Sample Category Title

Currencies: Trade War Angst Continues To Weigh On The Dollar

Sunrise Market Commentary

- Rates: Cohn's resignation vs hawkish comments by Fed Brainard

The US Note future gapped open higher overnight on White House economic adviser Cohn's resignation and on rumours of more US tariffs against China. The move is countered by a shift in tone of dovish Fed governor Brainard who favours a faster rate hike cycle than before. Tomorrow's ECB meeting could subdue today's session. - Currencies: trade war angst continues to weigh on the dollar

Today, uncertainty on the US trade policy will remain the key factor for global FX trading. For now, the issue is a negative for the dollar. At the same time, Fed speak and US eco data stay USD supportive, but are ignored for now. FX traders will also look forward to tomorrow's ECB meeting. Will the ECB be soft enough to prevent further EUR/USD gains?

The Sunrise Headlines

US stock markets closed up to 0.5% higher (Nasdaq) yesterday. Risk sentiment deteriorated overnight after economic adviser Cohn's resignation and on rumours of more US tariffs against China.

Gary Cohn will resign from the White House as President Trump's top economic adviser, days after Mr. Trump surprised his senior staff by announcing steel and aluminum tariffs that Mr. Cohn had opposed.

Washington-based Fed governor Brainard; one of the central bank's most ardent doves, sounded optimistic about the US economy's outlook and suggested the pace of monetary policy tightening may need to accelerate.

The Trump administration is considering clamping down on Chinese investments in the US and imposing tariffs on a broad range of its imports to punish Beijing for its alleged theft of intellectual property, according to sources.

Opponents of Brexit are looking into whether Britain could postpone its exit from the EU to give lawmakers and voters more time to weigh up whether they really want to leave.

Australia's economic growth slowed last quarter (0.4% Q/Q) as bad weather hit exports, though government spending and a revival in household consumption helped the country extend its 26-yr run without recession.

Today's eco calendar contains US ADP employment. Fed Bostic and Dudley are scheduled to speak and the Fed releases its Beige Book. The Bank of Canada is expected to keep policy rates unchanged at 1.25%. Germany taps the market.

Currencies: Trade War Angst Continues To Weigh On The Dollar

Trade war debate continues weighing on USD

Yesterday, USD dollar selling eased temporary as markets hoped that senior Republicans could convince Trump to avoid a trade war. Around noon, South Korean officials declared that North Korea was prepared to talk about denuclearization. Risky assets jumped and so did USD/JPY and EUR/JPY. The EUR/JPY short-squeeze also propelled EUR/USD above the 1.24 level. Later in the session, the decline of the yen slowed as markets tried to assess the meaning of the Korean headlines. USD/JPY closed the day at 106.13. EUR/USD finished at 1.2414.

Overnight, Gary Cohn announced to resign as President Trump's top economic adviser. He disagrees with Trump's foreign trade policy. The announcement revived the risk-off trade. Fed Brainard (a dove) hinted that tailwinds to the economy could lead to a faster rate hike path. However, the focus for (FX) trading remains on US trade policy as US president Trumps still intends to defend US interests by protectionist measures. USD/JPY dropped to the mid 105 area. EUR/USD is hovering near 1.2425 even as EUR/JPY came off yesterday's top.

The US trade balance and the ADP labour market report will be published today. Several Fed members speak and the central bank publishes the Beige Book. Of late, most Fed members, even the doves, were optimistic on growth and US data were OK. In theory, this is USD supportive. However, the market's focus is on the US trade policy. The ‘trade issue' is weighing on the dollar, but tomorrow's ECB meeting is also in play. We expect the ECB to make only limited changes to its communication (if any) as inflation stays low. However, will a ‘soft‘ ECB be enough to prevent further EUR/USD gains, as the dollar stays under pressure? For now, we assume the ECB to be soft enough for EUR/USD to hold the 1.2155/1.26 trading range. Of course, US political event risk makes the dollar vulnerable short-term.

Yesterday, there was plenty of diplomatic action between EU and UK policy makers at different levels. However, for now, there is no break-through on key pending issues. Especially financial services are a hot topic. This debate will probably continue today as the EU is expected to publish its starting text for the next round of the negotiations. EUR/GBP hovers near 0.8930/50 resistance. Swings in EUR/GBP remain modest, but the day-to-day momentum of sterling is again deteriorating.

EUR/USD rebounds higher in the consolidation range as US trade policy weighs on the dollar.

