Sample Category Title

Draghi’s Testimony In Focus Amid A Slow Trading Day

The U.S. dollar managed to close last week with some gains although investors weren't very confident. Data from the Eurozone confirmed that inflation rose at a pace of 1.3% on the headline in January while core inflation was seen rising 1.0%. The data was unchanged from the flash inflation estimates.

Canada's inflation data rebounded rising 0.7% on the month as January's inflation reversed the 0.4% decline from December while also beating estimates.

Looking ahead, the economic calendar today will see ECB President Mario Draghi testifying to the European parliament in Brussels. Investors will be closely watching for any references to the ECB's monetary policies. The central bank is due to meet in a week's time for its monetary policy meeting.

Elsewhere, new home sales data will be coming out during the NY trading session. Forecasts point to a modest increase of 655k compared to 625k print registered previously. However, the U.S. housing markets data remained mixed over the past week and could potentially offer some surprises for the market.

Among the policy maker speeches, the BoE's MPC member, Cunliffe will be speaking while the Fed's Quarles will be speaking later in the day.

Currencies: Dollar Struggles As Markets Await Powell’s Hearing Before Congress

Sunrise Market Commentary

- Rates: Consolidation ahead of Powell's testimony?

Sentiment on core bond markets turned more neutral last week, especially in Europe. The Bund approaches first resistance. We expect some consolidation today amid an uninspiring eco calendar and ahead of German CPI data and Fed chair Powell's testimony in front of US Congress. - Currencies: Dollar struggles as markets await Powell's hearing before Congress

The USD rebound slowed last week. US yields eased and strong US equities currently are a negative rather than a positive for the dollar. USD traders are looking forward to Fed Powell's testimony before Congress. Later this week, the news flow might be tentatively USD supportive/euro negative. Sterling traders keep an eye at a key speech of labour leader Corbyn

The Sunrise Headlines

- US equity markets closed last week on a strong footing, ending around 1.5% higher. Asian risk sentiment remains positive this morning with China and Japan outperforming.

- China's ruling Communist Party set the stage for President Xi Jinping to stay in office indefinitely, with a proposal to remove a constitutional clause limiting presidential service to just two terms in office.

- S&P raised Russia's foreign sovereign credit rating into investment grade (BBB- from BB+, positive outlook) citing the country's “prudent policy response” in the face of lower commodity prices and international sanctions.

- The White House plans to promote an adviser known for his hawkish views on trade policy, giving economic nationalists a stronger voice in internal debates as the Trump administration nears decisions on high-profile trade issues. (WSJ)

- The EU is set to publish a draft Brexit withdrawal agreement that omits key compromise language on Northern Ireland inserted by Britain in December's divorce deal, the FT reports, citing three officials familiar with the text.

- The opposition Labour Party is poised to announce a new strategy aimed at forcing Britain to maintain close economic ties with the EU after it leaves the bloc. Jeremy Corbyn will clarify the party's position today.

- Today's eco calendar contains US new home sales. Several central bankers are scheduled to speak and the Kingdom of Belgium probably launches its debut green OLO via syndication (OLO 86 Apr2033).

Currencies: Dollar Struggles As Markets Await Powell's Hearing Before Congress

USD struggles ahead of Powell's policy assessment

USD trading was technically-driven on Friday. Core yields eased, but rate differentials were little changed. Equities traded mixed in Europe, but staged an impressive rebound in the US. The rally failed to guide USD trading. EUR/USD hovered near 1.23 (close 1.2295). USD/JPY traded with a minor negative bias and finished the day at 106.89.

This morning, Asian equities join the rally from WS on Friday, but the gains area more modest. Risk-on sentiment is weighing slightly on the dollar as was often the case of late. EUR/USD trades in the 1.2325 area. USD/JPY is drifting south in the 106 big figure (currently 106.60).

Today, the US calendar contains regional activity surveys and new home sales. The data will only be of intraday significance for USD trading. Several Fed members give their view on the economy and on policy. However, the focus will be on tomorrow's hearing of Fed's Powell before Congress. He might confirm that solid US growth requires further normalization of monetary policy. This message could be mildly USD supportive. Later this week, there are plenty of eco data, including US PCE deflators (Thursday) and EMU February inflation, expected at a soft 1.2% Y/Y (Wednesday). There will also be headlines on political risk in EMU as markets look forward to the Italian elections and the approval of the German government coalition by the SPD next weekend. The news flow might be slightly supportive for USD and tentatively negative for the euro. However, the USD recently didn't profit much from good news. Last week, we advocated consolidation on the ST USD rebound. We maintain that view. LT US yields are near key resistance, but aren't ready for a break, further slowing the USD rebound. First support in EUR/USD is coming in at 1.2206/1.2165. It might be too early for a test. European political event risk is a wildcard, but we don't assume it to be a big negative for the euro. Equities remain a wildcard.

This weekend, BoE's Ramsden signaled that UK interest rates could be raised sooner rather than later. Today the focus for GBP-trading turns to a speech of Labour leader Corbyn. He is expected to support the case of the UK to maintain a customs union with the EU. This could cause further division within the conservative party, but sterling might profit from rising chances of a soft Brexit. EUR/GBP might drift further south in the 0.9033/0.8690 trading range. For now, we assume that this range bottom will hold short-term

EUR/USD: dollar rally slows as markets look forward to Fed Powell's hearing before Congress

EU Leaders Agree To Shore Up The Budget As Brexit Bites

EU European Council Meetings took place on Friday and EU Council President Donald Tusk made the following comments: EU leaders agreed to spend more on migration, defence and security and all EU leaders are ready to work to modernize the budget, some ready to contribute more. Reaching an agreement on the budget this year appears difficult. EU leaders endorse downsizing European Parliament to 705 seats from 751 seats. He hopes to get more clarity on British views on future relations after Brexit discussions next week.

German Gross Domestic Product w.d.a (YoY) (Q4) was as expected, unchanged at 2.9%. Gross Domestic Product (QoQ) (Q4) was as expected at 0.6%, from 0.6% previously, that was revised up to 0.7%. Gross Domestic Product (YoY) (Q4) was also as expected, at 2.3%, from 2.3% prior, that was revised down to 2.2%. EURUSD fell 1.22934 to a low of 1.22795.

Eurozone Consumer Price Index – Core (YoY) (Jan) was released, coming in as expected, unchanged at 1%. Consumer Price Index (MoM) (Jan) was as expected at -0.9%, from 0.4% previously. Consumer Price Index (YoY) (Jan) was as expected, unchanged at 1.3%. Consumer Price Index – Core (MoM) (Jan) was -1.7% v an expected -1.6%, from 0.5% prior. EURUSD moved higher from 1.23046 to a high of 1.23172 due to this data.

UK BOE Ramsden spoke at a panel discussion titled “Tackling the UK’s Productivity Challenge” at the East of England Confederation of British Industry event, in Cambridge. He made the following comments: The MPC’s judgement is that productivity growth will settle at just over 1% over the next three years. Structural shocks to the economy from Brexit can’t be offset by monetary policy. The pace of productivity influences what happens to inflation. Still no confirmation that productivity pickup is sustained in the near-term. UK business investment has been unusually weak relative to past recoveries. There are significant risks in both directions to the outlook for productivity. Naturally lower productivity growth and the dampening effect of Brexit are risks to productivity.

Canadian Consumer Price Index (MoM) (Jan) was 0.7% v an expected 0.4%, from -0.4% previously. BOC Consumer Price Index Core (YoY) (Jan) was as expected, unchanged at 1.2%. BOC Consumer Price Index Core (MoM) (Jan) was 0.5% v an expected 0.7%, from a prior -0.5%. Consumer Price Index (YoY) (Jan) was 1.7% v an expected 1.4%, from 1.9% previously. Consumer Price Index – Core (MoM) (Jan) was 0.2% v 0.1% previously, which was revised up to 0.2%. USDCAD dropped down from 1.26987 to a low of 1.26166 before recovering to 1.26948 after this release.

US Fed’s Dudley and Federal Reserve Bank of Boston President Rosengren spoke on a panel discussion about the Fed’s balance sheet at the United States Monetary Policy Forum, in New York. They made the following comments:

Dudley: QE still useful tool at zero lower bound. Bond portfolio run-down essentially on autopilot: has not disrupted markets. We should not care about treasury yields alone. The balance sheet is likely returning to 2 trillion or more.

Rosengren: Likely to have low real rates for some time and we will need QE again in the future. Expect low rates for some time due to slow US productivity, labor force growth. Large US deficits now make it more difficult for fiscal policy to curb future recessions. Quite likely Fed will need bond-buying policies in future. Also said he was not a big fan of negative interest rates.

Baker Hughes US Rig Count numbers were released, coming in at 799. The prior number last Friday showed that there were 798 Oil rigs in operation.

US FOMC Member Mester spoke at a panel discussion about monetary policy objectives at the United States Monetary Policy Forum, in New York and made the following comments: The labour market is strong and inflation is expected to rise to 2%. A smooth transition to new Fed leadership is underway and the economy is coming back to normal, with the Fed’s policy normalizing. She is open-minded on the need to alter Fed policy framework and the bars should be high for altering Fed policy framework. She backs the beginning assessment of said framework later in 2018. The negative rates work better in Europe than we expected.

ECB’s Coeur spoke on the same panel and made these comments: With the current share of the bund free flow constituting already a small fraction of the total outstanding, additional purchases become less necessary to contain the term premium at low levels. The amount of purchases needed to deliver a given compression of the term premium is likely to fall over time. In the future, the euro system can retreat as a buyer in the market, without risking an unwarranted decompression of the term premium. The stock effect of QE reduces the need for new purchases. The negative rates have not caused adverse negative effects. The ECB’s pace of communication is complicated by the region’s diversity.

US FOMC Member Williams spoke about economic and monetary policy at the City Club of Los Angeles. His comments were: The financial system now looks good, well-capitalized. The US labour market looks very strong and we are seeing some pickup in wage growth. Despite tailwinds, the US economic outlook is no different than prior years and the economy is improving broadly across sectors. The global economy is very good and improving, and financial conditions overall are still supportive of growth. Inflation is picking up as transitory factors begin to fade. The Fed’s guidance calls for gradual rate hikes and he expects that to continue but would have to reassess policy if inflation came out stronger. The tax cuts will have a moderate economic growth impact over the next several years. The Fed aims to keep the economy in balance to avoid overheating and needs to prepare to have tools for the next recession. It will be a challenge for China to manage debt build-up.

Japanese Coincident Index (Dec) was released at 120.2 against an expected 118.3, from 120.7 prior, which was revised down to 117.9. The Leading Economic Index (Dec) was 107.4 v an expected 108.3, from 107.9 previously, which was revised up to 108.2. USDJPY moved up to a high of 106.690 before selling off to 106.478.

EURUSD is up 0.29% overnight, trading around 1.23287.

USDJPY is down -0.36% in early session trading at around 106.476.

GBPUSD is up 0.40% to trade around 1.40241.

Gold is up 0.85% in early morning trading at around $1,339.67.

WTI is up 0.25% this morning, trading around $63.72.

Major data releases for today:

At 13:00 GMT, US Fed’s Bullard is due to make a scheduled speech with comments having the potential to move USD pairs.

At 13:30 GMT, US Chicago Fed National Activity Index (Jan) is expected to be 0.15 against a previous 0.27, with this data having the potential to move USD pairs.

At 14:00 GMT, ECB President Mario Draghi is due to testify on monetary policy and the inflation outlook before the European Parliament Economic and Monetary Affairs Committee in Brussels.

At 15:00 GMT, US New Home Sales (MoM) (Jan) is expected to come in at 0.642M from 0.625M previously. New Home Sales Change (MoM) (Jan) is expected at 0.1% v -9.3% previously. USD crosses may be heavily traded as a result of this data.

At 15:30 GMT, US Dallas Fed Manufacturing Business Index (Feb) is expected to come in at 28.4 from 33.4 previously.

At 18:00 GMT, UK MPC Member Cunliffe is due to deliver a speech titled “What is Money?” at the University of Warwick’s Speaker Series and his comments will be followed by traders for any hints on future BOE policy.

At 21:45 GMT, New Zealand Trade Balance (MoM) (Jan) numbers will be released and is expected to be $640M. The prior number was $-1,193M. Imports (Jan) were $4.91B previously. Trade Balance (YoY) (Jan) was $-2.84B previously. Exports (Jan) were $5.55B previously. This data could affect NZD crosses.

Major data releases for this week:

On Tuesday, at 13:00 GMT, German Harmonised Index of Consumer Prices (YoY) (Feb) will be released.

Also on Tuesday, at 13:30 GMT, US Fed’s Powell is due to testify on the Semi-Annual Monetary Policy Report before the House Financial Services Committee, in Washington DC, in his new capacity as Chairman.

On Wednesday, at 10:00 GMT, Eurozone CPI Data will be released.

At 13:30 GMT, US GDP data will be published along with Core Personal Consumption Expenditures for Q4.

On Thursday, at 13:30 GMT, US Core Personal Consumption Expenditures for January will be released.

At 15:00 GMT, ISM Manufacturing PMI and Prices Paid data for February will be published.

Powell’s Testimony And Macro Data To Dominate Markets Action

Asian equity markets kicked off the week on a strong footing following a positive lead from Wall Street on Friday.

Bulls seem to have taken control after the S&P 500 rallied 1.6% on Friday and Treasury yields retreated further from the 3% critical level. The broad-based rally on Friday wasled by the utilities, energy and technology sectors, suggesting that investors shrugged off concerns about rising interest rates. The Cboe's VIX decline of 11.9% on Friday also indicates that the worst of the volatility is most likely behind us. However, investors shouldn't take anything for granted, as this week is shaping to be a busy one, dominated by Fed Chair Jay Powell providing testimony to Congress and key data releases from the U.S. and Europe.

The FOMC's latest minutes show that policymakers have grown a little more hawkish recently, but the trajectory on interest rates has not changed significantly according to CME's FedWatch. Investors are pricing in a 62% chance of three rate hikes in 2018, suggesting that markets see Powell as asimilar version of Yellen.

A gradual policy normalization with three rate hikes in 2018, is likely to be the base case scenario in Powell's message. Any signal towards a fourthrate hike will likely disrupt markets, similar to the selloff witnessed last month.

The shape of the yield curve has also become a key indicator for risk. Although a flattening yield curve should signal slower economic growth, it has been enthusiastically welcomed by investors for the last couple of years. From November 2013 until late January 2018, the Treasury 30-5 yearswap spread shrunk to 41 basis points, the lowest since 2007. This was accompanied by new records in equities. Any indication from Powell that Trump's fiscal policies should be met with higher long-term interest rates will also be problematic for stocks. However, given where Treasury yields stand now, it doesn't seem bond traders are worried.

On the data front, Thursday's U.S. Core Personal Consumption Expenditure will be closely scrutinized given it's the Fed's preferred measure of inflation. A rise above 0.3% will again intensify fears that the U.S. central bank needs to accelerate rates at a faster pace. Investors will also be watching US GDP second reading, durable goods orders, home sales, personal income & spending, manufacturing PMI, and consumer confidence levels.

Daily Wave Analysis: EUR/USD Approaches 1.2350 And Prepares For Bullish Breakout

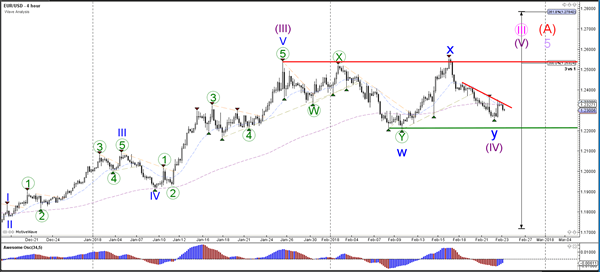

Currency pair EUR/USD

The EUR/USD is trying to show a bullish breakout above the resistance trend line (dotted red), which would confirm a potential continuation of bullish wave 5 (purple).Price is probably in a wave 4 (purple) as long as price stays above support (green).

The EUR/USD break above the tops (orange) could confirm the potential for a bullish breakout towards the Fib targets of wave 3 (blue). A strong bearish turn at 1.2475-1.25 could indicate that price has built an ABC rather than a 123.

Currency pair GBP/USD

The GBP/USD is building a triangle pattern. Price will need to break the S&R before a new trend can become visible.

The GBP/USD is breaking through resistance (dotted red) which could indicate the potential for a bullish breakout.

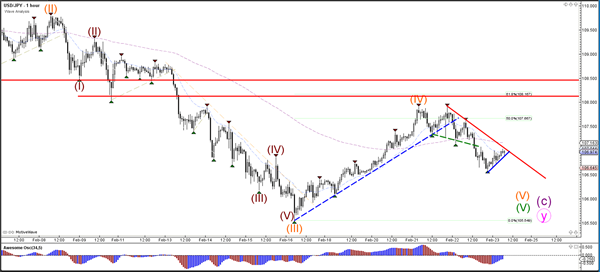

Currency pair USD/JPY

The USD/JPY could be ready for one more push lower within wave 5 (green) if price manages to break below the support trend line (blue).

The USD/JPY is building a sideways correction and is marked by support (blue) and resistance trend lines. A bullish breakout would probably invalidate wave 4 (orange) whereas a bearish break could indicate a downtrend continuation.

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD slightly rose against the USD and closed at 0.7837 on Friday.

LME Copper prices rose 0.6% or $41.5/MT to $7073.5/MT. Aluminium prices rose 0.7% or $16.0/MT to $2210.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7860, with the AUD trading 0.29% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7820, and a fall through could take it to the next support level of 0.7779. The pair is expected to find its first resistance at 0.7885, and a rise through could take it to the next resistance level of 0.7909.

With no macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Slowed As Initially Estimated In January

For the 24 hours to 23:00 GMT, the EUR declined 0.12% against the USD and closed at 1.2298 on Friday, after data confirmed that annual inflation in the Euro-zone slowed in January.

The Euro-zone's final consumer price index (CPI) rose 1.3% on an annual basis in January, confirming the preliminary print, thus indicating that inflation is shifting further away from the European Central Bank's (ECB) goal of just under 2.0%. In the previous month, the CPI had advanced 1.4%.

Separately, Germany's seasonally adjusted final gross domestic product (GDP) climbed 0.6% on a quarterly basis in the fourth quarter of 2017, in line with the flash print. The nation's GDP had recorded a rise of 0.8% in the previous quarter.

On Friday, the Federal Reserve (Fed), in its semi-annual Monetary Policy Report to the Congress, indicated that officials expect the ongoing strength in the US economy to warrant further gradual increases in the federal funds rate. Further, policymakers highlighted a pickup in inflation towards the end of last year.

In the Asian session, at GMT0400, the pair is trading at 1.2310, with the EUR trading 0.1% higher against the USD from Friday's close.

The pair is expected to find support at 1.2286, and a fall through could take it to the next support level of 1.2263. The pair is expected to find its first resistance at 1.2327, and a rise through could take it to the next resistance level of 1.2345.

Moving ahead, market participants would closely monitor a speech by the ECB President, Mario Draghi, due in a few hours. Additionally, the US new home sales data for January, slated to release later in the day, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Rises On Hopes For A Post-Brexit UK-EU Trade Deal

For the 24 hours to 23:00 GMT, the GBP rose 0.09% against the USD and closed at 1.3969 on Friday, amid renewed hopes of a softer Brexit, following reports that the 11-member Brexit cabinet committee reached an agreement on a proposal for post-Brexit trade with the European Union.

In the Asian session, at GMT0400, the pair is trading at 1.3997, with the GBP trading 0.2% higher against the USD from Friday’s close.

The pair is expected to find support at 1.3932, and a fall through could take it to the next support level of 1.3866. The pair is expected to find its first resistance at 1.4036, and a rise through could take it to the next resistance level of 1.4074.

Going ahead, traders would look forward to UK’s BBA mortgage approvals data for January, slated to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Stronger Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the JPY and closed at 106.71 on Friday.

In the Asian session, at GMT0400, the pair is trading at 106.56, with the USD trading 0.14% lower against the JPY from Friday’s close.

The pair is expected to find support at 106.27, and a fall through could take it to the next support level of 105.97. The pair is expected to find its first resistance at 107.03, and a rise through could take it to the next resistance level of 107.49.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.21% against the CHF and closed at 0.9360 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9345, with the USD trading 0.16% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9328, and a fall through could take it to the next support level of 0.9312. The pair is expected to find its first resistance at 0.9368, and a rise through could take it to the next resistance level of 0.9392.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.