Sample Category Title

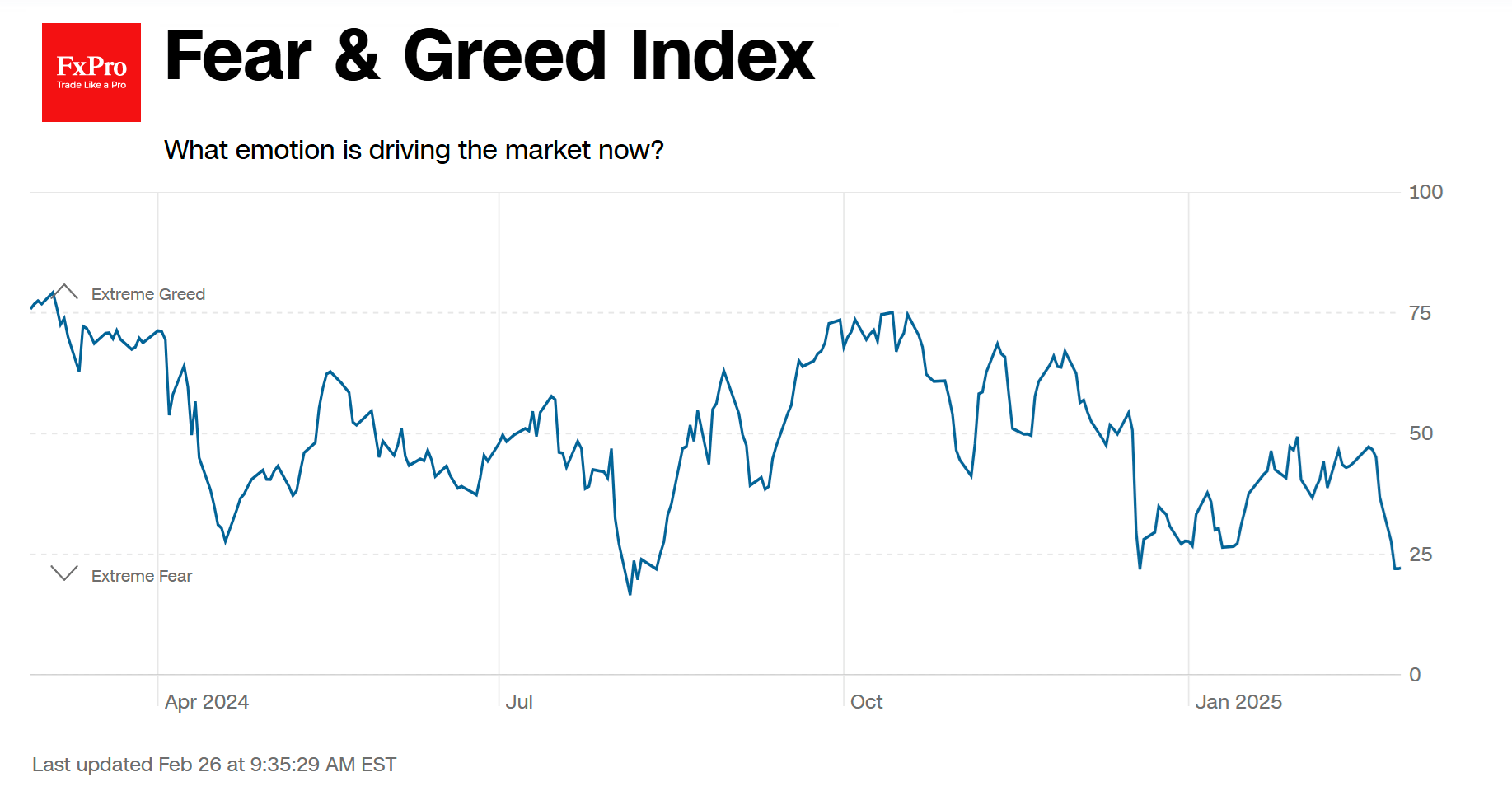

Fear in Stocks Hasn’t Crossed the Line Yet

Extreme fear is driving US stock indexes, according to a popular CNN Business index. Their index has fallen to 22, repeating December’s lows. Only in early August last year did the indicator dip below 22 for a few days. An area of extreme fear is often seen as an attractive time to buy. However, the dynamics of the past year are forcing some adjustments to this rule. In both August and December, the lows of the Fear and Greed Index were well ahead of the market lows and would have forced rash investors to endure several anxious sessions, even if they were able to buy at the peak of fear effectively.

It was much more rational to stay on the sidelines and join the rally only after the sentiment index had risen sharply out of fear territory.

