Sample Category Title

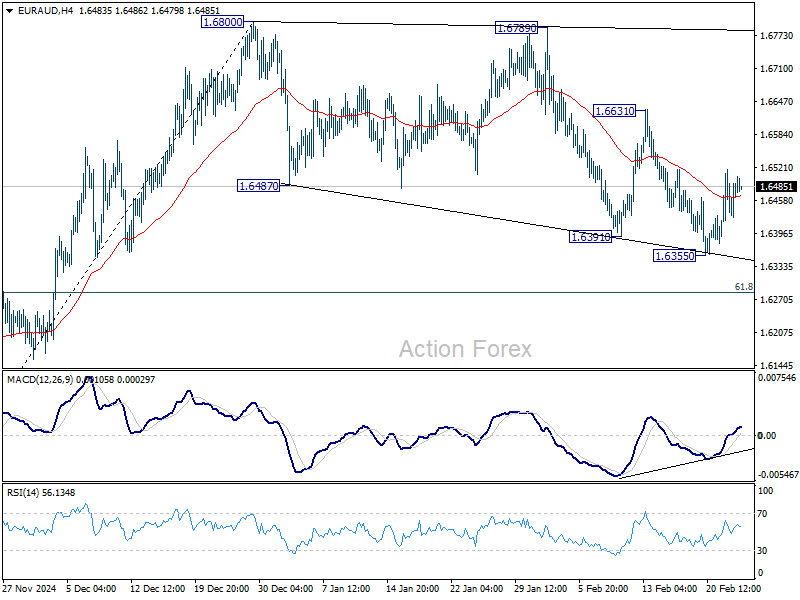

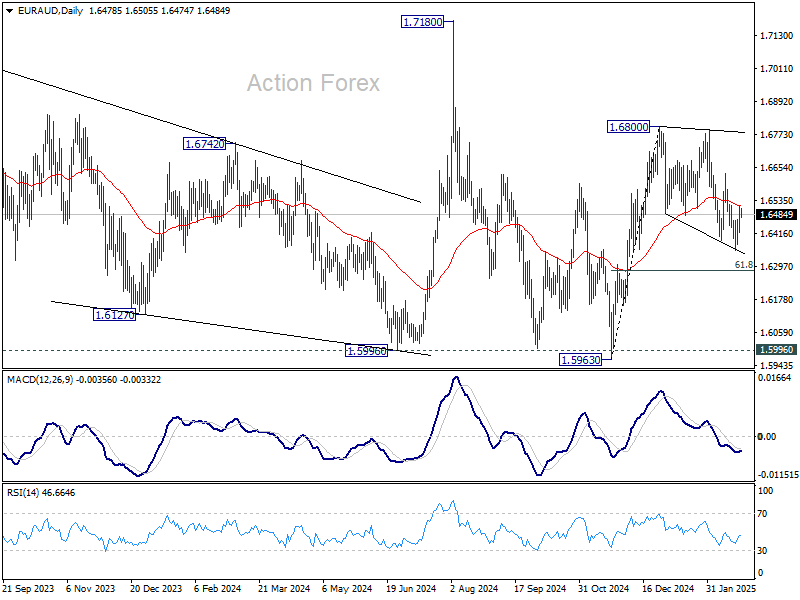

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6437; (P) 1.6479; (R1) 1.6528; More...

Intraday bias in EUR/AUD remains neutral at this point. Below 1.6355 will extend the corrective pattern from 1.6800 to 61.8% retracement of 1.5963 to 1.6800 at 1.6283. On the upside, firm break of 1.6631 resistance will suggest that the correction has likely completed, and rise from 1.5963 is finally ready to resume.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

