Sample Category Title

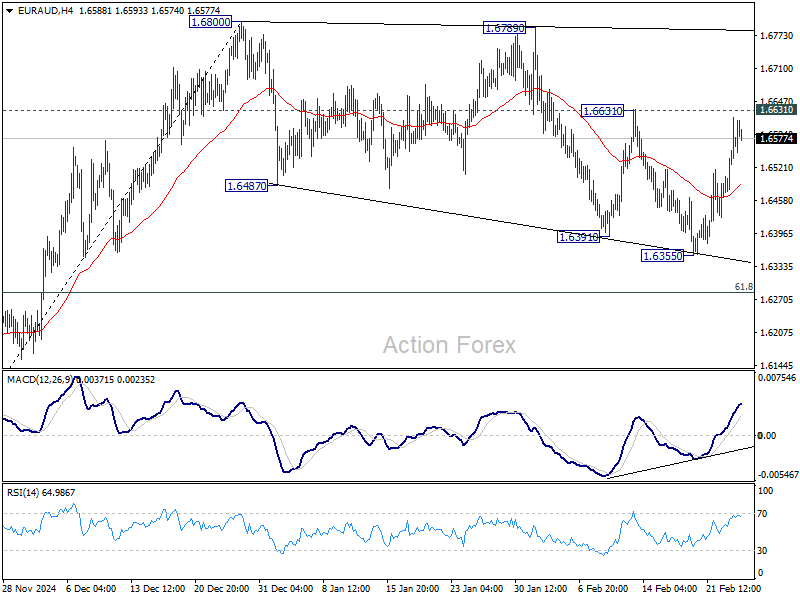

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6494; (P) 1.6557; (R1) 1.6638; More...

Immediate focus is now on 1.6331 resistance as EUR/AUD's rebound from 1.6355 extends. Break there would suggest that corrective pattern from 1.6800 has already completed, and turn bias to the upside for retesting this high. Firm break there will resume the rally from 1.5963. In case of another fall, strong support should be seen at 61.8% retracement of 1.5963 to 1.6800 at 1.6283 to contain downside.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

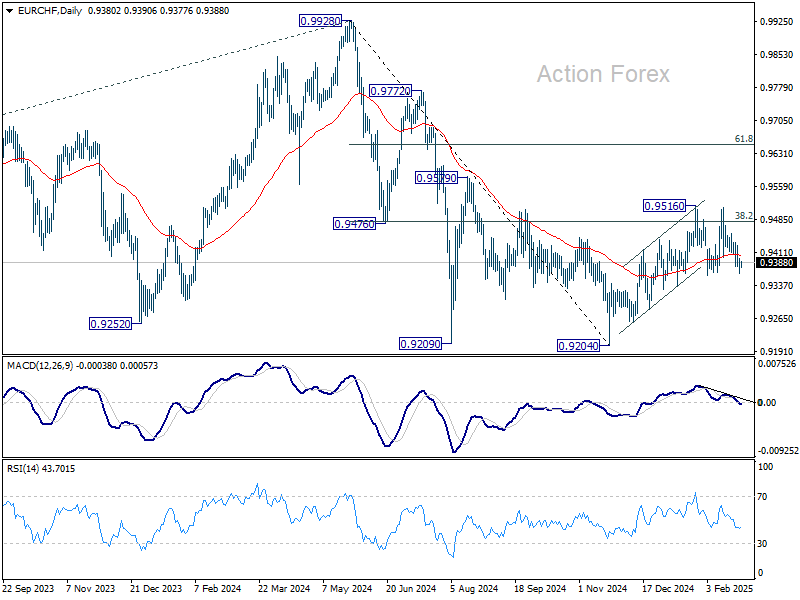

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9370; (P) 0.9385; (R1) 0.9404; More....

Intraday bias in EUR/CHF stays neutral as range trading continues inside 0.9359/9516. On the downside, firm break of 0.9359 will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204 at a later stage.

