Sample Category Title

Fed’s Barkin: Staying modestly restrictive until inflation risks clear

Richmond Fed President Tom Barkin highlighted the need for a “modestly restrictive” monetary policy stance until there is greater confidence that inflation is firmly returning to the 2% target.

Speaking in a speech overnight, Barkin emphasized the importance of remaining “steadfast” in tackling inflation, warning that history has shown the risks of easing policy too soon.

“We learned in the '70s that if you back off inflation too soon, you can allow it to reemerge. No one wants to pay that price,” he cautioned.

Barkin acknowledged the high level of uncertainty surrounding economic policy changes, geopolitical tensions, and natural disasters, all of which could influence inflation dynamics.

He noted that tariffs imposed during Donald Trump's first administration in 2018 added about 30 basis points to inflation. However, he cautioned that the effect of the latest round of trade policies is harder to predict, as firms may either pass costs onto consumers or absorb them.

Beyond trade policies, Barkin also flagged uncertainties around deregulation, tax policies, government spending, and immigration reforms, all of which could shape labor market dynamics and broader economic conditions.

Given these unknowns, he prefers to “wait and see how this uncertainty plays out” before advocating any adjustments to monetary policy.

Bitcoin Loses Ground—Falling Below $90K Sparks Panic

Key Highlights

- Bitcoin price declined heavily and even traded below the $90,000 support.

- BTC is now following a connecting bearish trend line with resistance at $91,600 on the 4-hour chart.

- Ethereum price also declined and traded below the $2,500 support.

- XRP dipped toward $2.00 before the bulls appeared.

Bitcoin Price Technical Analysis

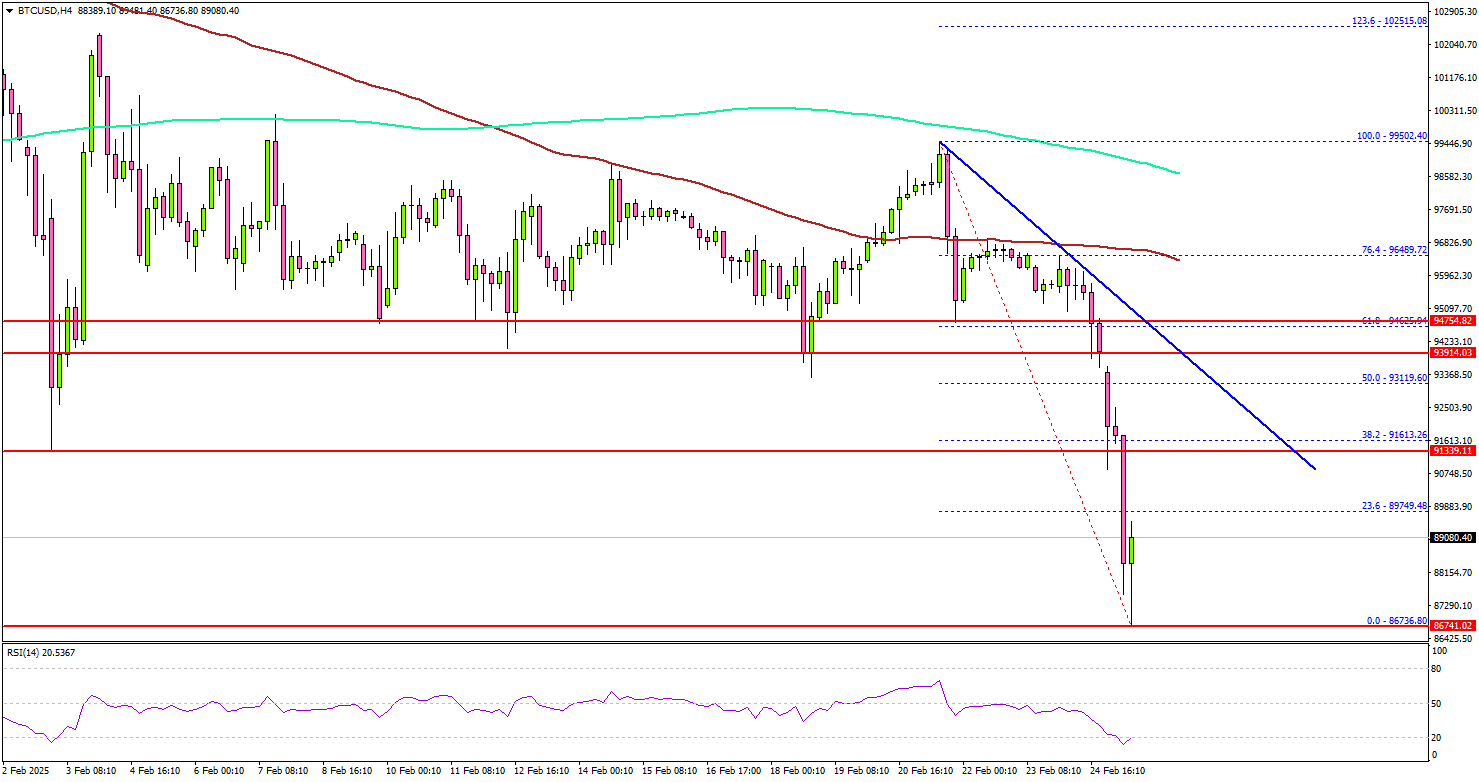

Bitcoin price made a couple of attempts to settle above $100,000 against the US Dollar. However, BTC failed and started a fresh decline.

