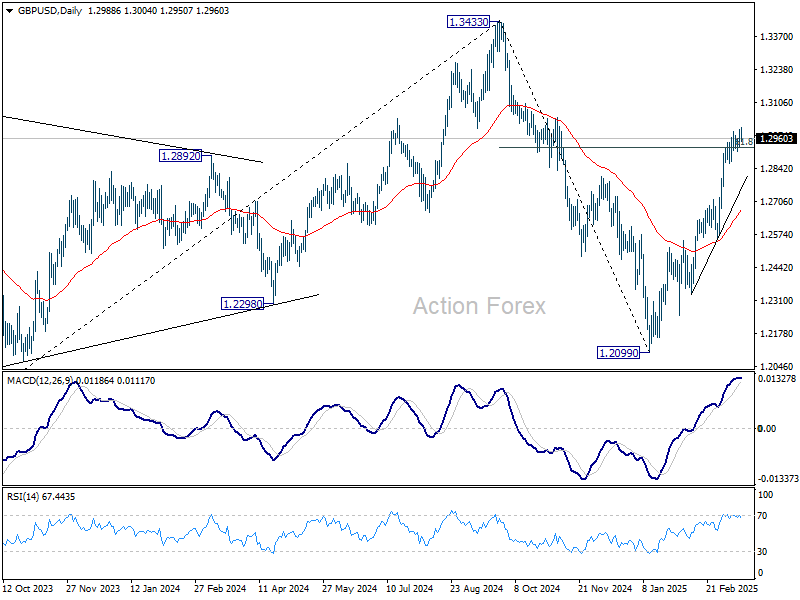

Further rally is still in favor in GBP/USD with 1.2910 minor support intact. Sustained trading above 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will pave the way back to 1.3433 high. However, break of 1.2910 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