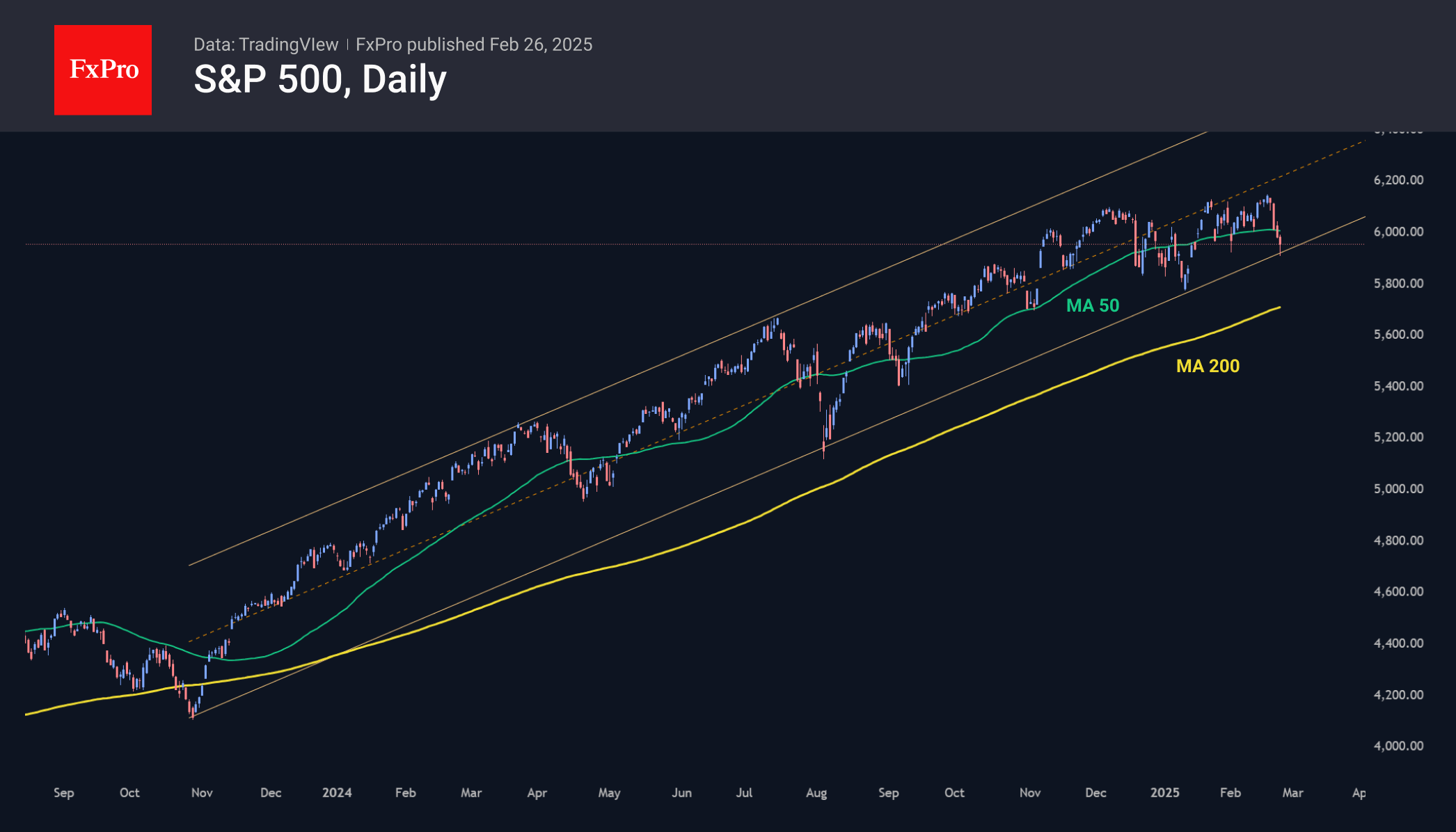

Let’s look at the individual indices. The S&P500 was back below 6000 at the start of the week and below its 50-day moving average. Since the second half of January, it had been heavily bought on touching this curve, but the buying strength was clearly not enough to push it further into historical highs. At Tuesday’s low, the S&P500 was close to the lower boundary of the ascending channel that has been in place since late 2023. A break below 5900 could trigger a broader sell-off in equities well beyond the US. An even more dramatic scenario could be triggered by a break below the 200-day moving average (now at 5750).