Looking at the 4-hour chart, the price gained bearish momentum after it broke the $95,000 support zone. There was a close below the $92,000 level, the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

The bears even pushed the price below the $90,000 mark. A low was formed at $86,736 and the price is now consolidating losses. On the upside, the price could face resistance near the $90,000 level.

The next key resistance is $91,500. There is also a connecting bearish trend line forming with resistance at $91,600 on the same chart. It is close to the 38.2% Fib retracement level of the downward move from the $99,502 swing high to the $86,736 low.

A successful close above $91,600 might start another steady increase. In the stated case, the price may perhaps rise toward the $93,000 level. Any more gains might call for a test of $95,000.

Immediate support is near the $87,200 level. The next key support sits at $86,650. A downside break below $86,650 might send Bitcoin toward the $85,000 support. Any more losses might send the price toward the $83,200 support zone.

Looking at Ethereum, there was a fresh bearish reaction and the bears pushed the price below the $2,500 support zone.

Today’s Economic Releases

- US New Home Sales for Jan 2025 (MoM) – Forecast +0.2% versus +3.6% previous.

NASDAQ Elliott Wave Forecast – Identifying The Next Buying Opportunity

The NASDAQ (NQ_F) remains bullish from the all-time low despite the pullback from December 2024. The pullback could present a perfect opportunity for buyers in the coming days. This blog post will address key price areas for the buyers to anticipate the next opportunity.

NASDAQ (NQ) is in an all-time bullish trend. Within this all-time bullish cycle, the index started the current bullish cycle from the low of October 2022 where it completed wave (II) and began wave (III). We reckon, as the chart below shows, that the peak of December 2024 marked the end of wave III of (III). Thus, the pullback from that high should be wave IV of (III).

Wave IV started from the peak of December 2024. In an ideal market condition, buyers anticipate going long from the extreme of pullbacks within an established bullish sequence. On the other hand, traders tend to sell at the extreme of corrective bounces within a bearish sequence. Thus, the corrective pullback from December could be another ideal setup for buyers. One of the easiest and most profitable structures to trade in this regard is the Zigzag or Double Zigzag corrective sequences.

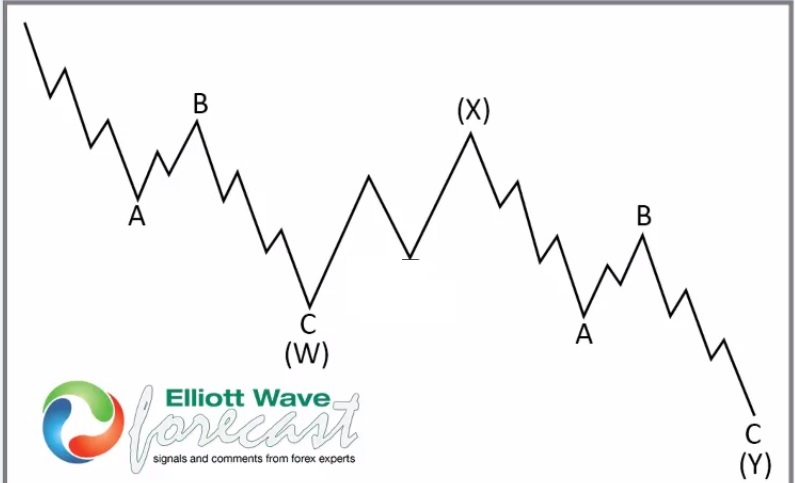

Double Zigzag Structure in Elliott Wave Theory

In Elliott Wave Theory, a double zigzag is a complex corrective pattern that consists of two zigzags (labeled W and Y) connected by an intervening corrective wave (labeled X). It is denoted as W-X-Y and serves to extend the duration and depth of a correction beyond a single zigzag.

Structure of a Double Zigzag (W-X-Y):

- Wave W – The first zigzag (A-B-C).

- Wave X – A corrective wave that connects W and Y. It can take various forms (flat, triangle, or another zigzag).

- Wave Y – The second zigzag (A-B-C), which typically follows the same direction as wave W.