Gary Cohn Resigns As Trump’s Chief Economic Advisor

Markets are in risk-off mode this morning, as news broke just after the US market close yesterday that Presidents Trump's Chief Economic Advisor, Gary Cohn, resigned after a clash with the president due to the implementation of trade tariffs. Cohn was an advocate of free trade and his resignation will dent market confidence in the administration. This leaves an imbalance in the administration, with an unopposed cadre of officials supporting trade tariffs, which could lead to a trade war developing as protectionist policies take hold. USDJPY sold off to 105.500, S&P500 sold off to 2680.00 and the Dow moved down to 24500.00.

Swiss Consumer Price Index (MoM) (Feb) was 0.4% v an expected 0.2%, from -0.1% previously. Consumer Price Index (YoY) (Feb) was as expected at 0.6%, from 0.7% previously. USDCHF sold off from 0.91425 to a low of 0.93936 following this data release. This data suggests that inflation is picking up on a monthly basis.

US Factory Orders (MoM) (Jan) was -1.4% v an expected -1.3%, from 1.7% previously, which was revised up to 1.8%. EURUSD moved higher from 1.23950 to 1.24090 on the release of this data. The range of the data over the last three years has been between +3% and -3.5%. This release showed a slip in the headline number but the revision last month was raised by the same amount.

Canadian Ivey Purchasing Managers Index s.a.(Feb) data was released and came in at 59.6 with a consensus of 56.3 expected, against a prior reading of 55.2. Ivey Purchasing Managers Index (Feb) was released at 58.4, with a prior reading of 51.3. USDCAD moved lower from 1.29052 to 1.28745. The headline number exceeded expectations, hinting at a strong economy for Canada and was a turnaround compared to the last two months, where the data missed to the downside.

Australian RBA Governor Phillip Lowe delivered a speech titled “The Changing Nature of Investment” at the Australian Finance Review Business Summit, in Sydney. Some of the comments made were: Expect stronger growth in 2018 than in 2017 and a further reduction in unemployment. The Australian economy is moving in the right direction and he expects inflation to increase a little from its current low level. It is likely that the next move in interest rates will be up not down, however, there is no need for a change in policy adjustment. The AUDNZD moved up from 107.243 to 107.372 after the comments. It then declined to 106.887 in the three hours following.

US FOMC Member Brainard is delivered a speech titled “Economic and Monetary Policy Outlook” at New York University's Money Marketeers event. She made the following comments: In relation to Trade wars, she said that there is uncertainty but it is too early to tell and the economic outlook has not changed. She said that material developments in international trade would be taken into account. She also said, in relation to leverage: household leverage remains relatively modest and credit spreads have been very tight, with leverage in the core banking system well contained. On rate hikes: continued gradual Fed rate hikes are likely warranted and global factors were impacting the long end of the yield curve. She said there was greater confidence that inflation will rise to the 2% target. On risks she said that persistently low inflation raises the risk that underlying prices have softened and falling unemployment raises the risk of financial imbalances; it is unclear how much labour slack remains. All in all, her comments were less dovish than usual but show that she is sticking with gradual rate hikes while watching the data for clues.

Australian AIG Performance of Construction Index (Feb) was released at 56.0 with a previous number of 54.3. This data point has remained in expansion above 50 since the March 2017 reading in what is the longest period of growth over the last decade. The peak was reached in August 2017 at 60.6. This shows a strong construction sector in what has been a difficult time of year historically for this data set.

Australian GDP (YoY) (Q4) was 2.4% against 2.5% expected, from 2.8% previously. Gross Domestic Product (QoQ) (Q4) was 0.4% v an expected 0.6%, with a prior 0.6%. AUDUSD moved higher from 0.77715 to 0.78093 as the data missed to the downside, showing a weakness in the Australian economy.

EURUSD is up 0.17% overnight, trading around 1.24246.

USDJPY is down -0.50% in early session trading at around 105.603.

GBPUSD is up 0.11% this morning, trading around 1.38993.

Gold is down -0.10% in early morning trading at around $1,333.58.

WTI is down -0.47% this morning, trading around $61.96.

Major data releases for today:

At 10:00 GMT, Eurozone Gross Domestic Product s.a. (QoQ) (Q4) is expected to be unchanged at 0.6%. Gross Domestic Product s.a. (YoY) (Q4) is expected to be unchanged at 2.7%. This data could see moves in EUR currency crosses. The QoQ number has been holding steady at around 0.6% since 2017, showing stable growth across the Eurozone. The YoY number is also expected to remain on target at 2.7% but any variation in the result could see volatility increase in the markets.

