Sample Category Title

BoJ’s Ueda acknowledges rising yields as market bets on policy shift

BoJ Governor Kazuo Ueda addressed the recent rise in bond yields, and noted, "I don't see a big divergence between our view and that of markets".

Speaking to parliament, Ueda emphasized the "biggest determinant" of long-term interest rates is market expectations regarding the central bank’s short-term policy rate.

He added, it is "natural for long-term rates to move in a way that reflects such market forecasts". His comments come as Japan’s benchmark 10-year bond yield surged to a 16-year high of 1.575% on Monday.

Separately, Japan’s latest inflation data showed that annual wholesale inflation slowed slightly in February. Corporate goods price index , which tracks the prices businesses charge each other for goods and services, rose 4.0% yoy, in line with market expectations, down from January’s 4.2% yoy increase.

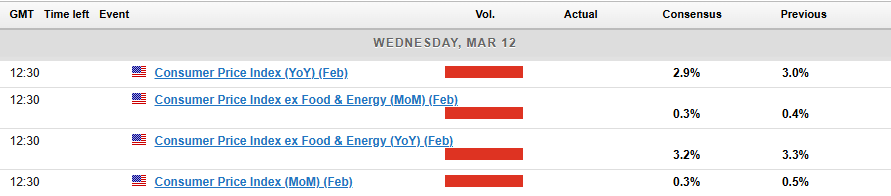

US CPI Release Today: What to Expect and Market Reactions

- Economists expect a slight slowdown in both overall and core CPI.

- Tariffs and potential future universal tariffs are a key concern, adding to price pressures and raising fears of stagflation and a possible recession.

- The US Dollar Index is currently struggling technically, with the 14-period RSI in oversold territory.

US CPI inflation data will be released on Wednesday March 12 at 12h30 GMT time. Markets are paying close attention to the release as it may offer insights into the trajectory of inflation amid an economy balancing persistent price pressures and emerging signs of a slowdown.

What are Markets Expecting from the CPI Data?

Economists expect February’s overall CPI to go up by 0.3% compared to last month, slowing down from January’s 0.5% increase. This slowdown would bring yearly inflation down to 2.9% from January’s 3.0%, marking the first time it has dropped below 3% since early 2023.

For core CPI, which leaves out food and energy prices, forecasts also point to a 0.3% monthly rise. Annually, core inflation is expected to slightly ease to 3.1% from 3.3% in January.

While this suggests inflation might be slowing, there are mixed signals in the economy. Wages are growing faster than expected, but costs for services are coming down, and demand in some key industries is weakening. This creates an unclear picture for where inflation is headed while inflation expectations have shown significant increases off late.

A Market at a Crossroad – Why This CPI Print Matters

Inflation trends are important for Federal Reserve decisions and financial markets. The Fed is focused on bringing inflation down to its 2% target, but unexpected changes in recent economic data have made things more uncertain. Recessionary fears have also muddied the outlook on Fed rate policy moving forward.

Markets are keeping a close eye to see if inflation will keep slowing or start rising again as tariffs are now playing a key role.

The imposition of tariffs on imports from Canada, Mexico, and China has raised concerns about future price pressures. These tariffs could add to goods inflation as businesses pass higher costs on to consumers.

There have also been warnings from President Trump that universal tariffs are still scheduled to come into effect on April 2, 2025. This would add just another layer of intrigue, while at the same time spur on fears of a potential recession.

Stagflation Concerns Loom

Stagflation, where the economy slows down but prices stay high, presents a tough challenge. If this happens, the Federal Reserve would have fewer options to manage the situation. Economists say that long-lasting tariffs and issues in the job market could make things worse. US data of late has been softer than expected while some companies have issued warnings around prospects for the next 12 months adding to the stagflation narrative.