Rules & Guidelines:

- Both W and Y are zigzags (A-B-C structures), meaning wave A is impulsive or leading diagonal, wave B is corrective, and wave C is impulsive or ending diagonal.

- Wave X is typically smaller than W and Y but can sometimes be complex.

- A double zigzag extends the correction compared to a single zigzag, often forming a deeper retracement.

- It usually appears in corrective waves (wave 2, wave 4, or within a larger complex correction).

NASDAQ Elliott Wave Analysis: Double Zigzag Pullback for Wave IV?

The wave IV pullback from December is close to finishing a W-X-Y double zigzag structure. Wave ((W)) and ((X)) of IV finished on 13th January 2025 and 18th February 2025. The fast decline that follows is identified as wave (A) of ((Y)). The price might correct the decline from the February high in wave (B) of ((Y)) before dropping again in wave (C) of ((Y)) and finishing the structure.

In Fibonacci ratios, wave Y often ends within 100%-123.6% of wave W but sometimes reaches close to 161.8%. 161.8% extension within a double zigzag is very rare and in most cases will be considered an impulse or triple zigzag instead. Thus, at the blue box (20571.75-19490.64), we will expect wave (V) to begin or at least a 3-swing bounce to a risk-free area. The blue box prices should be watched. It could attract fresh bids if the price gets there.

GBPCHF Technical Analysis

The Pound Sterling (GBP) rose 0.37% to 1.2669 after rebounding from a two-day low of 1.2605, as the US Dollar weakened due to falling US Treasury yields. Market sentiment turned negative following US President Trump's renewed tariff threats on Canadian and Mexican goods. Weak US economic data also weighed on the Dollar, with the 10-year Treasury yield dropping 10 basis points to 4.30%. US home prices rose 4.5% year-over-year in December, slightly higher than November's 4.3%. The Confederation of British Industry in the UK reported that retailers plan to cut investments due to weak spending and high prices. A Reuters poll suggests the Bank of England (BoE) will likely keep rates steady at 4.50% in March, possibly cutting to 4.25% in Q2. Traders now await comments from BoE's chief economist, Huw Pill.