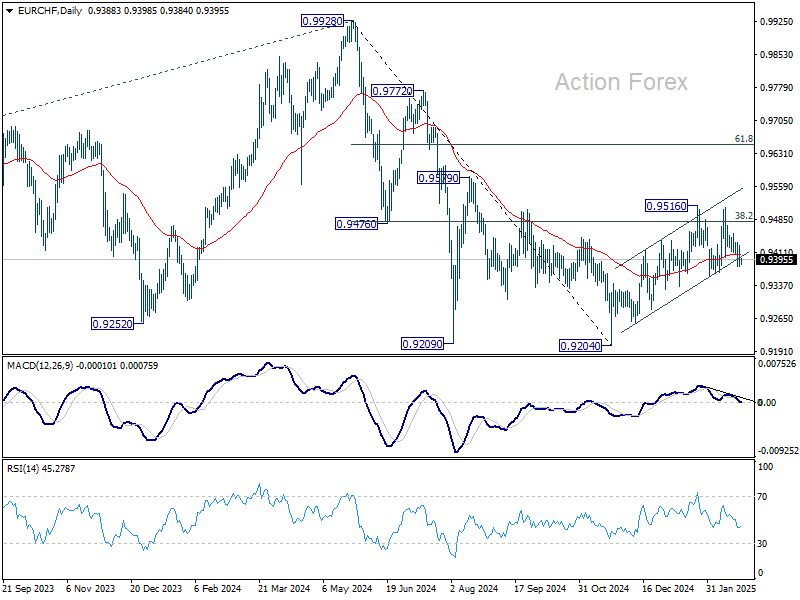

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9372; (P) 0.9400; (R1) 0.9419; More....

EUR/CHF is still bounded in range of 0.9359/9516 and intraday bias remains neutral. On the downside, firm break of 0.9359 will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204 at a later stage.

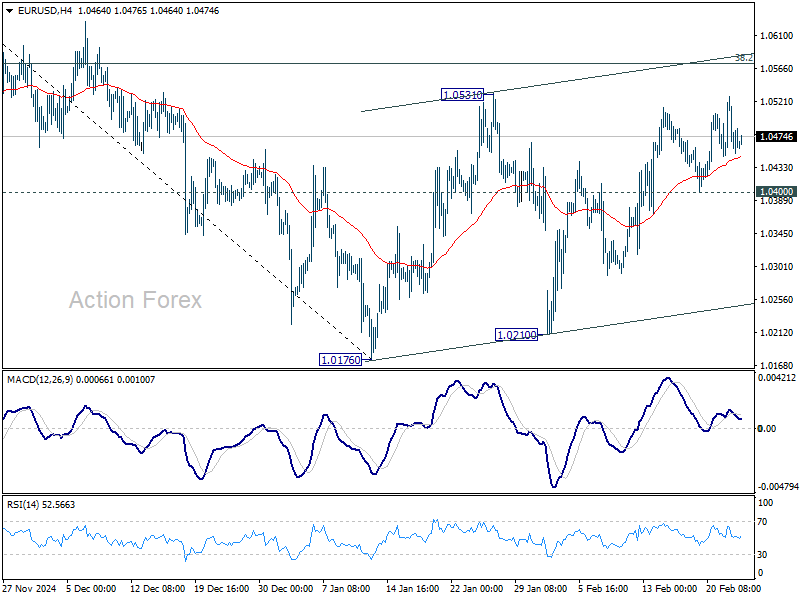

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0438; (P) 1.0483; (R1) 1.0513; More...

Intraday bias in EUR/USD remains neutral. Outlook is unchanged that price actions from 1.0176 are forming a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

