Sample Category Title

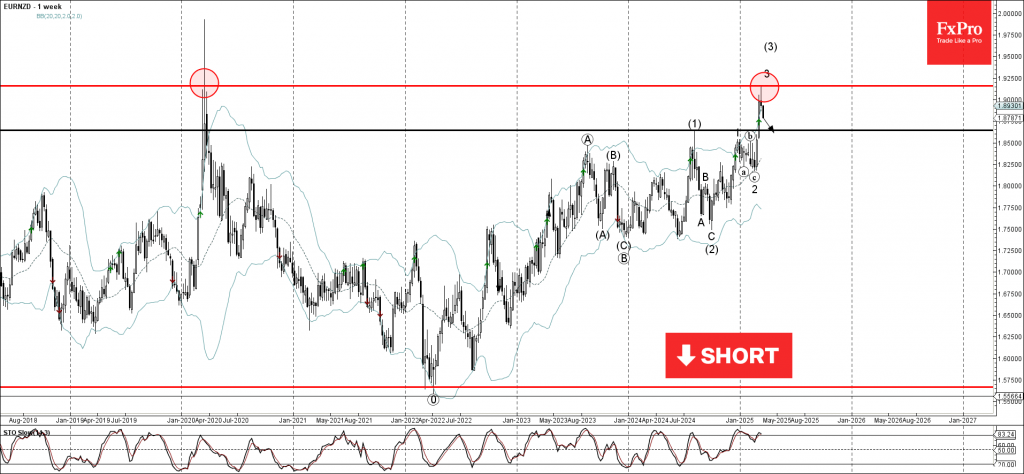

EURNZD Wave Analysis

EURNZD: ⬇️ Sell

- EURNZD reversed from long-term resistance level 1.9160

- Likely to fall to support level 1.8640

EURNZD currency pair recently reversed down from the long-term resistance level 1.9160, which stopped the sharp weekly uptrend at the start of 2020, as can be seen below.

The downward reversal from the resistance level 1.9160 created the weekly Japanese candlesticks reversal pattern Shooting Star.

Given the strength of the resistance level 1.9160 and the bearish divergence on the weekly Stochastic indicator, EURNZD currency pair can be expected to fall to the next support level 1.8640.

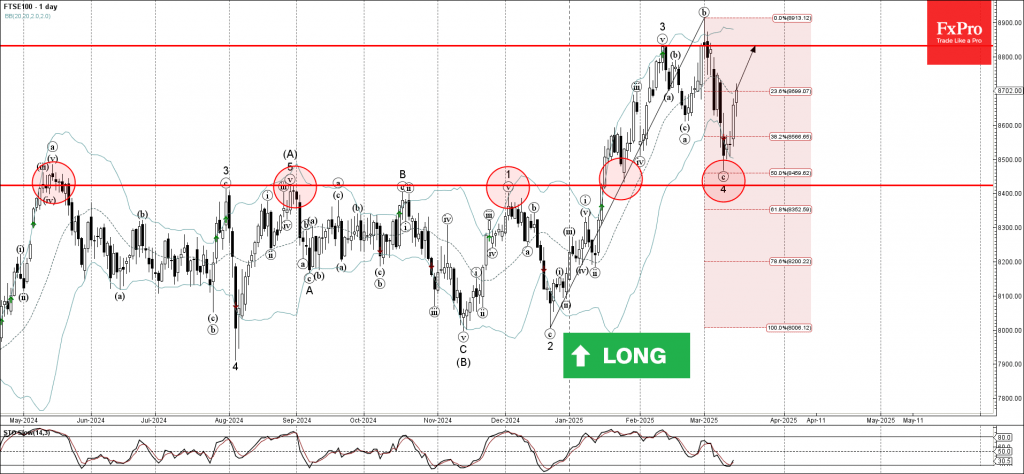

FTSE 100 Wave Analysis

FTSE 100: ⬆️ Buy

- FTSE 100 reversed from key support level 8425.00

- Likely to rise to resistance level 8832.00

FTSE 100 index recently reversed up from the key support level 8425.00, a former strong resistance from last year, which has stopped multiple upward impulses from May to December as can be seen from the daily FTSE 100 chart below.

