Sample Category Title

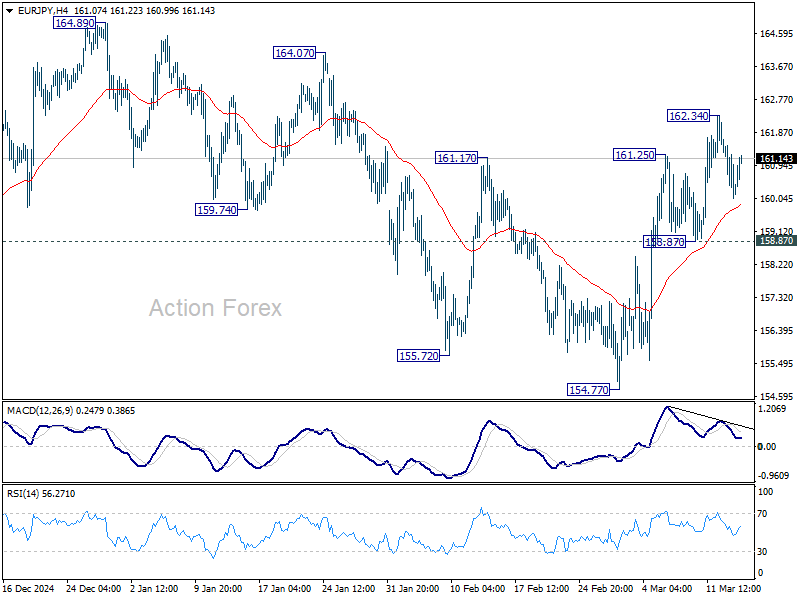

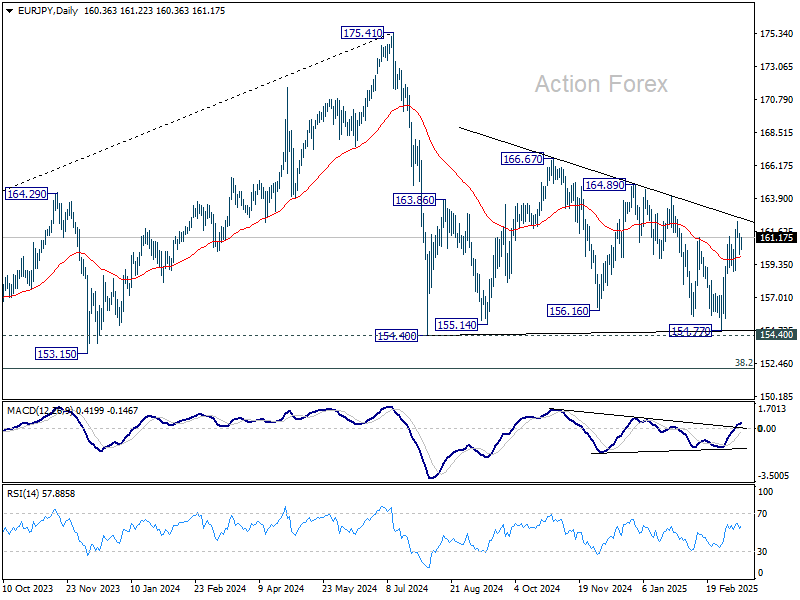

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.80; (P) 160.68; (R1) 161.30; More...

Intraday bias in EUR/JPY remains neutral for consolidations below 162.34. Further rise is expected as long as 158.87 support holds. Above 162.34 will resume the rise from 154.77 to 164.89 resistance, as another rising leg in the consolidation pattern from 154.40.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