At 13:00 GMT, US FOMS Member Bostic is scheduled to speak about the economic outlook, in Fort Lauderdale. Audience questions are expected and comments may affect the USD currency markets.

At 13:15 GMT, US ADP Employment Change (Feb) is expected to be 195K from 234K previously. USD crosses could be moved by this data. This data point has been holding steady around the 200 mark for much of 2017, with extremes at 300 above and 130 below over the course of the year. The data has remained above 100 since November of 2011, showing that the US jobs market is robust and performing steadily.

At 13:20 GMT, US Fed's William Dudley is due to speak about the economic impact of the 2017 hurricanes, in San Juan. Audience questions are expected and comments may move USD crosses.

At 13:30 GMT, US Trade Balance (Jan) is expected to come in at $-55.1B against a previous $-53.1B. Unit Labor Costs (Q4) is expected to be 2.1% against a prior reading of 2.0%. Nonfarm Productivity (Q4) is expected to be unchanged at -0.1%. The US trade Balance is what much of the current global market uncertainty is based around. While this number is not generally a market mover, it will be watched for a change in trend if new trade policies are implemented. This data is then viewed over a longer period of time, with any one data point largely irrelevant.

At 15:00 GMT, The Bank of Canada Rate Statement will be released, along with the Interest Rate Decision, which is expected to remain unchanged at 1.25%. This could impact CAD crosses, with the Statement examined to pick out key phrases that could hint at future policy direction. This is a major market-moving event for Canada and the Canadian Dollar, with any shift in tone potentially sending the market in a new direction.

At 20:00 GMT, US Consumer Credit Change (Jan) is expected to be $17.90B against a previous $18.45B. USD pairs could see an increase in volatility around the time of this release.

IMF Lagarde: Trade war find losers on both sides

IMF Managing Director Christine Lagarde on trade wars:

- "The macroeconomic impact would be serious, not only if the United States took action, but especially if other countries were to retaliate, notably those who would be most affected, such as Canada, Europe, and Germany in particular."

- "In a so-called trade war, driven by reciprocal increases of import tariffs, nobody wins, one generally finds losers on both sides."

- "There are some countries in the world that do not necessarily respect the World Trade Organization's agreements, and which impose technology transfers. China is a case in point, but it is not the only country with such practices."

BoJ deputy nominee Wakatabe: Policy should be date dependent, not date-driven

BoJ deputy governor nominee Masazumi Wakatabe in upper house confirmation hearing:

- "There are various things the BOJ can do under its yield curve control policy. It can strengthen its existing tool kit, or could come up with a new policy."

- "The BOJ shouldn't be bound by a set timeframe" for meeting the 2% inflation target.

- "Its policy should be data-dependent, not date-driven."

- Planned sales tax hike in fiscal 2019 is the important considering on whether more easing is needed

Another deputy nominee Masayoshi Amamiya said in the same occasion:

- BoJ has ample tools for smooth stimulus exit when time comes.

- But there is still a distant to 2% inflation target.