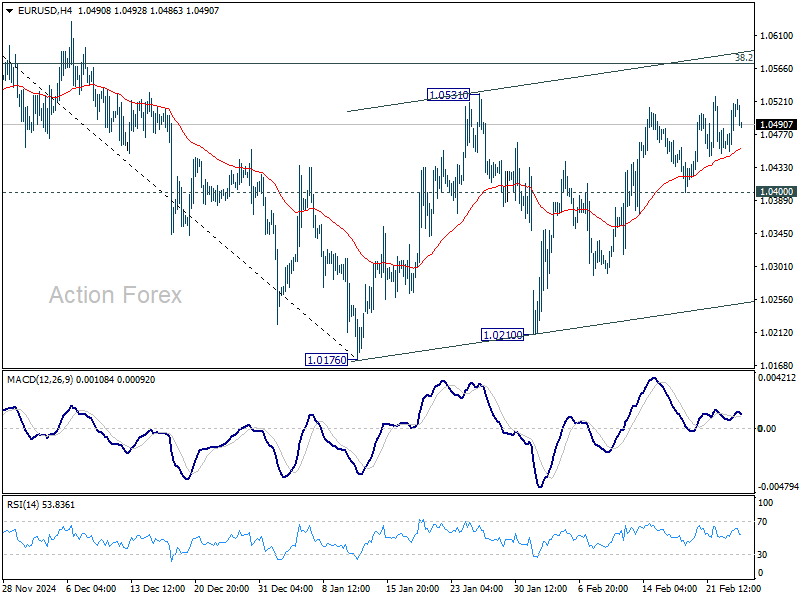

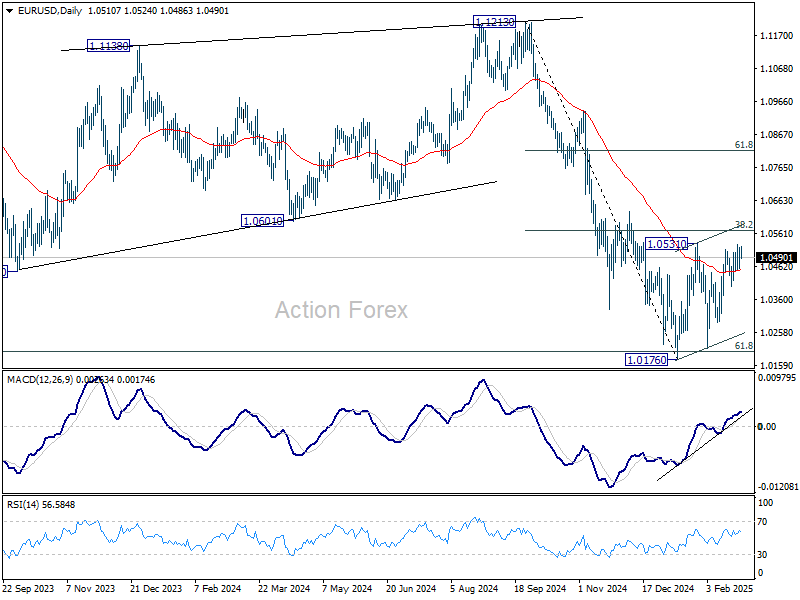

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0474; (P) 1.0497; (R1) 1.0537; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. Price actions from 1.0176 are seen as a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