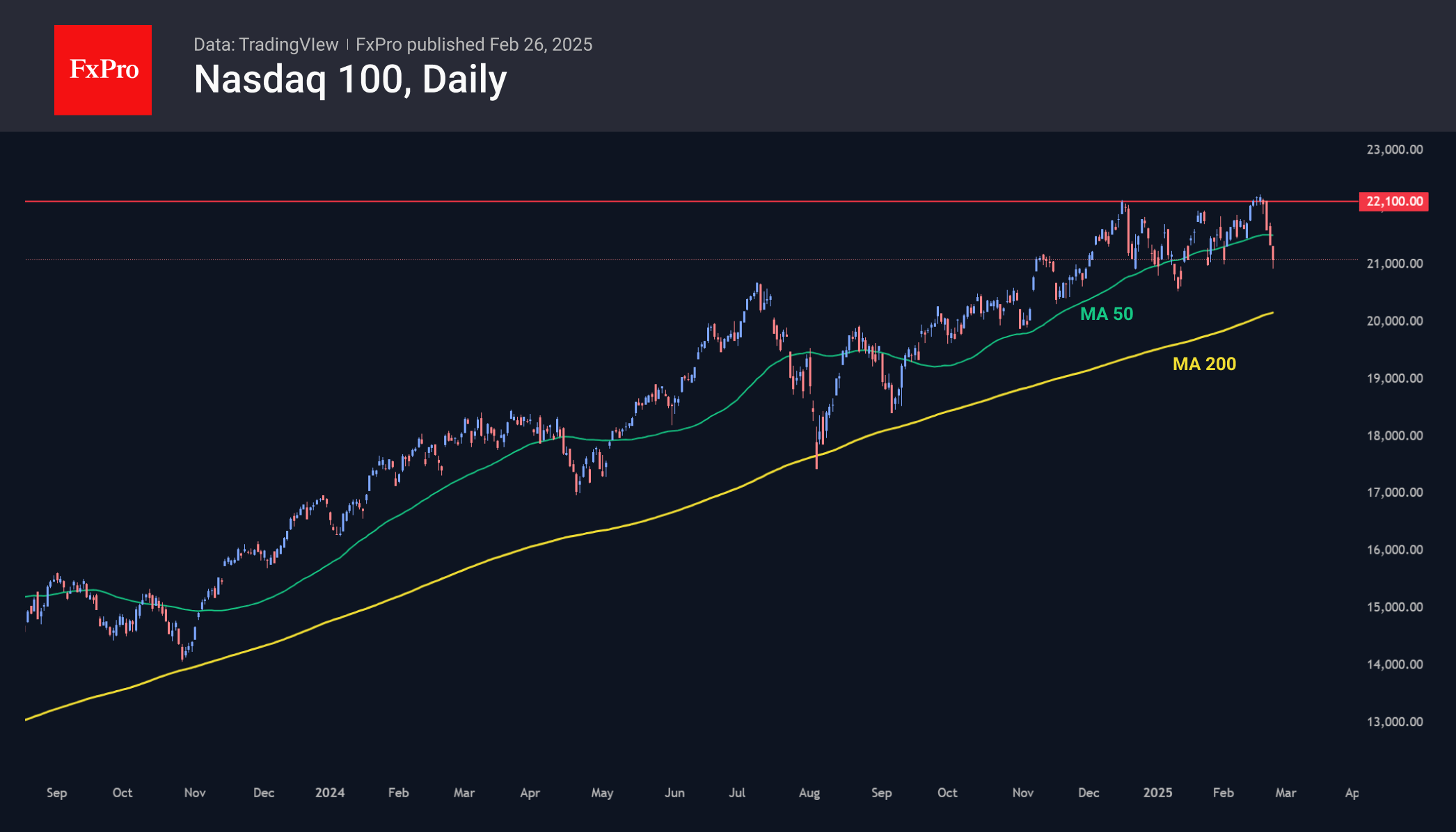

Indirect warning signals include the double tops on the Nasdaq100 and Dow Jones indices, which is a trend reversal pattern. It is important to note that the tops on the indices were formed at different times, which reduces their correlation and thus increases their significance.

At the same time, the basic scenario in such cases is still a rebound from the lower boundary and a move towards the upper boundary, which is now above 6600. The bulls are temporarily favoured by the relatively subdued dynamics of the VIX. This volatility index remains below 20, the level above which is often the first signal that the market is going into selling mode.

Sunset Market Commentary

Markets

The three-day rally in US Treasuries came to a halt today. An empty eco calendar played a part in that following three days of stagflationary worries (PMI’s, Michigan consumer confidence, Conference Board consumer confidence). More importantly, the US House passed a budget resolution that could pave the way for huge spending and especially tax cuts. The resolution is now headed to Senate where it will likely be amended as Senators target even more than the $4.5tn of lower taxes. Once the House and Senate are on the same line, legislation can pass via simple majority reconciliation process. US treasury yields are close to unchanged suggesting it’s way too soon to call the correction already over. Q4 Nvidia earnings after US close tonight could already be an important test for general sentiment. European trading lacked guidance from the eco calendar as well. Solid corporate earnings and the mineral-rights deal between the US and Ukraine (to be signed in Washington on Friday) pushed European stock markets up to 1% higher. Changes on bond markets were minimal with EUR/USD camping just below the 1.0533 resistance (YTD top).

The Flemish Community launched its first syndicated benchmark deal of the year. They issued a long 12y bond (Jun2037) which was priced 20 bps over the Belgian OLO curve. That’s 5 bps tighter than guidance in the OLO +25 bps area. Books were above €4.4bn allowing Flanders to print €1.5bn. Flanders Department of Finance estimates new funding needs for 2025 at roughly €11bn, the lion share of which is to cover new funding needs (€7.1bn). The funding need mainly stems from an estimated budget deficit of €3.4bn and other (recurring) funding needs such as the Flemish Social Housing Company (VMSW €0.8bn), the Flemish Housing Fund (VWF €1.41bn) and costs related to the Oosterweel link (LANTIS €0.8bn). Debt redemptions for 2025 are projected at €3.9bn. For its 2025 financing mix, Flanders hopes to raise €3.25-3.75bn via regular benchmarks, €1.25-1.50bn via sustainability (green) benchmarks, €0.75-1bn via private placements and €0.4bn through EIB loans.

News & Views

The Institute of International Finance (IIF) in its Global Debt Monitor reported the world’s debt stock rose to a new annual record high of $318tn in 2024. The debt-to-GDP ratio neared 328% in 2024, in what was the first (1.5 ppt) uptick since 2020 amid slowing economic growth. While the $7tn increase of last year was less than half of 2023’s, the IIF still warned persistent rising fiscal deficits are attracting growing market scrutiny. The governments’ share in the global stock of debt amounted to $95tn. The IIF forecasts a further $5tn rise this year though warned this could be even more due to calls for fiscal stimulus and defense spending in Europe. On a geographical level, emerging markets – driven by China, India, Saudi Arabia and Tukey – accounted for roughly two-thirds of 2024’s global debt growth.

Chief of staff to Hungary’s PM Orban Gulyas in an interview with news site 24.hu said GDP growth this year will likely be lower than the official government growth target of 3.4%. Economic growth of 2%-3% seemed more realistic, he said. As the 3.4% estimate still forms the basis of the 2025 budget approved end last year, it means the 3.7% deficit penciled in already appears outdated. That’s especially the case with the Orban administration trying to (fiscally) revive the economy ahead of next year’s parliamentary elections. Orban’s Fidesz party is trailing the Tisza Party since the end of 2024. The Tisza Party gained rapidly in popularity after former Fidesz member Peter Magyar resigned out of discontent with government functioning and took the lead of Tisza in early 2024.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0474; (P) 1.0497; (R1) 1.0537; More...