The support level 8425.00 was strengthened by the lower daily Bollinger Band and by the 50% Fibonacci correction of the sharp upward impulse from December.

Given the clear daily uptrend, FTSE 100 index can be expected to rise to the next resistance level 8832.00 (which reversed the previous waves 3 and b).

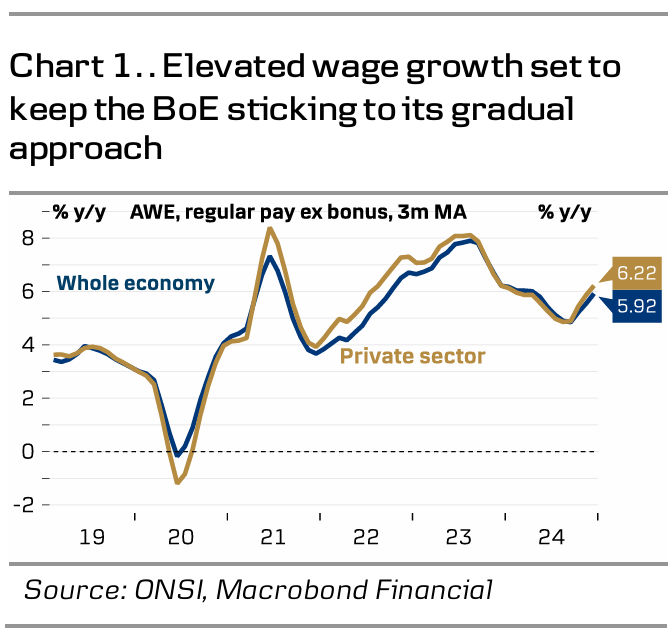

Bank of England Preview – Quarterly Cuts Amid Elevated Uncertainty

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 4.50% on Thursday 20 March in line with consensus and market pricing.

- Data has been mixed and amid elevated uncertainty, this warrants a continued signalling of only a gradual approach to monetary policy easing.

- We expect the reaction in EUR/GBP to be rather muted with risks tilted to the topside.

We expect the Bank of England to keep the Bank Rate unchanged at 4.50% on Thursday 20 March in line with consensus and market pricing. We expect the vote split to be 6-3 with the majority voting for an unchanged decision and Dhingra, Taylor and Mann voting for a cut. Note, this meeting will not include updated projections nor a press conference following the release of the statement.

Overall, we expect the BoE to stick to its previous guidance noting that "a gradual and careful approach to removing monetary policy restraint remains appropriate". We expect the MPC to highlight heightened uncertainty due to domestic fiscal policy initiatives and trade policy tensions. By extension, we expect them to be in no rush to alter the current guidance. Since the last monetary policy decision in February, data has been mixed. The economy continues to stagnate, the labour market is gradually loosening while price pressures continue to be elevated. The economy ended 2024 on a slightly stronger note than in the MPC's projection, growing 0.1% q/q in Q4 2024. However, PMI data and monthly GDP estimate for January signals that growth remains muted, increasing the downside risks to the growth outlook. While private sector wage growth was slightly lower than expected at 6.2% in the three months to September (vs BoE forecast of 6.3%) it remains significantly elevated. On the inflation front, inflation was slightly higher than expected in headline terms but still showed broad based easing when looking at the service sector. The reaction to the impending increase in employers' national insurance contribution from April remains a risk for the labour market.

BoE call. We expect the BoE to stick to quarterly cuts, leaving the Bank Rate at 3.75% by YE 2025, which is lower than markets are expecting. Markets are pricing around 55bp for the remainder of the year. However, we highlight that the risk is skewed towards a swifter cutting cycle in 2025, given the dovish bias within the MPC.

Market reaction. We expect the market reaction to be rather muted upon announcement with an unchanged decision fully expected by markets and the BoE aiming to keep its options fully open. More broadly, we expect EUR/GBP to move lower in the coming quarters driven by a relatively hawkish BoE, and a growth pickup in the UK relative to the euro area in 2025. The key risks are continued elevated uncertainty, more euro optimism and a more forceful policy easing stance from the BoE.