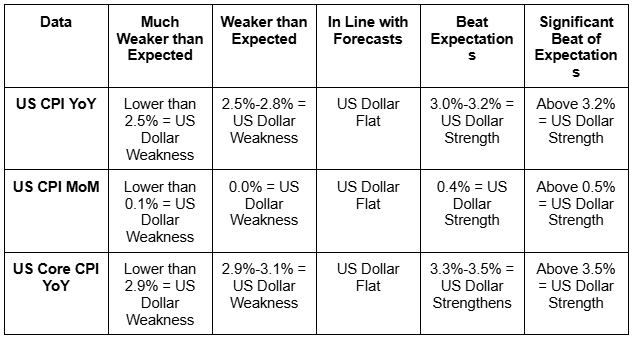

Potential Market Impact

Looking at the potential scenarios from the CPI release, I have created a table that may help. Now this of course is no guarantee as to how the market may react but rather my take on the potential movements that could materialize.

Source: LSEG, TradingEconomics. Table created by Zain Vawda

The above table provides an insight into what I expect will happen depending on the CPI prints released later in the day.

My personal expectations are that the data will land quite close to expectations which could lead to some short-term volatility and whipsaw price action before markets settle down.

Technical Analysis

US Dollar Index (DXY)

From a technical standpoint, the US Dollar Index has struggled and continues to do so. The index is trading below the levels it did when the US election took place on November 5 2024.

The only positive for the US Dollar at the moment is that the 14-period RSI is in oversold territory. A sign that a recovery may be around the corner?

However, as we know the RSI could hover in oversold territory for extended periods of time.

The CPI print will definitely stoke some volatility but at present the tariff and geopolitical developments are overshadowing data releases.

Given that there is the possibility that any move may prove short-lived as tariff developments and comments are coming through thick and fast.

Immediate resistance rests at 103.650 and 104.00 before the confluence level at 105.00.

Immediate support rests at 103.170 and 103.00 before the 102.65 and 102165 handle comes into play.

US Dollar Index Daily Chart, March 11, 2025

Source: TradingView (click to enlarge)

Support

- 103.17

- 103.00

- 102.65

Resistance

- 103.65

- 104.00

- 105.00

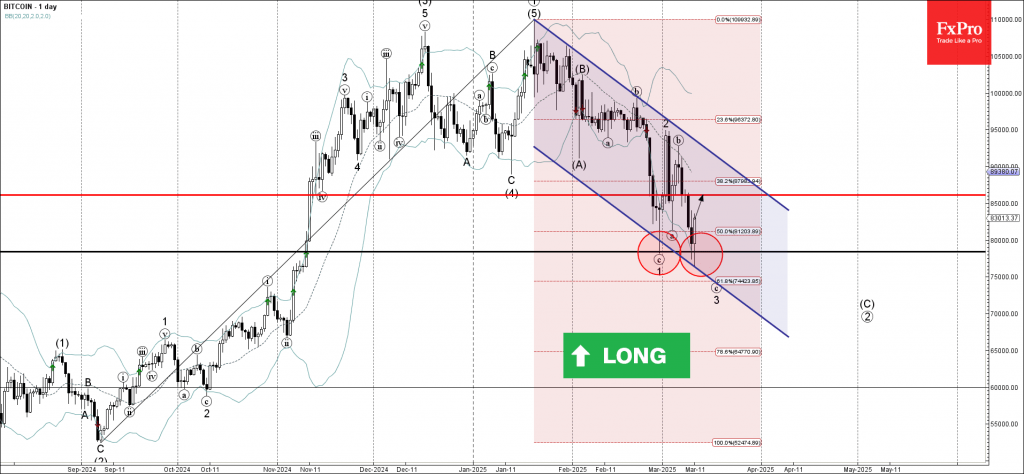

Bitcoin Wave Analysis

Bitcoin: ⬆️ Buy

- Bitcoin reversed from pivotal support level 78375.00

- Likely to rise to the resistance 85000.00

Bitcoin cryptocurrency recently reversed up from the support area between the pivotal support level 78375.00 (which formed the daily Hammer in February), the support trendline of the daily down channel from January and the lower daily Bollinger Band.

The upward reversal from this support area is expected to form the daily Japanese candlesticks reversal pattern Bullish Engulfing (strong buy signal for Bitcoin).

Given the long-term uptrend, Bitcoin can be expected to rise to the next resistance level 85000.00.

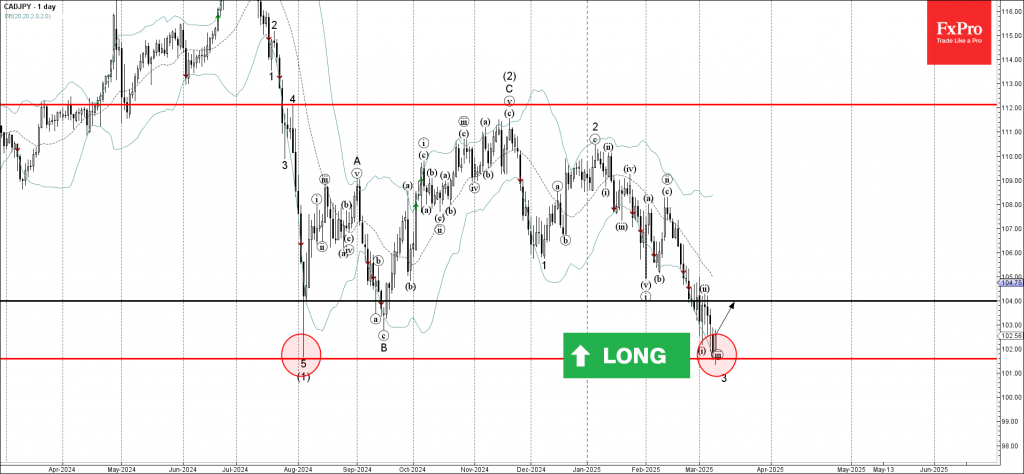

CADJPY Wave Analysis

CADJPY: ⬆️ Buy

- CADJPY reversed from the support area

- Likely to rise to the resistance level 104.00

CADJPY currency pair recently reversed up from the support area between the major long-term support level 101.60 (former multi-month support from August) and the lower daily Bollinger Band.

The upward reversal from this support area will likely form the daily Japanese candlesticks reversal pattern Bullish Engulfing.

Given the strength of the support level 101.60, CADJPY currency pair can be expected to rise to the next resistance level 104.00 (former top of wave ii).

Key CPI Data: Impact on EURUSD and Fed

Fundamental Analysis

The EURUSD pair has recently surged, surpassing the 1.09 mark, driven by growing concerns of a US recession that have weakened the dollar. These fears intensified after Citigroup downgraded US stocks to neutral, citing bearish market signals. Additionally, uncertainty surrounding US trade policies—including new tariffs set to take effect on April 2—has caused market jitters on Wall Street and contributed to dollar volatility.

Meanwhile, the euro has strengthened, reaching its highest level since November, supported by a slight recovery in European markets and a shift in ECB President Christine Lagarde’s stance, highlighting the risks the European Union faces due to US trade policies.

Market attention is now focused on the US Consumer Price Index (CPI) data, set to be released tomorrow, March 12. February’s annual inflation rate is expected to slightly decline to 2.9% from January’s 3%, though it remains above the Federal Reserve’s 2% target. This report is crucial ahead of the Fed’s March 18–19 policy meeting, as persistently high inflation could limit the central bank’s ability to implement further stimulus amid growing economic concerns. Additionally, food prices have shown significant increases, with expectations of a 0.6% rise in February, which could influence monetary policy decisions. Investors will be closely monitoring this data to assess the future direction of the dollar and the EUR/USD pair.

Technical Analysis

EURUSD, H4

Supply Zones (Sell): 1.10

Demand Zones (Buy): 1.0855 / 1.0765 / 1.07

Price continues to rally past 1.09, activating 1.0805 as the last validated intraday support and forming a volume concentration around 1.0855. This level acts as a local demand zone, potentially triggering new buy orders to push the pair towards November’s resistance at 1.0937 and ultimately testing the key psychological level at 1.10.

This bullish scenario may gain traction if the upcoming CPI data confirms a decline. However, if inflation data surprises to the upside—exceeding market expectations—the price could fall towards the last validated intraday support at 1.0805. A confirmed break below this level would signal a trend reversal.