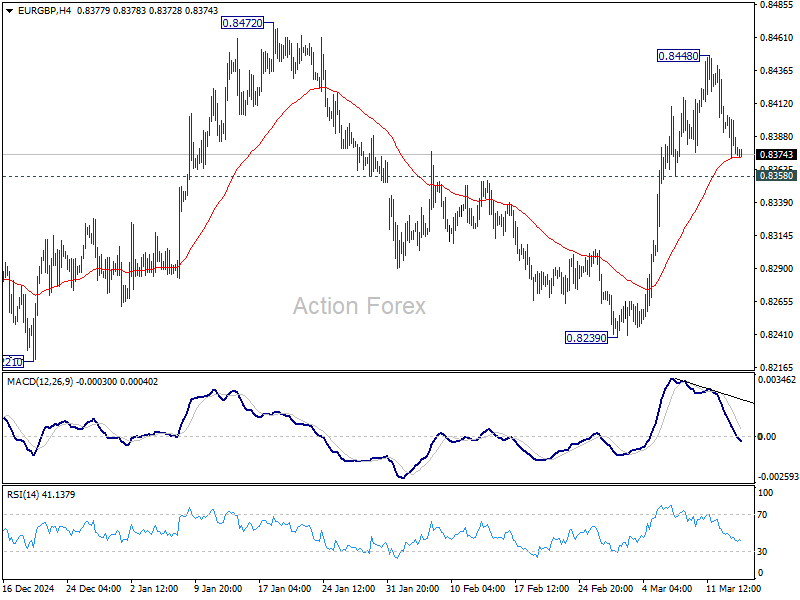

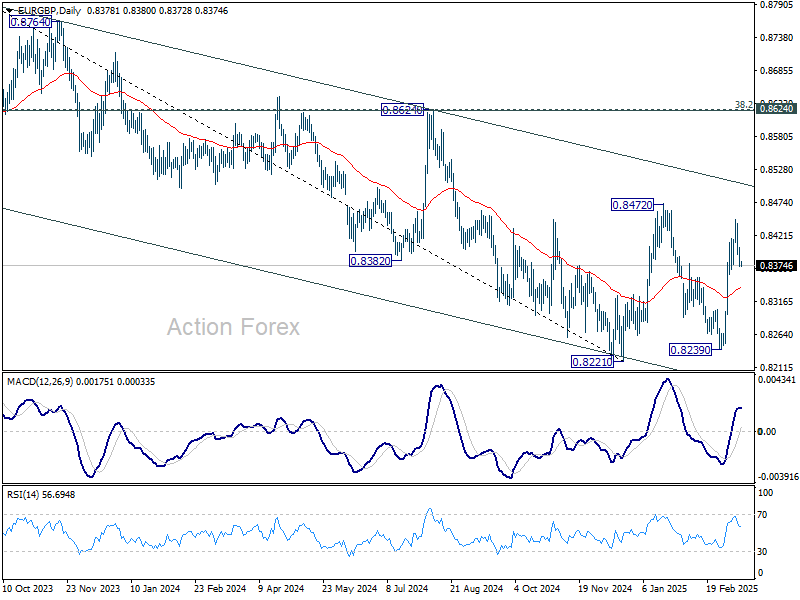

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8366; (P) 0.8387; (R1) 0.8401; More...

Intraday bias in EUR/GBP remains neutral for consolidations below 0.8448. Further rise is expected as long as 0.8358 support holds. Above 0.8448 will target 0.8472 resistance. Firm break there will resume whole rebound from 0.8221 to medium term falling channel resistance. Nevertheless, break of 0.8358 will suggest that rise from 0.8239 has completed and turn bias back to the downside instead.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8506).

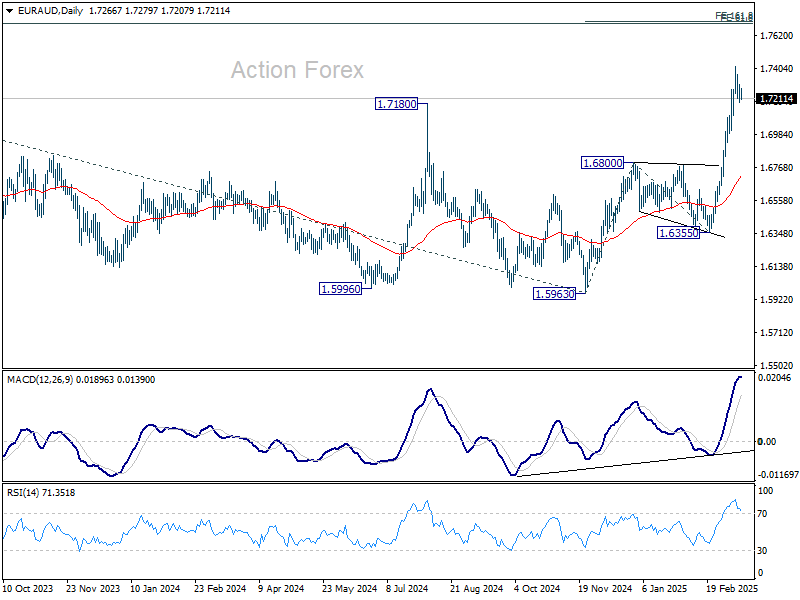

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7204; (P) 1.7256; (R1) 1.7323; More...

