Sample Category Title

AUD/JPY Outlook: Vulnerable for a Major Bearish Breakdown Below 93.65 Key Support

- Revigorated US trade tariffs threat on Canada spark refresh weakness in commodities proxy currencies such as AUD.

- AUD/JPY may face further headwinds supported by a further narrowing of the 2-year yield spread premium between Australian and Japanese government bonds.

- A further risk-off in the major US stock indices may also trigger further weakness in the AUD/JPY.

- Watch the 93.65 potential major downside trigger level of the AUD/JPY.

Despite a slew of less dovish rhetoric speeches from Australia’s central bank (RBA) Governor Bullock and Deputy Governor Hauser warmed market participants to tone down the expectation of further interest rate cuts in 2025 after RBA enacted its first 25 basis points cut in four years to reduce the cash policy rate to 4.1% on last Tuesday, 18 February, the AUD/USD has failed to kickstart a bullish momentum run.

On the contrary, the Aussie dollar could not maintain its earlier gains against the US dollar from 18 February to 21 February. Instead, the AUD/USD recorded a decline of 1.3% from an intraday high of 0.6409 on 21 February to a current level of 0.6329 at this time of writing.

Risk-off in US stock indices and Trump’s incoming 25% trade tariffs on Canada

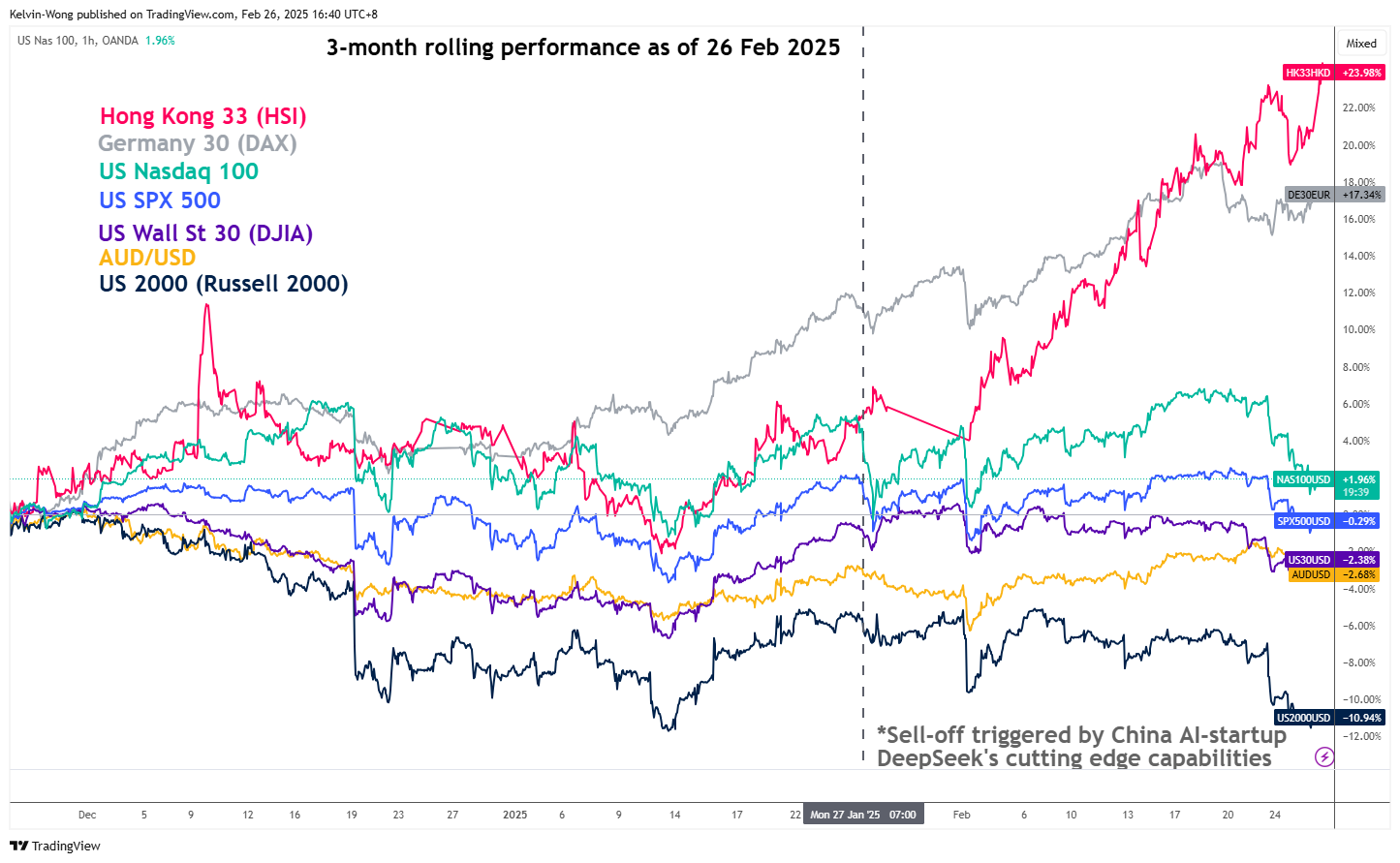

Fig 1: 3-month rolling performance of AUD/USD with major US stock indices as of 26 Feb 2025 (Source: TradingView, click to enlarge chart)