- BoJ needs to continue with powerful monetary easing patiently

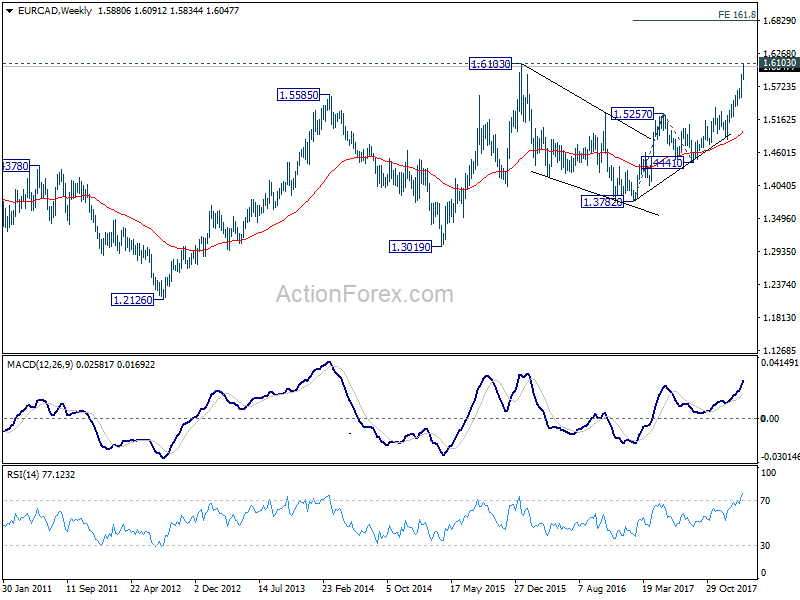

CAD the clear loser this week ahead of BoC

No clear winner this week so far. Yen trades generally higher today. But that's mainly because rebound in Yen crosses lost steam. While Euro is strongest for the week, there is not much follow through buying.

Nonetheless. CAD is the clear loser so far, as the weakest for the week and stays pressured today.

BoC rate decision is a focus later today. Based on uncertainty around NAFTA and Trump's steel and aluminum tariffs, there is practically no chance for another hike today. And, further, there is little chance for BoC to sound anything but cautious.

EUR/CAD is a pair to watch today as it's set to take on 1.6103 key resistance (2016 high). Firm break there will resume long term rebound from 2012 low at 1.2126. Next medium term target will be 161.8% projection of 1.3782 to 1.5257 from 1.4441 at 1.6828.

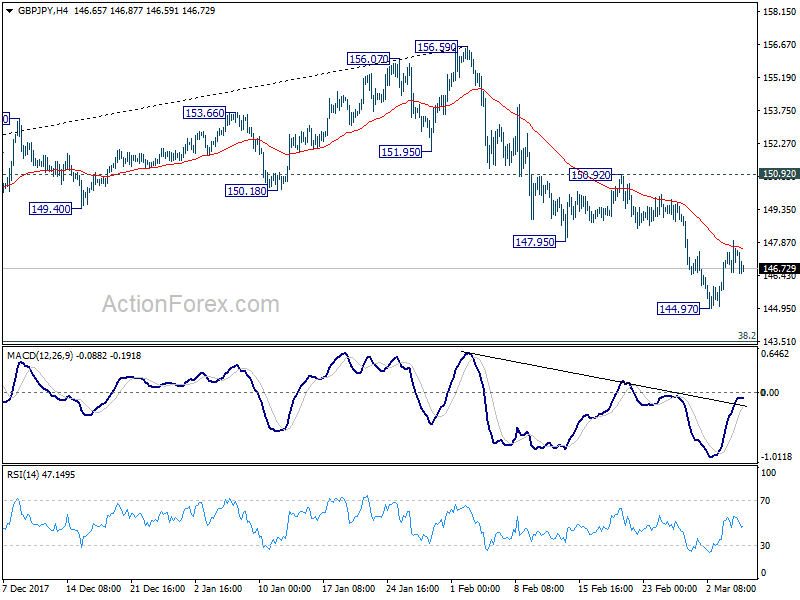

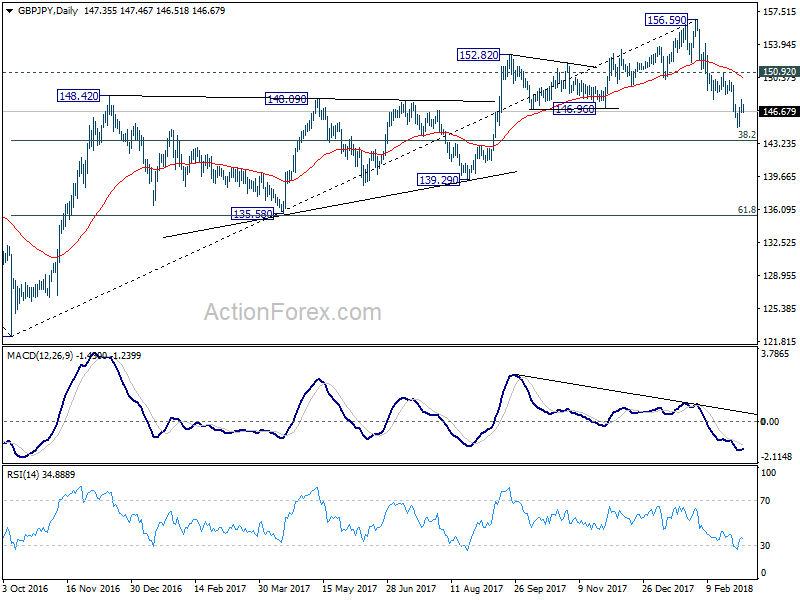

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.61; (P) 147.31; (R1) 148.06; More...

