Sample Category Title

Trump Strikes Again With Steep Tariffs, Stocks Crumble

A negative vibe lingered across financial markets on Friday, after Donald Trump's vow to impose severe tariffs on imports of steel and aluminium sparked fears of a global trade war.

In a move that dealt a blow to global sentiment, Trump said on Thursday that the United States would set tariffs of 25% on steel imports and 10% on aluminium. This bombshell development is likely to fuel concerns of retaliatory actions from major US trade partners consequently weighing on risk appetite. Investors are clearly jittery by the threat of a potential global trade war and its possible effect on stock markets.

Asian equities were under intense selling pressure during early trading on Friday, following Wall Street's painful declines overnight. In Europe shares ventured lower, as investors maintained a safe distance from riskier assets. The negative sentiment from Asian and European markets could find its way back into Wall Street this afternoon.

Dollar slips on Trump's tariff hikes

The Dollar sharply depreciated against a basket of major currencies on Thursday evening after Trump's tariff announcement sparked market jitters. Federal Reserve Chairman Powell's softer tone during his second day of testimony also played a role in the Greenback's decline - with the Dollar Index trading around 90.20 as of writing. While heightened worries of a trade war could pressure the Dollar, speculation over higher US interest rates has the ability to cushion the downside. Focusing on the technical picture, the Dollar Index is at threat of extending losses if bears are able to conquer the 90.00 level.

Sterling turns to Theresa May for direction

This is certainly shaping up to be a painful trading week for the British Pound, thanks to renewed jitters over Brexit negotiations. The fresh dispute over Northern Ireland's border has effectively eroded market optimism over a “soft Brexit” outcome, consequently weighing heavily on the Pound.

Theresa May will be in the spotlight today as she delivers a speech about Britain's future relationship with the European Union after Brexit. Markets will be closely scrutinizing May's remarks for any fresh clues on how the UK plans to address the EU's Irish border proposal. Sterling could turn volatile today, especially when considering how the currency remains highly reactive to Brexit developments.

Taking a look at the technical picture, the GBPUSD remains bearish below 1.3850. Sustained weakness below this level could invite a decline back towards 1.3750 and 1.3700, respectively.

Commodity spotlight – Gold

Gold staged a sharp rebound on Thursday evening after Trump's tariff plan sparked risk aversion and weakened the Dollar.

While the yellow metal could venture higher in the near term amid the skittish market sentiment, losses are likely to be limited by US rate hike expectations. It must be kept in mind that Gold is a zero-yielding asset which will feel the burn in a high interest rate environment. From a technical standpoint, prices remain under pressure below $1324.15. A failure for bulls to break above this level could result in a decline back towards $1310 and $1300, respectively. Alternatively, a breakout above $1324.15 may pave a way higher back to $1340.

Technical Outlook: SPOT GOLD Bounces On Fresh Risk Aversion

Spot Gold stands at the front foot on Friday after bouncing from two-month low at $1303 on Thursday, as news about US tariffs on imported metals caused turmoil in the markets and prompted investors into safer assets.

Fresh recovery attempts sideline downside risk which was built on strong fall in previous sessions and signal gold price could climb higher in new risk aversion environment.

Reversal signal is developing after Thursday’s long-tailed Doji which was the second consecutive Doji candle and signaling strong indecision.

Recovery probes through initial barrier at $1322 (Wednesday’s high), for test of daily Tenkan-sen ($1325) but needs to emerge above daily cloud (cloud top lies at $1329) to confirm reversal and expose next pivotal barrier at $1340 (26 Feb lower top/near Fibo 61.8% of $1361/$1303 bear-leg).

Broken 55 SMA now acts as support ($1318) and should keep the downside protected.

Res: 1325, 1329, 1332, 1340

Sup: 1318, 1315, 1313, 1307

Markets Rattled By Protectionist Trump

- Trump's Tariffs Weigh on Global Stock Markets;

- May Speech in Focus as EU Pushes For Progress in Talks;

- Italian Election and German Coalition Vote Eyed Over the Weekend.

Trump's Tariffs Weigh on Global Stock Markets

US President Donald Trump's protectionist trade measures announced on Thursday is the latest thing to take its toll on stock markets, with indices in Europe heavily in the red and US futures pointing to another tough session on Wall Street.

Trump has long been accused of prioritising protectionist populist measures over those that will benefit both domestic and global growth, something he has repeatedly dismissed, claiming the measures being considered were aimed at making trade fair and reciprocal. He may be able to persuade his core voter base of that but investors are far from convinced, as was evident by the market reaction to the announcement.