Intraday bias in EUR/AUD remains neutral for consolidations below 1.7417. Downside of retreat should be contained by 0.6990 support to bring rebound. Meanwhile, break of 1.7417 will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 key resistance will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6355 support holds, even in case of deep pullback.

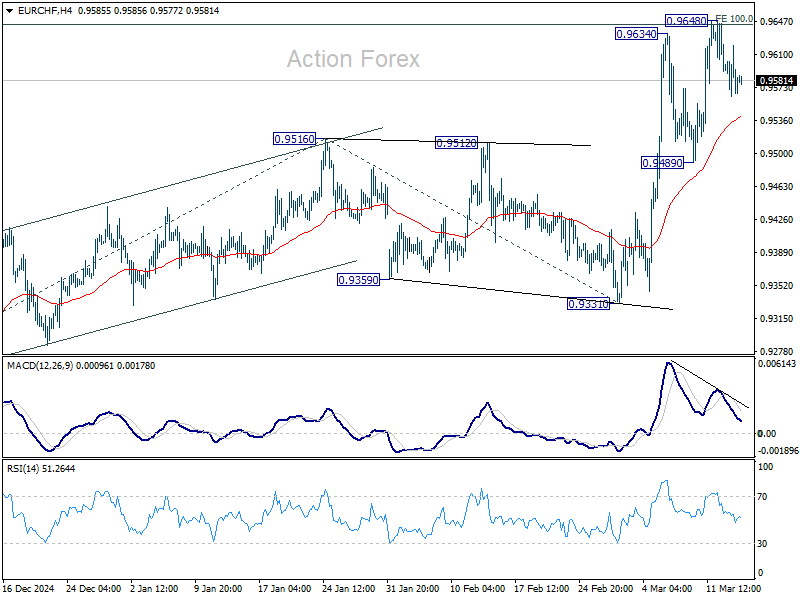

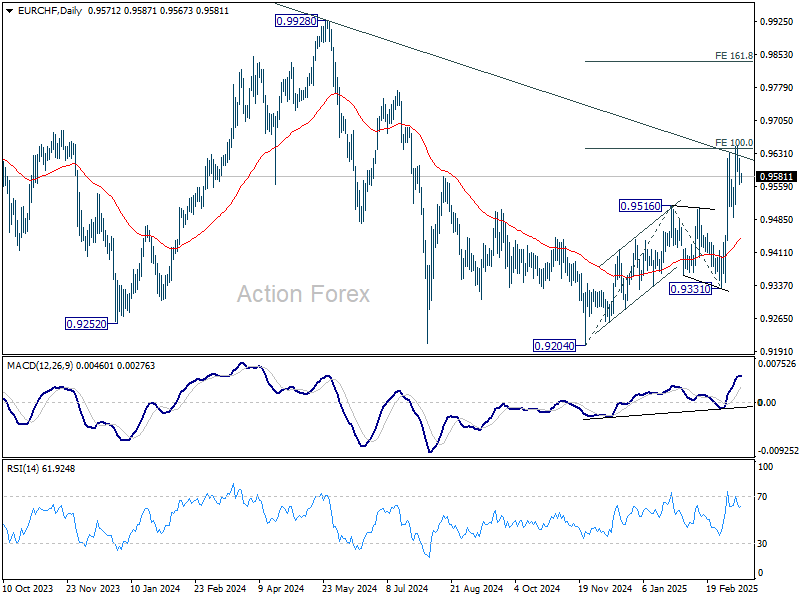

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9549; (P) 0.9586; (R1) 0.9607; More....

Intraday bias in EUR/CHF remains neutral for consolidations below 0.9648. Further rally is expected as long as 0.9489 support holds. On the upside, firm break of 100% projection of 0.9204 to 0.9516 from 0.9331 at 0.9643 will pave the way to 161.8% projection at 0.9836 next.

In the bigger picture, the strong break of 55 W EMA (now at 0.9482) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9620) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be see to 0.9928 key resistance at least.