Technical Summary

Bullish Scenario: Buy positions above 1.0855 with targets at 1.09, 1.0940, 1.0950, and an extended move to 1.10.

Bearish Scenario: Sell positions below 1.10 as a correction towards 1.0950. Additionally, early sell signals if the price drops below 1.0950, extending declines to 1.08, with further downside potential towards 1.0765 and 1.07.

Discovered POC (Point of Control):

The POC is the price level with the highest volume concentration. If a previous bearish move originated from this zone, it acts as a resistance (sell zone). Conversely, if an upward impulse began there, it serves as a support (buy zone), typically located at lows.

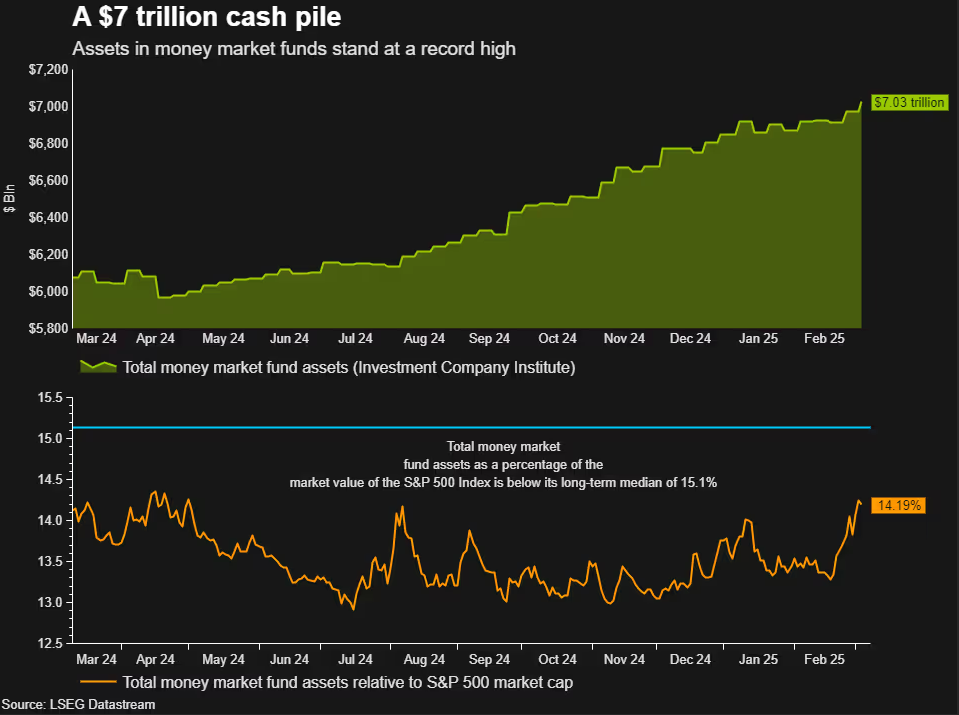

Dow Jones (DJIA), S&P 500 Under Pressure as Record Cash Levels Suggest More Downside Ahead

- Investors are holding record levels of cash ($7.3 trillion), indicating significant caution and potential for further market downside.

- Concerns about the Trump administration’s tariffs and policy uncertainty, including the threat of universal tariffs, are weighing on market sentiment.

- S&P 500 recorded its biggest one-day drop since December.

Wall Street Indexes have recovered overnight but investors remain cautious. This is evidenced by data from the Investment Company Institute. According to the data, cash levels are high with assets at money market funds at a record.

Cash levels climbed steadily last week, reaching a record high of $7.3 trillion, according to Peter Crane, president of Crane Data, a firm specializing in tracking market flows. This marks an increase from approximately $7.17 trillion at the start of 2025, Crane noted.

This could in part be why recent dips have not enjoyed significant bounces as they did in the past.

Source: LSEG

Markets have bounced somewhat this morning following yesterday which turned out to be the biggest one-day drop this year for Wall Street’s main Indexes. The S&P 500 had its biggest one-day drop since December 18 because of worries that the Trump administration’s tariffs might lead to a serious trade war.