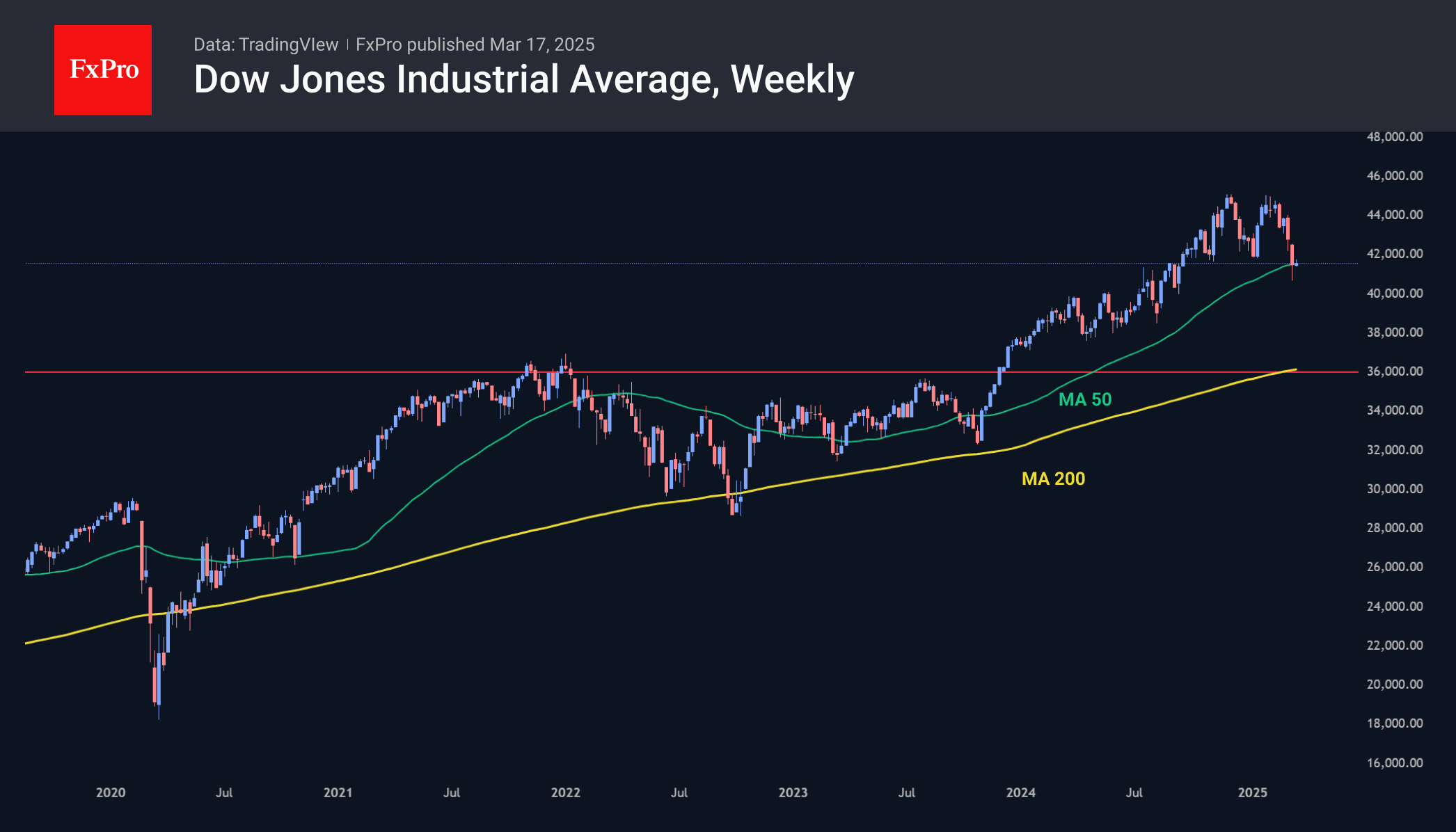

Dow Jones: Rebound or Rally? The Fed Holds the Key

Key US indices staged an impressive rebound on Friday, turning the Dow Jones Industrial Average (DJI) up one step away from formally entering correction territory (-10% from the peak). In doing so, the US economy is headed for recession if the theories coined by the index’s founder and first editor of the Wall Street Journal still apply.