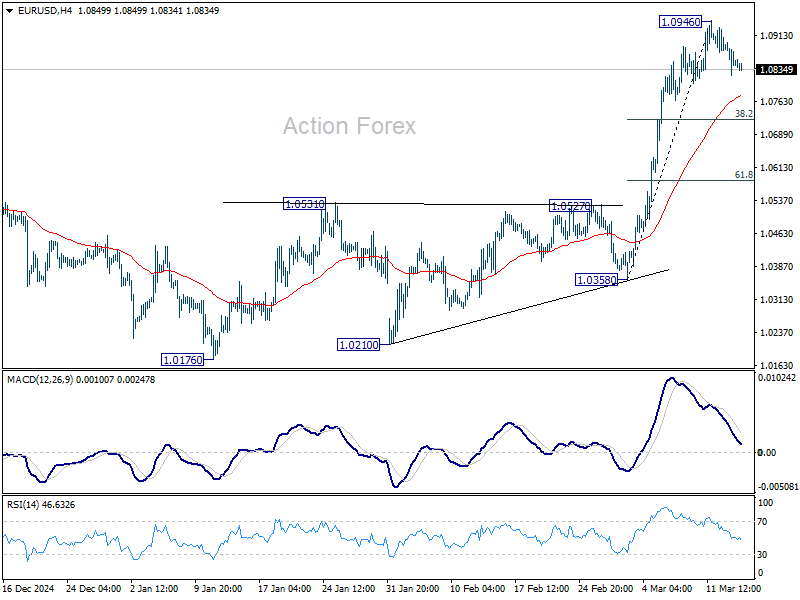

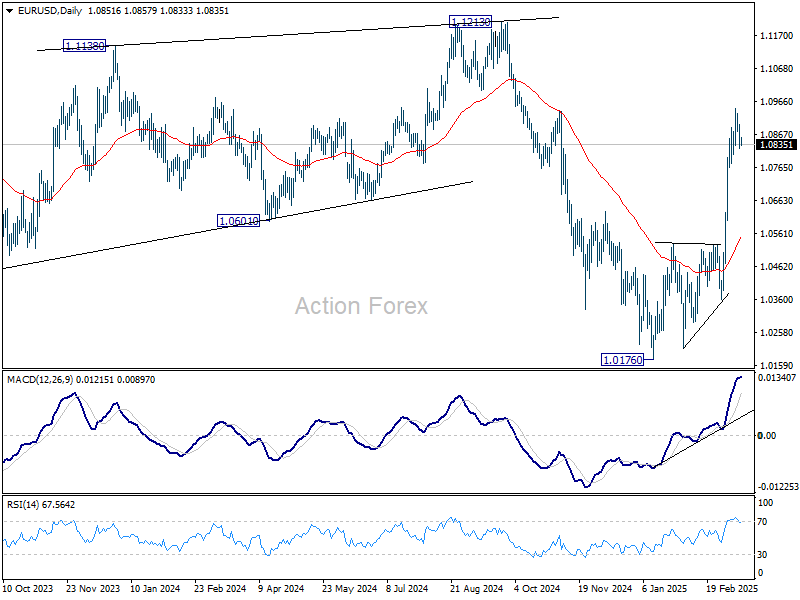

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0818; (P) 1.0857; (R1) 1.0892; More...

Intraday bias in EUR/USD remains neutral for consolidations below 1.0946. Deeper retreat might be seen towards 55 4H EMA (now at 1.0772). But strong support should be seen from 38.2% retracement of 1.0358 to 1.0946 at 1.0721 to contain downside. On the upside, break of 1.0946 will resume the rally from 1.0176 to retest 1.1274 key resistance next.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