Intraday bias in EUR/USD stays neutral at this point. Price actions from 1.0176 are seen as a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

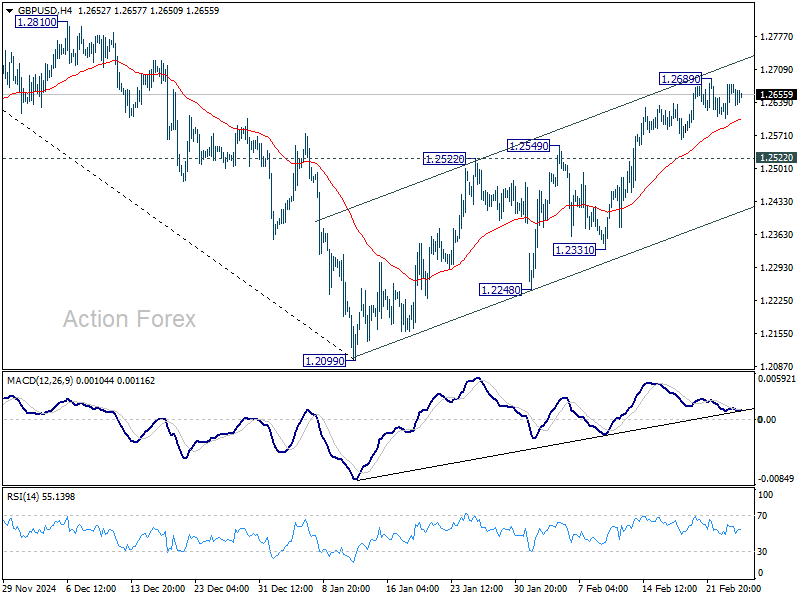

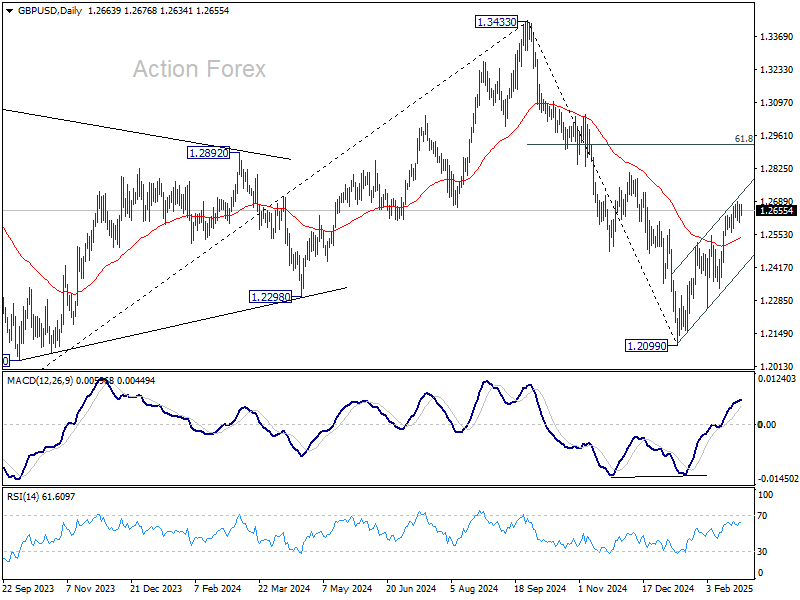

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2623; (P) 1.2650; (R1) 1.2695; More...

Intraday bias in GBP/USD remains neutral for consolidation below 1.2689. Further rally is in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rise from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

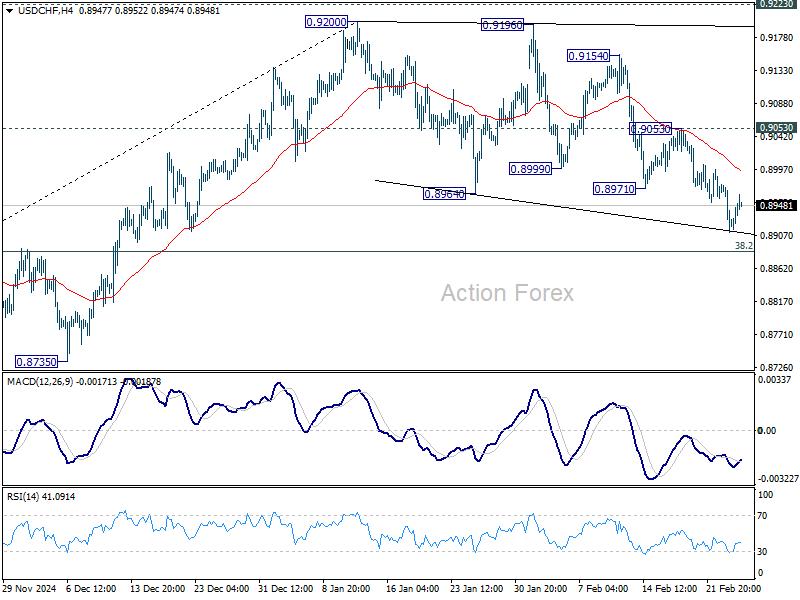

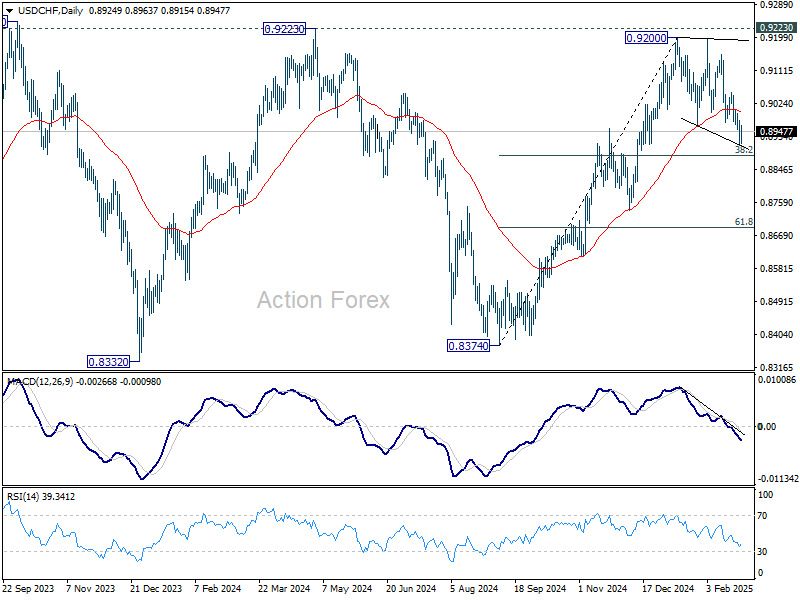

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8900; (P) 0.8941; (R1) 0.8971; More…