Intraday bias in GBP/JPY remains neutral as recovery from 144.97 temporary low is in progress. While further rise cannot be ruled out, upside should be limited below 150.92 resistance to bring another decline. Break of 144.97 will extend the fall from 156.69 to 143.51 medium term fibonacci level next. We'll look for bottoming signal there. But firm break will target 139.29 support.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

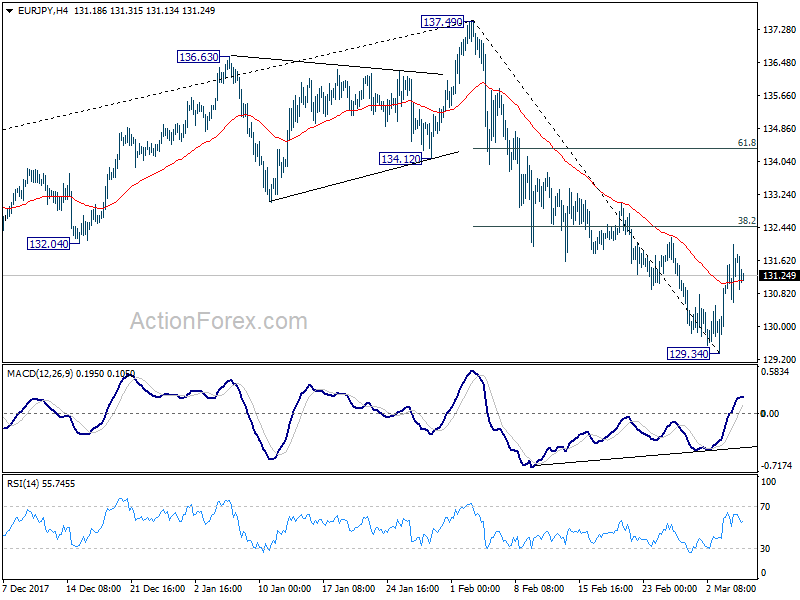

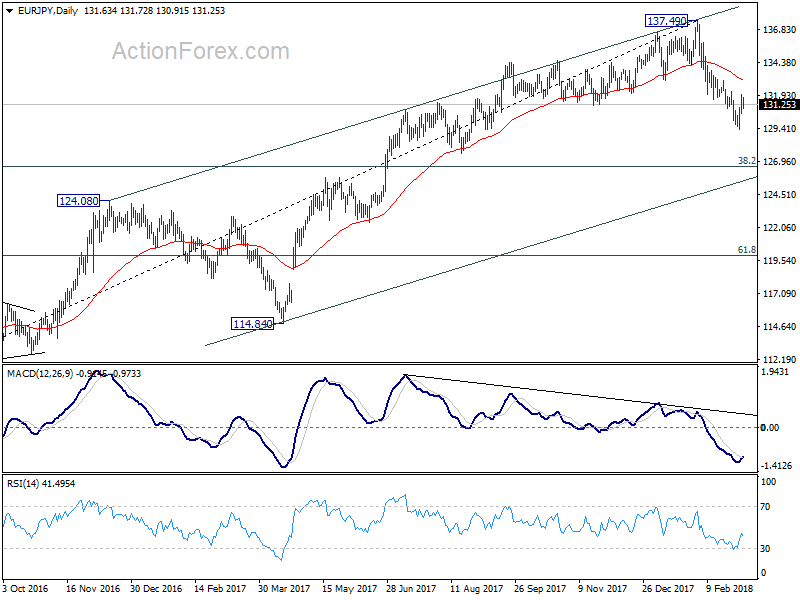

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.82; (P) 131.41; (R1) 132.23; More....