The Aussie dollar is considered a high-beta currency that has a higher sensitivity toward sentiment swings in the global stock market and commodities especially base metals as well as a direct correlation with other commodities proxy currencies such as the Canadian Loonie (CAD).

US President Trump has highlighted that the earlier planned 25% tariffs on Canadian exports to the US were scheduled to hit Canada on time next Tuesday after the “cooling off period” ends on 4 March.

Based on a five-day rolling performance basis, the Loonie (CAD) is the weakest major currency against the US dollar where it shed 0.6% at this time of the writing, and the Aussie dollar (AUD) trails behind with a loss of 0.2% against the US dollar.

Also, the lacklustre movements of the major US stock indices in the past month where the mega-cap and Artificial Intelligence (AI) centric S&P 500 and Nasdaq 100 have broken below their respective 50-day moving averages on Monday, 24 February, ignited a current risk-off sentiment behaviour that in turn triggered a negative feedback loop back into the Aussie dollar (see Fig 1).

Bearish technical elements remain intact on the AUD/JPY

Fig 2: AUD/JPY medium-term & major trends as of 26 Feb 2025 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis and an intermarket study, the 11 July 2024 swing high area of 107.85/109.40 may be considered as a medium-term top for the AUD/JPY cross pair, and its current prices are evolving into a potential medium-term downtrend phase (multi-week) in the first step.

The daily MACD trend indicator has been trending downwards steadily since 14 October 2024. It broke below its centerline on 27 November 2024 and at this time of the writing, it has flashed out an impending MACD bearish crossover condition below the centerline.

These observations suggest that the downward movement seen on the AUD/JPY in place since the 7 November 2024 high may extend further to the downside as its medium-term bearish trend condition remains intact.

Intermarket analysis also advocates further potential weakness on the AUD/JPY as the yield spread between the 2-year Australian Government Bonds and Japanese Government Bonds (JGB) has continued to narrow since 31 October 2023 and it has staged a recent bearish breakdown below its previous 11 December 2024 swing low of 3.20%. Right now, the 2-year yield spread between the sovereign bonds of Australia and Japan is trading 20 bps lower at 3%.

Watch the major support of 93.65 defined by the lower boundary of the long-term secular ascending channel from the March 2020 low, and a break with a weekly close below 93.65 may trigger the start of a potential multi-week corrective decline sequence to expose the next medium-term supports at 90.14 and 87.00 in the first step (see Fig 2).

On the flip side, clearance above the 97.24 key medium-term pivotal resistance invalidates the bearish tone for a retest on the next medium-term resistance at 99.60 (also the 200-day moving average), and above it sees the next resistance coming in at 102.30 (7 November 2024 swing high).

USD/CHF Rebounds from Yearly Low

As shown in the USD/CHF chart, the exchange rate dipped below 0.89250 Swiss francs per US dollar yesterday—the lowest level since December 2024. The Swiss franc, often seen as a safe-haven currency, may gain appeal due to:

→ heightened geopolitical tensions;

→ uncertainty surrounding Trump's plans to impose trade tariffs on 4 March.

Technical Analysis of USD/CHF

Fluctuations in 2025 have formed a downward channel (marked in red), with bearish sentiment prevailing in February as key psychological levels continue to be breached (as indicated by arrows):

→ in mid-February, bears pushed the price down from 0.905;

→ later, 0.900 acted as resistance.

If bearish momentum persists, further resistance may emerge around 0.895 and the median of the downward channel.

The upcoming market direction will likely be influenced by key economic data releases:

→ Swiss GDP (11:00 GMT+3) and US GDP (16:30 GMT+3) tomorrow;

→ US Core PCE Price Index (16:30 GMT+3) on Friday—an important inflation gauge.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBP/USD Gains Strength While EUR/GBP Recovers

GBP/USD is attempting a fresh increase from the 1.2600 zone. EUR/GBP is gaining pace and might extend its upward move above the 0.8300 zone.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is attempting a decent increase above the 1.2620 zone against the US Dollar.