Outlook in USD/CHF is unchanged that price actions from 0.9200 are still seen as a corrective pattern only. Strong support should be seen from 38.2% retracement of 0.8374 to 0.9200 at 0.8884 to complete it, and bring larger rise resumption. On the upside, above 0.9053 will bring retest of 0.9200 resistance. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

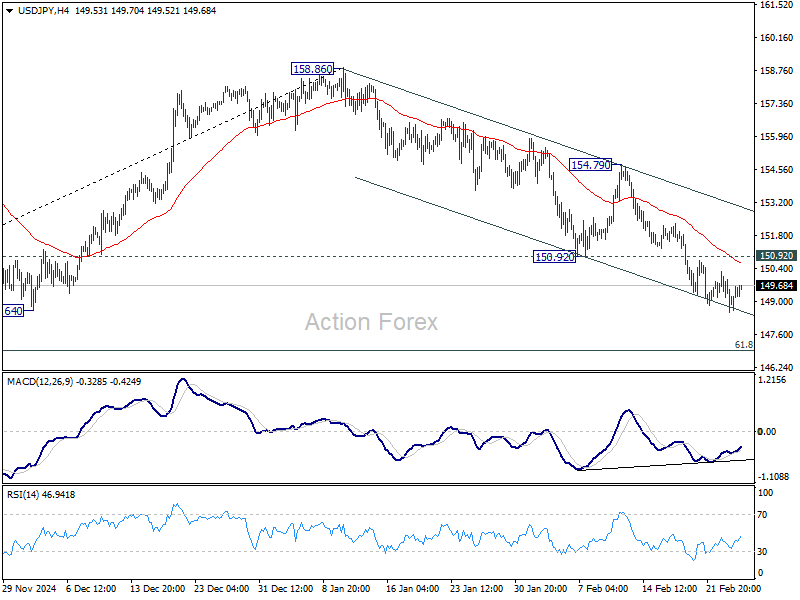

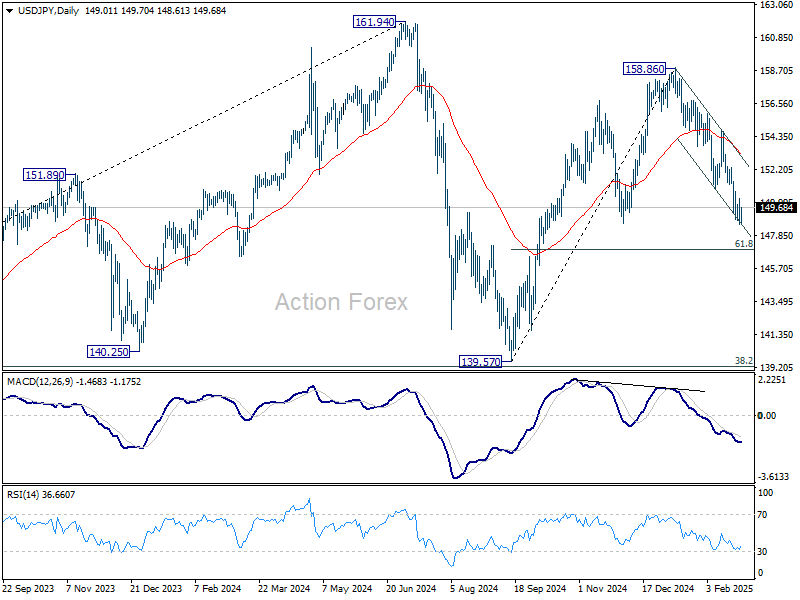

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.30; (P) 149.30; (R1) 150.03; More...

While downside momentum is not too convincing, further decline is expected in USD/JPY as long as 150.92 support turned resistance holds. Current fall from 158.86 is seen as the third leg of the pattern from 161.94 high. Deeper decline should be seen to 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, however, break of 150.92 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

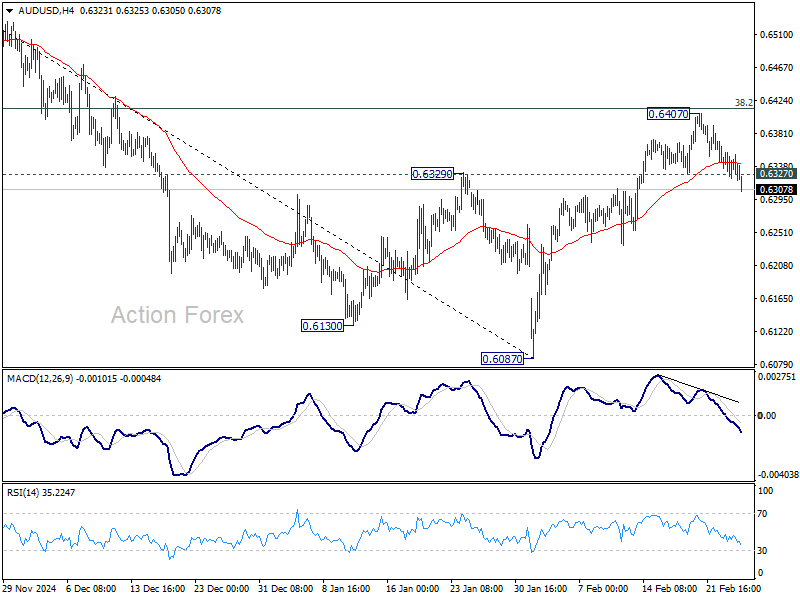

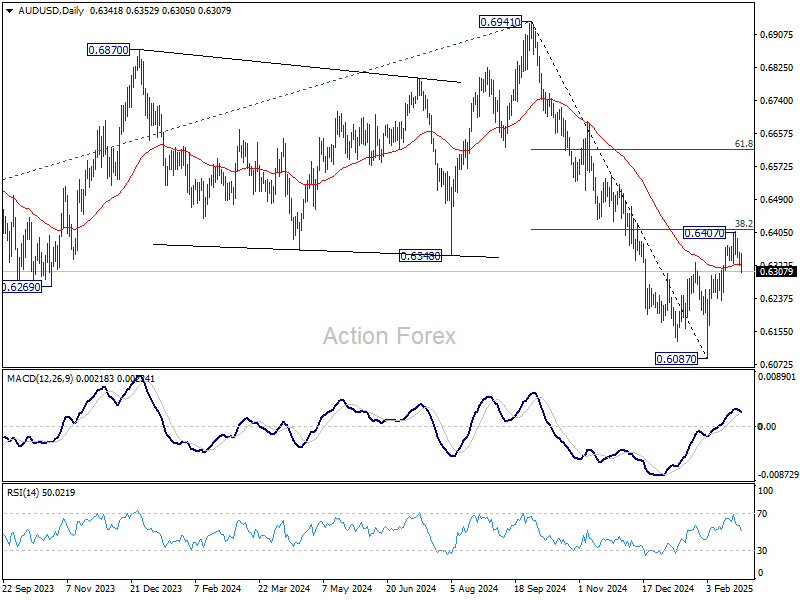

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6325; (P) 0.6341; (R1) 0.6360; More...

AUD/USD's break of 0.6327 support should confirm short term topping at 0.6407, on bearish divergence condition in 4H MACD. Corrective rebound should have completed just ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Intraday bias is back on the downside for retesting 0.6087 low. For now, risk will stay on the downside as long as 0.6407 holds, in case of recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.

Dollar Gathers Momentum, Gold Cools Off, Market Jitters Ahead?

Dollar appears to be gathering steam for a stronger, sustainable near-term rebound, although the precise catalyst remains unclear. One contributing factor an undercurrent of risk aversion, which is reflected in the broad selloff in the Australian and New Zealand Dollars. Yet, the overall market picture is mixed, as US stock futures inch higher and Treasury yields hold steady, hardly signaling a deep risk-off move or robust safe-haven flows.

Another explanation points to traders positioning ahead of Nvidia’s earnings release, due after the bell. With the AI-driven rally serving as a key theme for tech stocks, any surprise in the results could influence wider market sentiment, thereby affecting the currency markets. Additionally, speculation is building around the upcoming March 4 tariff deadline, when US levies on Canada and Mexico—postponed for a month to address border and fentanyl issues—are set to take effect.

At present, the greenback tops the leaderboard for the day, followed by Sterling and Loonie. Aussie and Kiwi lag, with Swiss Franc also underperforming. Euro and Yen are holding middle ground.

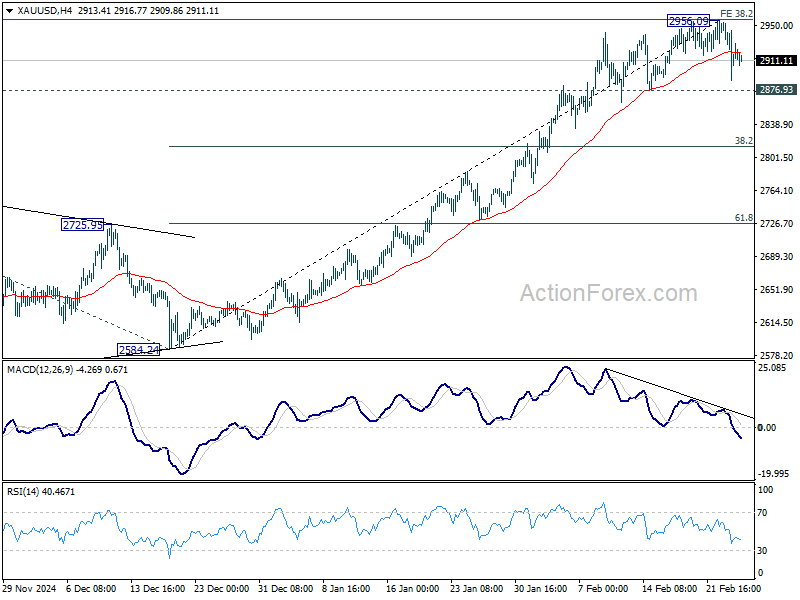

Technically, considering bearish divergence condition in 4H MACD, a short term top could already be in place in Gold at 2956.09, ahead of 3000 psychological level. Firm break of 2876.93 support should confirm this case, and bring deeper correction to 38.2% retracement of 2584.24 to 2956.09 at 2814.04. If realized, that would be a confirmation for Dollar's rebound.

In Europe, at the time of writing, FTSE is up 0.65%. DAX is up 1.69%. CAC is up 1.32%. UK 10-year yield is down -0.0316 at 4.483. Germany 10-year yield is down -0.032 at 2.429. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 3.27%. China Shanghai SSE rose 1.02%. Singapore Strait Times fell -0.20%. Japan 10-year JGB yield fell -0.0098 to 1.367.

German Gfk consumer sentiment drops to -24.7, no sign of recovery yet

Germany's GfK Consumer Sentiment Index for March declined further from -22.6 to -24.7, missing expectations of -21.1.