The Nasdaq also saw its largest percentage drop since September 2022. It had already fallen 10% from its peak late last week.

Altogether, the market selloff wiped out $4 trillion in value from the S&P 500’s high point just a month ago.

The optimism around a Trump Presidency appears to be fading as the uncertainty of tariff policy is now starting to affect and dampen sentiment. The constant flip-flopping around policy has left market participants unconvinced and does not inspire confidence.

The threat of universal tariffs still in the pipeline for April has added to the uncertainty and increased bets of a recession. This is also weighing on sentiment.

All of these developments have led to the CBOE Volatility index closing at its highest level since August.

A snapshot of Market Performance paints a dour picture.

Source: LSEG (click to enlarge)

Adding to the gloomy outlook, Citi was the latest brokerage to change its view on U.S. stocks. It downgraded its recommendation from “overweight” to “neutral” while upgrading Chinese stocks to overweight.

US Data Ahead & Funding Bill in Focus

On the day front, focus will now shift to Jobs data with job opening and labor turnover survey due later in the day. Market participants will also be keeping a watch on Capitol Hill as voting begins for a funding bill to avoid a partial Federal Government Shutdown.

All of this comes ahead of the highly anticipated CPI release due tomorrow.

Overall sentiment does not seem all that bright moving forward with the potential for further losses growing.

Technical Analysis

Dow Jones

From a technical standpoint, the Dow Jones remains in a bearish trend and continues to break through crucial support levels.

Any attempted push higher has been met with significant selling pressure as dip buyers have not come to the fore. A sign of the current cautious approach we are seeing by market participants.

The Dow is trading at levels last seen in September 2024 after yesterdays 900-odd point move.

Gains from earlier in the day have now been wiped away as the Dow trades below support at the 42000 handle with the next level of support of resting at 41400 before the 41000 handle comes into focus.

Immediate resistance rests at 42000 before the 42446 and 42764 handles comes into focus.

The 14-day RSI is currently in oversold territory and thus a short-term bounce cannot be ruled out.

Dow Jones (US30) Daily Chart, March 11, 2025

Source: TradingView (click to enlarge)

Support

- 41400

- 41000

- 40738

Resistance

- 42000

- 42446

- 43402

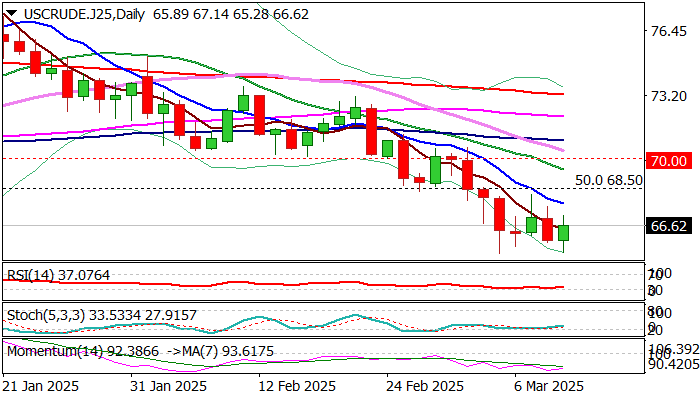

WTI Oil – Consolidation/Limited Correction to Precede Fresh Push Lower

WTI oil price bounces on Tuesday following repeated downside rejection at key support at $65.26 (Sep 10 low), but recovery is likely to be limited, as larger picture is bearish and fundamentals predominantly negative.

Oil sentiment is firmly negative on growing concerns about the impact of tariffs on global economy, fears that the US economy is heading into recession and plans of OPEC + group to increase production in April.

Situation on daily chart points to firm bearish setup of technical studies, with triple recovery stall falling under 10DMA (daily candles with long upper shadows) contributing to negative scenario.

Near term action, however, may hold in prolonged consolidation above $65.26 support, which should be ideally capped by falling 10DMA ($67.75), but extended upticks (cannot be ruled out) to stay capped under psychological $70 barrier and mark healthy correction before larger bears regain full control.

Markets focus on releases of crude inventories reports (API and EIA) for fresh signals.

Res: 67.75; 68.20; 68.50; 69.44

Sup: 65.26; 65.00; 64.34; 63.63

Sunset Market Commentary

Markets

Bunds continued their underperformance vs US Treasuries as well as against swap. German rates add another 4 bps in a bear steepening move that’s still the result of last week’s dramatic fiscal policy U-turn. Its importance simply cannot be overstated and it’s unambiguously good news for Europe, European rates and the common currency. The German fiscal envelope (€500bn special fund, defense expenditures exempted from the debt brake and easier spending rules on a local & state level) is subject to approval by the Greens, which are needed to deliver the two-third majority. While they don’t agree to the proposal as it is in its current state, their opposition is not at all unsurmountable. If anything, we think it’ll only lead to an even bigger cheque that includes some green sweeteners. Its co-leader today in any case said she’s hopeful of a deal this week. The German 10-yr yield is on track for its highest close since 2023Q4. US yields trade 2 bps lower in whipsawed trading. They continue to look vulnerable at the downside. The euro remains in the driver’s seat. EUR/USD rallies to north of 1.09, the strongest level since November 2024. Barring some intermediate resistance levels around 1.0961 and 1.10, the road towards 1.1214 is wide open. The US dollar in any case won’t stop the common currency. The greenback remains in the defensive with local/US cyclical worries riding high. These get compounded by increasing talk of the US losing its exceptionalism status that catapulted the dollar towards the world’s reserve currency (and kept bond yields lower than they otherwise would be). The trade-weighted DXY index tanks to new YtD lows around 103.37 and is testing the November 2024 correction low in the process. EUR/USD’s 1.1214 mirror image in DXY is 100.157. The Japanese yen is taking a breather after a nice run over the last couple of days. USD/JPY tested the 148 area. US eco data was limited to JOLTS job openings, where a small January beat was offset by a similar-sized December downward revision. Small business optimism (NFIB) fell for a second month from it’s 5-yr high to 100.7 on concerns about inflation and uncertainty on tariffs and trade wards that’s leaving business owners in a wait-and-see mode. President Trump’s fresh announcement is a case in point. He’s doubling the steel and aluminum tariffs on Canadian steel to 50%, effective tomorrow, in a response to Canada’s levy on electricity exports to the US. The CAD loses ground and with Trump’s announcement dies a shy, unconvincing attempt by US equities (-0.9% to -1.4%) to find a bottom after yesterday’s knockout punch. European equity losses mount to 1.7%.

News & Views

Inflation in Hungary in February printed at 0.8% M/M and 5.6% Y/Y (1.5% M/M, 5.5% Y/Y in January), substantially outpacing expectations again. Food prices (1.2% M/M, 7.1%Y/Y) were a factor beyond the overall rise. However, the national bank of Hungary (MNB) analyses that most product groups were contributing to the rise in core and headline inflation. Core inflation rose 0.4% M/M and 6.2% Y/Y. Monthly changes were above historical averages. Inflation of sticky-price products and core inflation excluding processed foods stood at 5.8% Y/Y. Prices of tradeable goods increased 0.3% M/M and 2.4% Y/Y. Prices of market services also showed a strong upward dynamic (0.9% M/M, 9.9% Y/Y). The MNB adds that households’ inflation expectations remain high. Corporate expectations also confirm an upward trend since October. Mihaly Varga, who became MNB governor last week, already indicated that there was no room to ease the policy rate (currently 6.5%) in the near future. The 2-y swap yield jumped 7 bps (6.44%). Prime Minister Orban said the government will cap profit margins of retailers on 30 basic food products to 10% from mid-March to end May. The forint weakened to EUR/HUF 400 after testing the 398 area yesterday.