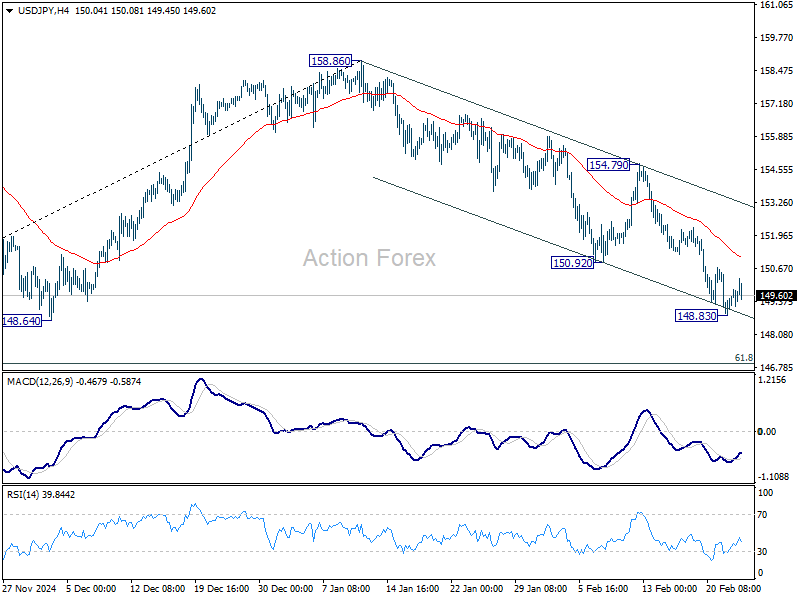

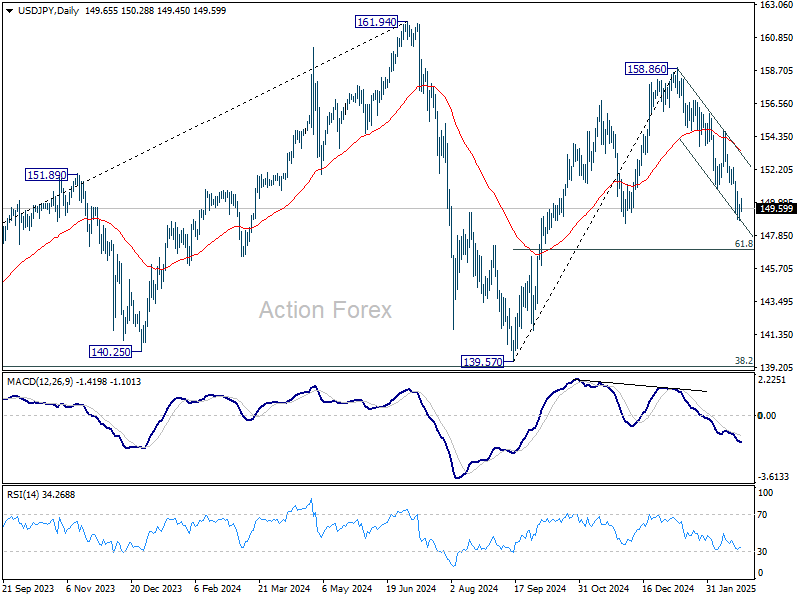

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.09; (P) 149.48; (R1) 150.12; More...

A temporary low is formed at 148.83 with current recovery and intraday bias in USD/JPY is turned neutral first. Further decline is expected as long as 154.79 resistance holds. Fall from 158.86 is seen as the third leg of the pattern from 161.94 high. Below 148.83 will target 61.8% retracement of 139.57 to 158.86 at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

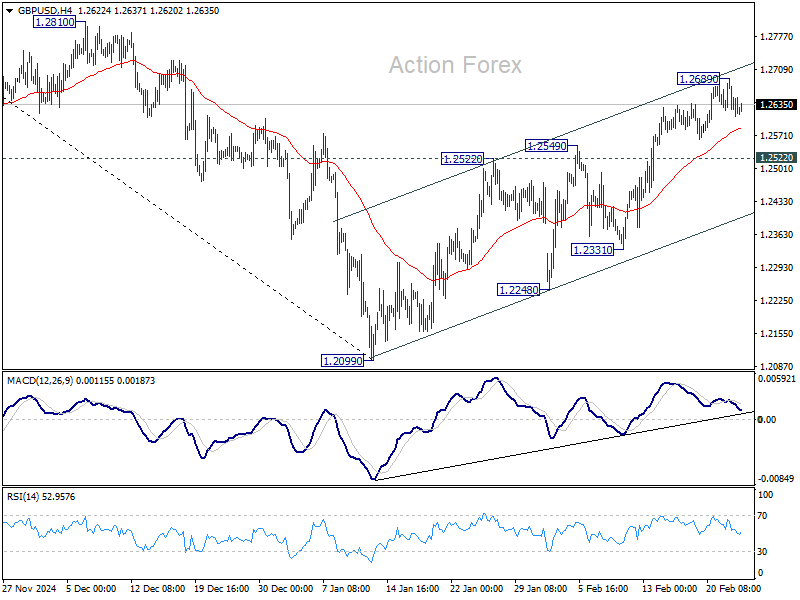

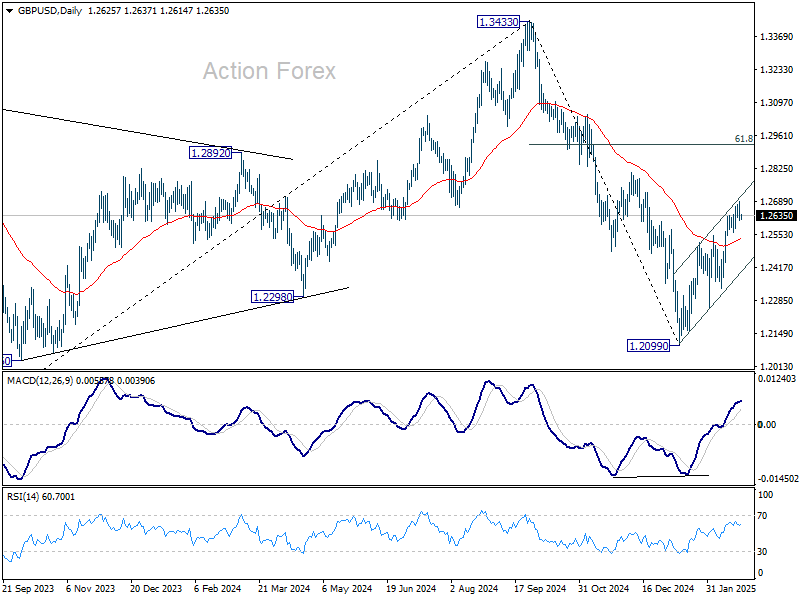

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2594; (P) 1.2643; (R1) 1.2673; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.2689 temporary top. Further rise will remain in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rally from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