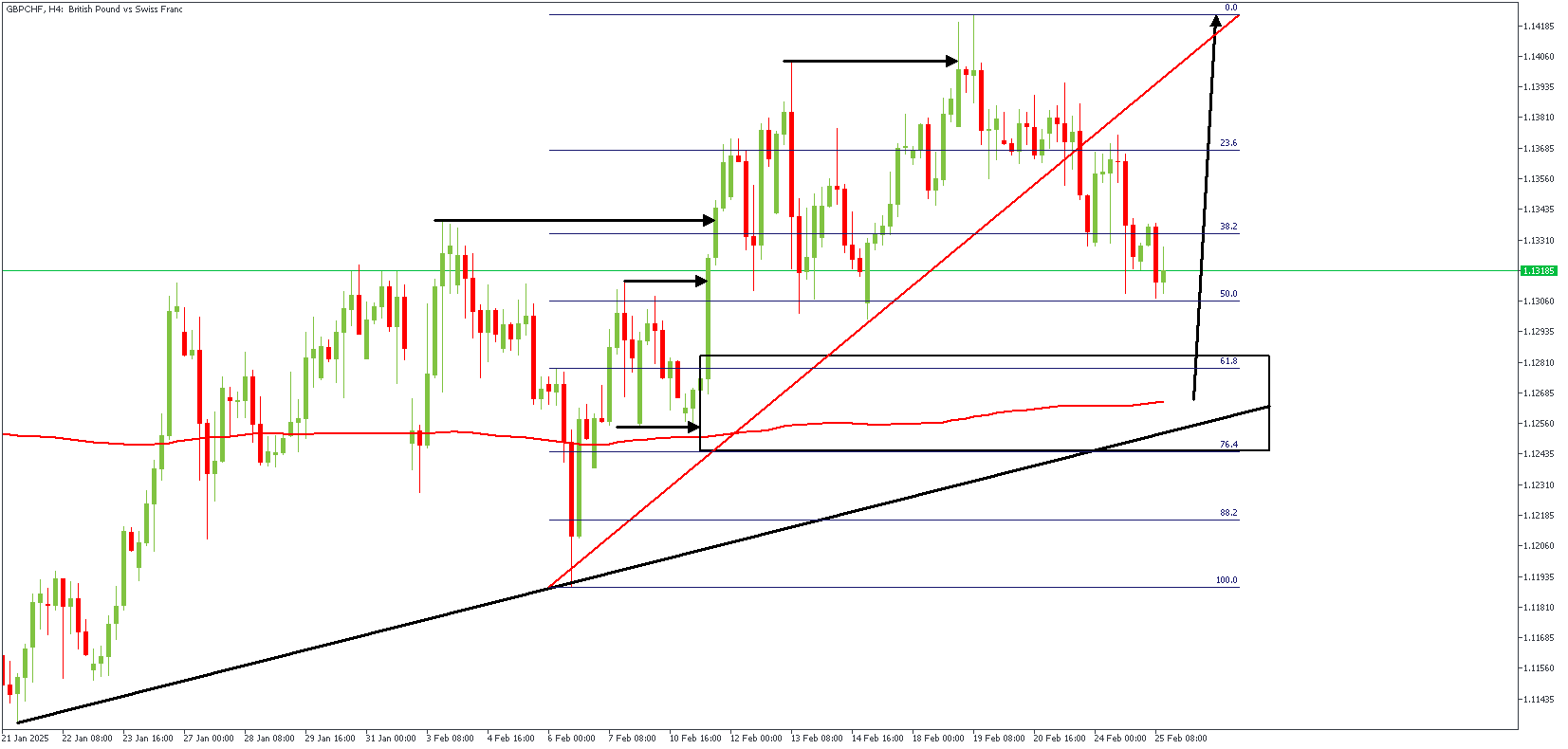

GBPCHF – H4 Timeframe

The highlighted demand zone on GBPCHF's 4-hour timeframe chart is the result of a bullish SBR pattern, with confluences from the 61% Fibonacci retracement level, 200-period moving average support, and trendline support. An FVG near the demand area lends further credence to the bullish sentiment.