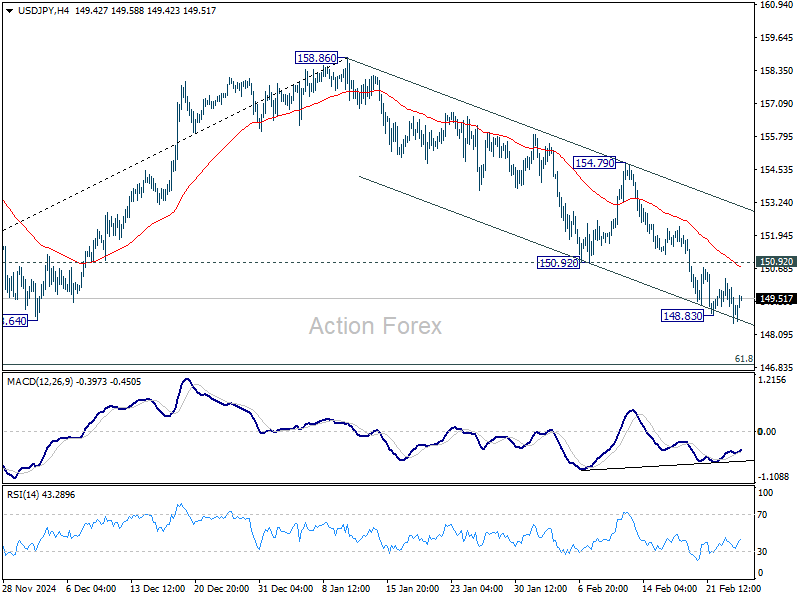

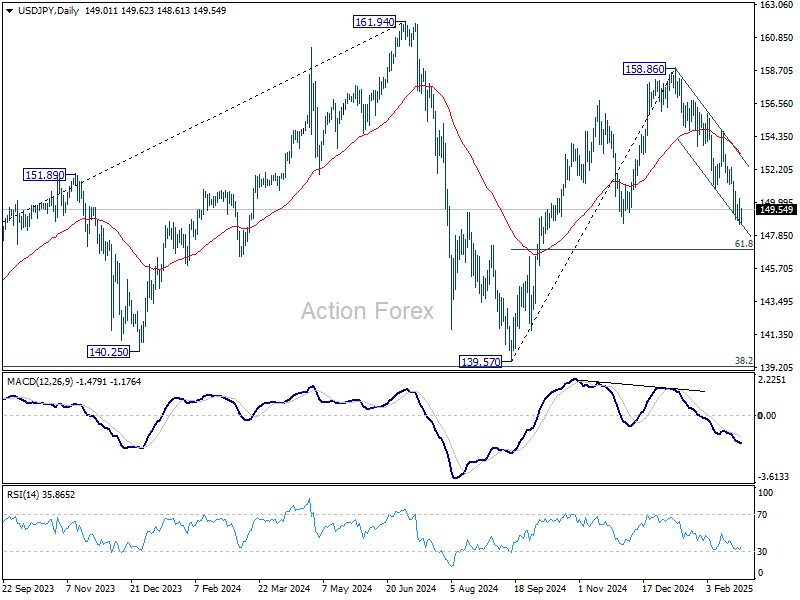

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.30; (P) 149.30; (R1) 150.03; More...

USD/JPY's fall from 158.86 resumed after brief consolidations and intraday bias back on the downside. This decline is seen as the third leg of the pattern from 161.94 high. Further fall should be seen to 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, however, break of 150.92 support turned resistance will indicate short term bottoming and bring stronger rebound.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