We're favoring the case that a short term bottom is formed at 129.34 already, on bullish convergence condition in 4 hour MACD. Further rise is now expected to 38.2% retracement of 137.49 to 129.34 at 132.45. Break will target 61.8% retracement at 134.37. However, decline 137.49 shouldn't be finished yet. We'd still expect another fall at a later stage. And break of 129.34 will pave the way to 126.61 medium term fibonacci level

In the bigger picture, current development argues that rise from 109.03 has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

Market Update – Asian Session: Equity Markets Generally Decline Amid Resignation Of White House Advisor Cohn

Fed's Brainard suggests greater confidence in reaching inflation target; tailwinds could speed up rate hike pace (Note: Brainard is seen as dovish by some)

Fed's Brainard and Kaplan comment on possible trade impact

AUD/JPY underperforms: Q4 GDP below ests

RBA Gov Lowe reiterates there is no strong case for a near-term policy adjustment; likely that next RBA rate move will be up

China PBoC conducts 1-year MLF facility at unchanged rate; skips daily OMO for third straight session

China Finance Ministry official suggested drafting process has started for property tax bill

Cold weather conditions in the US Northeast in focus: NY's JFK to cancel ~250 flights on Wed

BoJ Dep Gov Nominees continue testimonies

India's government starts to question banks on business man Nirav Modi amid fraudulent transactions scandal.

Australia/New Zealand

ASX 200 opened -0.2%: closed: -1%

ASX 200 Energy Index -1.4%, Financials -1.1%, Utilities -1%

(AU) Australia Q4 GDP Q/Q: 0.4% v 0.5%e (slowest since Q1 2017); Y/Y: 2.4% v 2.5%e

(AU) Australia Treasurer Morrison: Q4 GDP data shows Australia not immune to global influences; Net exports were the main drag on the data

(AU) RBA Gov Lowe: Reiterates there is no strong case for a near-term policy adjustment; likely that next RBA rate move will be up - comments in Sydney

(AU) Australia sells A$500M v A$500M indicated in 4.75% April 2027 bonds, avg yield: 2.7391%, bid to cover: 3.85x

(AU) Australia PM Turnbull: Election to be held in H1 of 2019

(NZ) NEW ZEALAND Q4 VOLUME OF ALL BUILDINGS Q/Q: 1.4% V 1.0%E

China/Hong Kong

Shanghai opened flat, Hang Seng -0.6%

Hang Seng Materials Index -2%, Energy -1.7%, Info Tech -0.9%, Financials -0.7%, Property/Construction -0.6%

Shanghai Composite Property Sub-declines less than 1%

(CN) PBOC CONDUCTS 1-YEAR CNY105.5B MEDIUM-TERM LENDING FACILITY (MLF) OPERATION: Interest rate unchanged at 3.25%

(CN) China PBoC Open Market Operation (OMO): Skips OMO for third straight session

(CN) China Vice Finance Min: NPC and other departments are drafting the property tax bill; Will reasonably design property tax system

(CN) China Feb New Loans may decline m/m to less than CNY1T compared to Jan record level of CNY2.90T (in-line with analyst views) - China Securities Journal

(CN) China End 2017 Outstanding Government Debt CNY29.95T; Debt-to-GDP ratio 36.2% v 36.7% y/y – MOF

(CN) China announces new rules related to equity stakes in insurers, to take effect on April 10th

(CN) China: To release surveyed jobless rate data monthly from April

Looking Ahead: Looking Ahead: China FX reserves expected to be released during European session

Japan

Nikkei 225 opened -0.7%; closed -0.8%

TOPIX Iron & Steel Index -2.2%, Electric Appliances -1.1%

(JP) BoJ Dep Gov Nominee Wakatabe: Won't automatically propose more easing, but does not exclude proposing extra easing

(JP) BoJ Dep Gov Nominee Amamiya ('Mr BoJ'): Reiterates Japan economy making progress toward CPI goal

(JP) Japan Feb Official Reserve Assets: $1.26T v $1.27T prior

(JP) Ripple said to develop blockchain payment app with banks in Japan - US financial press

Looking Ahead: Looking Ahead: Japan Q4 GDP revision due for release on Thursday

Korea

Kospi opened +0.1%

Samsung Electronics rises over 2%

(KR) North Korea said to be open to denuclearize if regime safety is guaranteed and not use any weapons against South Korea – financial press

(KR) South Korea said to closely monitor for possible rise in FX volatility - South Korea Press

(KR) South Korea parliament to hold hearing on Bank of Korea (BoK) Gov Lee on Wed, March 21st - South Korean Press

(KR) US imposes new sanctions on North Korea in relation to the assassination of Kim Jong Nam; Kim Jong Nam was the half brother of North Korea Leader Kim Jong Un. - FT

Other Asia

(TW) Taiwan's Advanced Semiconductor Engineering [2311.TW] said to receive orders from Bitmain, says a Taiwanese press report

North America

US equity markets closed mostly higher: Dow flat, S&P500 +0.3%, Nasdaq +0.6%, Russell 2000 +1%

S&P500 Materials +1.1%; Utilities -1.3%

(US) White House economic adviser Gary Cohn to resign; Expected to leave in next few weeks - NYT

( US) Andrew Puzder said to be considered as replacement for Cohn, says US financial press; Separate report suggests Adviser Peter Navarro and Larry Kudlow are said to be the top two candidates to replace Cohn

(US) President Trump said that he will be making a decision soon on the appointment of a new Chief Economic Advisor, says 'many' people want the job.