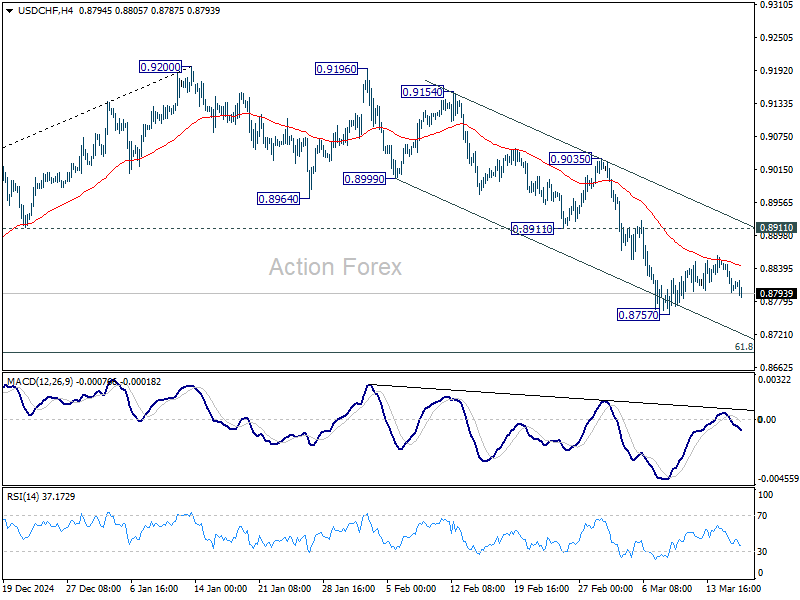

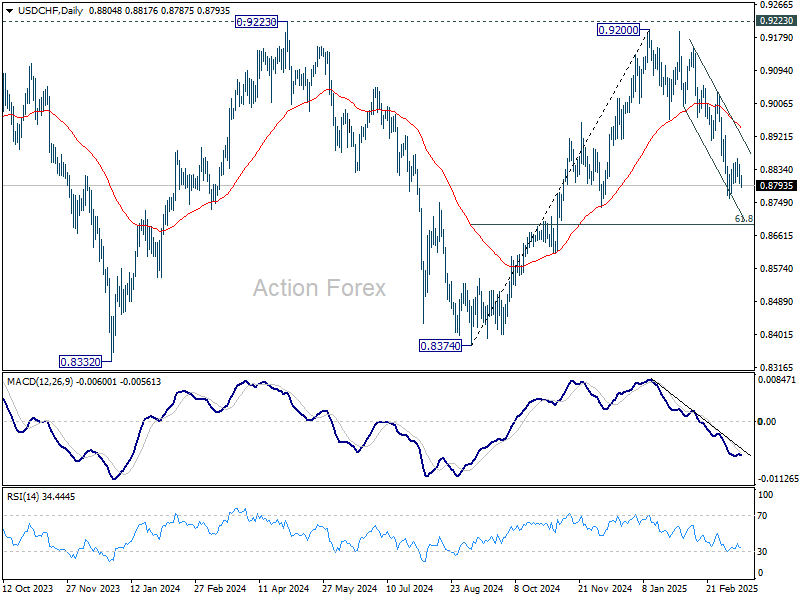

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8786; (P) 0.8821; (R1) 0.8844; More…

Intraday bias in USD/CHF remains neutral for now, and more consolidations would be seen. In case of another recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

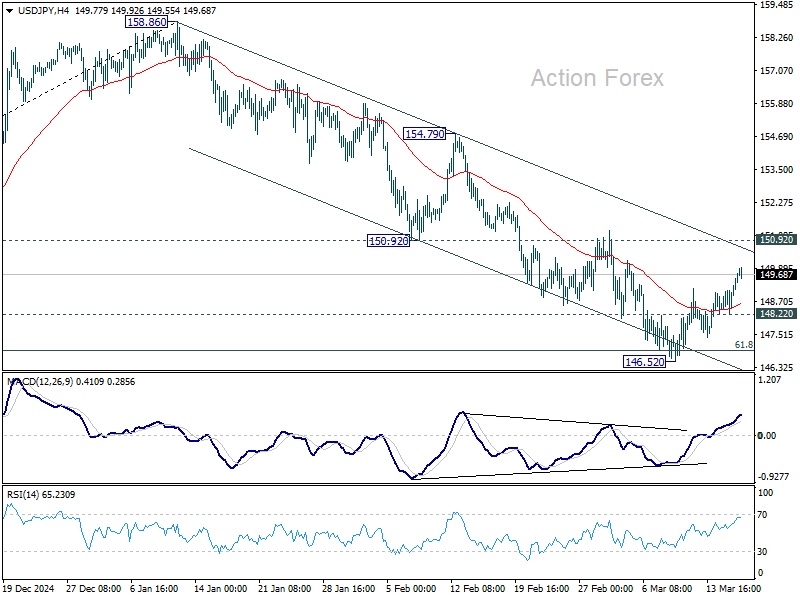

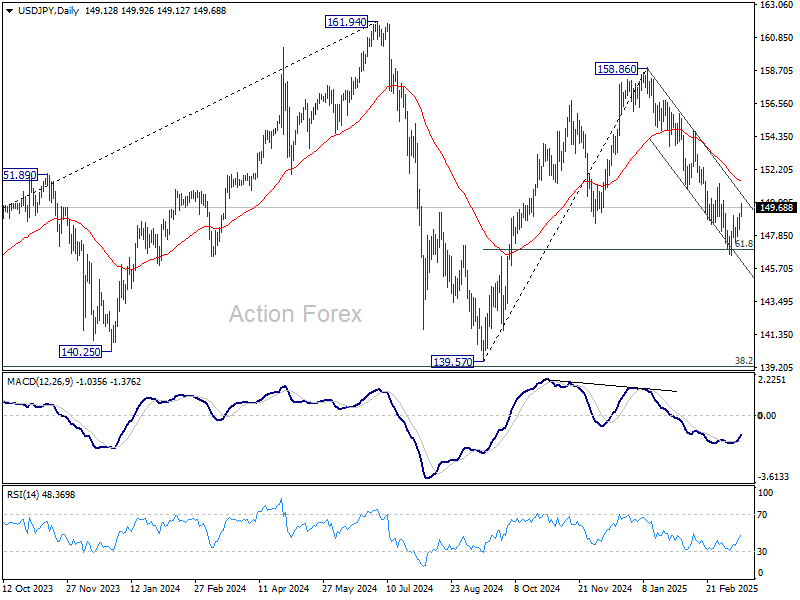

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.89; (P) 148.45; (R1) 149.20; More...