- There is a connecting bullish trend line forming with support at 1.2625 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP started a fresh increase above the 0.8285 resistance zone.

- There is a major bullish trend line forming with support at 0.8300 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair started a downside correction from the 1.2690 zone. The British Pound traded below the 1.2650 zone against the US Dollar.

A low was formed near 1.2605 and the pair is now attempting a recovery wave. There was a break above the 50% Fib retracement level of the downward move from the 1.2690 swing high to the 1.2605 low.

The pair even spiked above the 76.4% Fib retracement level of the downward move from the 1.2690 swing high to the 1.2605 low and settled above the 50-hour simple moving average.

On the upside, the GBP/USD chart indicates that the pair is facing resistance near 1.2675. The next major resistance is near the 1.2690 level. If the RSI moves above 60 and the pair climbs above 1.2690, there could be another rally. In the stated case, the pair could rise toward the 1.2750 level or even 1.2820.

On the downside, there is a major support forming near 1.2625. There is also a connecting bullish trend line forming with support at 1.2625. If there is a downside break below the 1.2625 support, the pair could accelerate lower.

The next major support is near the 1.2605 zone, below which the pair could test 1.2560. Any more losses could lead the pair toward the 1.2525 support.

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair started a fresh increase from the 0.8265 zone. The Euro traded above the 0.8285 level to move into a positive zone against the British Pound.

The EUR/GBP chart suggests that the pair settled above the 50-hour simple moving average and 0.8300. Immediate resistance is near 0.8305. The next major resistance for the bulls is near the 0.8320 zone.

A close above the 0.8320 level might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8365. Any more gains might send the pair toward the 0.8400 level in the coming days.

Immediate support sits near a major bullish trend line at 0.8300 and the 23.6% Fib retracement level of the upward move from the 0.8275 swing low to the 0.8305 high. The next major support is near the 0.8285 zone.

The 61.8% Fib retracement level of the upward move from the 0.8275 swing low to the 0.8305 high is also at 0.8285. A downside break below the 0.8285 support might call for more downsides.

In the stated case, the pair could drop toward the 0.8265 support level. Any more losses might send the pair toward the 0.8240 level in the near term.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Hopes Rest on Nvidia’s Shoulders

Yesterday was yet another ugly session for US stocks. The increasingly heavier weight of Trump talk, deteriorating relationships across the globe – except Russia – combined with higher inflation expectations on tariffs, the uptick in inflation and weakening expectations from US consumers are certainly to blame for the selloff in equities – that boost appetite in bonds, considered to be a safer investment option. Remember, last Friday, the data had showed that the US 5-10 year inflation expectations had spiked to the highest levels since 1995, another set of data yesterday – from Conference Board - approved concerns about rising inflation expectations and warned that consumer confidence declined for the third straight reading – the drop concerned all age and income groups. Also note that small businesses that have grown more optimistic about the America First policies are losing that optimism and have been severely cutting their capex plans... As such, small caps are extending losses below the 200-DMA, the mid caps, the same. The S&P500 extended losses yesterday, as well, and tipped a toe below the 100-DMA, while Nasdaq 100 retreated more than 1% - also testing levels below its own 100-DMA. Only the Dow Jones eked out gains yesterday thanks to gains in consumer staples and healthcare sectors, which are considered defensive industries. The rest... looked bad. Roundhill’s Magnificent 7 ETF for example dived more than 2%, Tesla tumbled more than 8% on news that its European sales nosedived 45% in January. The company sold less than 10’000 cars last month across Europe, a significant part of the decline is believed to be due to rising frustration about Elon Musk political involvement in European countries’ domestic affairs. Nvidia lost 2.80% and tested its 200-DMA to the downside a day before announcing its quarterly earnings.

Happy Nvidia day

Nvidia will reveal its Q4 earnings today, after the bell, and expectations are strong. The company is expected to have increased its quarterly sales to $38bn last quarter on the back of the launch of Blackwell chips and sustained spending from Big Tech companies. Note that TSM results were strong during the same quarter, as well. Moreover, the company’s forecast should be strong, as well, on the back of Stargate project and further spending pledges from the Big Tech companies. Big Tech companies that include names like Meta, Microsoft, Apple, Amazon, are nothing to be minimized as they made up to 50% of Nvidia’s revenue in the Q3. And the fact that they are looking for premium chips for game-changing innovations could turn to be an advantage for Nvidia in the short run, though the risk of high concentration should be addressed in the medium to long-run given that these companies are working to launch their own chips. Besides that, investors will also monitor other risks, including supply chain and capacity issues, profit margins, rising competition and the developments in China with DeepSeek claiming to have built its AI model on cheaper versions of Nvidia chips. Also, Morningstar warns that Nvidia chips dominate only 40% of GPUs used for inference training – that’s the process of drawing conclusions based on evidence and reasoning rather than direct statements or observations – and that, for inference, there could be increased competition for chips. All in all, investors are very much used to see impressive results, therefore the risk factors could reverse optimism from strong results. Add to that the fact that the market environment is not ideal these days, Nvidia has the heavy task of lifting the market mood this week. If it can not, the selloff in stocks could accelerate despite the falling yields. Note that the technology selloff is also impacting mood in cryptocurrencies. Bitcoin plunged below the $86K level yesterday, another weakening leg of the early Trump optimism.