In his theory, Charles Dow pointed out that the trend of the industrial index is correct if confirmed by the dynamics of the transport sector. However, since peaking in late November, the DJTA index has lost nearly 20%, accelerating its decline three weeks ago. The rapid decline has led to the formation of a ‘death cross,’ a bearish market signal when the 50-day moving average dips below the 200-day moving average.

The accumulated oversold conditions in equities over the past three weeks suggests a high chance of a rebound, but how soon that rebound will lose strength will depend on monetary policy and incoming data.

The DJI was down as low as 25 on the RSI index last week. This is an oversold area from where a reversal to the upside was forming in October 2023 and September 2022. However, this technique could be broken or confirmed by market reaction to the FOMC meeting later in the week.

It is within Powell and Co’s power to break the mature beginning of the recovery by softening the tone of comments and promising further rate cuts soon. In this case, the market would be in an attractive position for buyers, who could launch a global rally towards new highs above 45000.

However, downside risks are pretty much equivalent. Since Trump’s presidential election victory, Powell has noticeably tightened his tone: tariffs have a pro-inflationary effect and are operating even with expectations. Friday’s jump in inflation expectations to 2.5-year highs recorded by the University of Michigan doesn’t help matters either.

Consolidation and rebound in the indices are quite fragile right now. Without Fed support, the sell-off could quickly take on threatening proportions, triggering a liquidation of long positions and margin calls that could quickly take the index to 36000.

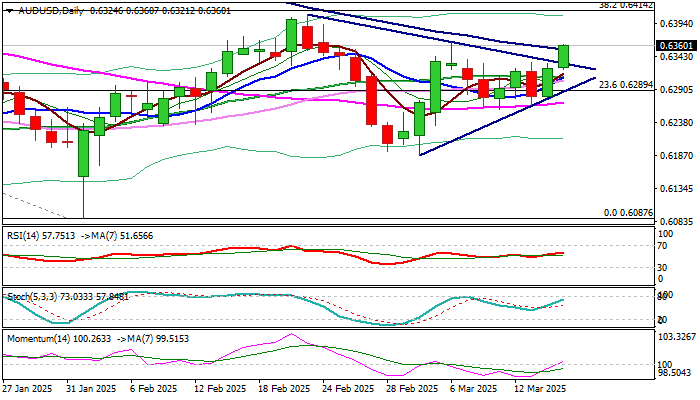

AUD/USD: Bulls Crack Important Barriers

AUDUSD rose to two-week high on Monday, continuing to benefit from weaker dollar and boosted by signals of China’s stimulus plan to boost domestic consumption.

Fresh bulls crack pivotal resistance zone at 0.6353/63 (100DMA / Mar 6 high), with break here to firm near-term structure for attack at more significant barriers at 0.6410/14 (Feb 21 high / Fibo 38.2% of 0.6942/0.6087 downtrend).

Improved technical picture on daily chart (MA’s turned to bullish setup / 14-d momentum is entering positive territory/today’s break above upper boundary of triangle) adds to growing positive signals.

Holding above broken triangle upper boundary (0.6329, now reverted to support) is seen as minimum requirement to keep near-term action in bullish mode, with sustained break 0.6410/14 barriers to signal continuation of larger recovery from 0.6087 (2025 low posted on Feb 3).

Res: 0.6330; 0.6408; 0.6414; 0.6441.

Sup: 0.6329; 0.6307; 0.6295; 0.6269.

