Sample Category Title

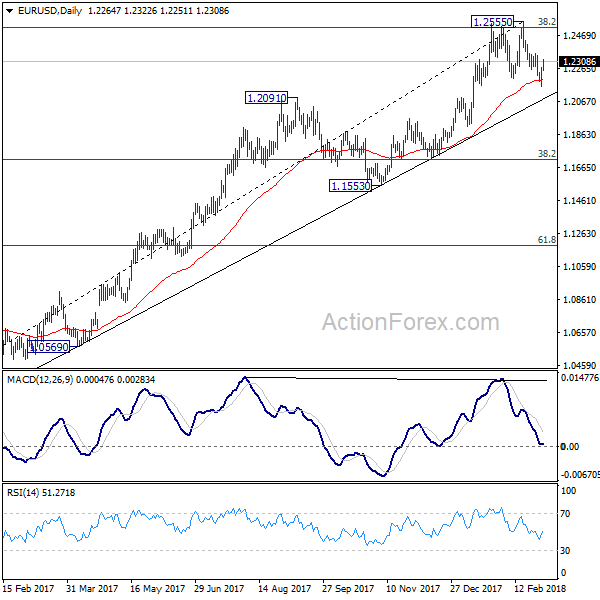

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2207 (R1) 1.2227; More....

EUR/USD's rebound from 1.2154 but stays below 1.2354 minor resistance. Intraday bias remains neutral first. On the upside, break of 1.2354 will indicate that pull back from 1.2555 has completed. In such case, intraday bias will be turned back to the upside for 1.2555 high. Break there will carry larger bullish implication. On the downside, break of 1.2154 will revive the case of trend reversal and turn outlook bearish for 38.2% retracement of 1.0339 to 1.2555 at 1.1708.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.5553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

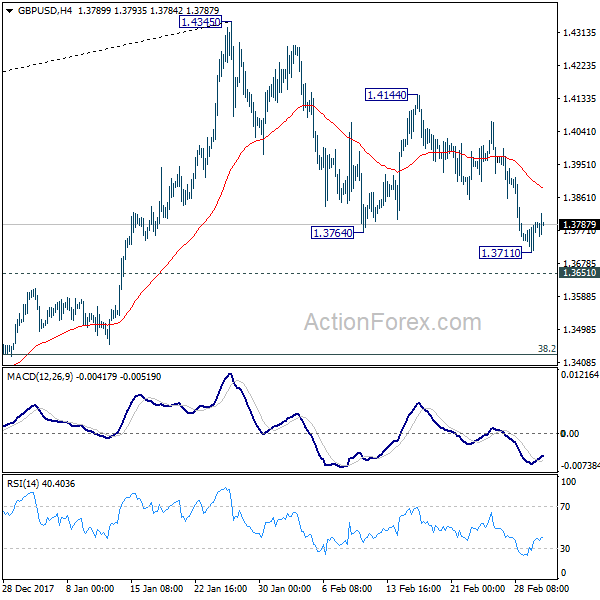

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3729; (P) 1.3756; (R1) 1.3802; More....

Intraday bias in GBP/USD remains neutral at this point. Further fall is still expected as long as 1.4144 resistance holds. Below 1.3711 will target 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

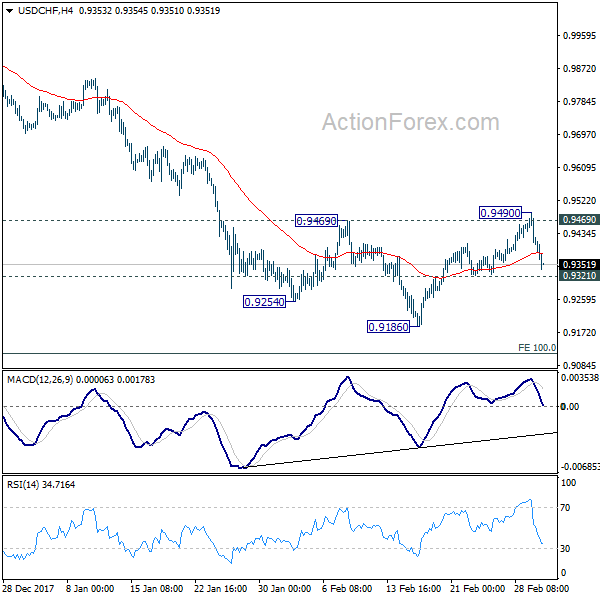

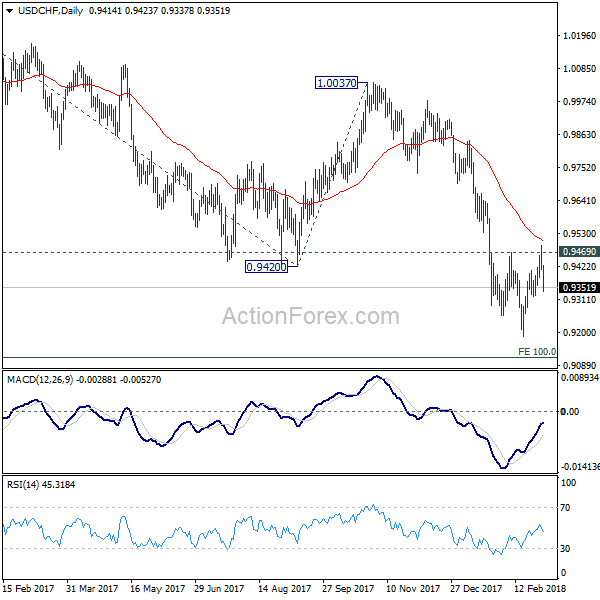

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9388; (P) 0.9439; (R1) 0.9468; More...

USD/CHF's fall from 0.9490 continues but it's staying above 0.9321 minor support. Intraday bias remains neutral first. Rejection from 0.9469 resistance retained near term bearishness. Below 0.9321 will target a test on 0.9186 low. Break will resume larger down trend to 0.9115 medium term projection level next. On the upside, break of 0.9490 should indicate near term trend reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

Global Markets Tumble Further as Trump Declares Trade Wars are Good, Dollar Pressured

Risk aversion continues to be the main theme today as US President Donald Trump declared that trade wars are good. At the time of writing, German DAX is trading down -2.2%, French CAC down -1.9% and UK FTSE down -1.1%. That follows -2.5% decline in Japanese Nikkei. US futures are pointing to triple digit decline in DOW at open. In the currency markets, Dollar is suffering steep selling against Euro, Yen and Swiss Franc. Nonetheless, commodity currencies are even weaker with Canadian Dollar leading the way down.

Dollar suffers again as Trump said trade wars are good

Fresh selling is seen in Dollar after latest tweet by Trump. He said in early morning that "when a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win." This is a follow up to the news that Trump is going to impose tariffs of 25% on steel and 10% on aluminum. And he plans to announce that formally next week.

It should be noted again that accord to data of IHS Global Trade Atlas, in 2017, Canada was the top supplier of steel to the US, with 16% share. It's followed by Brazil (13%), South Korea (10%), Mexico (9%), Russia (9%), Turkey (7%), Japan (5%), Taiwan (4%), Germany (3%) and India (2%). China is outside of top 10 at 11.

EU to react firmly against Trump's trade war

Response from EU regarding the planned tariff was firm. In a statement, "President of the European Commission, Jean-Claude Juncker said: "We strongly regret this step, which appears to represent a blatant intervention to protect US domestic industry and not to be based on any national security justification." And, "We will not sit idly while our industry is hit with unfair measures that put thousands of European jobs at risk." Juncker pledged "The EU will react firmly and commensurately to defend our interests. The Commission will bring forward in the next few days a proposal for WTO-compatible countermeasures against the US to rebalance the situation."

Data from European steel association Eurofer showed that Turkey was the bloc's biggest steel customer in 2017, with 20% share. The US was just the second with 15% share. Also, that's only around 2% of EU's total steel production.

Canadian Foreign Minister Chrystia Freeland said the country buys more than half of American steel. And the results in a USD 2b surplus for the US. She criticized that it's "entirely inappropriate" for the US to consider Canada a national security threat. Freeland pledged that "we will always stand up for Canadian workers and Canadian businesses." And she warned that "should restrictions be imposed on Canadian steel and aluminum products, Canada will take responsive measures to defend its trade interests and workers."

In China, Foreign Ministry spokeswoman Hua Chunying sounded pedestrian. She warned that "in recent years, the global economy has still recovered slowly and the basis for the global recovery is is still unstable." And she urged all countries to "make concerted efforts to to cooperate to resolve the relevant issues, instead of taking trade restrictive measures unilaterally."

UK PM May to deliver Brexit speech at Mansion House

The markets are awaiting Prime Minister Theresa May's high profile speech regarding post Brexit UK-EU relationship. The speech will take place at Mansion House in London at 1:30pm local time. Accord to the extracts by her office, May would seek "broadest and deepest possible agreement - covering more sectors and co-operating more fully than any Free Trade Agreement anywhere in the world today." And, "rather than having to bring two different systems closer together, the task will be to manage the relationship once we are two separate legal systems."

May is expected to set out five "tests" for the deal with EU. They are:

- That any deal must respect the referendum result

- That any deal must not break down

- That any deal must protect jobs and security

- That any deal must be "consistent with the kind of country we want to be" - modern, outward-looking and tolerant

- That any agreement must bring the country together

On the data front

Canada GDP grew 0.1% mom in December, in line with consensus. Eurozone PPI rose 0.4% mom, 1.5% yoy in January. German import price index rose 0.5% mom in January, retail sales dropped -0.7% mom. UK construction PMI rose to 51.4 in February. New Zealand building permits rose 0.2% mom in January. Japan unemployment rate dropped sharply to 2.4% in January, monetary base rose 9.4% yoy in February, Tokyo CPI rose to 0.9% yoy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.85; (P) 106.53; (R1) 106.90; More...

USD/JPY's medium term decline from 118.65 resumed by breaking 105.54 and reaches as low as 105.24 so far. Intraday bias remains on the downside for 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Jan | 0.20% | -9.60% | -9.50% | |

| 23:30 | JPY | Jobless Rate Jan | 2.40% | 2.80% | 2.80% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 0.90% | 0.80% | 0.70% | |

| 23:50 | JPY | Monetary Base Y/Y Feb | 9.40% | 9.20% | 9.70% | |

| 07:00 | EUR | German Retail Sales M/M Jan | -0.70% | 0.70% | -1.90% | -1.10% |

| 07:00 | EUR | German Import Price Index M/M Jan | 0.50% | 0.40% | 0.30% | |

| 09:30 | GBP | Construction PMI Feb | 51.4 | 50.5 | 50.2 | |

| 10:00 | EUR | Eurozone PPI M/M Jan | 0.40% | 0.40% | 0.20% | |

| 10:00 | EUR | Eurozone PPI Y/Y Jan | 1.50% | 1.60% | 2.20% | |

| 13:30 | CAD | GDP M/M Dec | 0.10% | 0.10% | 0.40% | |

| 15:00 | USD | U. of Mich. Sentiment Feb F | 99.5 | 99.9 |

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.85; (P) 106.53; (R1) 106.90; More...

USD/JPY's medium term decline from 118.65 resumed by breaking 105.54 and reaches as low as 105.24 so far. Intraday bias remains on the downside for 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

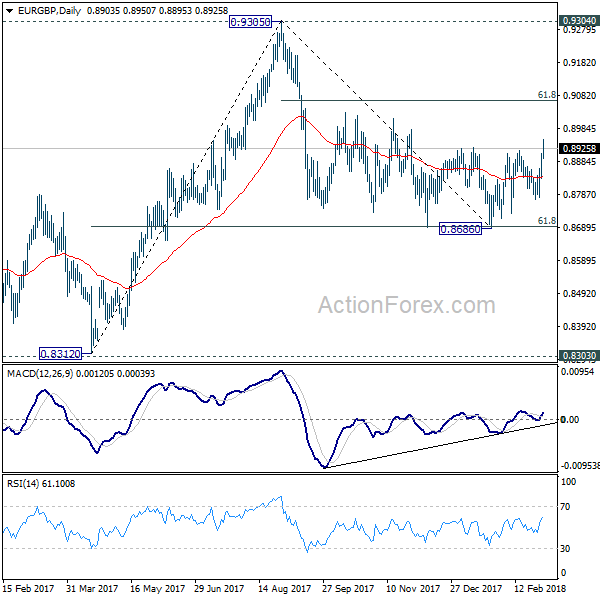

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8857; (P) 0.8883; (R1) 0.8929; More...

EUR/GBP surges to as high as 0.8950 today. The break of 0.8928 resistance now indicates medium term reversal. That is fall from 0.9305 has completed at 0.8868 after drawing support from 61.8% retracement of 0.8312 to 0.9305. Intraday bias is now on the upside for 61.8% retracement of 0.9305 to 0.8686 at 0.9069. Firm break there will target retest of 0.9305 high. On the downside, below 0.8877 minor support will turn intraday bias neutral again.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

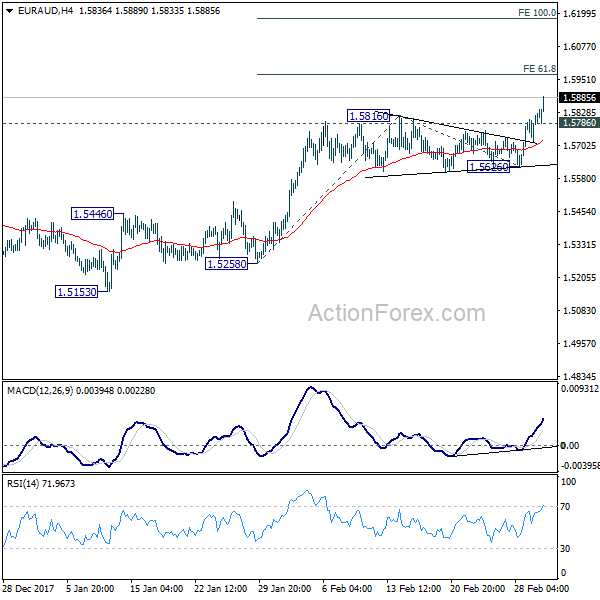

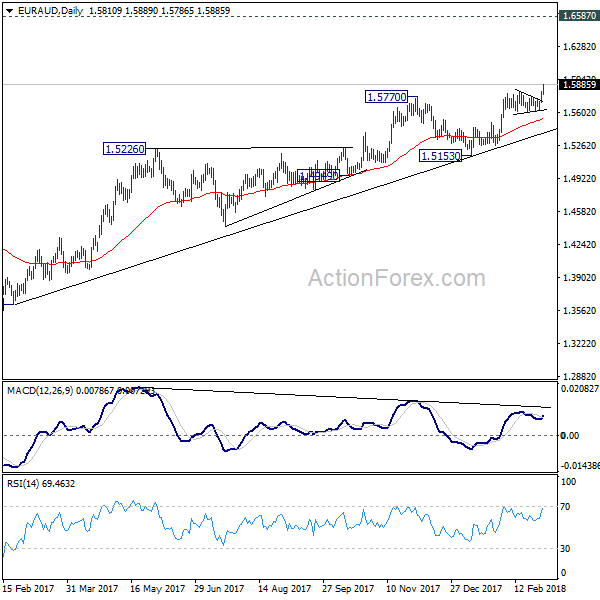

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.5737; (P) 1.5776; (R1) 1.5852; More....

EUR/AUD surges to as high as 1.5889 so far today and the development confirms resumption of medium term rally. Intraday bias stays on the upside for 61.8% projection of 1.5258 to 1.5816 from 1.5626 at 1.5971. Break will target 1.6526. On the downside, below 1.5786 minor support will turn intraday bias neutral. But outlook will remain bullish as long as 1.5626 support holds.

In the bigger picture, medium term rise from 1.3624 is still in progress for 1.6587 key resistance. At this point, we'd be cautious on strong resistance from there to limit upside. But decisive break will confirm resumption of long term rise from 1.1602. On the downside, break of 1.5153 support is needed to indicate completion of the medium term rise. Otherwise, outlook will remain bullish in case of pull back.

Dollar Bears Retake Control Amid Trade Risks; European Equities Dragged by Automakers

Here are the latest developments in global markets:

FOREX: Dollar bears remained in charge during early European trading afternoon amid trade uncertainties spurred by the US President, Donald Trump, yesterday, who said that he would impose new hefty tariffs on steel (25%) and aluminum (10%) imports. Fears that these measures could trigger a trade war between the US and the rest of the global economy including the biggest world exporter China, who responded today saying that it will safeguard its interests if harmed by the tariffs, pressured the dollar index to 89.89 (-0.44%) and sent dollar/yen to a fresh 15-month low of 105.26 (-0.78%). Comments from the BoJ Governor, Haruhiko Kuroda earlier today, were also supporting the yen, as Kuroda said that he would consider removing the ultra-accommodative monetary policy if inflation hits 2.0% by March 2020. Pound/dollar was moving sideways around 1.3787 (+0.10%) with investors being cautious ahead of May's Brexit speech later today, while euro/dollar was extending gains, slightly above the 1.23 key level (+0.41%) ahead of the Italian elections on Sunday, which could strengthen Eurosceptic parties, including the far-right Five Star Movement. This could be a headwind to euro pairs next week. Euro/pound jumped to a three-month high of 0.8932 (+0.22%). Dollar/loonie changed hands higher at 1.2861 (+0.21%).

STOCKS: European equities were on track to end the week in the red as hawkish monetary prospects in the US and trade concerns weighed on the market. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 1.56% and 1.76% respectively at 1200 GMT, with the automobile sectors losing the most as investors were worried that Trump's potential tariffs on steel and aluminum would hurt automakers. The German DAX 30 was one of the worst performers, losing 2.20% to trade near six-month lows, the Italian FTSE MIB dived by an equivalent amount, while the French CAC 40 tumbled by 1.88%. UK's FTSE 100 retreated by 1.0%. Germany's Volkswagen, Daimler, BMW, and France's Peugeot fell more than 2 percent. US stock futures were on the back foot as well.

COMMODITIES: Oil prices were set for a weekly loss for the first time in two weeks. WTI crude was last seen steady at $60.93/barrel (-0.10%) and Brent was flat at $63.89/barrel (-0.03%). In precious metals, gold was gaining momentum, trading at $1321.76/ounce (+0.40%).

Day ahead: Canadian GDP growth eyed; Theresa May comments on Brexit

Looking forward in the day, the focus will turn to Canada and the release of GDP growth figures, which have the potential to shake the loonie in times when the government faces trade headwinds arising from the US.

At 1330 GMT, the Canadian annualized GDP growth is expected to rise by 2.0% on a quarterly basis in the final quarter of 2017, surpassing the previous print of 1.7% and signaling that the economy ended the year on a strong foot. For the month of December, though, analysts believe that the country's economic performance slowed down, predicting a growth of 0.1% in monthly terms compared to 0.4% seen in November. An upward surprise in the data could push the loonie higher if the numbers approve stronger enough to convince investors to buy the currency despite Trump's announcement on steep tariffs on steel and aluminum which are likely to complicate the already subdued NAFTA talks even further. Note that Canada is the largest steel importer in the US, holding 16% of the product's volume.

In the US, data releases will include the final estimate of the Michigan consumer confidence index for the month of February and the Baker Hughes oil rig count for the week ending February 23 due at 1500 GMT and 1800 GMT respectively.

Political developments in Eurozone will be in the highlights during the weekend as Italy prepares to elect its next government on Sunday, while Germany is scheduled to publish results regarding a coalition vote held by Merkel's former coalition partners, the SPD, last month.

It would be interesting to see whether the pro-European sentiment will strengthen in Eurozone in case Italy's former ruling party, the center-left Democratic Party which has been in power from 2013 to 2016 wins the trust of the Italian citizens. However, the markets are currently suggesting that the outcome is likely to be a hung parliament and predict that the center-left coalition of Matteo Renzi's Democratic Party, the populist Five Star Movement, and the right-wing bloc comprising Silvio Berlusconi's Forza Italia and the far-right Lega Nord could be among those to lead the government in the upcoming months.

The Brexit story will remain in the spotlight after the British Prime Minister Theresa May's rejection of the Brexit draft treaty issued by the European Commission questioned any progress made in the EU-UK negotiations so far, including mainly the Irish border problem. May is anticipated to give a major speech on the Brexit front today in London at 1330 GMT.

Canadian Dollar Edges Lower Ahead of GDP

The Canadian dollar has posted slight losses in the Friday session. Currently, USD/CAD is trading at 1.2859, up 0.17% on the day. On the release front, Canada releases GDP, with the markets braced for a negligible gain of 0.1%. The US publishes UoM Consumer Sentiment, which is expected to jump to 99.4 points.

Global stock markets are seeing red on Friday, after US President Trump announced that he would be imposing stiff tariffs on steel and aluminum, in order to protect domestic producers. Under the new scheme, foreign steel will be taxed at 25% and aluminum at 10%. The response to the move was overwhelmingly negative, but abroad and in the US. China, Canada and the EU immediately denounced the move US auto makers and oil and gas producers also condemned the tariffs, saying they could get caught in the middle of a nasty trade war if other countries retaliate. In imposing the tariffs, Trump relied on a provision which allows such measures for national security, but clearly, US trading partners will not quietly accept these protectionist measures.

Canadian policymakers continue to look with growing alarm at protectionist moves by the Trump administration. Negotiations on NAFTA have not shown much progress, as a seventh and final round of talks are underway in Mexico City. As if the headache of a possible blowup of NAFTA wasn't bad enough, the Canadian government has to deal with the stiff imports that President Trump is set to apply to steel and aluminum imports. With some 80% of Canadian exports heading south to the US, Canada can ill afford a trade war with its giant neighbor. Still, the government will be under pressure to respond forcefully and stand up for its domestic steel industry.

The Bank of Canada is one of many spectators monitoring events at the Federal Reserve. With the Fed expected to raise rates up to four times in 2018, the BoC will be pressed to match rate hikes with its southern neighbor, or risk having the Canadian currency head lower. Currently, the BoC is projecting only two rate hikes in 2018. Strong growth has propelled the BoC to raise rates three times since July, but there are some factors weighing against a rate hike before May. First, fourth quarter expansion may fall short of the BoC's forecast of 2.5%. As well, the future of NAFTA remains unclear, as negotiations between Canada, Mexico and the US have floundered. If the US decides to pull out of NAFTA, the repercussions on the Canadian economy could be significant, and the BoC will have to delay any plans to raise rates.

USDJPY: Sells Off, Targets Further Bearishness

USDJPY: The pair sold off further on price weakness on Friday. On the downside, support lies at the 105.00 level where a break if seen will aim at the 104.50 level. A cut through here will turn focus to the 104.00 level and possibly lower towards the 103.50 level. On the upside, resistance resides at the 106.00 level. Further out, we envisage a possible move towards the 106.50 level. Further out, resistance resides at the 107.00 level with a turn above here aiming at the 107.50 level. On the whole, USDJPY faces further downside pressure.