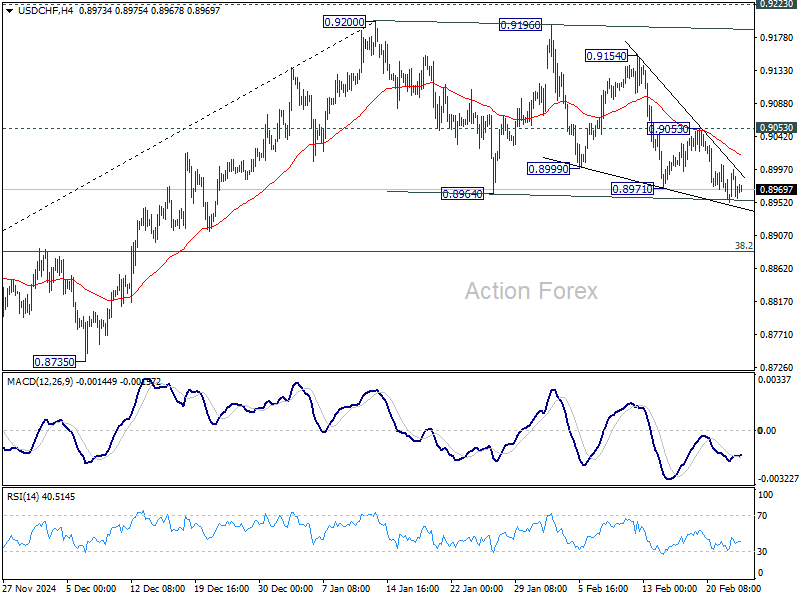

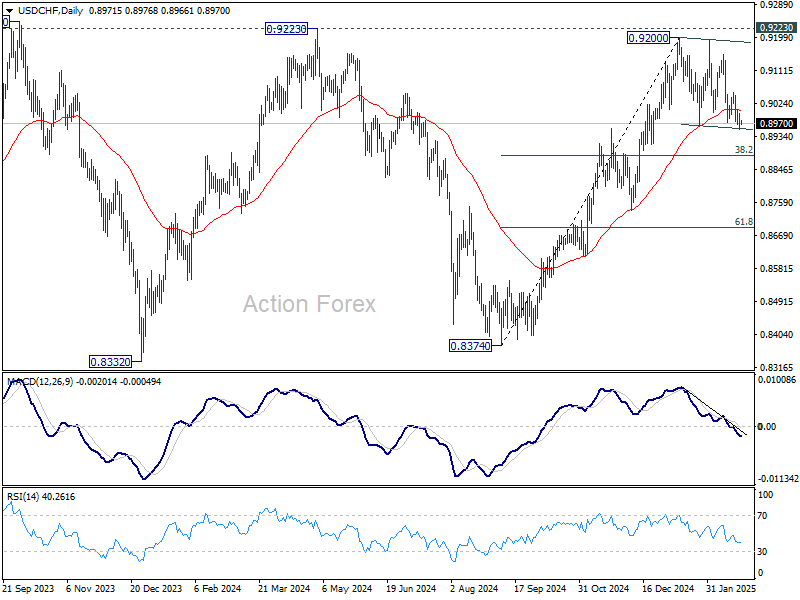

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8951; (P) 0.8974; (R1) 0.8995; More…

No change in USD/CHF's outlook and intraday bias remains neutral at this point. Consolidation pattern from 0.9200 might extend with deeper decline. But larger rally is still expected to continue as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, above 0.9053 will bring retest of 0.9200 resistance. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