Sunset Market Commentary

Markets

Some final input to the Fed policy meeting on Wednesday included February retail sales and the NY’s manufacturing confidence index for March. The former printed mixed, coming in at 0.2% m/m today, missing the 0.6% analyst estimate. In addition, the January print was revised downwards to -1.2%. Core gauges, however, were in line or better than expected. The most important one of them all, the control group (ex. food, gas, building materials and car dealers) used for GDP calculations, rose 1% m/m, the most since September last year and far more than the 0.4% expected. Below the surface, we spot weaknesses in the only services-related category (eating & drinking down 1.5% m/m) while several other categories merely rebounded after a poor January month. The NY confidence gauge for its part fell off a cliff, dropping from 5.7 to -20 (-1.9 expected). The 25.7 point drop came amid falling new orders, shipments and employment. The six-month ahead reading fell for a second-month straight to the lowest in over a year. Prices paid, meanwhile, rose in both series to a two-year (or more) high. It's mounting evidence, after Friday’s consumer confidence, of a potentially stagflationary scenario materializing in the US. This leads to a flatter yield curve with rates up 1.5 bps at the front but 3.5 bps down at the longest maturities (30-yr). The German curve flattens too in a move outperforming Treasuries. Yields at the very long end decline 9.5 bps. Germany’s outgoing parliament officially votes on the huge debt package tomorrow. After securing support from the Greens last week, this should be a non-event. But perhaps markets are closing some Bund-short positions ahead of the deal in a buy the rumour, sell the fact alike move that we in any case don’t expect to go very far. Either way, it’s not hurting the euro, not against the dollar at least. EUR/USD makes another attempt to take out 1.09 with the backing of a risk-on equity climate. Stocks in Europe add 0.7%, Wall Street trades 0.4% higher. The trade-weighted dollar index is holding tight in the very narrow sideways trading range of the last couple of days between 103.37 (November 2024 correction low) and 103.98 (61.8% retracement on the September 2024 – January 2025 rally). Sterling recoups some of Friday’s losses with EUR/GBP 0.84 at stake. JPY underperforms its major peers. USD/JPY rises towards 149. Currencies Down Under are among the top performers today. The AUD (0.635 against USD) and NZD (0.58, highest since mid-December) draw comfort from new stimulus measures announced by China which should support private consumption.

News & Views

The OECD released its interim economic outlook today, titled “steering through uncertainty”. Global GDP growth is expected to moderate from 3.2% in 2024 to 3.1% in 2025 and 3.0% in 2026, with higher trade barriers in several G20 economies and increased policy uncertainty weighing on investment and household spending. Details show a difference between decelerating US and accelerating European growth. Over 2025-26 inflation is projected to be higher than previously expected, although still moderating as economic growth softens. Headline inflation is projected to fall from 3.8% in 2025 to 3.2% in 2026 in the G20 economies. Underlying inflation is now projected to remain above central bank targets in many countries in 2026. Risks to the baseline scenario include the escalation of trade restrictive measures (downside growth, upside inflation). The OECD recommends monetary policy to remain vigilant against inflation risks and calls for fiscal actions to ensure debt sustainability. The latter goes against current political trends. The OECD wants to see ambitious structural policy reforms to improve the foundations for growth.

UK Chancellor Reeves in an interview with Bloomberg defended her fiscal rules in the run up to the government’s Spring statement (March 26): “When we’re spending £100bn a year on servicing government debt, I don’t think anyone could seriously argue that we don’t need to get a grip of government borrowing and government debt”. She’s expected to announce spending cuts (eg social security spending) in order to meet her fiscal rule which requires day-to-day spending to be covered by tax receipts as her £9.9bn buffer from the Autumn budget already evaporated because of higher rates and lower growth forecasts.