Outlook in USD/JPY remains unchanged for now and intraday bias stays neutral. While recovery from 146.52 might extend further, upside should be limited by 150.92 support turned resistance. On the downside, below 148.22 minor support will bring retest of 146.52 low first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. However, decisive break of 150.92 will dampen this bearish view and turn bias to the upside for 154.79 resistance instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

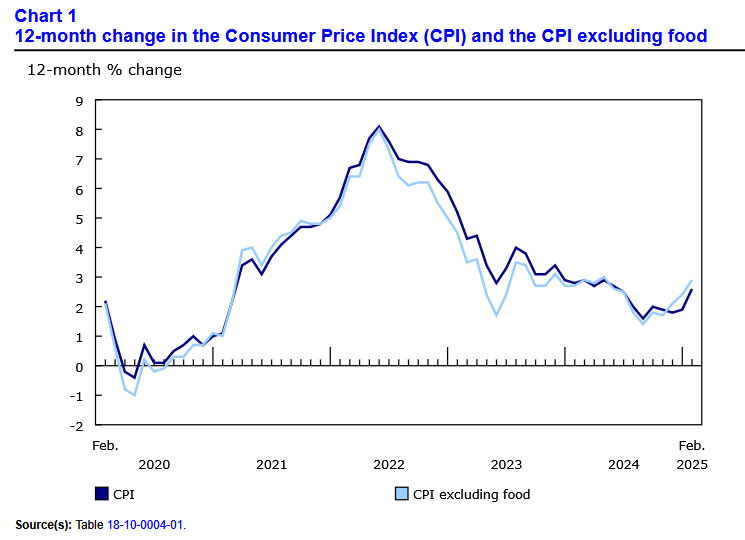

Canadian Inflation Moves Higher in February as Sales Tax Holiday Ends

Headline CPI inflation increased in February to 2.6% year-on-year (y/y), above expectations and up from 1.9% in January. The GST/HST holiday that ended Feb. 15th, played a key role in higher inflation.

Not surprisingly given the sales tax holiday, restaurant prices contributed the most to the acceleration in headline CPI in February. Prices for food in restaurants were down 1.4% versus a year ago compared to -5.1% y/y in January.

Slower energy price gains at the pump moderated the increase in inflation. Gasoline prices were up 5.1% y/y in February, down from 8.6% y/y in January.

Inflation continued to slow for the key shelter component (+4.2% y/y) and transportation (+3.0% y/y). Shelter has been a major source of inflation in recent years, but should be a moderating force in the months ahead.

The Bank of Canada's preferred "core" inflation measures were also hotter-than-expected, averaging 2.9% y/y in February, up from 2.7% y/y in January. The trends over the past three months suggest that core inflation is set to head a bit higher in the months ahead, with the three-month annualized pace running slightly above 3% in February.

Key Implications

Headline inflation was a little hotter than expected as the sales tax holiday came to an end. However, the three-month annualized trend in core inflation has been tracking above 3%, signaling that core inflation should continue to grind higher. Our Quarterly Economic Forecast published today shows core inflation rising next quarter as tariffs contribute to price pressures.

This puts the BoC in a difficult place. Canadians' inflation expectations have risen, but the hit to demand from uncertainty and the tariffs themselves are already weighing on demand. How tariffs play out remains highly uncertain. Our forecast assumes elevated U.S. tariffs over the next six months, and then gradual reductions. In this world, we expect the Bank of Canada to provide some further cushion in the form of two more 25 basis point rate cuts at its next two rate announcements. Markets have lowered their odds of a cut on April 16th slightly in the wake of today's inflation numbers, but we will know a lot more about the path of tariffs by the time the decision rolls around.