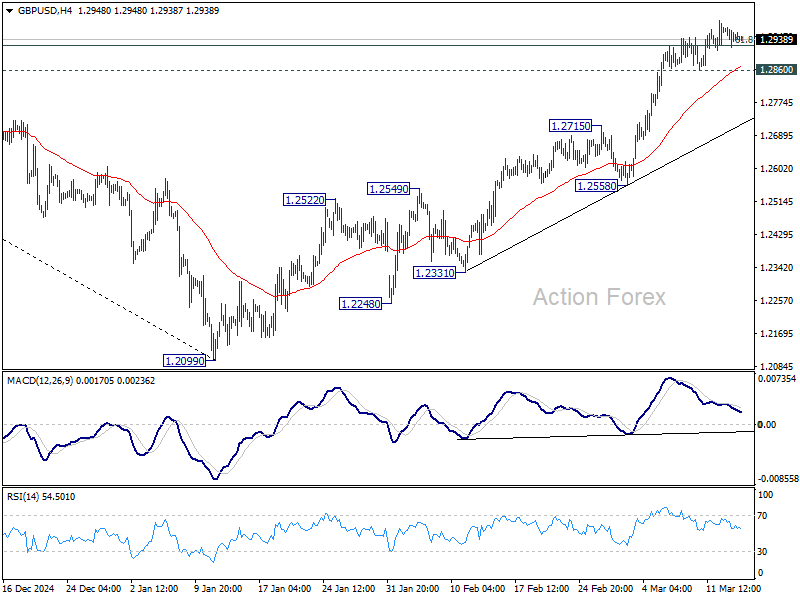

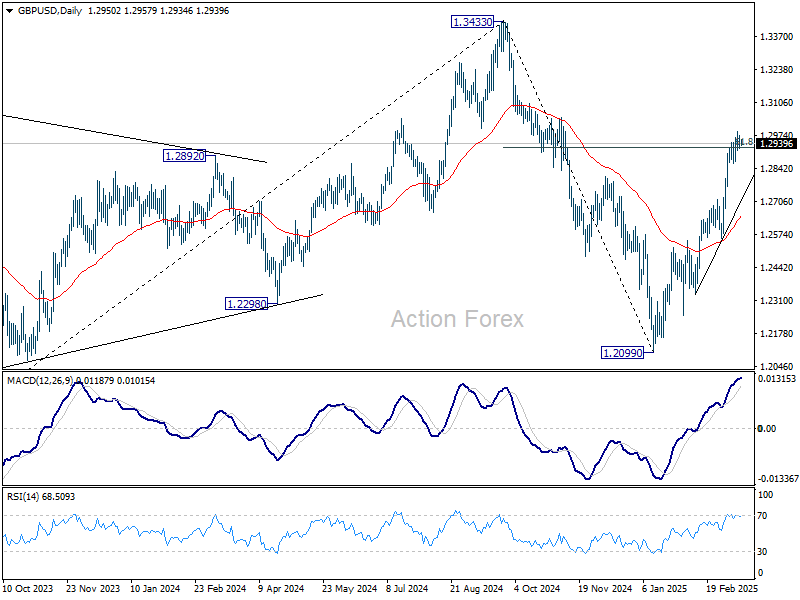

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2923; (P) 1.2949; (R1) 1.2978; More...

No change in GBP/USD's outlook, and further rally is mildly in favor with 1.2860 minor support intact. Sustained trading above 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will resume the rise from 1.2099, and pave the way back to 1.3433 high. Nevertheless, break of 1.2860 support should indicate short term topping and turn bias back to the downside for deeper pullback.

In the bigger picture, fall from 1.3433 (2024 high) should have completed at 1.2099 as a corrective move. Up trend from 1.3051 (2022 low) is still in progress but it's too early to say that it's resuming. Corrective pattern from 1.3433 could extend with one more down leg. But after all, eventual upside breakout is expected at a later stage.