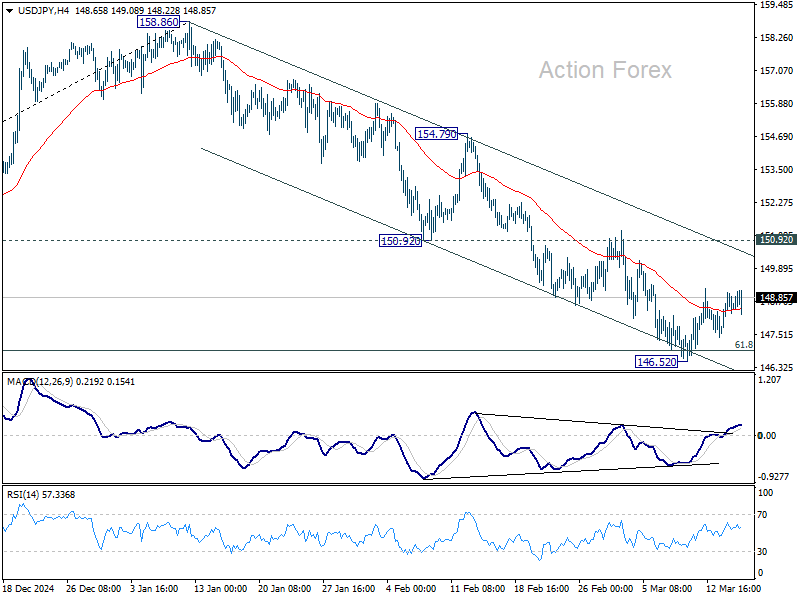

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.89; (P) 148.45; (R1) 149.20; More...

USD/JPY is extending the consolidations above 146.52 and intraday bias stays neutral. Upside of recovery should be limited by 150.92 support turned resistance. On the downside, sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support.