(US) Fed Brainard (voter): Has greater confidence Fed to achieve 2% inflation target; tailwinds could speed up pace of rate hikes

(US) Fed's Kaplan (non-voter, dove): Trade discussion has not changed my outlook; Reiterates expects Fed to hike three times this year and should get started soon

(US) House Speaker Ryan: Section 232 protocol is a little broad; urges administration to make potential tariffs narrower

(US) Senate Maj Leader McConnell (R-KY): there is a lot of concern among GOP Senate caucus that steel/aluminum tariffs could spark trade war

(US) OPEC Sec Gen Barkindo: supply is good but demand is even more robust - CNBC interview

(US) Weekly API Oil Inventories: Crude: +5.7M v 0.9M prior

Looking ahead: US Feb ADP Nonfarm Employment change expected to be released, along with the Bank of Canada (BoC) interest rate decision and weekly US DOE Crude Oil Inventories

Europe

(UK) EU internal report argues that UK PM May is 'double cherry-picking' on Brexit and calls her model unworkable; Report dismissed May's Brexit speech as "being more about Conservative Party management than putting forward sensible solutions on trade" - UK press

Telecom Italia [TIT.IT]: Reports Q4 Rev €5.1B v €5.1B y/y

Looking Ahead: UK Annual Budget expected to be released

Levels as of 01:00ET

Hang Seng -0.9%; Shanghai Composite -0.2%; Kospi -0.2%

Equity Futures: S&P500 -1.3%; Nasdaq100 -1.2%, Dax-1.1 %; FTSE100 -0.8%

EUR 1.2402-1.2430 ; JPY 105.45-106.23; AUD 0.7771-0.7831 ;NZD 0.7275-0.7302

Feb Gold flat at $1,334/oz; Feb Crude Oil -0.8% at $62.09/brl; Mar Copper -0.4% at 3.145$/lb

EUR/USD Is Now Trading At 1.2420

Market movers today

Focus remains on US trade policy and Italian politics while the market awaits the ECB meeting tomorrow and the US employment report on Friday. Today, US ADP employment for February is up for release. It is expected to rise 200k after an increase of 234k in January. However, it is not a very good indicator for the non-farm payrolls. Also, the most watched component of the employment report on Friday will be wage growth after the upward surprise last month.

US trade balance is also due out today. In December, the trade deficit increased to the highest level in nine years adding insult to injury to the issue of US trade imbalances. We have dived in to US trade policy, what Trump's focus on protectionism me an s for the economy and markets and what to expect from here in this piece released this morning: Research US: Symbolic protectionism with limited impact on growth and inflation but risks.

At the Bank of Canada meeting today, rates are expected to stay unchanged at 1.25%.

The Swedish Debt Office is releasing the budget balance for February, see next page.

Selected market news

Markets continue to focus on US trade policy after Trump's e conomic advisor, Gary Cohn, announced late last night that he has resigned. The reason is the ongoing discussions on trade policy where he strongly disagrees with Trump, as he sees the proposed tariffs as being unfriendly to business. Gary Cohn 's resignation means it is more likely that we will see a formal decision to impose tariffs on steel and aluminium next week.

In addition, Bloomberg wrote a story that the next step for the Trump administration is targeting China by imposing tariffs on Chinese imports and limiting Chinese investments in US businesses. It is not a surprise Trump wants to target China, as the US runs the largest trade deficit with China and the investigat ion of Chinese theft of intellectual property rights have been ongoing since August 2017. St ill, it is noteworthy that the story is being more concrete than what we have seen before. For instance, in the most severe scenario, the US could impose tariffs on imports of Chinese-produced clothing and electronics, according to the story. On the investment side, the US may prohibit Chinese takeovers in sectors, where US companies cannot access the Chinese market . The investigation on China is expected in the coming weeks. As with tariffs on steel and aluminium, we expect any measures taken against China to be small in magnitude, meaning this is more about politics than economics. There is a risk we are being too optimistic and that we are heading for a full -blown global trade war.