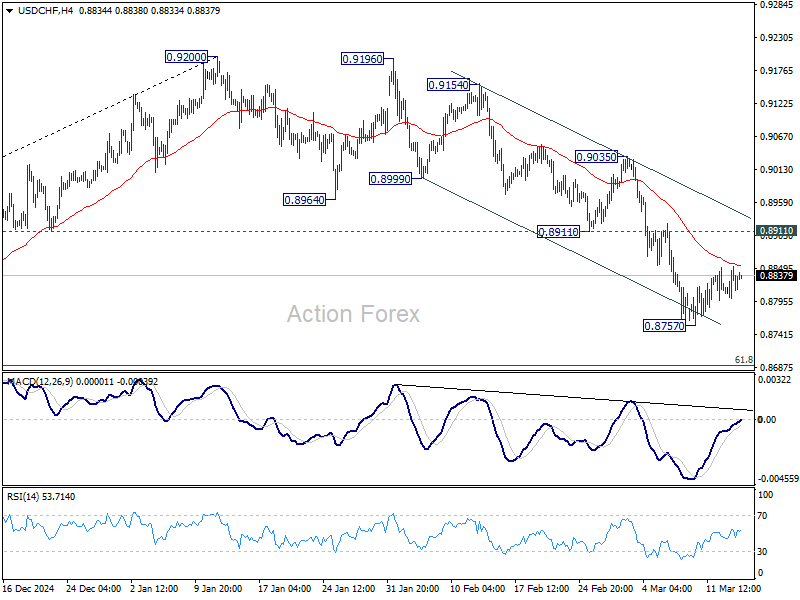

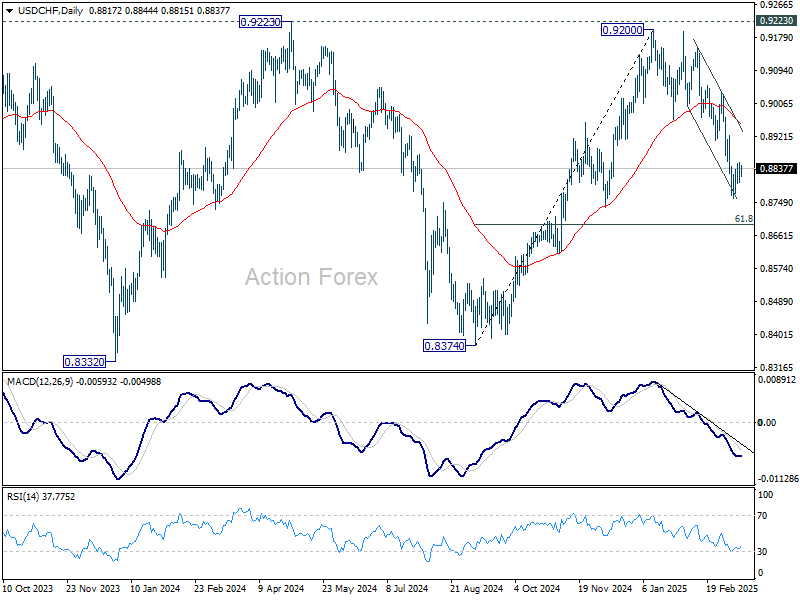

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8798; (P) 0.8827; (R1) 0.8849; More…

Intraday bias in USD/CHF stays neutral. Consolidation from 0.8757 is extending, but upside of recovery should be limited by 0.8911 support turned resistance to bring another fall. On the downside, below 0.8757 will resume the fall from 0.9200 and target 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