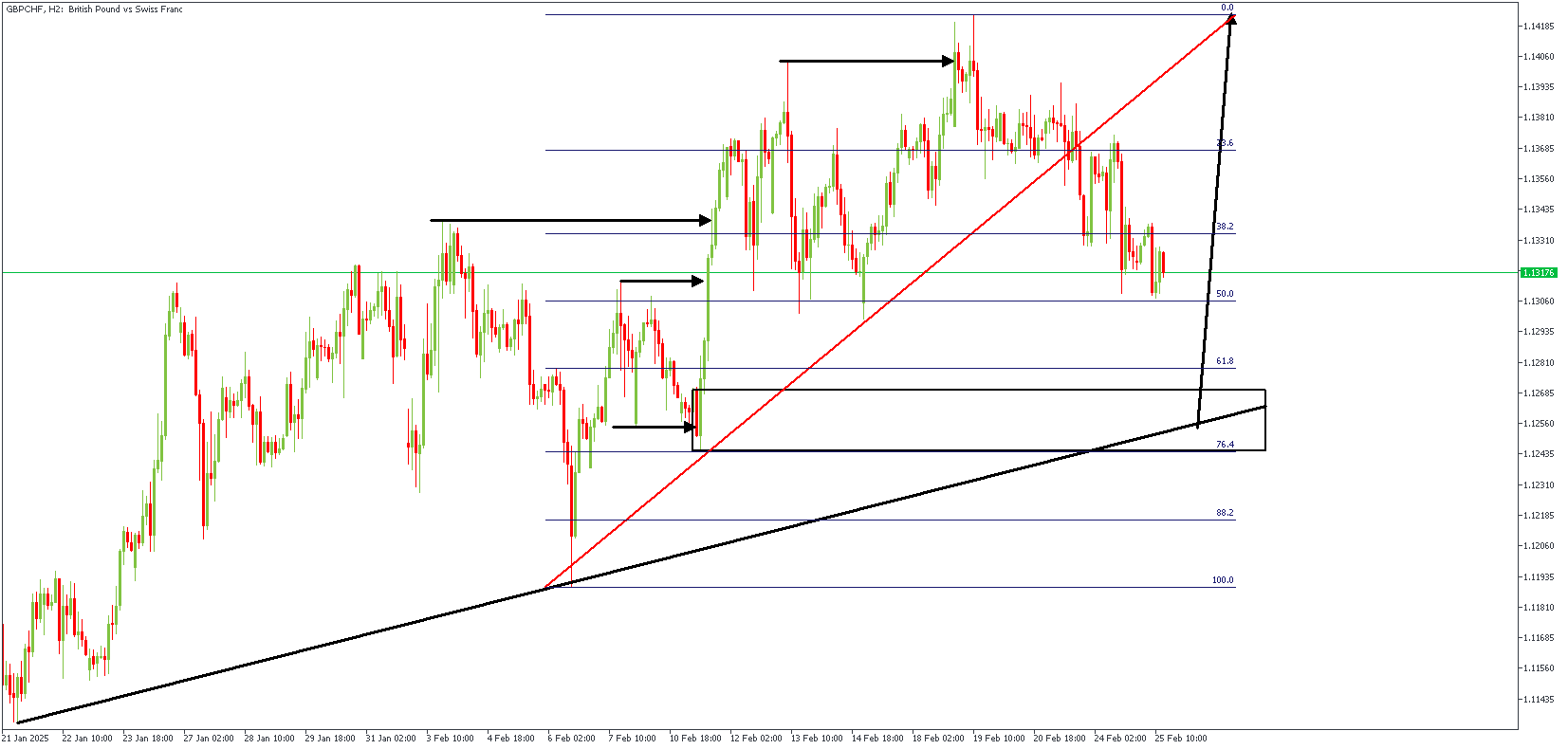

GBPCHF – H3 Timeframe

The 3-hour timeframe chart of GBPCHF shows the SBR pattern in more detail, with the induced low visibly retracing before filling up the FVG area. The reaction from the confluence of the demand zone, the trendline support, and the 61% Fibonacci retracement level is expected to push prices to create a new higher high.

Analyst's Expectations:

- Direction: Bullish

- Target- 1.14218

- Invalidation- 1.12162

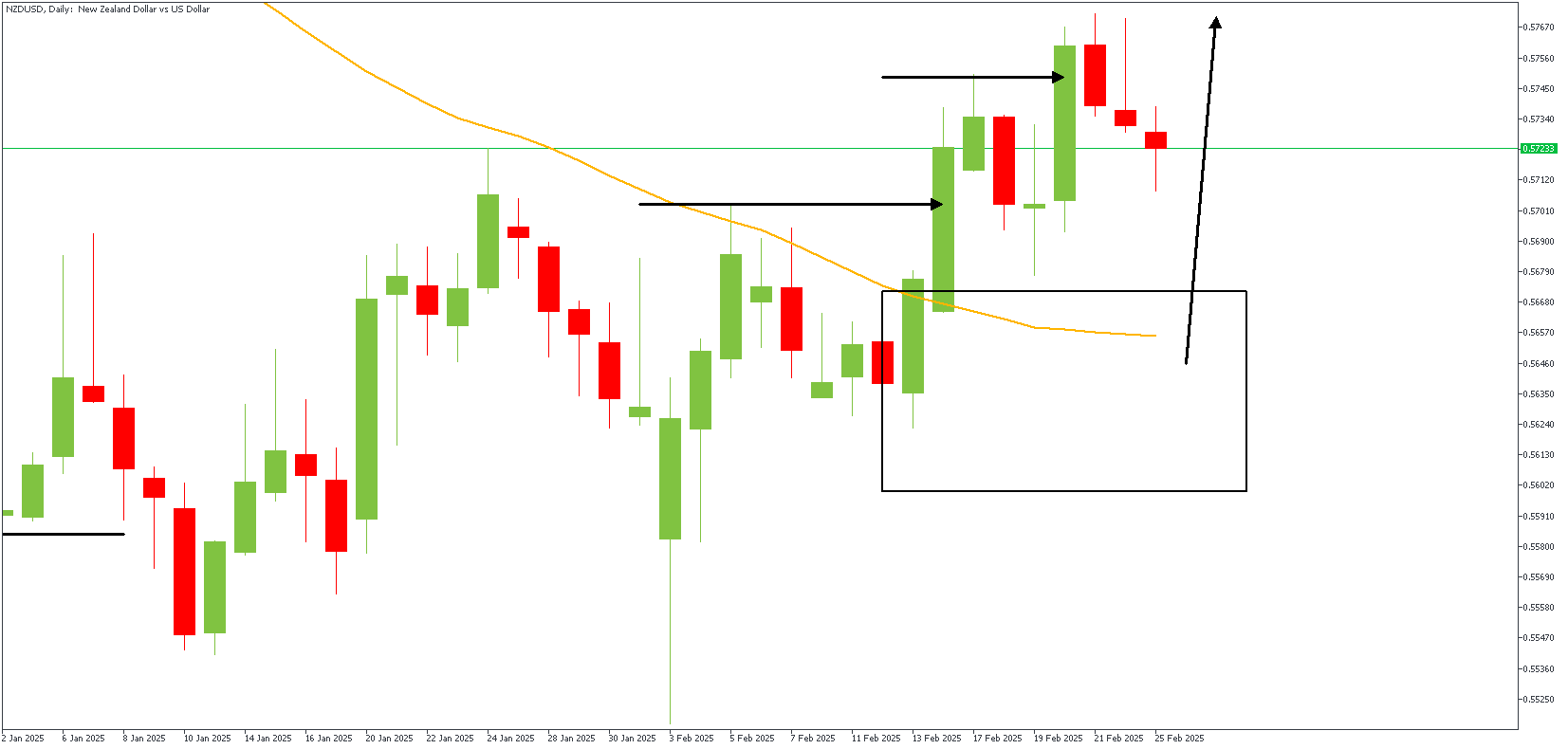

NZDUSD Technical Analysis

The New Zealand Dollar (NZD) is facing slight downward pressure against the US Dollar (USD) and could dip further, though it's unlikely to fall clearly below 0.5715. If it does break that support, reaching 0.5790 is doubtful. In the short term, analysts expected the NZD to move between 0.5735 and 0.5770, which it did—hitting both levels before closing at 0.5733, down 0.17%. The downward momentum has slightly increased, suggesting the NZD might edge lower today. However, any drop is expected to stay above 0.5715. This mild pressure will likely hold if the NZD remains below 0.5760, with minor resistance at 0.5745.