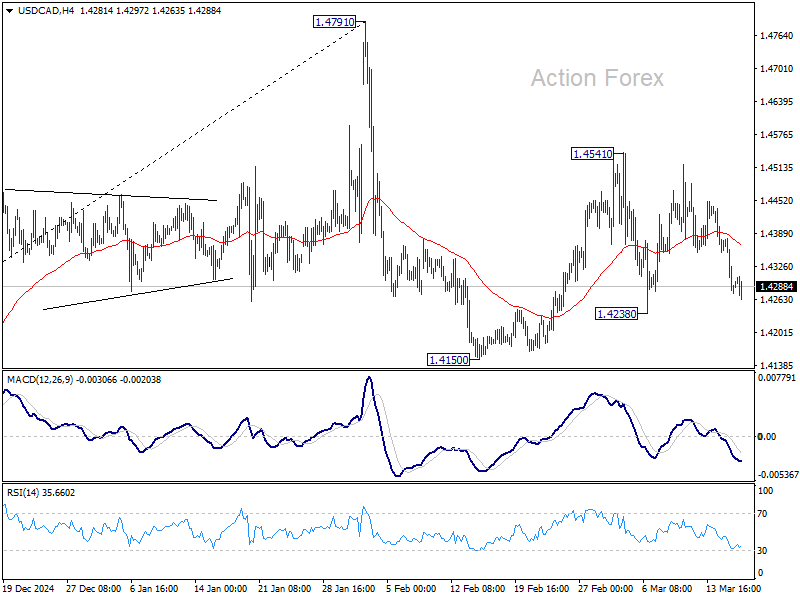

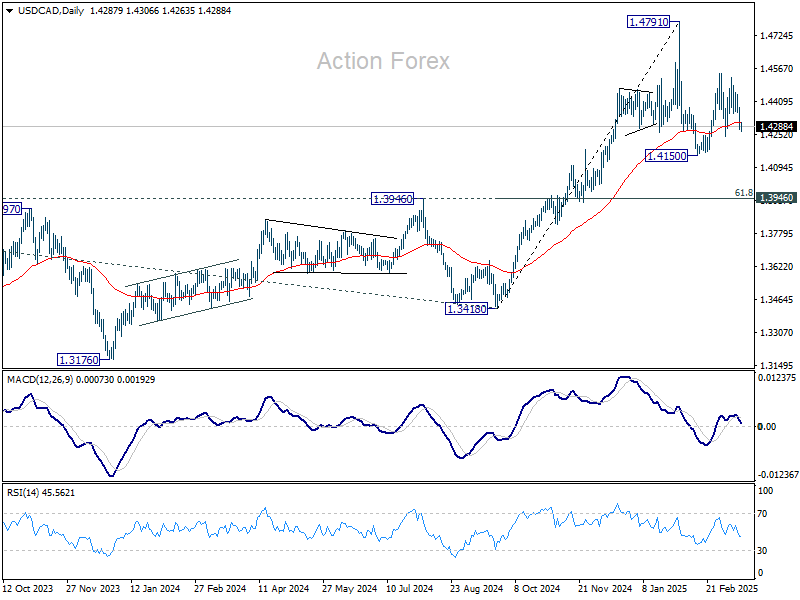

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4246; (P) 1.4315; (R1) 1.4355; More...

Range trading continues in USD/CAD and intraday bias remains neutral. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Canadian Dollar Gains on Inflation Surprise, But Growth Risks Keep Traders Cautious

Canadian Dollar edged higher in early US session after much stronger-than-expected inflation data. However, Loonie quickly lost momentum, as investors remained cautious about Canada’s broader economic outlook, particularly in the face of rising trade tensions with the US.

While higher-than-expected inflation reduces the likelihood of another immediate rate cut, Canada’s economy is under serious pressure due to U.S. tariffs. If upcoming economic indicators, particularly March employment data, show signs of deterioration, it could strengthen the case for BoC to ease policy again. Traders appear hesitant to aggressively push the Loonie higher, as uncertainty remains over how BoC will balance inflation concerns with mounting growth risks.

For the day so far, Swiss Franc is the strongest performer, followed by Dollar and Loonie. Yen lags behind, followed by Aussie and Sterling. However, outside of Yen’s sharp decline, movements in most currency pairs have been relatively contained, as investors hold positions ahead of key central bank policy announcements in the upcoming days.

The focus will shift to BoJ during the upcoming Asian session, where it is widely expected to keep interest rates unchanged at 0.50%. While solid GDP growth and robust wage increases support the case for another hike as soon as May, the uncertain global trade outlook and potential volatility in US stock markets could prompt BoJ to delay further tightening until risks are clearer.