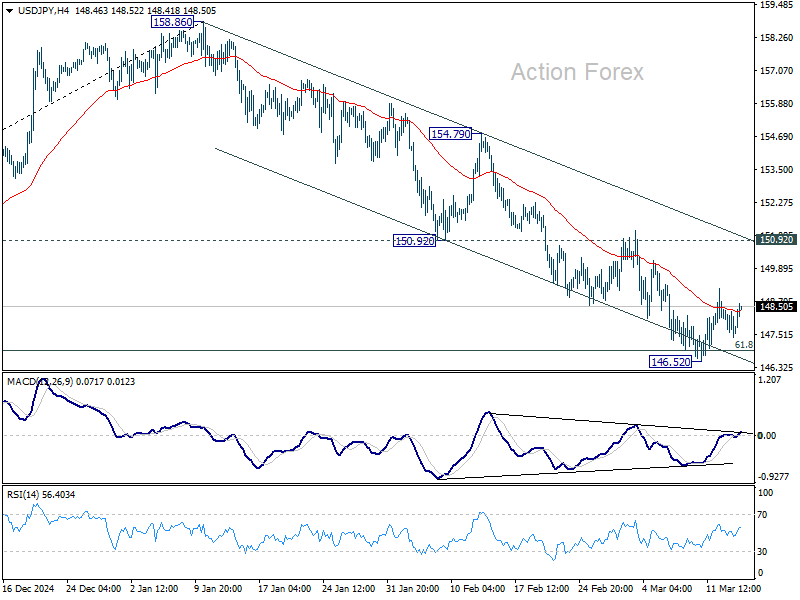

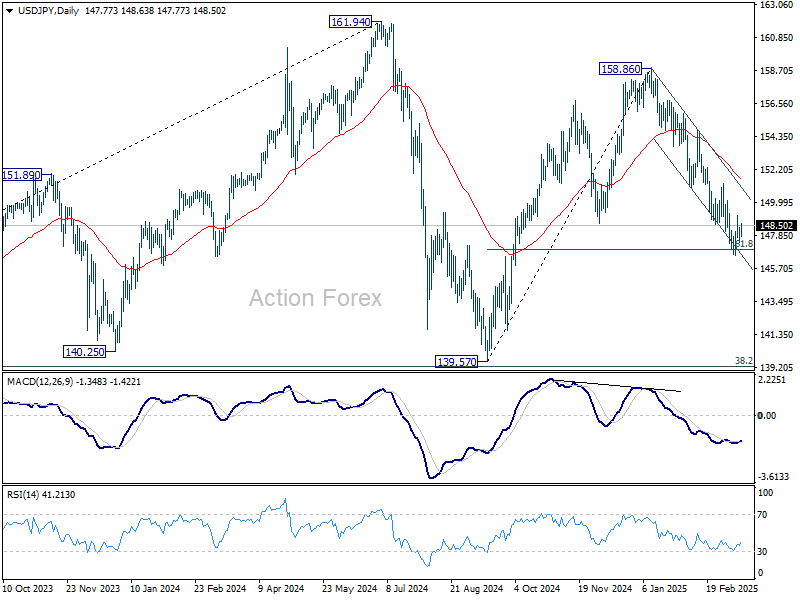

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.35; (P) 147.87; (R1) 148.32; More...

Intraday bias in USD/JPY remains neutral. Consolidation from 146.52 is extending, but upside of recovery should be limited by 150.92 support turned resistance. On the downside, sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

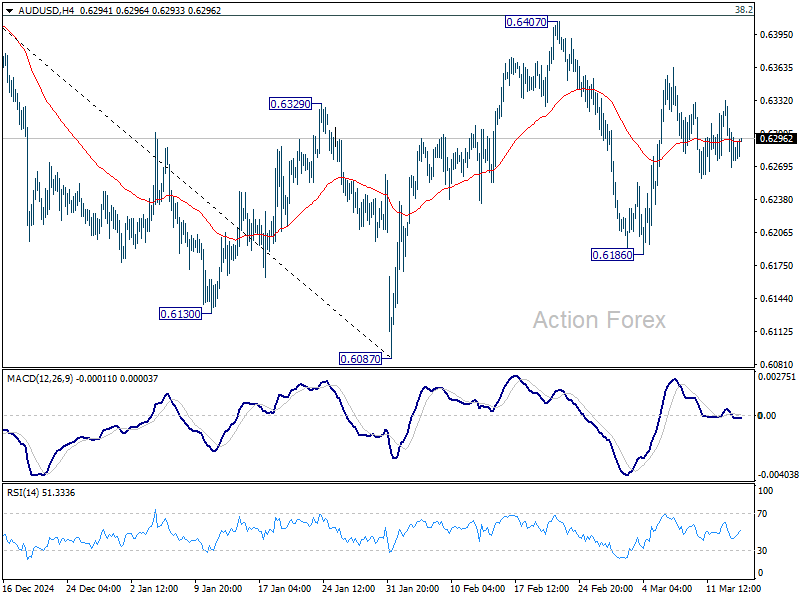

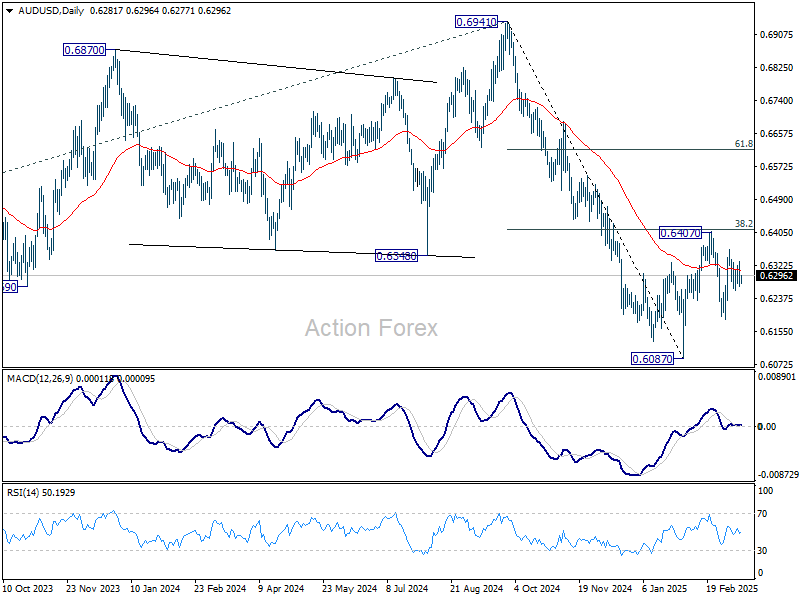

AUD/USD Daily Report

Daily Pivots: (S1) 0.6257; (P) 0.6295; (R1) 0.6322; More...