NZDUSD – D1 Timeframe

After breaking above the 50-day moving average, the price action on the daily timeframe chart of NZDUSD proceeded to overshoot the previous high, creating a new higher high in the process. The momentum from the breakout has waned, giving rise to the ongoing retracement move. The expectation is that the confluence region of the drop-base-rally demand zone and the 50-day moving average would provide adequate support for a bullish continuation.

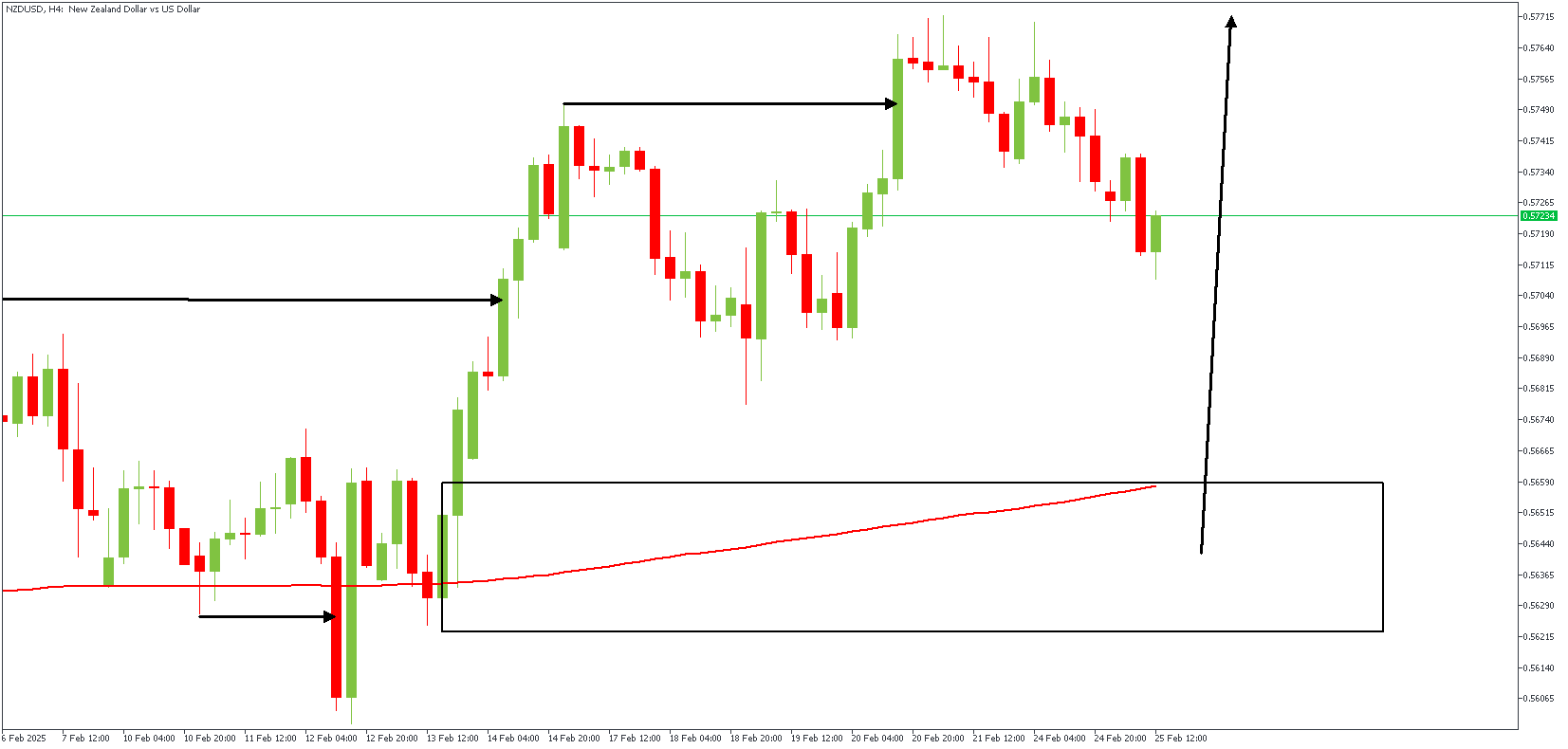

NZDUSD – H4 Timeframe

The 4-hour timeframe chart of NZDUSD shows that the daily timeframe demand zone doubles as the trough of a bullish SBR pattern, with the presence of an FVG, 100-period moving average support, 76% Fibonacci retracement level support, and liquidity at the previously induced low. The expected outcome in this scenario is bullish, with an initial target at the BSL (Buy-Side Liquidity) at the recent high.