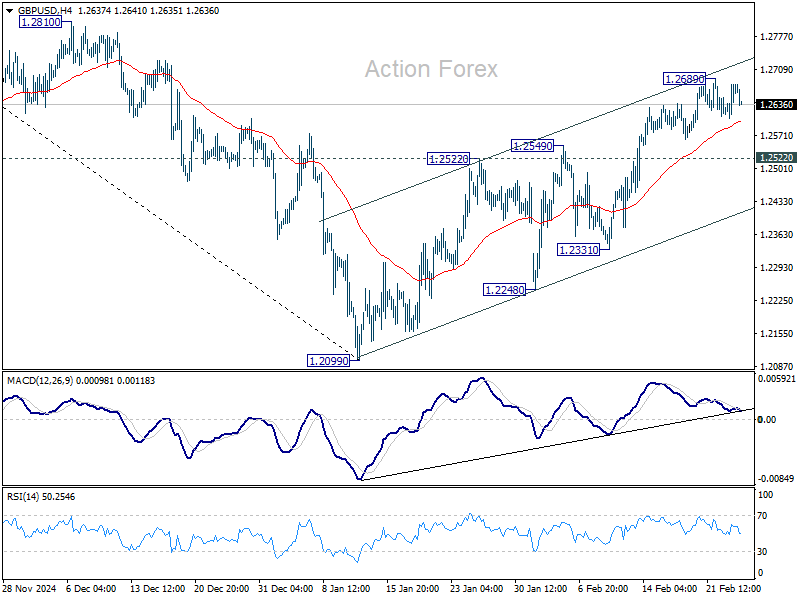

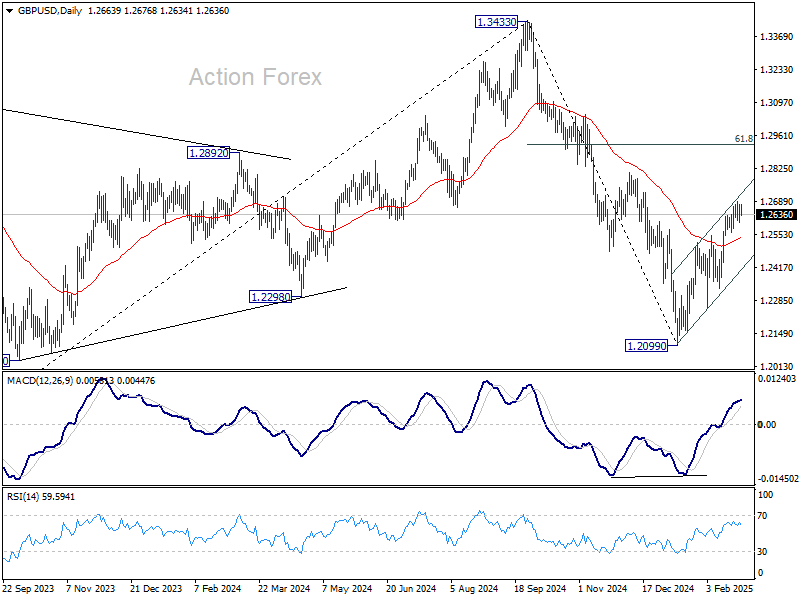

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2623; (P) 1.2650; (R1) 1.2695; More...

GBP/USD is staying in consolidation below 1.2689 temporary top and intraday bias remains neutral. Further rally is in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rise from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

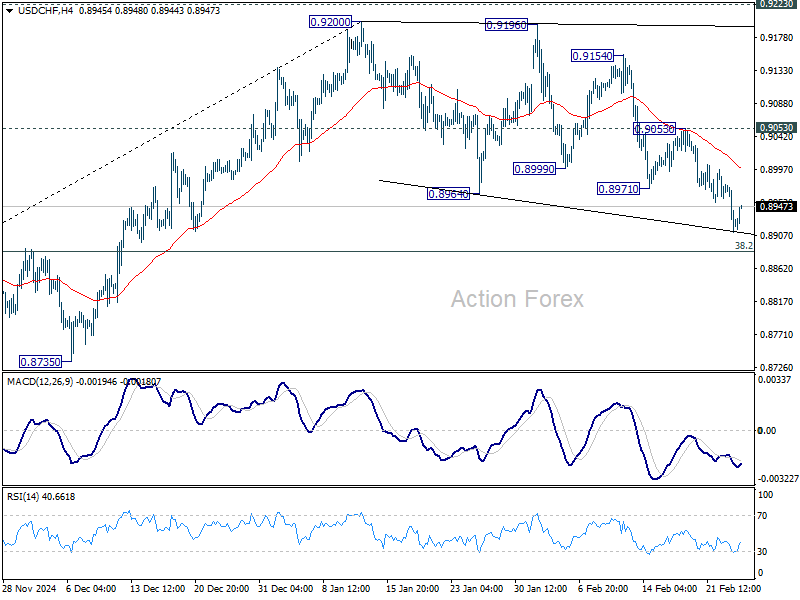

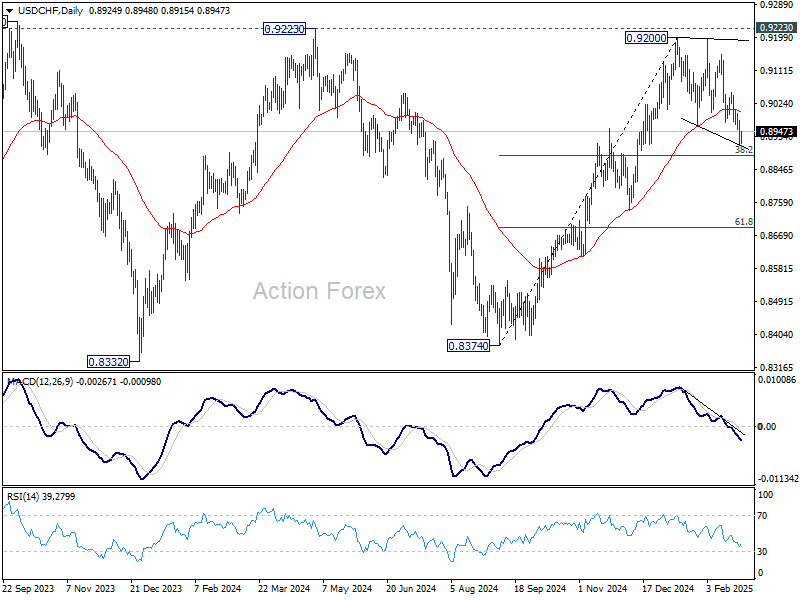

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8900; (P) 0.8941; (R1) 0.8971; More…