February data showed income expectations plunging -4.3 points to -5.4, marking a 13-month low, while the economic outlook for the next 12 months improved slightly by 2.8 points to 1.2.

According to Rolf Bürkl, consumer expert at NIM, the data highlights that "no signs of a recovery" are visible in German consumer sentiment. He noted that headline index has been stuck at a low level since mid-2024, with "great deal of uncertainty among consumers and a lack of planning security".

Australia’s monthly CPI holds at 2.5%, core measures edge higher

Australia’s monthly CPI was unchanged at 2.5% yoy in January, falling short of expectations for a slight uptick to 2.6%.

However, underlying inflation pressures showed signs of persistence, with CPI excluding volatile items and holiday travel rising from 2.7% yoy to 2.9% yoy. Trimmed mean CPI edged up from 2.7% yoy to 2.8% yoy.

These figures suggest that while headline inflation appears stable, core price pressures are still lingering, reinforcing RBA’s cautious stance on further easing.

The largest contributors to annual inflation included food and non-alcoholic beverages (+3.3% yoy), housing (+2.1% yoy), and alcohol and tobacco (+6.4% yoy).This was partly offset by a notable decline in electricity prices, which fell -11.5% yoy.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6325; (P) 0.6341; (R1) 0.6360; More...

AUD/USD's break of 0.6327 support should confirm short term topping at 0.6407, on bearish divergence condition in 4H MACD. Corrective rebound should have completed just ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Intraday bias is back on the downside for retesting 0.6087 low. For now, risk will stay on the downside as long as 0.6407 holds, in case of recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.

Crypto Market: Time for the Bold?

Market Picture

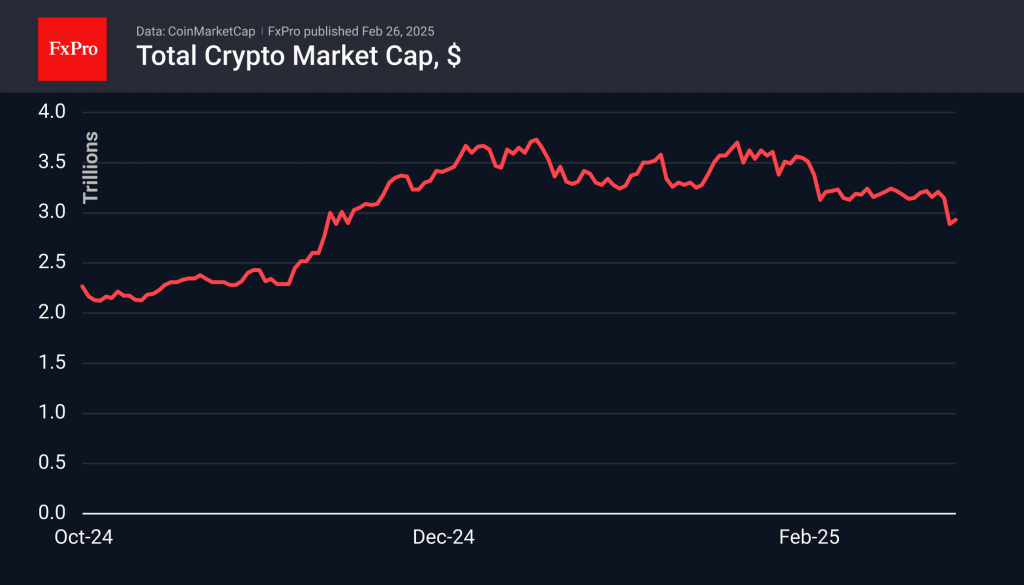

The crypto market fell below the support for the last three months on Tuesday, going into a brutal sell-off mode. Institutional investor sentiment didn’t help either, as US stock indices also saw a sell-off. Sentiment stabilised on Wednesday, and we see an attempt to form a bottom, pushing off from the $2.87T market cap and now up to $2.93T.

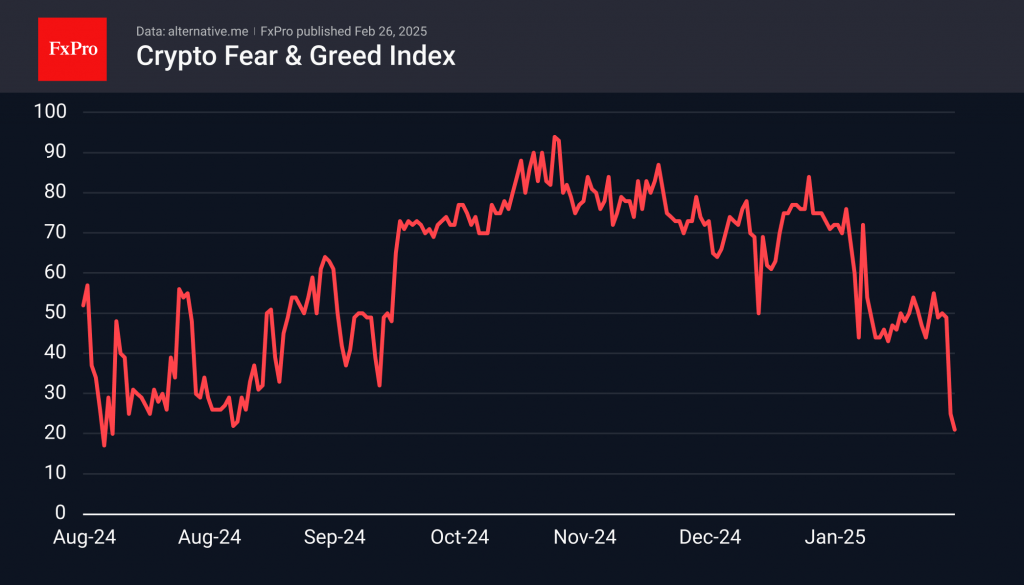

The cryptocurrency index has pulled back to the extreme fear area at 21, its lowest value since August last year. Earlier, we pointed out that the market lacked the drop into the fear region to attract greedy speculators. But now the question is whether those speculators have enough courage to buy.

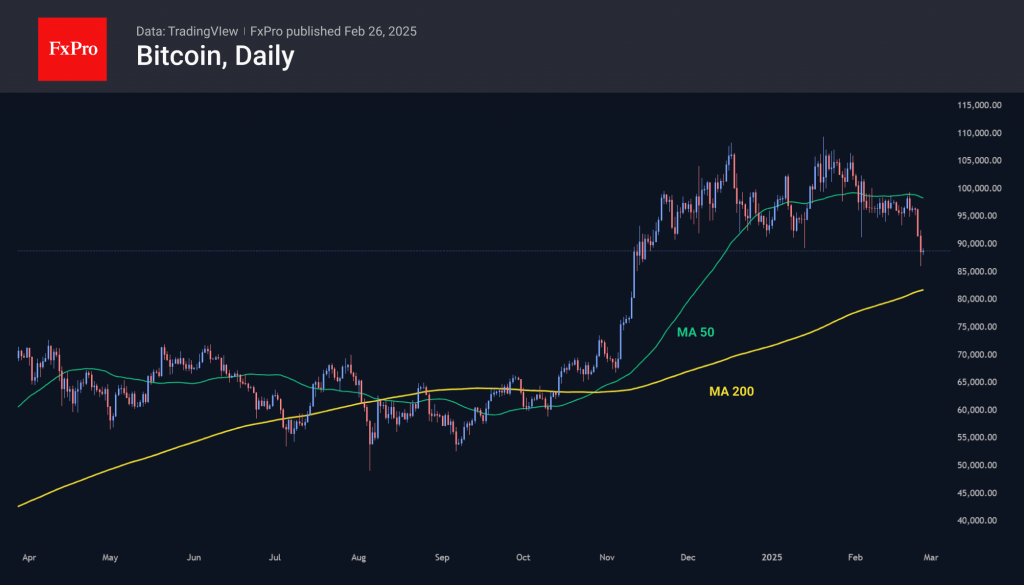

Bitcoin broke through support in the 92000 area on Tuesday, near where the 61.8% retracement level of the November-December rally was. Bitcoin has given up half of the gains of that rally. The local target for the bears now looks like the area of the 200-day moving average at 82000. But already, Bitcoin is walking the edge of a bear market, losing about 20% from the peak. Further declines could open the floodgates for expanded liquidation of long positions in the crypto. As usual, saying, ‘I’ll be greedy when everyone else is scared,’ is much easier when you don’t have skin in the game.

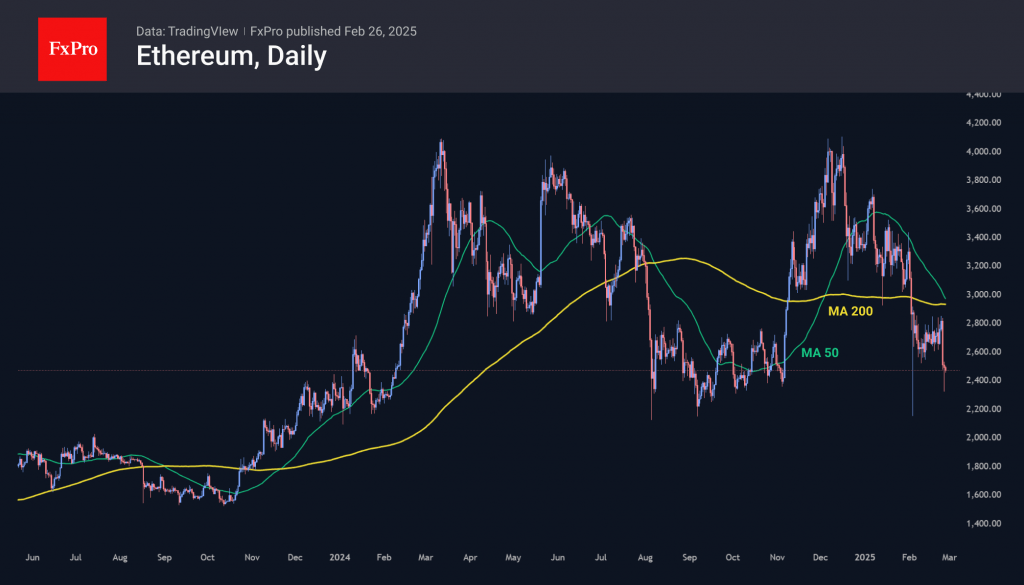

Ethereum and Solana have already rolled back to October-November levels, with huge technical potential for further capitulation. In the event of a further sell-off, Ethereum could fall another 35% to $1600, while Solana faces a much steeper potential decline of over 80% from its current price.

News Background

Bitcoin will fall to $70,000 if hedge funds liquidate positions in spot bitcoin ETFs, ex-BitMEX chief Arthur Hayes said. He noted that the funds are focused on gaining the so-called ‘basis spread,’ which is generated by the difference between longs in ETFs and shorts on CME-traded futures. The strategy looks attractive if its profit exceeds the yield on short-term US government bonds.

Strategy last week bought an additional 20,356 BTC for $1.99bn at an average price of $97,514. The company now holds 499,096 BTC worth $33.1bn at an average price of $66,357.

Pectra’s update to Holesky’s Ethereum testnet didn’t go according to plan, so the network stopped finalising slots. A bug related to Holesky’s features has already been identified, and it does not affect the main network in any way.

OKX will pay more than $504 million in settlement of the US Department of Justice claims. The exchange pleaded guilty to operating an unlicensed money transfer business in the US.