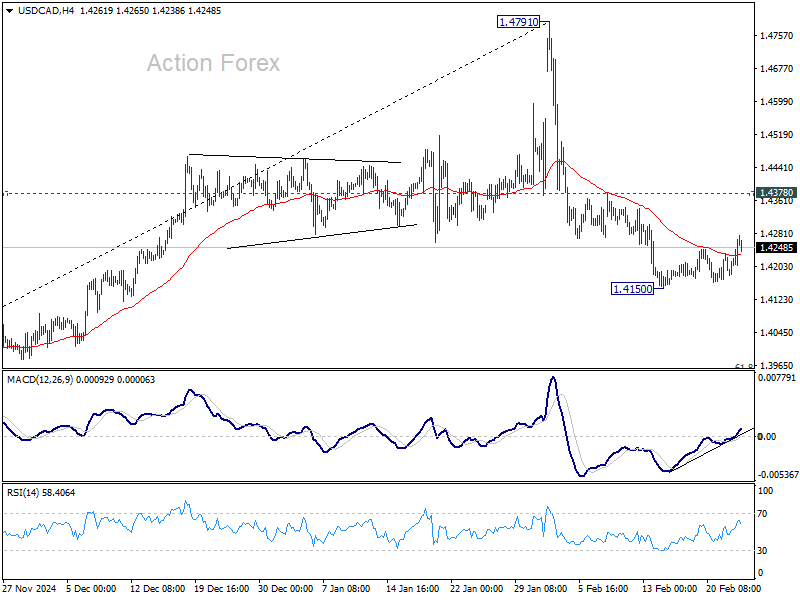

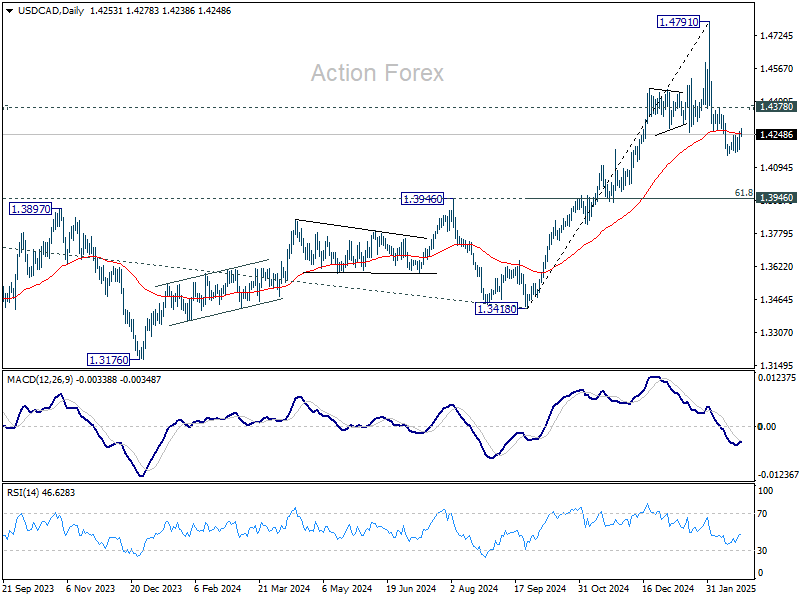

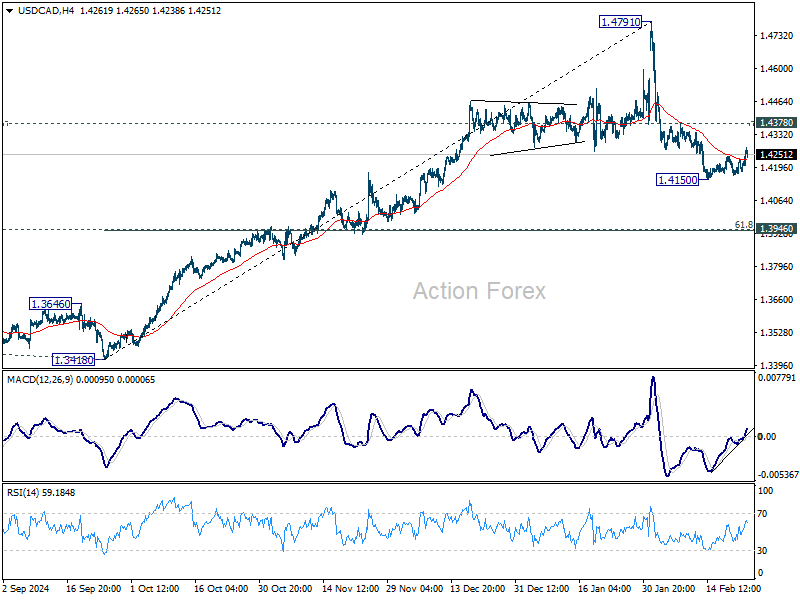

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4205; (P) 1.4236; (R1) 1.4291; More...