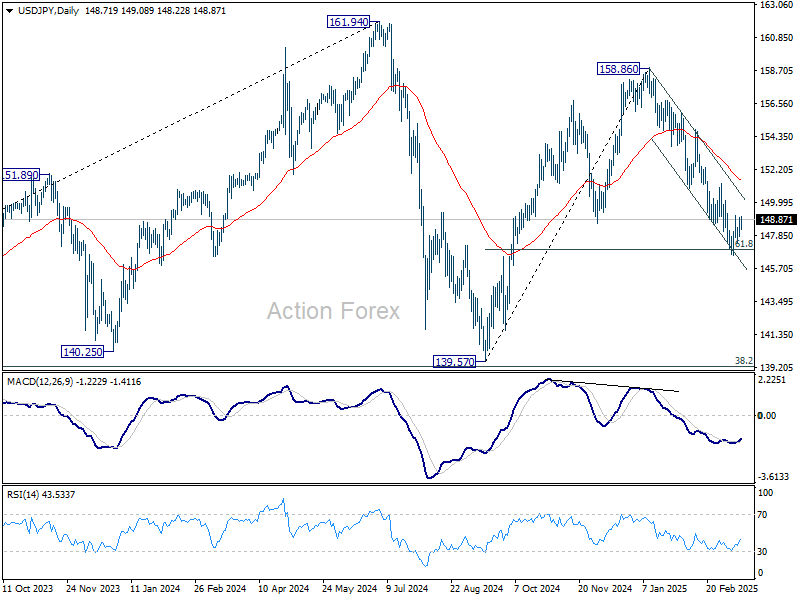

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

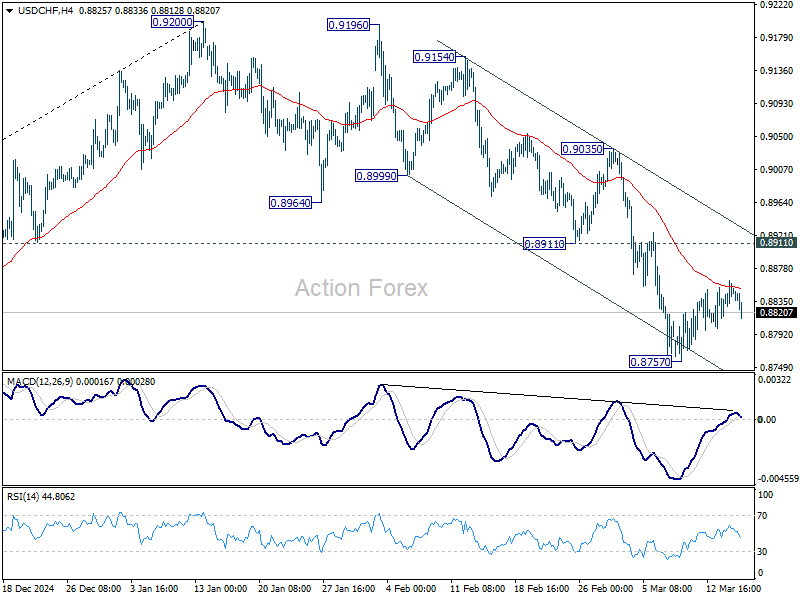

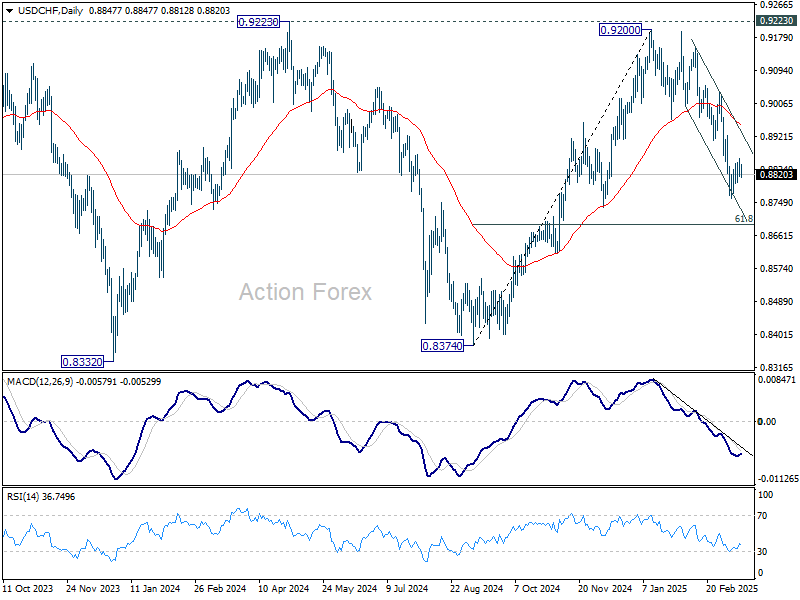

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8823; (P) 0.8844; (R1) 0.8871; More…

Consolidations continues above 0.8757 and intraday bias in USD/CHF stays neutral. Upside of recovery should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

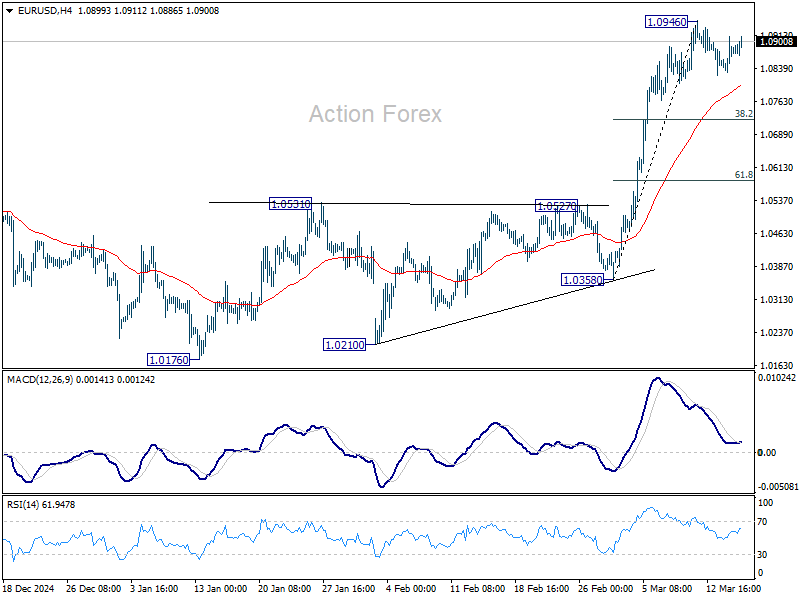

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0874; (R1) 1.0918; More...

EUR/USD is staying in consolidations below 1.0946 and intraday bias remains neutral for now. In case of another fall, downside should be contained by 38.2% retracement of 1.0358 to 1.0946 at 1.0721 to bring rebound. On the upside, break of 1.0946 will resume the rally from 1.0176 to retest 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.