Analyst's Expectations:

- Direction: Bullish

- Target- 0.57713

- Invalidation- 0.56004

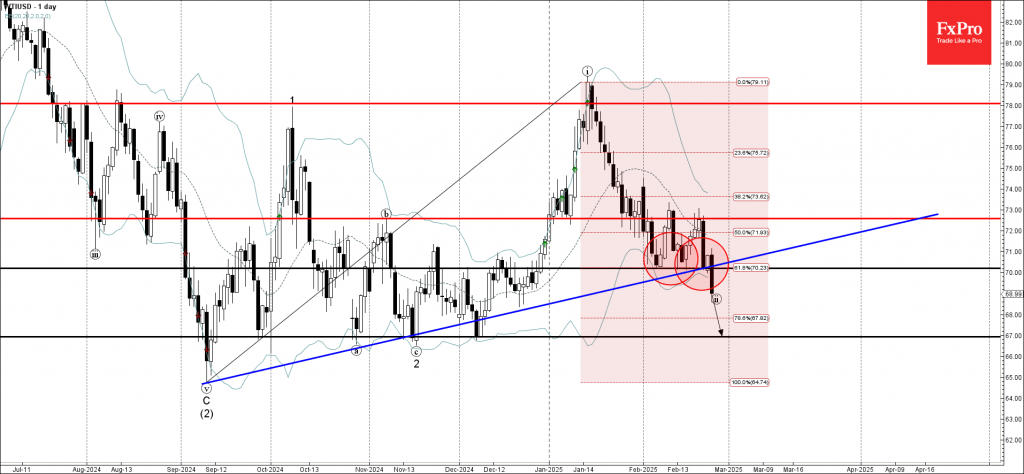

WTI Crude Oil Wave Analysis

- WTI crude oil broke support zone

- Likely to fall to support level 67.00

WTI crude oil recently broke the support zone between the round support level 70.00 (which reversed the price multiple times from the start of February), the support trendline from September and the 61.8% Fibonacci correction of the upward impulse from September.

The breakout of this support zone accelerated the active short-term correction ii of the intermediate upward impulse sequence (3) from September.

WTI crude oil can be expected to fall further to the next support level 67.00 (former monthly low from December).

WTI Oil Falls Below $70 per Barrel as Tariff Concerns Further Sour Sentiment

WTI oil price fell below psychological $70 support on Tuesday and hit the lowest levels in two months.

Oil was down nearly 3% on renewed fears about the global economy and lower demand after the latest economic data showed that German economy contracted for the second straight quarter and US consumer confidence declined at the fastest pace since mid-2021.

Strong concerns among investors were also fueled by US tariffs on imports, as President Trump signaled that initially delayed tariffs on imports from Canada and Mexico, will be implemented according to the schedule – at the beginning of next month.

Tariffs on China’s goods imports further contribute to negative outlook, as this would directly fuel inflation, while consequences of trade war would be significant.

Negative fundamentals continue to sour the sentiment and raise pressure on oil prices.

Sustained break below $70/$69.90 supports (psychological / Fibo 76.4% of $66.98/$79.35 rally) to further firm bearish stance and risk dip towards weekly base at $67.00/66.30 zone (Oct/Dec 2024).

Broken $70 zone reverted to solid resistance which should ideally cap.

Res: 69.79; 70.00; 70.83; 71.44

Sup: 68.44; 67.70; 66.98; 66.54

Aussie Awaiting Inflation Data

The Australian dollar is steady after two straight losing trading days. In the North American session, AUD/USD is trading at 0.6343, down 0.09% on the day.

Australia’s CPI expected to tick higher

Australia releases the consumer price index for January on Wednesday. Inflation has been moving higher, as CPI accelerated in December to 2.5% y/y, up from 2.3% and its highest level since August. The market estimate for January stands at 2.6%.

Inflation remains within the Reserve Bank of Australia’s target band of 2%-3% but the central bank remains concerned about upside risks to inflation. The RBA finally lowered rates last week after maintaining rates for over a year and joined most of the major central banks which are in the midst of an easing cycle. The RBA delivered a “hawkish cut” as the central bank stated it “remains cautious” on the possibility of further cuts and the markets aren’t expecting a rate cut before May.

The latest headache for RBA policymakers is the Trump administration which has hit China with tariffs and threatened to apply tariffs to other trading partners. This could lead to another trade war with China which would likely raise inflation and hurt China’s economy. China is Australia’s largest trading partner and a slowdown in China would hurt Australia’s key export sector.