Intraday bias in USD/CAD remains neutral the moment. Further decline is expected with 1.4378 resistance intact. Fall from 1.4791 is seen as a correction to rally from 1.3418. Break of 1.4150 will target 1.3946 cluster support (61.8% retracement of 1.3418 to 1.4791 at 1.3942). However, firm break of 1.4378 will suggest that the pull back has completed, and turn bias back to the upside for retesting 1.4791.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

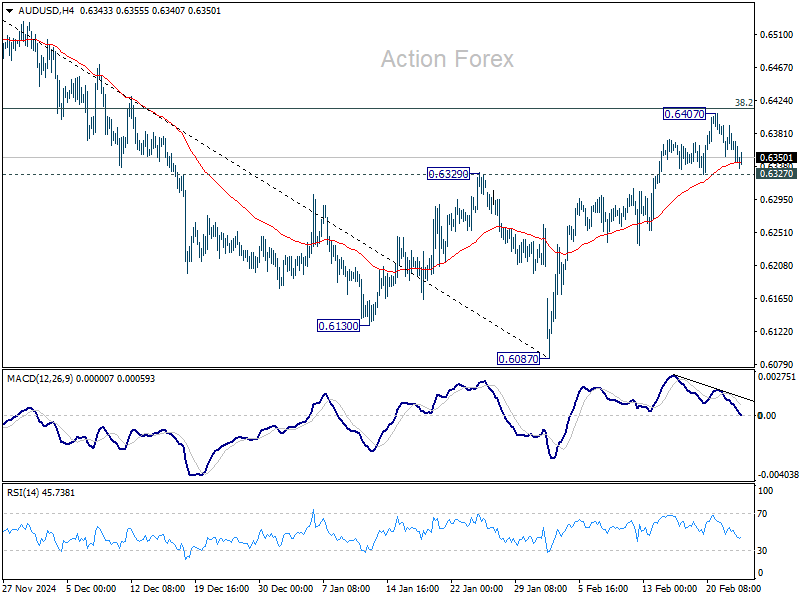

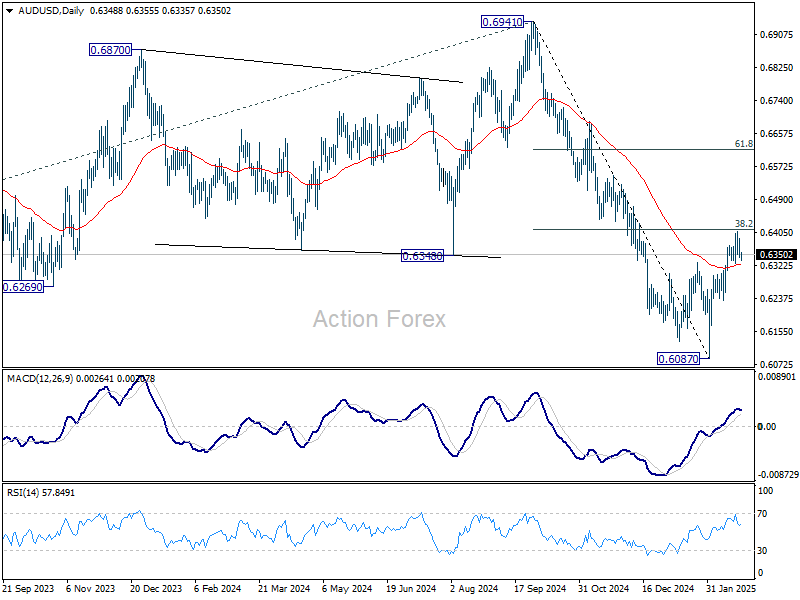

AUD/USD Daily Report

Daily Pivots: (S1) 0.6331; (P) 0.6362; (R1) 0.6379; More...

AUD/USD is staying in tight range above 0.6327 support and intraday bias stays neutral. On the downside, firm break of 0.6327 will suggest that the corrective rebound from 0.6087 has completed ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Intraday bias will be turned back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 0.6413 will pave the way back to 61.8% retracement at 0.6615, even still as a correction.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.

Dollar Rises Slightly After Trump Reaffirms March 4 Tariff Plans for Mexico and Canada

Dollar gained slightly overnight, buoyed by mild risk aversion and ongoing tariff threats from President Donald Trump. However, the lack of follow-through momentum in the greenback suggests traders remain hesitant to commit to large directional bets amid persistent policy uncertainty.

US stock market weakness has been most pronounced in the NASDAQ, which fell by more than -1%. Some of this pullback appears related to profit taking ahead of Nvidia’s quarterly results, due on Wednesday. There are concerned about lower demand for AI technology if China’s low-cost DeepSeek gains traction, posing competition to the industry’s current frontrunners.

Adding to the cautious tone, Trump doubled down on his plan to impose 25% tariffs on Mexico and Canada, stating the levies are “on time, on schedule” for March 4, following a one-month delay. However, markets have been reluctant to react too strongly, given Trump’s history of sudden policy reversals, which adds to the uncertainty surrounding trade relations.