In the FX

The US dollar remained under the pressure of trade and geopolitical worries and bad data. The EURUSD made another attempt on the 1.05 offers but is still below this level this morning, while sterling bulls continue to fight the bears against the US dollar near the 100-DMA. But hey, the mood in the European stock markets is somewhat different than the US. The Stoxx 600 was slightly positive yesterday, near a record high level.

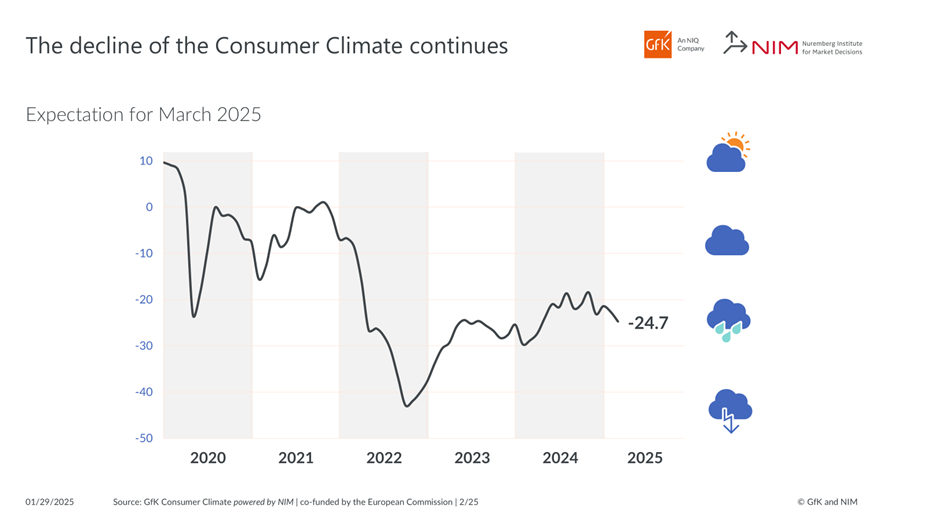

German Gfk consumer sentiment drops to -24.7, no sign of recovery yet

Germany's GfK Consumer Sentiment Index for March declined further from -22.6 to -24.7, missing expectations of -21.1.

February data showed income expectations plunging -4.3 points to -5.4, marking a 13-month low, while the economic outlook for the next 12 months improved slightly by 2.8 points to 1.2.

According to Rolf Bürkl, consumer expert at NIM, the data highlights that "no signs of a recovery" are visible in German consumer sentiment. He noted that headline index has been stuck at a low level since mid-2024, with "great deal of uncertainty among consumers and a lack of planning security".

Significant Deterioration of US Consumer Confidence Highlighted Current Worries

Markets

Same dynamics were at play for a third session straight with US assets starting to discount the possibility of a stagflation rather than a goldilocks scenario for the US economy. Key US stock markets lost 0.50% for the S&P 500 and 1.35% for the Nasdaq. EUR/USD tested the YtD top at 1.0533 again, but failed to break beyond. US Treasuries extended their rally with US yields losing around 10 bps across the curve, falling below YtD support levels. The US Treasury’s $70bn 5-yr Note auction copied the success of Monday’s $69bn sale, stopping through the 1:0 pm WI and producing strong bidding metrics. A significant deterioration of US consumer confidence (February) highlighted current worries. The Conference Board gauge fell from 105.3 to 98.3 with especially the forward looking expectations index suffering. In particular, pessimism intensified about future employment prospects (DOGE?!), while a growing number of consumers see a recession is likely over the next 12 months. German Bunds outperformed US Treasuries with yields slipping a more modest 2 bps across the curve. ECB data showed negotiated wage growth in Europe slowing from a record 5.4% Y/Y pace in Q3 to 4.1% in Q4. This level remains very uncomfortable and probably strengthens hands of policy hawks to argue in favour of a rate cut pause after the ECB lowers its policy rate from 2.75% to 2.5% in March.

US Treasuries lose some ground this morning after House Republicans passed a budget blueprint (see News & Views). It’s an important step towards extending tax cuts and avoiding bumping into the debt ceiling early next month. US equity futures and the dollar equally trade somewhat stronger. European news centers around the Ukrainian agreement to a mineral-rights deal with the US which Ukrainian president Zelensky would sign in Washington on Friday. It would be a first face-to-face meeting between the two after the US initially started brokering a peace deal with Russia. The deal doesn’t include US security guarantees (yet). It only suggests that Ukraine would pay some proceeds from future mineral resource development into a fund that would invest in projects in Ukraine. The size of the US stake in the fund and joint ownership deals need to be specified later on. Today’s eco calendar only contains second tier numbers, leaving more room for general risk sentiment to set the overall tone. We’d continue to err on the side of caution despite this morning’s signs of improvement. Nvidia earnings (after market close) are a wildcard.

News & Views

The US House of Representatives passed a budget resolution in a tight 217-215 vote that could pave the way for huge spending and tax cuts. The resolution offers the broad framework for Trump’s “big beautiful bill” and proposes around $2tn of reduced expenses but a much bigger $4.5tn of lower taxes. The resolution is now headed to the Senate. While the GOP there has a larger majority, Senate republicans favor even larger tax cuts, making amendments to the resolution highly likely. That would mean it the House needs to vote on the altered version again. Once the House and Senate do agree on the same budget, the subsequent bill can be pushed through faster and more easy than usual through the so-called reconciliation process (which avoids the 60-vote threshold in the Senate required for most bills). The US non-partisan Committee for a Responsible Federal Budget estimated that the current House-approved bill would add at least $2.8tn (or $3.4tn including interest costs) to deficits through 2034. Deficits would then average 6.8% of GDP over the decade instead of 5.8% under current law. That pushes up the debt ratio to 125% (compared to 117% if no bill passes).

The Hungarian central bank (MNB) delivered kept the policy rate at 6.5% yesterday. Both headline and core CPI of 5.5% and 5.8% are well above the central bank’s target. “Incoming data provide evidence that the risk of a higher inflation path this year has increased further.” The MNB now thinks inflation will return to the 3% +/- 1 ppt tolerance band later than projected in December. The technical recession in Hungary came to an end in 2024Q4 (+0.5% Q/Q) and growth should strengthen further on the back of consumption. Budapest noted that investor sentiment has improved (i.e. the forint has strengthened), a.o. due to the geopolitical developments. However, “the uncertain international environment and the outlook for inflation warrant the maintenance of tight monetary conditions.” The forint came close to the symbolical EUR/HUF 400 barrier yesterday but stayed shy from testing.

Ukraine and US Have Agreed to Terms on Minerals Deal

In focus today

Today, the EU Commission is set to publish its "Clean Industrial Deal", which is the Commission's grand strategy on how to revitalise manufacturing and meet climate goals. A leaked draft shows that the Commission intends to introduce "Made in the EU" quotas and carbon product labels. It focuses on reducing energy costs, stimulating demand, fostering investment, ensuring access to critical raw materials, developing global partnerships, and reskilling workers.

In Sweden, producer prices are released at 08:00 CET. While PPI consumer goods domestic supply usually aligns close with CPI, recent trends show rising PPI since October, while the CPI has moved sideways to lower. Somewhat simplified, this indicates a pressure on margins for companies.

Economic and market news

What happened yesterday

On the geopolitical scene, Ukraine agreed to terms with the US on a minerals deal. The deal does not entail any US security guarantees or continued flow of weapons. However, the deal can be seen as part of a bigger puzzle, broadening relations with the US to strengthen Ukraine's prospects after three years of war, according to Ukraine's deputy prime minister and justice minister who led the negotiations. Zelenskyy is planning to travel to Washington on Friday to sign the deal. We are hosting a webinar tomorrow (27 February) from 09:30 to 10:00 CET with our analysis of the current situation. Please use the following link to attend the session: Webinar - The new security disorder in Europe - what are the economic implications?, 27 February.

In the US, the Conference board's sentiment survey mirrored the weakening seen in the University of Michigan's sample earlier. The forward-looking economic expectations declined, while labour market indicators, including the "jobs plentiful"-index, also weakened slightly. Inflation expectations climbed higher, increasing to 6.0% from 5.2%, which marks the highest level since May 2023. The marked surges in inflation expectations over the recent months likely reflect household's perception of tariffs' impact on inflation. We believe that the Fed will be sidelined in March and May, but still think the cutting cycle is far from over.

Turning to the Fed, Richmond Fed President Barkin (hawk and non-voter) stressed the need to remain cautious on inflation amid current uncertainty. Dallas Fed president Logan (hawk and non-voter) was also on the wire emphasizing that the Fed's balance sheet would work best when the maturities of its securities holdings roughly match with US Treasury issuances. Importantly, Logan noted that the Fed is not considering changes to its implementation framework.

In politics, the House of Representatives passed a budget resolution calling for trillions of dollars in tax and spending cuts, extending Trump's 2017 tax cuts, and delivering a massive boost to his 2025 priorities. The vote on the resolution was 217-215. The deal proposes USD 4.5tn in tax cuts, about USD 2tn in spending cuts and allocates hundreds of billions of dollars more to immigration enforcement and the military. The Senate is now set to discuss the budget resolution.

In the euro area, the ECB's negotiated wages indicator declined to 4.1% y/y in Q4 from 5.4% in Q3. We stress that one should cautiously interpret the indicator as it is rather volatile currently amid the mining of one-off inflation compensation payments. That said, looking across alternative wage indicators, the notion of fading wage pressures is underpinned along inflation easing.

In Hungary, the central bank kept the policy rate unchanged at 6.5% as widely anticipated.

In commodities space, Brent crude oil fell sharply, dropping below USD74/bbl, seemingly due to the souring risk appetite that may partly relate to the yesterday's weaker US consumer confidence figures. Demand concerns related to trade woes and weaker US key figures continue to outweigh potential supply concerns from the recent tightening of sanctions on Iran's oil exports. We anticipate Brent prices to average USD 75/bbl in Q1 and rise to USD 85/bbl in Q4.

Equities: Global equities were lower again, with renewed growth fear amid weaker US macro data. Europe managed to defy the sour sentiment and rose 0.3%, whereas S&P sold off -0.5% and Nasdaq -1.4%. This takes S&P 500 -3% off its peak, Nasdaq -5% and Russell -11% off its 2024 record and -6% since the sell-off early February. Meanwhile, Stoxx 600 is only decimals away from a new record high. So, the weakness has really been ringfenced to the US. Same story this morning, with Asian markets bouncing higher driven by Chinese tech (Hang Seng 3%). On a global scale, the defensive rotation has been substantial, with defensive sectors outperforming cyclicals by 5p.p. the last week. This rotation continued Tuesday with tech and consumer discretionary (Tesla -8%) underperforming while yield sensitive homebuilders, off-priced stores, staples and health care fared better. US futures are higher this morning.

FI: Global yields continued drifting lower through yesterday's session due to a range of factors, including the softening of the US Conference Board Consumer confidence survey in February. 10Y US Treasury yields dropped 10bp to 4.29%, the lowest level of the year, with markets adding to expectations of additional Fed easing this year. The direction of yields was also downward pointing in Europe, but to a much lesser extent. Bunds saw significant underperformance following the speculations that the current Bundestag will rush through a softening of the German debt brake rules before convening on 25 March. The Bund ASW spread dropped to an all-time low of -5.2bp in the early part of the session, but most of the move faded in the afternoon. Longer term inflation swap rates fell for the third session in a row along with energy prices.

FX: JPY rallied, and NOK came under pressure yesterday amid souring risk sentiment and a sell-off in oil. USD/JPY fell below 149 and EUR/USD rose back above 1.05.

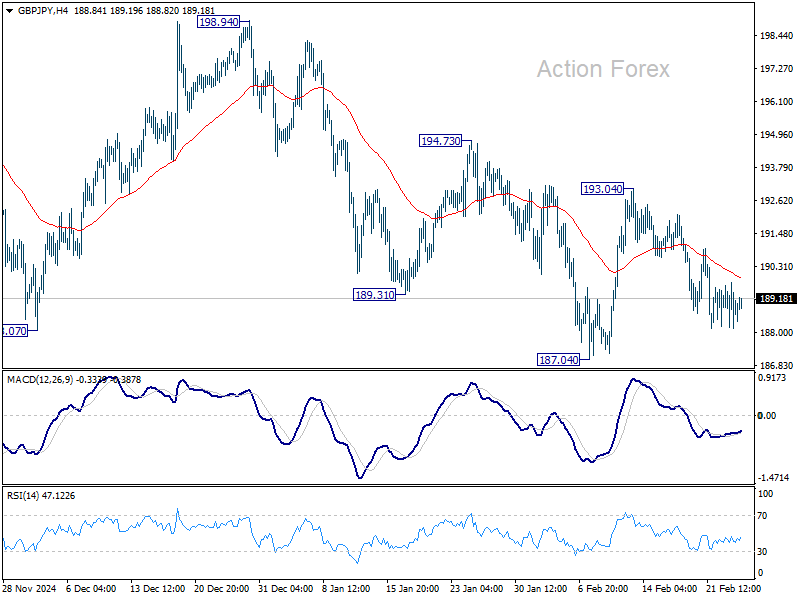

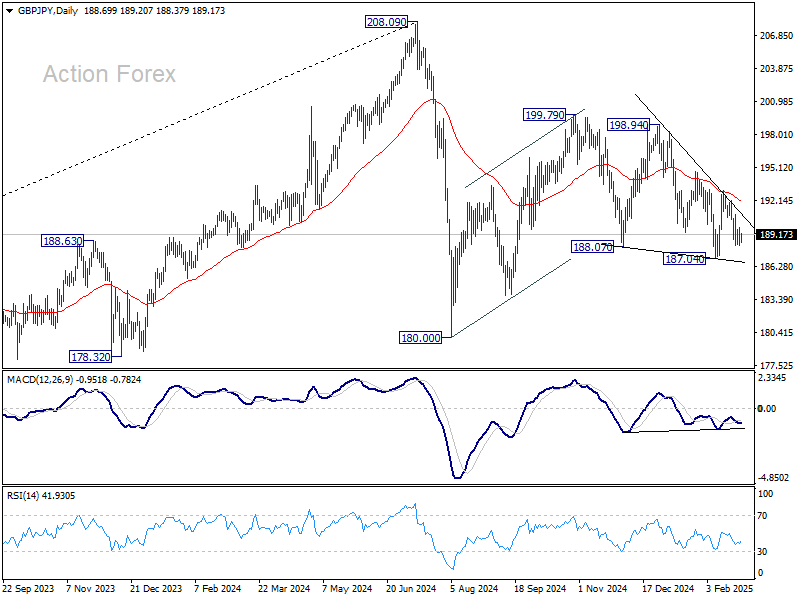

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.04; (P) 188.89; (R1) 189.62; More...

Outlook in GBP/JPY is unchanged and intraday bias stays neutral. Risk will be mildly on the downside as long as 193.04 resistance holds. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

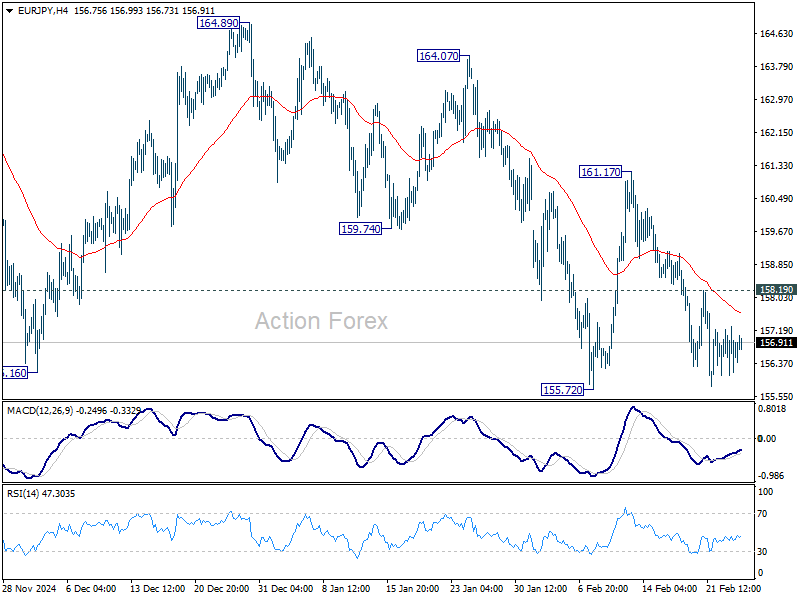

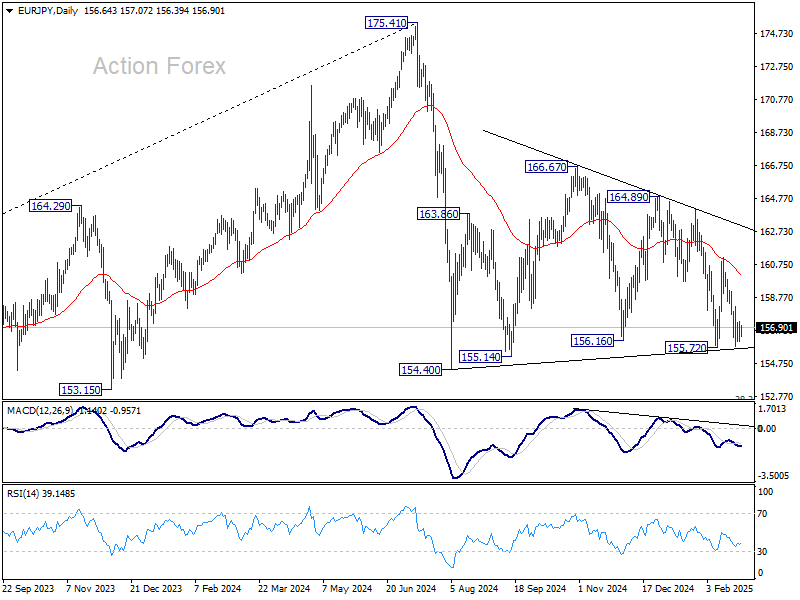

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.09; (P) 156.70; (R1) 157.32; More...