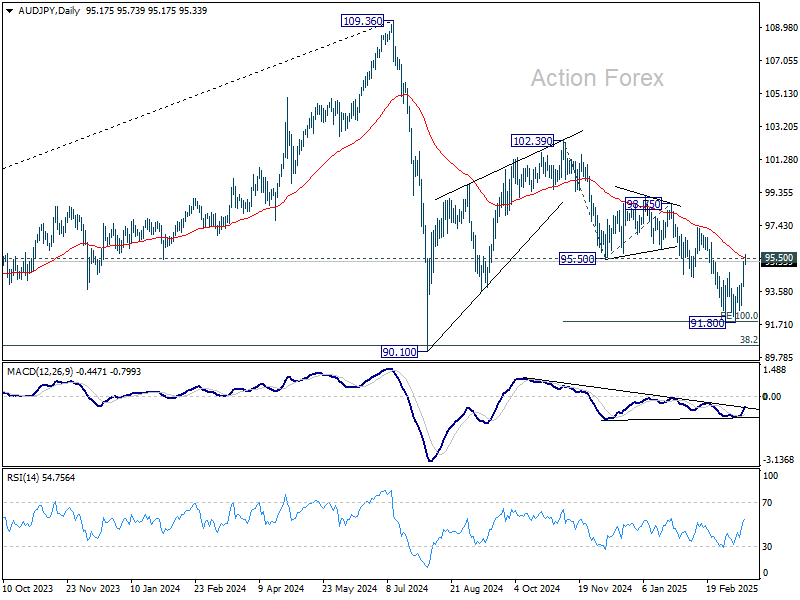

Technically, AUD/JPY's immediate focus is on 95.50 support turned resistance and 55 D EMA (now at 95.60) in AUD/JPY. Sustained break there should confirm that fall from 102.39 has completed with three waves down to 91.80, as the second leg of the pattern from 90.10. In this case, stronger rally should be seen through 98.75 towards 102.39. However, rejection by the resistance zone will extend the decline from 103.39 to 90.10 low.

In Europe, at the time of writing, FTSE is up 0.46%. DAX is up 1.18%. CAC is up 0.65%. UK 10-year yield is up 0.034 at 4.683. Germany 10-year yield is up 0.014 at 2.839. Earlier in Asia, Nikkei rose 1.20%. Hong Kong HSI rose 2.46%. China Shanghai SSE rose 0.11%. Singapore Strait Times rose 0.92%. Japan 10-year JGB yield rose 0.003 to 1.506.

Canada’s CPI surges to 2.6%, growing chance for BoC pause at next meeting

Canada’s CPI jumped sharply from 1.9% yoy to 2.6% yoy in February, exceeding market expectations of 2.1%. This marks the first time in seven months that inflation has risen above the 2% mid-point of BoC's target range.

A key driver of the surge was the expiration of a sales tax break in mid-February, which added to an already broad-based increase in prices. Without the tax impact, inflation would have hit 3.0%. On a monthly basis, CPI rose by 1.1% mom.

A closer look at the CPI basket shows widespread price increases across multiple categories. Food prices rose 1.3% yoy, while clothing and footwear climbed 1.4% yoy. Transportation costs surged 3.0% yoy, and shelter costs remained significantly elevated, rising 4.2% yoy.

Core inflation measures also pointed to underlying price pressures. CPI median rose from 2.7% yoy to 2.9% yoy, above expectation of 2.7% yoy. CPI Trimmed rose from 2.7% yoy to 2.9% yoy, above expectation of 2.8% yoy. CPI Common also rose from 2.2% yoy to 2.5% yoy, above expectation of 2.2% yoy.