In currency markets, Euro is currently the strongest performer for the week, followed by Swiss Franc and then Dollar. Meanwhile, Loonie is the worst so far, trailed by Yen and Kiwi. Aussie and Sterling are trading in the middle of the pack. Looking ahead, US consumer confidence data could provide the next directional cue for the market.

USD/CAD stands out as a pair to watch, especially under the looming tariff threat. Technically, the fall from 1.4791 (considered a correction to the rally from 1.3418) is in favor to continue as long as 1.4378 resistance holds. Break below 1.4150 would open the way to 1.3946 cluster support ( 61.8% retracement of 1.3418 to 1.4791 at 1.3942).

However, firm break above 1.4378 would suggest the pullback has ended, paving the way for a stronger rebound to retest 1.4791 high.

In Asia, at the time of writing, Nikkei is down -1.34%. Hong Kong HSI is down -0.62%. China Shanghai SSE is down -0.14%. Singapore Strait Times is down -0.11%. Overnight, DOW rose 0.08%. S&P 500 fell -0.50%. NASDAQ fell -1.21%. 10-year yield fell -0.027 to 4.393.

Fed’s Goolsbee: Rate cuts on hold until policy uncertainty clears

Chicago Fed President Austan Goolsbee emphasized the need for caution before resuming rate cuts, citing uncertainty over the economic impact of the Trump administration’s policies.

Speaking in a TV interview overnight, Goolsbee stated that Fed remains in “wait-and-see” mode as it assesses the effects of new tariffs, immigration policies, tax cuts, government spending reductions, and federal workforce changes.

Goolsbee made it clear that if the administration’s policies push inflation higher, Fed is obligated by law to respond accordingly. However, he stressed that the overall policy package remains unclear, making it difficult for Fed to determine its next steps.

“There’s a lot of uncertainty, a lot of kind of dust in the air, and before the Fed can go back to cutting the rates, I feel and have expressed that we got to get a little dust out of the air,” he said.

BoE’s Dhingra reaffirms dovish stance, signals concern over weak consumption

BoE MPC member Swati Dhingra, one of the most dovish voices on the committee, reinforced her call for faster rate cuts. She argued that policy remains overly restrictive despite ongoing disinflation.

Dhingra, who voted for a 50bps rate cut earlier this month, pushed back against the common interpretation that gradual easing cycle means 25bps cuts per quarter, stating that "that's not actually what the committee has said. That's not my definition, clearly." She emphasized that even under the assumption of quarterly 25bps cuts, monetary policy would still be "in restrictive territory all of this year".

Her primary concern remains the persistent weakness in consumer spending, stating that "consumption remains pretty weak, so we’re not seeing that resurgence of inflationary pressures." She also noted that the slow recovery in demand justifies a more accommodative stance, as "we basically aren’t recovering fully."

Despite concerns about potential inflationary pressures in certain items, Dhingra maintained that the disinflation process remains intact. She believes the key takeaway is that monetary policy is still restrictive, and reducing the level of restraint would not necessarily derail inflation's downward trend.

Her remarks highlight a clear divide within the MPC, where some members advocate patience, while doves like Dhingra and Catherine Mann argue that rate cuts should come sooner and in larger increments.

Looking ahead

Germany GDP final will be released in European session. Later in the day, US consumer confidence will be the main focus, and house price index will be published too.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6331; (P) 0.6362; (R1) 0.6379; More...

AUD/USD is staying in tight range above 0.6327 support and intraday bias stays neutral. On the downside, firm break of 0.6327 will suggest that the corrective rebound from 0.6087 has completed ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Intraday bias will be turned back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 0.6413 will pave the way back to 61.8% retracement at 0.6615, even still as a correction.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.