AUD/USD is still bounded in range trading and intraday bias stays neutral. On the downside, break of 0.6186 will target 0.6087 support first. Firm break there will resume whole decline from 0.6941. However, sustained trading above 38.2% retracement of 0.6941 to 0.6087 at 0.6413 will raise the chance of near term bullish reversal, and target 61.8% retracement at 0.6615 next.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6487) holds.

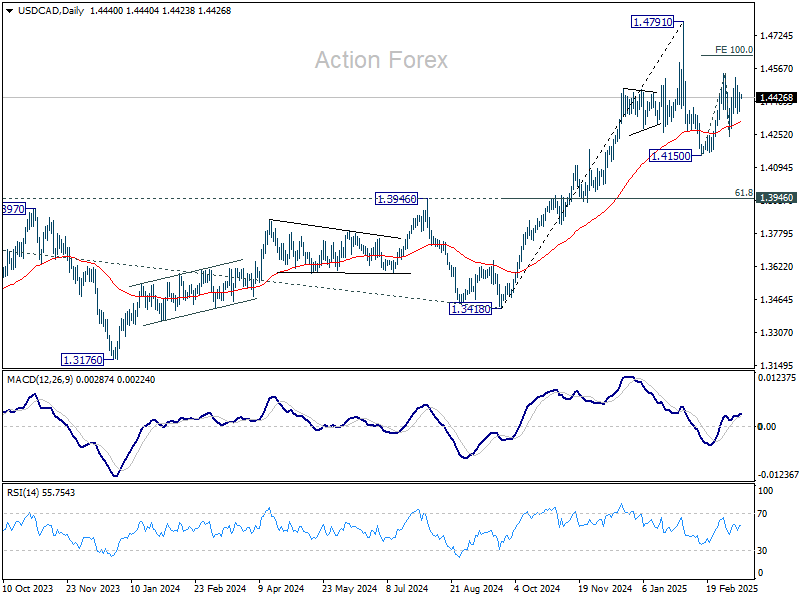

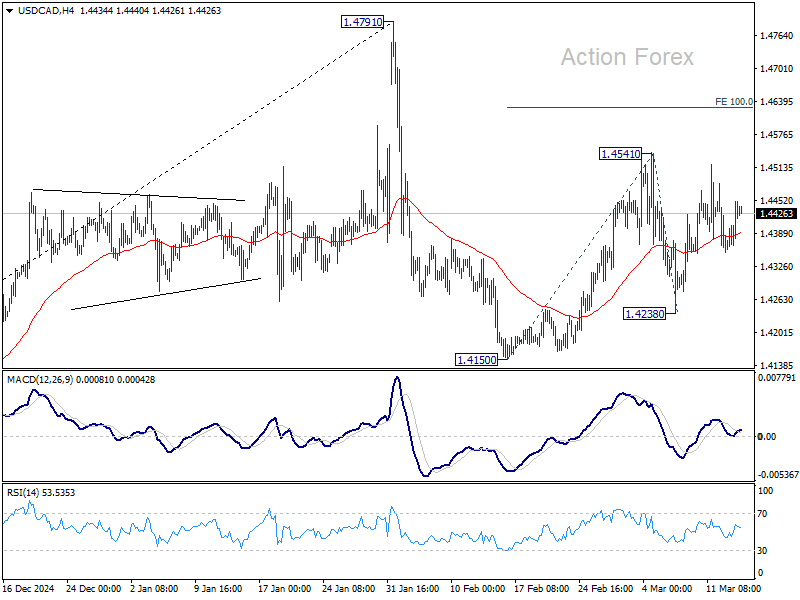

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4384; (P) 1.4418; (R1) 1.4477; More...

Intraday bias in USD/CAD stays neutral as sideway trading continues. Price actions from 1.4791 high are seen as a corrective pattern, with rebound from 1.4150 as the second leg. On the upside, break of 1.4541 will target 100% projection of 1.4150 to 1.4541 from 1.4238 at 1.4629 and above. But for now, strong resistance is expected from 1.4791 to limit upside to bring the third leg. On the downside, break of 1.4238 will confirm that the third leg has started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.