No change in EUR/JPY's outlook and intraday bias stays neutral. On the downside, firm break of 155.72 will be a strong sign that whole fall from 175.41 is resuming. Retest of 154.40 support should be seen next and firm break there should confirm. However, break of 158.19 resistance will turn bias back to the upside and extend the corrective pattern from 154.40 with another rising leg.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

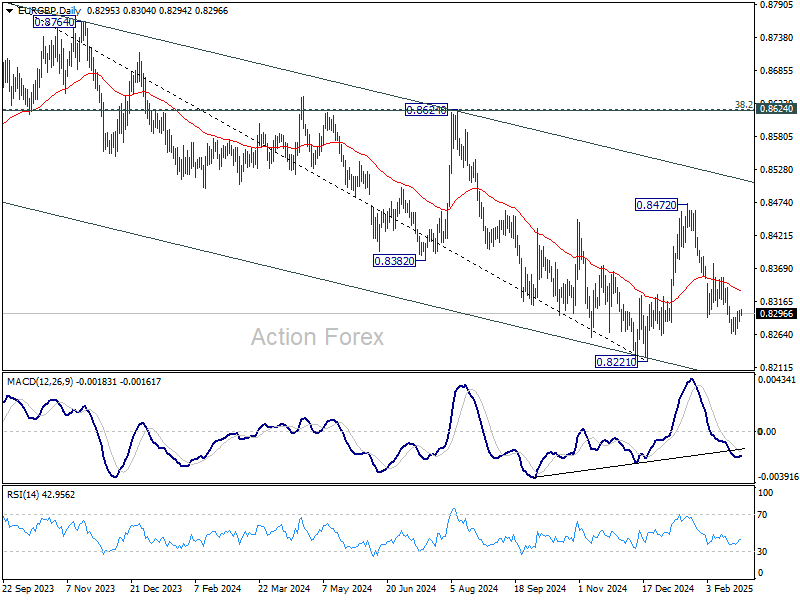

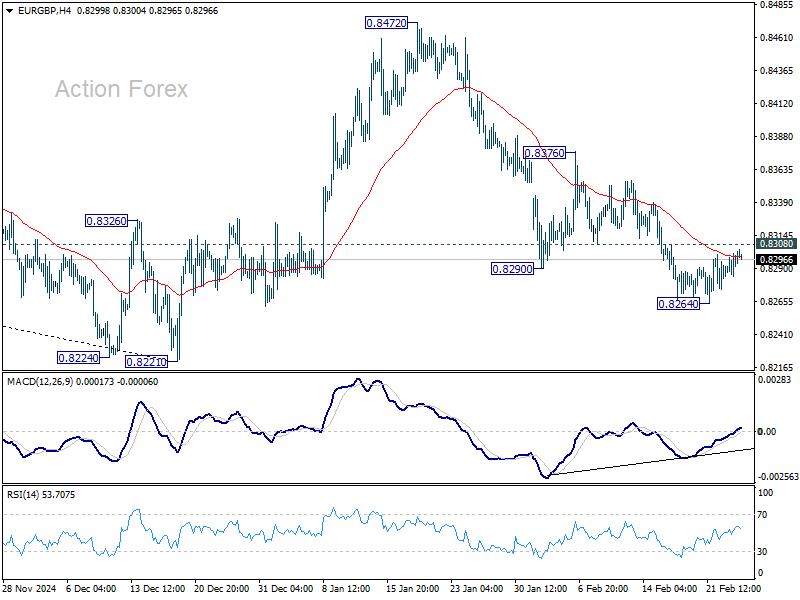

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8288; (P) 0.8296; (R1) 0.8309; More...

No change in EUR/GBP's outlook and intraday bias stays neutral at this point. Another fall is expected as long as 0.8308 minor resistance holds. Below 0.8264 will resume the whole decline from 0.8472 to retest 0.8221 low. Nevertheless, firm break of 0.8308 minor resistance will turn bias back to the upside for stronger rebound to 0.8376 resistance instead.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.