The US releases the Conference Board consumer confidence index later today. The market estimate stands at 102.5 for January, down from 104.1 in December. The US consumer is spending, as retail sales for December rose 0.4% m/m and 5.5% annualized from November. The labor market is strong, wages are outpacing inflation and the economy is humming. This rosy picture means that the Federal Reserve isn’t under pressure to lower rates and the markets aren’t expecting another rate cut before June.

AUD/USD Technical

- AUD/USD tested support at 0.6331 earlier. Below, there is support at 0.6314

- 0.6362 and 0.6379 are the next resistance lines

Sunset Market Commentary

Markets

US bond yields slid further in moves that greatly outpace those in Germany. Declines vary between -5.7 and 7.5 bps with some minor outperformance by the belly of the curve. Rates showed signs of fatigue by mid-February. At that time markets were priced for growth perfection with elevated inflation embraced as the necessary byproduct. Such a stretch was only tenable in case of near-perfect data. Enter Friday’s US PMIs. Inflation fears swapped for a growth scare and pushes the US 2-yr yield towards first support at 4.06-4.09% - the 38.2% retracement on the Sep-Jan rally and lower bound of the sideways trading range in place since November last year. The 10-yr tenor moves to new YtD lows at 4.31% today and breaks below the 38.2% retracement (4.34%) of that same Sep-Jan rally in the process. Moves in Germany are limited to 2 bps. The front end of the curve is more or less locked in to the downside with the bar to add to the current amount of expected ECB easing getting higher by the day. ECB’s Nagel, Kazaks and Schnabel all showcased that by calling either for caution when cutting rates further or saying that rates below neutral are not a discussion for now. Today’s euro area negotiated wage index underscored their view. Wage growth slowed from Q3’s record 5.4% in Q3 but the pace remains at a high 4.1%. The ECB’s own tracker a few weeks ago suggested wages would continue to grow fast at least through the first half of this year. Longer-term yields are better protected now Europe’s largest economy, Germany, is on the verge of loosening the fiscal reins, in first instance to increase its military capacity but later perhaps to jumpstart broader business and consumption. Bloomberg reported that the upcoming chancellor Merz of the winning CDU/CSU party is in talks with the SPD to change the constitution to create a special €200bn fund. The aim is to do so ahead of the new legislature (March 24) in which the far right and left have blocking minorities. The SPD indicated they are open to do so as well as to adjust the debt brake that’s limiting the amount of annual borrowing to just 0.35% of GDP. Sticking to the subject, UK PM Starmer today outlined plans to increase defense spending from 2.3% to 3% of GDP over the next decade. He added that it would be funded through spending cuts rather than higher taxes or borrowing. In a first step he wants to raise it to 2.5% by 2027, from 2.3% currently. This amounts to around £5bn. UK yields (-6 bps)are caught in the broader downtrend though. Currency markets are relatively calm. The dollar trades with a slight negative bias. EUR/USD rises to 1.05, the trade-weighted DXY returned to the recent lows around the 38.2% support of the Sep-Jan move higher at 106.35.

News & Views

UK retail sales volumes in February declined (Y/Y) for the fifth consecutive month according to the Confederation of British Industry’s (CBI) quarterly distributive trades survey. The weighted balance printed at -23. Retailers even expect sales to fall at a somewhat faster pace in March. ‘Retailers remain downbeat about their future business situation, and this sentiment was reflected in their expectations to cut back on headcount and capital expenditure going forward. In particular, investment intentions worsened to the greatest extent since May 2019.’, CBI said. Sales for the time of year are judged to be “poor” and firms expect their business to deteriorate over the coming quarter (-19) too. Retailers especially expect to reduce investment in the next 12 months. Headcount in retail declined at a moderate pace and is anticipated to fall at a broadly similar rate in March. CBI blames persistently weak demand and the impact of the Autumn budget to have dampened sentiment and urges the government to take measures.

Brazilian consumer prices in Brazil accelerated sharply from 0.11% M/M and 4.50% Y/Y in January to 1.23% M/M and 4.96% Y/Y in February, the highest level since October 2023. The M/M rise was the highest since April 2022 and even the fastest pace for the month February since 2016. According to IBGE statistical agency, the jump in inflation was mainly due to housing related costs and education. While at elevated levels, the market consensus still expected an even slightly faster rise (5%+ Y/Y). The central bank targets inflation at 3.0% with a deviation of +/- 1.5ppt. The Banco do Brazil resumed its tightening cycle in September of last year and in January for the second consecutive meeting raised its policy rate by 100 bps to 13.25%. The slightly softer than expected February reading won’t change the banks intention the raise the policy rate again by 100 bps at the March meeting as its seeks to reign in an de-anchoring of inflation expectations. The real trades marginally softer against the dollar today (USD/BRL 5.784).