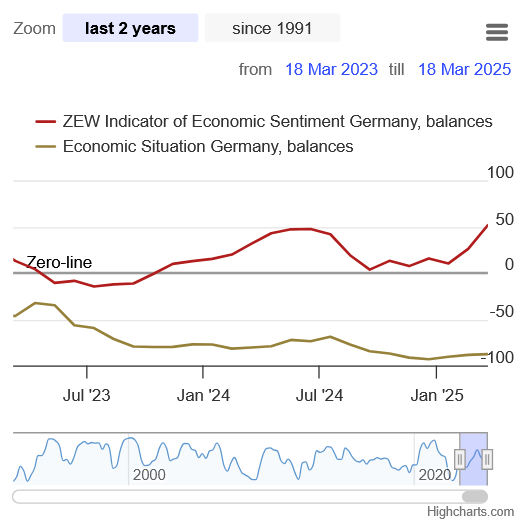

German ZEW economic sentiment surges to 51.6 on fiscal optimism

Germany’s ZEW Economic Sentiment Index surged from 26.0 to 51.6 in March, exceeding expectations of 48.1. However, the Current Situation Index only saw a marginal improvement, rising from -88.5 to -87.6, well below the forecast of -80.5.

Similarly, in the Eurozone, economic sentiment rose from 24.2 to 39.8, though it missed expectations of 43.6. Current Situation Index barely moved, edging up to -45.2.

ZEW President Achim Wambach attributed the sharp improvement in economic expectations to positive signals regarding German fiscal policy, particularly the agreement on a multi-billion-euro financial package for the federal budget.

This stimulus plan has boosted optimism for key industrial sectors, including metal and steel manufacturing and mechanical engineering, which have been struggling with weak demand and global trade uncertainty.

Another supportive factor for economic optimism has been ECB’s ongoing monetary easing.

ECB’s Rehn flags growth risks from tariff uncertainty, stays cautious on rate Cuts

Finnish ECB Governing Council member Olli Rehn acknowledged that US. tariffs and increased uncertainty are "already having adverse effects" on the Eurozone’s economic outlook, with immediate and near-term growth prospects deteriorating.

However, he pointed out that one offsetting factor could be higher defense spending across Europe, which is expected to provide some support to GDP growth in the medium term.

Rehn took a cautious stance on further ECB rate cuts, refusing to commit to any specific policy actions given the uncertainty surrounding the economic outlook.

While inflation in the Eurozone is stabilizing around the 2% target, he noted that risks are "two-sided." Despite his cautious tone, Rehn pointed to the ECB’s latest projections, which include several more rate cuts this year if the economy and inflation follow the baseline scenario.

SECO lowers Swiss growth outlook, underperformance to continue fro two more years

Switzerland’s State Secretariat for Economic Affairs has slightly lowered its growth projections for the economy, reflecting ongoing global trade tensions and economic uncertainty.

The latest forecast now sees GDP growth at 1.4% in 2025 and 1.6% in 2026, down from the previous estimates of 1.5% and 1.7%, respectively. This means the Swiss economy will likely continue expanding at a pace below its historical average of 1.8%, extending a period of subdued economic momentum for at least two more years.

SECO emphasized that while the base scenario assumes no full-blown global trade war, some negative effects from current trade frictions are still expected, adding pressure on both investment and economic activity.

According to SECO, a negative trade scenario—where international economic activity weakens further—would "significantly impact Swiss exports and domestic economic activity". On the other hand, an upside scenario exists, particularly if Germany successfully implements its massive fiscal package.

However, for now, SECO believes "downside risks to the economy currently outweigh upside potential". Also Swiss Franc’s could face upward pressure if downside risks materialize.

RBA’s Hunter cautious on further rate cuts, Treasurer warns of trade war's indirect impacts

RBA Chief Economist and Assistant Governor Sarah Hunter reinforced the central bank’s cautious stance on further rate cuts. She emphasized in a speech today that while the February cut was deemed an appropriate time to "take some restrictiveness away", the Board were "more cautious than the market about prospects for further easing".

Hunter highlighted that US policy settings and their impact on the global economy as "one of the things we are focused on right now.

She added that policy decisions are always made in uncertain environments, where the baseline forecast is just one of many possible scenarios rather than a strict roadmap for future moves. The link between economic forecasts and rate decisions is "not mechanical".

Separately, Australian Treasurer Jim Chalmers acknowledged that the direct impact of US tariffs on Australia is "concerning, but manageable". But he warned that the larger risk lies in a broader global trade war. He described the current environment as a “new world of uncertainty”, where the spillover effects from rising trade tensions could have far-reaching consequences for Australia’s economy.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4246; (P) 1.4315; (R1) 1.4355; More...