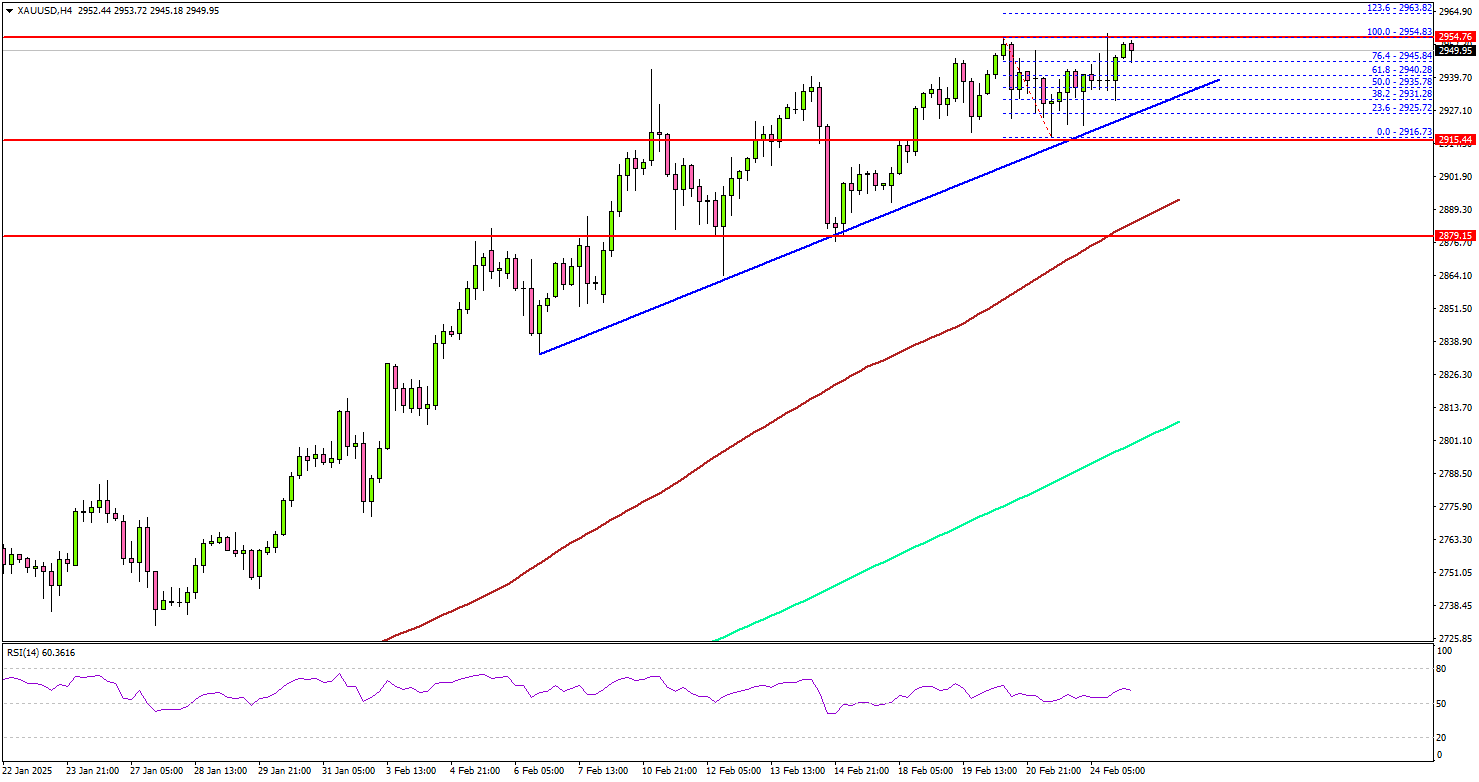

Gold Strengthens—Is a $3K Breakout Imminent?

Key Highlights

- Gold started a fresh surge above the $2,950 resistance and traded to a new record high.

- A key bullish trend line is forming with support at $2,930 on the 4-hour chart.

- Bitcoin is still struggling to clear the $100,000 resistance zone.

- EUR/USD failed to settle above the 1.0535 resistance zone.

Gold Price Technical Analysis

Gold prices started a fresh rally above the $2,900 resistance. The bulls pumped the price above the $2,950 level and the price traded to a new record high.

The 4-hour chart of XAU/USD indicates that the price remained in a positive zone above the $2,920, the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

The current price action suggests a high chance of more gains above the $2,965 level. On the upside, immediate resistance is near the $2,972 level. The next major resistance sits near the $2,985 level.

A clear move above the $2,985 resistance could open the doors for more upsides. The next major resistance could be $3,000, above which the price could rally toward the milestone level at $3,050.

On the downside, initial support is near the $2,930 level. There is also a key bullish trend line forming with support at $2,930 on the same chart. The first key support is near $2,920. The next major support is near the $2,915 level.

The main support is now $2,885. A downside break below the $2,885 support might call for more downsides. The next major support is near the $2,840 level.

Looking at Bitcoin, the price attempted a recovery wave but the bears are still active below the $100,000 level.

Economic Releases to Watch Today

- S&P/Case-Shiller Home Price Indices for Dec 2024 (YoY) - Forecast +4.5%, versus +4.3% previous.

- US Housing Price Index for Dec 2024 (MoM) - Forecast +0.2%, versus +0.3% previous.