No change in USD/CHF's outlook as price actions from 0.9200 are still seen as a corrective pattern only. Strong support should be seen from 38.2% retracement of 0.8374 to 0.9200 at 0.8884 to complete it, and bring larger rise resumption. On the upside, above 0.9053 will bring retest of 0.9200 resistance. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

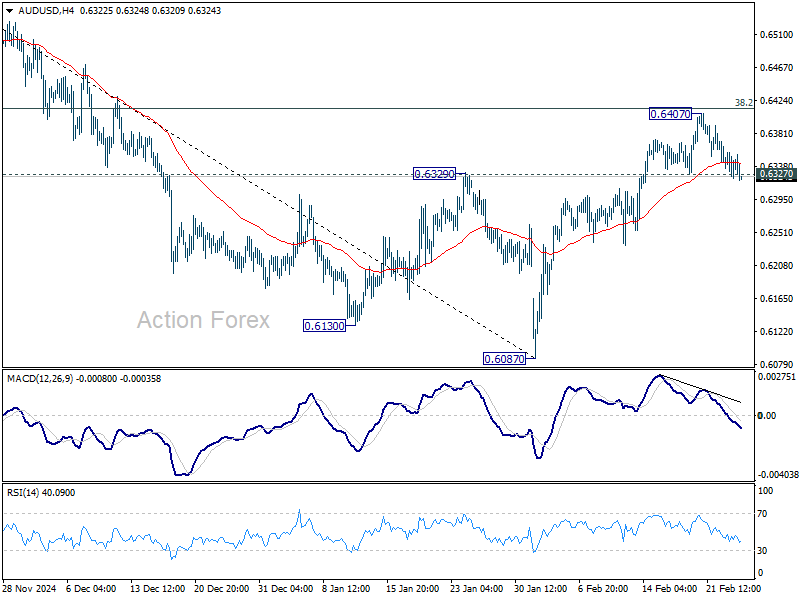

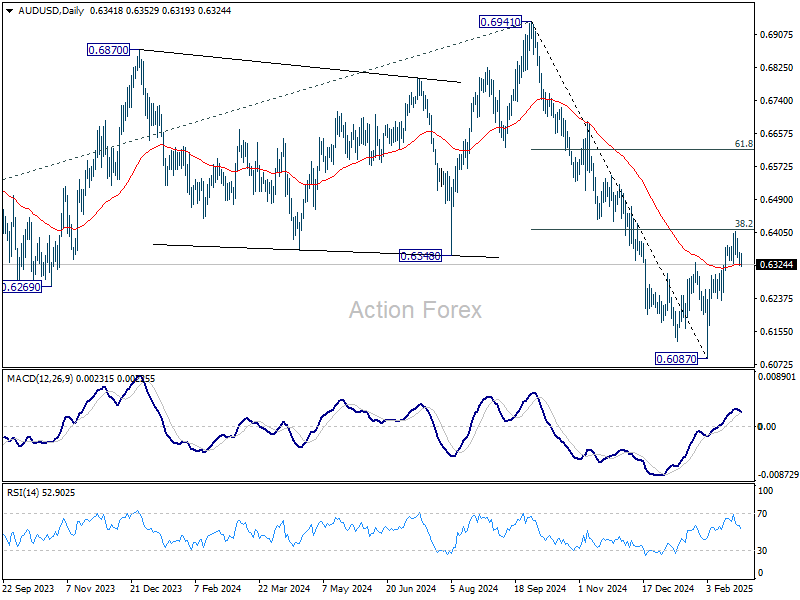

AUD/USD Daily Report

Daily Pivots: (S1) 0.6325; (P) 0.6341; (R1) 0.6360; More...

Immediate focus stays on 0.6327 support in AUD/USD. Decisive break of 0.6327 will suggest that the corrective rebound from 0.6087 has completed ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Intraday bias will be turned back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 0.6413 will pave the way back to 61.8% retracement at 0.6615, even still as a correction.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.