Range trading continues in USD/CAD and intraday bias remains neutral. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Canada’s CPI surges to 2.6%, growing chance for BoC pause at next meeting

Canada’s CPI jumped sharply from 1.9% yoy to 2.6% yoy in February, exceeding market expectations of 2.1%. This marks the first time in seven months that inflation has risen above the 2% mid-point of BoC's target range.

A key driver of the surge was the expiration of a sales tax break in mid-February, which added to an already broad-based increase in prices. Without the tax impact, inflation would have hit 3.0%. On a monthly basis, CPI rose by 1.1% mom.

A closer look at the CPI basket shows widespread price increases across multiple categories. Food prices rose 1.3% yoy, while clothing and footwear climbed 1.4% yoy. Transportation costs surged 3.0% yoy, and shelter costs remained significantly elevated, rising 4.2% yoy.

Core inflation measures also pointed to underlying price pressures. CPI median rose from 2.7% yoy to 2.9% yoy, above expectation of 2.7% yoy. CPI Trimmed rose from 2.7% yoy to 2.9% yoy, above expectation of 2.8% yoy. CPI Common also rose from 2.2% yoy to 2.5% yoy, above expectation of 2.2% yoy.

With inflation climbing back above the BoC’s 2% target, speculation about another near-term rate cut has diminished. Unless major economic indicators such as GDP and unemployment show significant signs of deterioration, the central bank would probably pause the easing cycle at its next meeting.

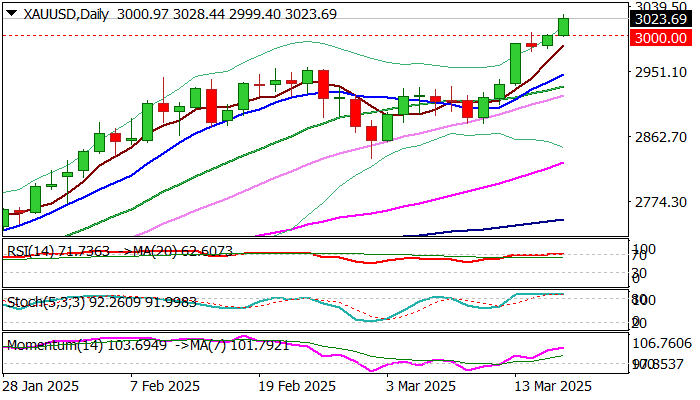

XAU/USD: Gold Hits New Historical High, on Track for Firm Break of $3,000

Gold surged through $3000 level again and hit new record high on Tuesday.

Worsening geopolitical situation on renewed attacks on Gaza area, deepening political crisis between the US and European Union and growing concerns of the magnitude of negative impact of trade war on global economy, added to already fragile overall situation and prompted fresh migration into safety the yellow metal.

Bulls are on track for a firm break of $3000 milestone as favorable fundamentals mainly offset negative signals from broadly overbought technical studies.

Initial target lays at $3032 (Fibo 138.2% projection of the upleg from $2832), followed by $3050 (176.4%) and $3076 (Fibo 200% projection.

Broken $3000 level reverted to initial support followed by higher base at $2980.

Res: 3032; 3050; 3076; 3100.

Sup: 3004; 3000; 2980; 2956.

German ZEW economic sentiment surges to 51.6 on fiscal optimism

Germany’s ZEW Economic Sentiment Index surged from 26.0 to 51.6 in March, exceeding expectations of 48.1. However, the Current Situation Index only saw a marginal improvement, rising from -88.5 to -87.6, well below the forecast of -80.5.

Similarly, in the Eurozone, economic sentiment rose from 24.2 to 39.8, though it missed expectations of 43.6. Current Situation Index barely moved, edging up to -45.2.

ZEW President Achim Wambach attributed the sharp improvement in economic expectations to positive signals regarding German fiscal policy, particularly the agreement on a multi-billion-euro financial package for the federal budget.

This stimulus plan has boosted optimism for key industrial sectors, including metal and steel manufacturing and mechanical engineering, which have been struggling with weak demand and global trade uncertainty.

Another supportive factor for economic optimism has been ECB’s ongoing monetary easing.