This move isn't only bad for steel and aluminium producers, protectionist measures such as tariffs are bad for everyone who's costs have now increased, which impacts companies and end consumers. And these measures are unlikely to be a unique case, other countries will now consider counter-measures against the US which won't necessarily target this particular sector.

The announcement has also come at a time when investors sentiment is already fragile, with markets having been rocked by the prospect of more aggressive monetary tightening, which Trump is already partially responsible for after passing the tax reform measures late last year. For someone so obsessed with stock market performance, he's taking a big gamble with these tariff's, the benefits of which are questionable.

May Speech in Focus as EU Pushes For Progress in Talks

The timing of Trump's tariffs could work in the favour of the UK as it pushes the EU for a free trade deal that promotes cooperation and brings down protectionist barriers. Theresa May's speech today will be monitored closely as she seeks to pick up the pace of negotiations and bridge the gap between the two sides.

As ever, I'm sceptical that the speech will contain anything of substance having heard numerous speeches over the last 18 months and given the tough position May finds herself in, shackled by Brexiteers on her cabinet and with only a slim working majority in parliament. Another Florence speech moment is what people are hoping for today but I'm neither convinced by the potential for it or that it was as significant as was made out.

Italian Election and German Coalition Vote Eyed Over the Weekend

Finally, European investors will have an eye on Italy and Germany ahead of a massive weekend for both countries. The election in Italy on Sunday is likely to result in a hung parliament and months of coalition talks while Germans will be hoping they're at the end of that process with the SPD voting on whether to go into coalition again with Angela Merkels centre right block.

CRUDE OIL Trading Lower

Crude oil upward trend vanished, currently trading below 60.75 and approaching hourly support at 59.72 (15/02/2018 low). Hourly resistance at 64.77 (11/01/2018 high) remains. The technical structure suggests short-term downward moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

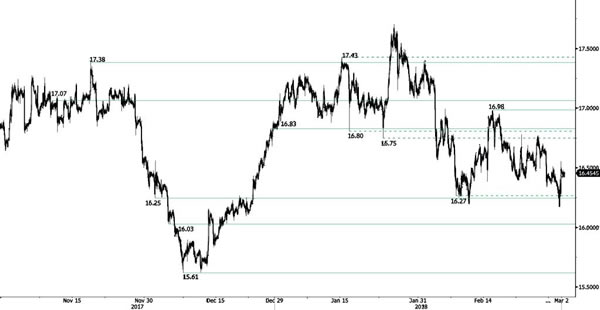

SILVER Declining

Silver bounced back after breaking hourly support at 16.27 (07/02/2018 low). Silver bearish pattern is maintained, heading for further decline along hourly support at 16.25 (12/01/2018 low). The short-term technical structure suggests further decline.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Stabilized At The 1317 Range

Gold recovers back from its recent descent below hourly support at 1306 (04/01/2018). The pair is stabilized at the 1317 range and is ready to trade sideways. Hourly support and resistance are given at 1351 (01/02/2018 high) and 1300 (29/12/2017 low).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

Market Update – European Session: Protectionism Weighs On Risk Appetite, Key Political Events In Europe This Weekend

Notes/Observations

Protectionism concerns weigh on markets

BOJ Gov Kuroda mentions the possibility of policy exit for the 1st time in his tenure

Busy political weekend for Europe (result of the SPD vote on whether to enter a coalition with Merkel’s CDU and Italian election)

Federal Offices closed in Washington DC on Friday due to high winds

Asia:

Japan Jan Jobless Rate at lowest level since 1993 (2.4% v 2.8%e) while job availability highest since 1974

Japan Feb Tokyo CPI data registers its highest level since March 2015 with headline at 1.4% and core at 0.9%

BOJ Gov Kuroda stated during his reappointment hearing in Parliament that would be considering an exit in its loose monetary around Fiscal 2019/20 because of the chances of hitting inflation target at that time (**Note: 1st time ever BOJ has mention any potential timing of exit)

Europe:

ECB unlikely to signal any policy changes at March 8th meeting, but might discuss dropping easing bias language. General Council wants plenty of evidence that inflation will rise, fearing damage to its credibility if moved too early and had to reverse course.