In its quarterly economic report on the Spanish economy, the Bank of Spain today upwardly revised its expectations for both 2025 economic growth and inflation. GDP growth expectations were raised from 2.5% in December to 2.7%. Aside from a positive overhang from last year, the Bank of Spain sees the outlook for household income now being better than in December, which could have a positive effect on consumption. Inflation is revised by 0.4 pp compared to 2.5%. While substantial, this upward revision is mainly due to expected higher energy costs. The bank sees risks slightly skewed to the upside. It keeps a close eye on domestic inflationary pressures.

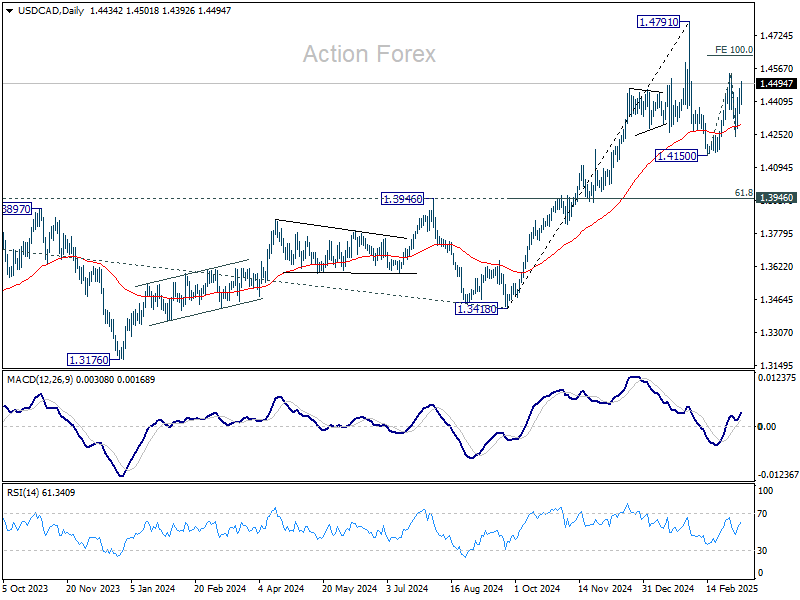

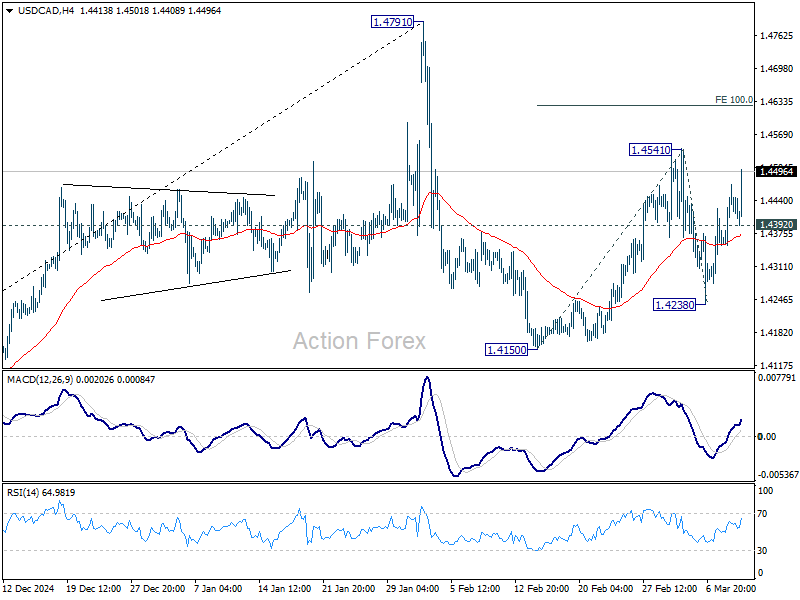

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4370; (P) 1.4422; (R1) 1.4490; More...

USD/CAD's current upside acceleration argues that rise from 1.4150 is already the second leg of the corrective pattern 1.4791 high. Break of 1.4541 will target 100% projection of 1.4150 to 1.4541 from 1.4238 at 1.4629 and above. But for now, strong resistance is expected from 1.4791 to limit upside to bring the third leg. Meanwhile, below 1.4392 will turn bias to the downside for 1.4238 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.