More protectionist US is bad for global risk sentiment and the Asian markets are flashing red. The bad mood came after a positive day for risk yesterday with the stories that North Korea is willing to discuss disarmament and that the Republican establishment is pushing back on the protectionist agenda. S&P500 futures are trading 1.1% lower and yields on US 10-year Treasuries have fallen 4bp. More interestingly, we have also seen a small weakening of the USD and EUR/USD is now trading at 1.2420.

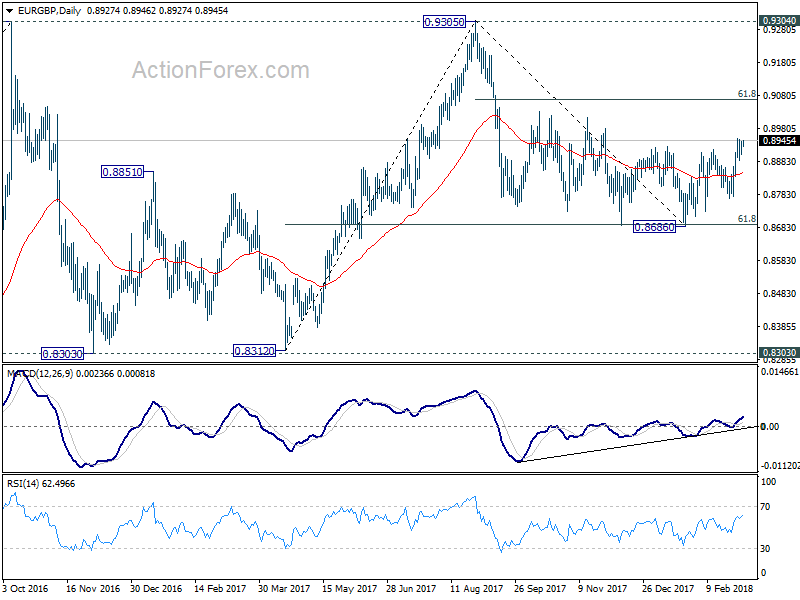

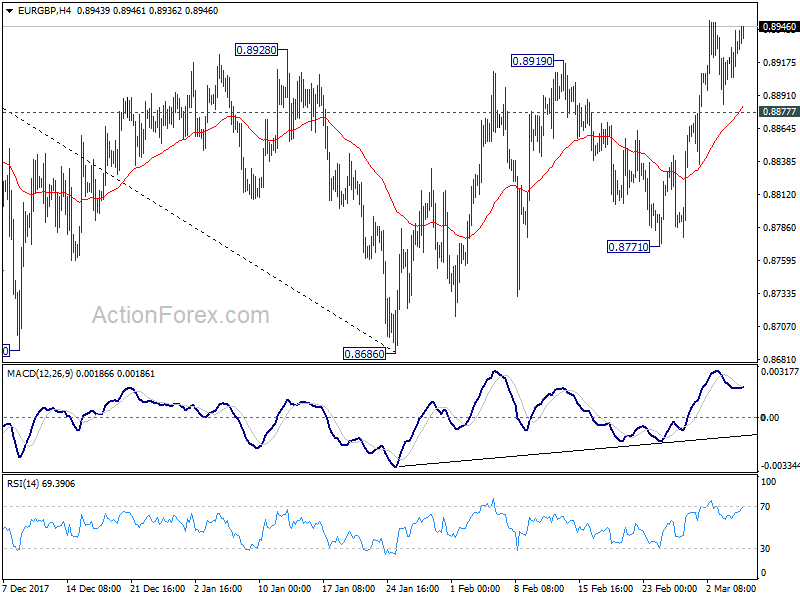

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8908; (P) 0.8926; (R1) 0.8948; More...

With 0.8877 minor support intact, further is expected in EUR/GBP/ Prior break of 0.8928 resistance indicates near term trend reversal. Decline from 0.9305 has completed at 0.8686 after hitting 61.8% retracement of 0.8312 to 0.9305. Further rise should be seen back to 61.8% retracement of 0.9305 to 0.8686 at 0.9069. Firm break there will target retest of 0.9305 high. On the downside, below 0.8877 minor support will dampen this bullish view and target 0.8771 support instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.