Likelihood that ECB's Weidmann would replace Draghi said to be increasing; His candidacy gaining support as Germany agreed to support Spain's De Guindos as next ECB Vice President

PM May said to warn that warns the EU that relations will "break down" unless it respects the wishes of the British people. Will set out 'five tests' for a successful Brexit. Brexit result was a decision to "take back control of our borders, laws and money"

EU's Juncker: EU will "react firmly" to Trump administration tariffs; will bring forward countermeasures. To put forward a proposal for WTO-compatible countermeasures against the United States in the next few days to rebalance the situation

Spanish regional official Puigdemont confirmed he had withdrawn his candidacy for leader of Catalonia; to support Sanchez as a Presidential candidate

Americas:

President Trump: US will institute tariffs during week of March 5th; will impose 25% tariffs on steel and 10% on aluminum imports; details to be released next week

White House Economic Advisor Cohn said to be again rumored to be on the brink of leaving the White House

PIMCO economist Rich Clarida likely front runner for Fed deputy role

Economic Data:

(DE) Germany Jan Retail Sales M/M: -0.7% v +0.7%e; Y/Y: 2.3% v 3.0%e

(DE) Germany Jan Import Price Index M/M: 0.5% v 0.4%e; Y/Y: 0.7% v 0.7%e

(DK) Denmark Jan Gross Unemployment Rate: 4.1% v 4.2%e, Unemployment Rate (seasonally adj): 3.3% v 3.3% prior

(CN) Weekly Shanghai copper inventories (SHFE): 260.3K v 218.5K tons prior

(TH) Thailand Feb Business Sentiment Index: 51.4 v 52.2 prior

(ES) Spain Feb Net Unemployment M/M: -6.3K v -6.0Ke

(CZ) Czech Q4 Preliminary GDP (2nd reading) Q/Q: 0.5% v 0.5%e; Y/Y: 5.2% v 5.1%e

(BR) Brazil Feb FIPE CPI (Sao Paulo) M/M: -0.4% v -0.2%e

(HK) Hong Kong Jan Retail Sales Value Y/Y: 4.1% v 5.2%e; Retail Sales Volume Y/Y: 2.2% v 4.1%e

(NO) Norway Feb Unemployment Rate: 2.5% v 2.5%e

(IT) Italy Q4 Final GDP Q/Q: 0.3% v 0.3%e; Y/Y: 1.6% v 1.6%e

(BR) Brazil Jan Total Formal Job Creation: +77.8K v +58.0Ke

(UK) Feb Construction PMI: 51.4 v 50.5e (5th month of expansion)

(EU) Euro Zone Jan PPI M/M: 0.4% v 0.4%e; Y/Y: 1.5% v 1.6%e

Fixed Income Issuance:

(ZA) South Africa sold total ZAR430M vs. ZAR900M indicated in I/L 2029, 2033 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -1.3% at 370.0, FTSE -0.7% at 7124, DAX -2.0% at 11952, CAC-40 -1.6% at 5176 , IBEX-35 -1.2% at 9620, FTSE MIB -1.9% at 22026 , SMI -1.1% at 8698, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes: European Indices continues to trade lower across the board with the Dax dropping below 12K as possible ramifications over proposed US Steel and Aluminium tariffs weigh on markets. Asian markets were hit with notable declines in Steel names, with ArcelorMittal, Thysenkrupp some of the European names under pressure. In the earnings space, LafargeHolcim, LSE, Beterbed trade lower, while Mondi, Promimus, Eleka trade higher. Technicolor trades sharply lower in France after divesting its patent licensing business, Plus500 falls after a share placement, while Verona Pharma trades sharply higher after favorable trial data. Looking ahead notable earners include Footlocker, JC Penney and JD.com.

Movers

Consumer Discretionary [Asos [ASC.UK] -1.2% (CFO to step down), Technicolor [TCH.FR] -12% (Divests unit)]

Materials [ArcelorMittal [MT.NL] -3.5% (JV bid for Essar Steel India, US Steel Tariffs), LafargeHolcim [LHN.CJ] -4.3% (Earnings)]

Industrials [ Thyssenkrupp [TKA.DE] -2.7% Salzgitter [SZG.DE] -4.3% (US Steel Tariffs), Mondi [MNDI.UK] +1.3% (Earnings)]

Financial [LSE [LSE.UK] -2.0% (Earnings), Plus500 [PLUS.UK] -5% (Placement) ]

Healthcare [Verona Pharma [VRP.UK] +19% (Positive trial update), Shire [SHP.UK] +2.7% (Takeover chat)]

Energy [Electromagnectic Geoservices [EMGS.NO] -29% (Earnings)]

Speakers

EU Commission: Greece has completed the measures for the 3rd bailout review, ESM-backed bailout program was on track and paved the way for the next disbursement

BOE Gov Carney: Need for better regulation of cryptocurrencies; isolating crypto assets might not be the best option

EU's Dombrovskis: Momentum in the global economy remained strong

Germany BDI Industry Association: Trump risks protectionist spiral with steel tariffs; risks a global trade war

German Association of Chambers of Trade and Industry (DIHK): Risks that tariffs will cost businesses millions

Currencies

The USD lost some ground over the past 24 hours as protectionism concerns weigh on sentiment. Dealers noted that Steel tariffs introduced by the Bush administration in 2002 did coincide with broad USD weakness around the time of the announcement