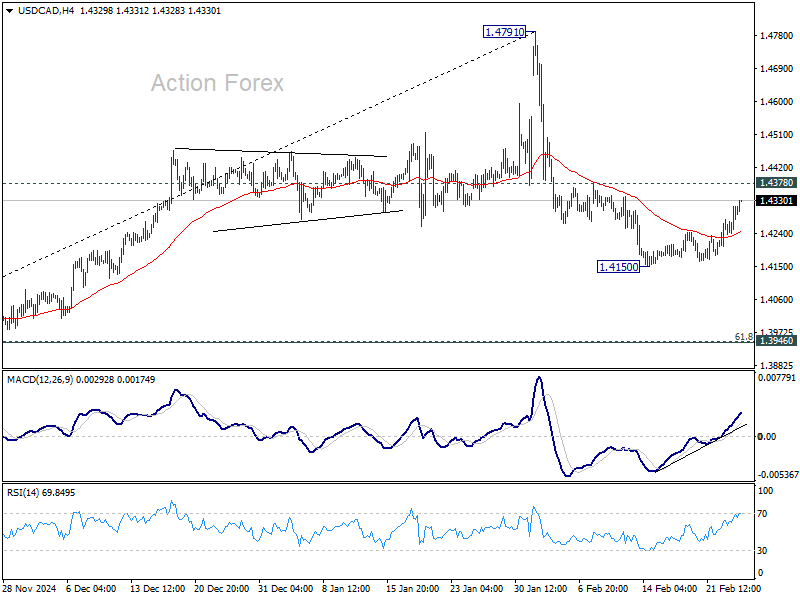

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4266; (P) 1.4293; (R1) 1.4345; More...

Intraday bias in USD/CAD stays neutral with focus turning to 1.4378 resistance as rebound from 1.4150 extends. Firm break there will suggest that the correction from 1.4791 has completed, and turn bias back to the upside for retesting 1.4791. On the downside, break of 1.4150 will target 1.3946 cluster support (61.8% retracement of 1.3418 to 1.4791 at 1.3942).

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Dollar Stuck Between Falling Yields and Risk Aversion, Struggles for Direction

Dollar remains stuck in a tug-of-war of conflicting forces. On one side, extended decline in US Treasury yields is pressuring the greenback, while on the other, risk aversion is offering some support.

10-year Treasury yield fell to its lowest level since December, looks on track to test the next Fibonacci support at 4.2%. Bond markets appear to be betting on a downturn, reflecting growing fears that the US economy could be headed for a rough landing as the administration's policies weigh on consumer confidence.

Meanwhile, risk aversion is pressuring US stock markets, indirectly giving Dollar some support as a safe-haven asset. S&P 500 closed lower for the fourth straight session, while NASDAQ shed -1% following weak consumer confidence data. The uncertainty surrounding tariffs, fiscal policy, and economic growth is amplifying recession fears, leading investors to seek refuge in bonds and defensive assets.

The key issue is that both declining yields and falling equities stem from the same core concerns—whether the US economy is losing steam faster than anticipated. Confidence in Washington's economic policies is rapidly deteriorating. This dual pressure on stocks and yields is keeping markets on edge, with Dollar stuck between a weakening growth outlook and flight-to-safety flows.

Adding to the market’s cautious stance is Nvidia’s highly anticipated earnings report, set to be released Wednesday after the bell. Given the company’s pivotal role in the AI-driven stock market rally, its results could have significant implications for risk sentiment for the near term.

In the currency markets, European majors are leading the session, with Swiss Franc being the strongest, followed by Euro and Sterling. On the weaker side, commodity currencies are underperforming, with Loonie being the worst, followed by Aussie and Kiwi.

Technically, the case of near term reversal in 10-year yield is building up after strong break of 38.2% retracement of 3.603 to 4.809 at 4.348. Further break of 50% retracement at 4.206 will argue that fall from 4.809 is indeed another leg inside the medium term corrective pattern from 4.997. That would set up deeper decline to 61.8% retracement at 4.063 and below.

In Asia, at the time of writing, Nikkei is down -0.72%. Hong Kong HSI is up 3.03%. China Shanghai SSE is up 0.64%. Singapore Strait Times is down -0.18%. Japan 10-year JGB yield is down -0.0086 at 1.368. Overnight, DOW rose 0.37%. S&P 500 fell -0.47%. NASDAQ fell -1.35%. 10-year yield fell -0.095 to 4.298.

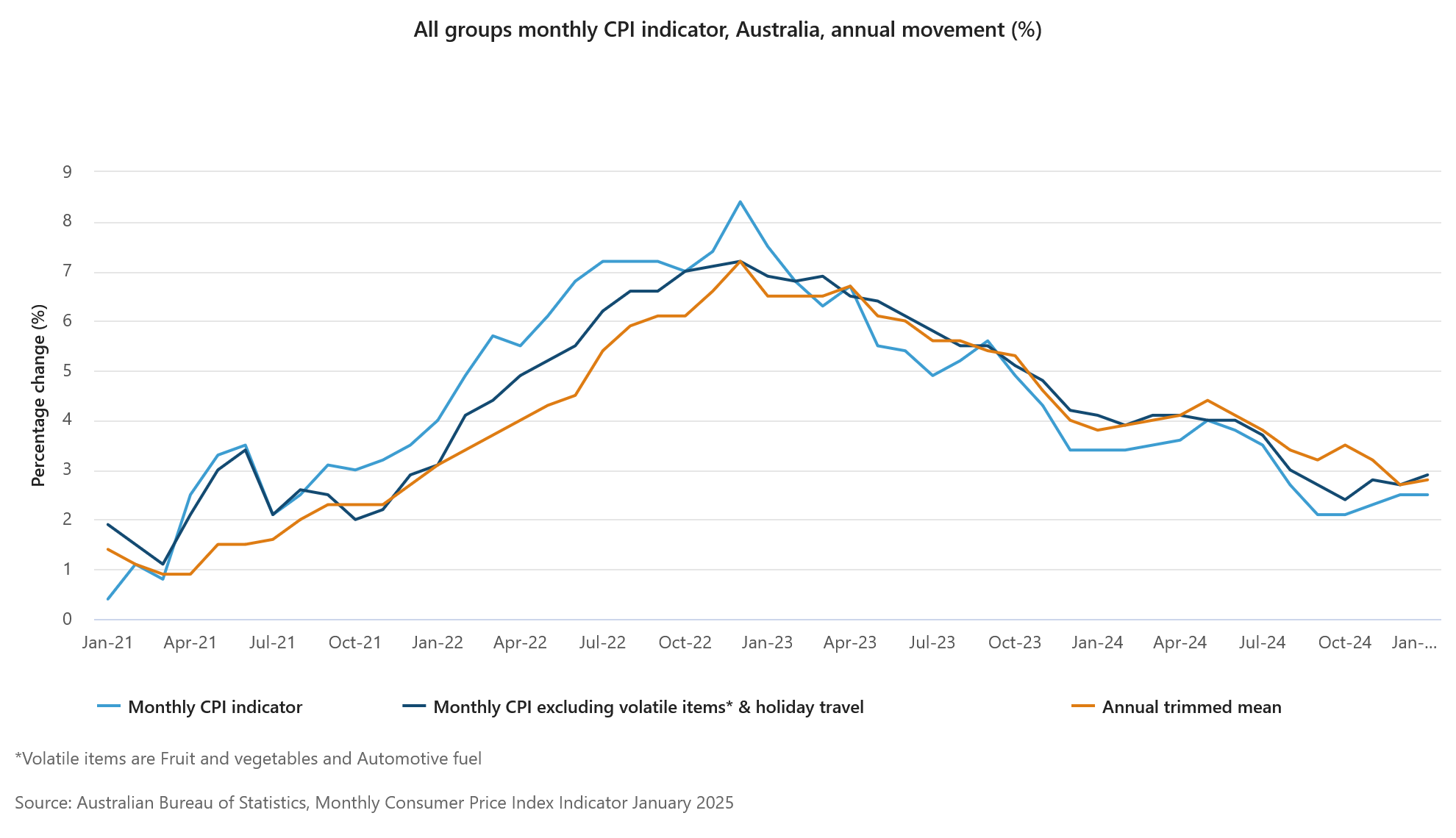

Australia’s monthly CPI holds at 2.5%, core measures edge higher

Australia’s monthly CPI was unchanged at 2.5% yoy in January, falling short of expectations for a slight uptick to 2.6%.

However, underlying inflation pressures showed signs of persistence, with CPI excluding volatile items and holiday travel rising from 2.7% yoy to 2.9% yoy. Trimmed mean CPI edged up from 2.7% yoy to 2.8% yoy.

These figures suggest that while headline inflation appears stable, core price pressures are still lingering, reinforcing RBA’s cautious stance on further easing.

The largest contributors to annual inflation included food and non-alcoholic beverages (+3.3% yoy), housing (+2.1% yoy), and alcohol and tobacco (+6.4% yoy).This was partly offset by a notable decline in electricity prices, which fell -11.5% yoy.

Fed’s Barkin: Staying modestly restrictive until inflation risks clear

Richmond Fed President Tom Barkin highlighted the need for a “modestly restrictive” monetary policy stance until there is greater confidence that inflation is firmly returning to the 2% target.

Speaking in a speech overnight, Barkin emphasized the importance of remaining “steadfast” in tackling inflation, warning that history has shown the risks of easing policy too soon.

“We learned in the '70s that if you back off inflation too soon, you can allow it to reemerge. No one wants to pay that price,” he cautioned.

Barkin acknowledged the high level of uncertainty surrounding economic policy changes, geopolitical tensions, and natural disasters, all of which could influence inflation dynamics.

He noted that tariffs imposed during Donald Trump's first administration in 2018 added about 30 basis points to inflation. However, he cautioned that the effect of the latest round of trade policies is harder to predict, as firms may either pass costs onto consumers or absorb them.

Beyond trade policies, Barkin also flagged uncertainties around deregulation, tax policies, government spending, and immigration reforms, all of which could shape labor market dynamics and broader economic conditions.

Given these unknowns, he prefers to “wait and see how this uncertainty plays out” before advocating any adjustments to monetary policy.

Looking ahead

German Gfk consumer climate and Swiss UBS economic expectations will be released in European session. Later in the day, US will release new home sales.

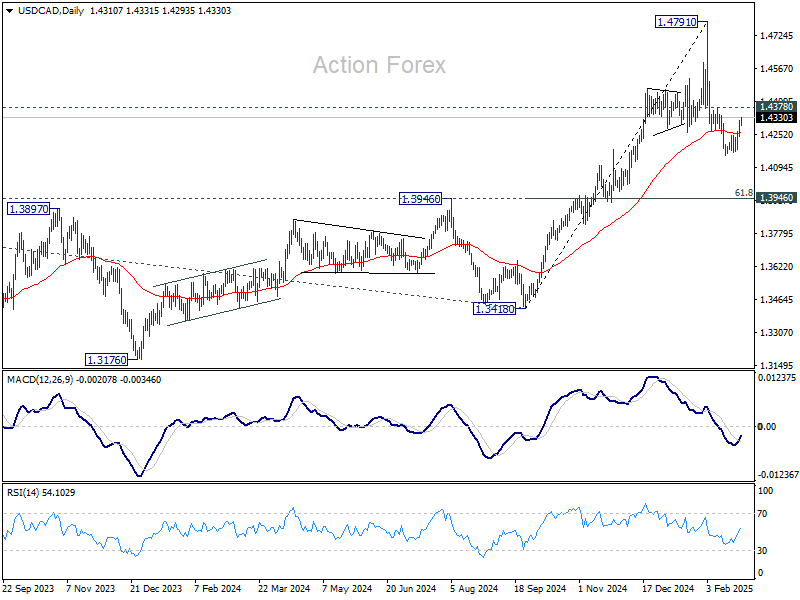

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4266; (P) 1.4293; (R1) 1.4345; More...

Intraday bias in USD/CAD stays neutral with focus turning to 1.4378 resistance as rebound from 1.4150 extends. Firm break there will suggest that the correction from 1.4791 has completed, and turn bias back to the upside for retesting 1.4791. On the downside, break of 1.4150 will target 1.3946 cluster support (61.8% retracement of 1.3418 to 1.4791 at 1.3942).

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Australia’s monthly CPI holds at 2.5%, core measures edge higher

Australia’s monthly CPI was unchanged at 2.5% yoy in January, falling short of expectations for a slight uptick to 2.6%.

However, underlying inflation pressures showed signs of persistence, with CPI excluding volatile items and holiday travel rising from 2.7% yoy to 2.9% yoy. Trimmed mean CPI edged up from 2.7% yoy to 2.8% yoy.

These figures suggest that while headline inflation appears stable, core price pressures are still lingering, reinforcing RBA’s cautious stance on further easing.

The largest contributors to annual inflation included food and non-alcoholic beverages (+3.3% yoy), housing (+2.1% yoy), and alcohol and tobacco (+6.4% yoy).This was partly offset by a notable decline in electricity prices, which fell -11.5% yoy.