USD/JPY fell below the 106 level during that latter part of the Asian session after BOJ Gov Kuroda stated during his reappointment hearing in Parliament that would be considering an exit from its loose monetary around Fiscal 2019/20 because of the chances of hitting inflation target at that time (**Note: 1st time ever BOJ has mention any potential timing of exit)

Busy political weekend for Europe with the looming result of the SPD party vote on whether to enter a coalition with Merkel’s CDU and Italian election. Dealers noted that if SPD rejected the coalition proposal the EUR/USD could bust below the current 1.21 support and probe a few big figures lower. On the Italian election front analysts believe the risk of a hung parliament outcome remained high but the centre-right coalition had been closing the gap. The risk of a second election should not be underestimated. get an outright majority. Pair steady in today’s session at 1.2275 area.

GBP/USD was steady at 1.3780 area ahead of PM May’s Bexit speech. Press reports noted that May would warns the EU that relations would "break down" unless it respected the wishes of the British people

Fixed Income

Bund Futures trades flat at 160.04 as political risks are set to dominate the weekend headlines. Upside targets 160.25, while a return lower targets the157.75 level.

Gilt futures trade at 122.85 up 30 ticks as Gilts continue to attempt to push higher. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.879T from €1.860T prior. Use of the marginal lending facility rose to €112M from €90M prior.

Corporate issuance saw equity fund inflows of $13.3B in w/e Feb 28th vs inflows of $1.1B in w/e Feb 21st

Looking Ahead

(MX) Mexico Jan YTD Budget Balance (MXN): No est v -238.5B prior

(UK) PM May to give Brexit speech on future relationship with EU

06:00 (PT) Portugal Jan Industrial Production M/M: No est v -0.4% prior; Y/Y: No est v 1.3% prior

06:00 (PT) Portugal Jan Retail Sales M/M: No est v 0.3% prior; Y/Y: No est v 5.7% prior

06:00 (UK) DMO to sell combined £6.0B in 1-month, 3-month and 6-month Bills (£2.0B, £2.0B and £2.0B respectively)

06:30 (IN) India Weekly Forex Reserves

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Jan PPI Manufacturing M/M: No est v 0.3% prior; Y/Y: No est v 3.9% prior

07:00 (CL) Chile Jan Retail Sales Y/Y: 5.0%e v 4.8% prior, Commercial Activity Y/Y: No est v 3.1% prior

08:00 (SG) Singapore Feb Purchasing Managers Index (PMI): 53.1e v 53.1 prior, Electronics Sector Index: No est v 52.9 prior

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Dec GDP M/M: 0.1%e v 0.4% prior; Y/Y: 3.3%e v 3.5% prior, Quarterly GDP Annualized: 2.0%e v 1.7% prior

09:00 (MX) Mexico Jan Leading Indicators M/M: No est v 0.08 prior

10:00 (US) Feb Final University of Michigan Confidence: 99.5e v 99.9 prelim

10:00 (DK) Denmark Feb Foreign Reserves (DKK): No est v 463.9B prior

10:00 (CO) Colombia Jan Exports: $3.4Be v $3.95B prior

11:00 (IS) Iceland Q4 Current Account (ISK): No est v 68.0B prior

11:00 (EU) Potential Sovereign ratings after European close

(RO) Romania Sovereign Debt to be rated by S&P

(SE) Sweden Sovereign Debt to be rated by S&P

(RO) Romania Sovereign Debt to Be Rated by Moody's

(SE) Sweden Sovereign Debt to Be Rated by Moody's

13:00 (US) Weekly Baker Hughes Rig Count data

Weekend Sun

(CH) Switzerland votes on Popular Initiatives

(DE) German SPD announces result of member vote on Coalition Pact

(IT) Italy holds elections

BITCOIN Pausing

Bitcoin is stabilized at the 10900 range, following recent decline below 9390. Hourly support and resistance remain at 9022 (30/11/2018 low) and 12130 (18/01/2018 high). The short-term technical structure suggests further consolidation moves.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading above its 200 DMA (6'500 range).

EUR/CHF Weakening

EUR/CHF is currently trading above the 1.15 range and presents a bearish bias. The pair is approaching hourly support at 1.1471 (09/02/2018 low) while hourly resistance at 1.162 (07/02/2018 high) remains. The technical structure suggests short-term downward moves.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support can be found at 1.0234 (20/04/2015 low).

EUR/GBP Rising Further

EUR/GBP is trading higher, approaching hourly resistance at 0.8929 (12/01/2018 high). Hourly support at 0.8756 (04/12/2017 low) is distanced. The technical structure suggests short-term upside moves.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA.