Sample Category Title

Dollar Broadly Lower, Fed Powell and UK May to Watch This Week

Dollar weakens broadly as another week starts rather quietly. On the other hand, Aussie and Kiwi stage a strong come back. Canadian Dollar doesn't follow as weighed down by concerns over the NAFTA talks that resumed this week. Euro is also mildly softer ahead of Italy election and outcome of German SPD vote on grand coalition this weekend. Technically, as noted before, dollar remains limited comfortably below near term resistance against others. It remains to be seen whether new Fed chair Jerome Powell's testimony would make or break the greenback.

BoJ Kuroda dismissed review on policy framework

BoJ Governor Haruhiko Kuroda, recently reappointed for another five year term, dismissed the request by an opposition lawmaker to review the policy framework. Kuroda told the parliament that "it's unfortunate that achievement of our price target has been delayed. But thanks to the effect of our powerful monetary easing, Japan's economy is no longer in a state that can be described as deflation." He also pointed to recovery in the economy and said "things are proceeding smoothly". And therefore, "I don't have any plan at this stage to conduct another comprehensive review."

Fed Powell's testimony unlikely to deviate from the monetary policy report

The week ahead is very busy. New Fed chair Jerome Powell's testimony will be a major focus. As a prelude, Fed released its semi annual Monetary Policy Report last Friday. The report noted that "with inflation having persistently run below the 2% longer-run objective the Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal". It appears that similar reference had not been revealed in previous FOMC statement or minutes.

The Fed also warned of the elevated valuation of asset prices. As suggested in the report, "valuation pressures continue to be elevated across a range of asset classes even after taking into account the current level of Treasury yields and the expectation that the reduction in corporate tax rates should generate an increase in after-tax earnings. Leverage in the nonfinancial business sector has remained high, and net issuance of risky debt has climbed in recent months".

Powell's message in the testimony will likely not deviate much from the report regarding monetary policy. He's expected to reiterate the gradual path of monetary policy normalization. Yet, his comments about the growth outlook in light of the tax reform plan would be closely watched.

UK PM May to make high profile speech on Brexit again

Another focus is UK Prime Minister Theresa May's high profile speech on Brexit on Friday. May is expected to lay out an "ambitious" vision of future relationship with EU. That came after the Cabinet's Brexit "war committee" has finally reached a consensus on the stance last week. May said that "the deal we negotiate with the EU must present an ambitious future for our great country".

And, she added " I will present the committee's conclusions to an additional session of the full Cabinet before travelling to the North-east on Friday to give a speech setting out this Government's vision of what our future economic partnership with the European Union should look like."

May also emphasized that "delivering the best Brexit is about our national future, part of the way we improve the lives of people all over the country. So I concluded the meeting by reminding the committee that the decisions we make now will shape this country for a generation."

It should be reminded that there are expectations of a BoE rate hike as early as during the meeting in May. But that's heavily tied to the assume for an agreement with EU for the transition period after Brexit. Such expectation could change drastically depending on what markets would expect after PM May's speech.

On the data front

Here are some highlights for the week ahead:

- Monday: UK BBA mortgage approvals; US new home sales

- Tuesday: German CPI; Eurozone M3; US durables, trade balance, wholesale inventories, house price indices, consumer confidence, Fed Powell's testimony

- Wednesday: Japan industrial production, retail sales, housing starts; New Zealand business confidence; UK BRC shop price, Gfk consumer confidence; China PMIs; Swiss UBS consumption indicator, KOF economic barometer; German Gfk consumer sentiment; Eurozone CPI flash; Canada IPPI and RMPI; US GDP revision, Chicago PMI, pending home sales

- Thursday: New Zealand terms of trade; Japan capital spending, consumer confidence; China Caixin PMI; Swiss GDP, retail sales; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing, M4, mortgage approvals; UK ISM manufacturing, construction spending

- Friday: New Zealand building consents; Japan household spending, unemployment rate, monetary base, Tokyo CPI core; German retail sales, import prices; UK construction PMI; Eurozone PPI; Canada GDP

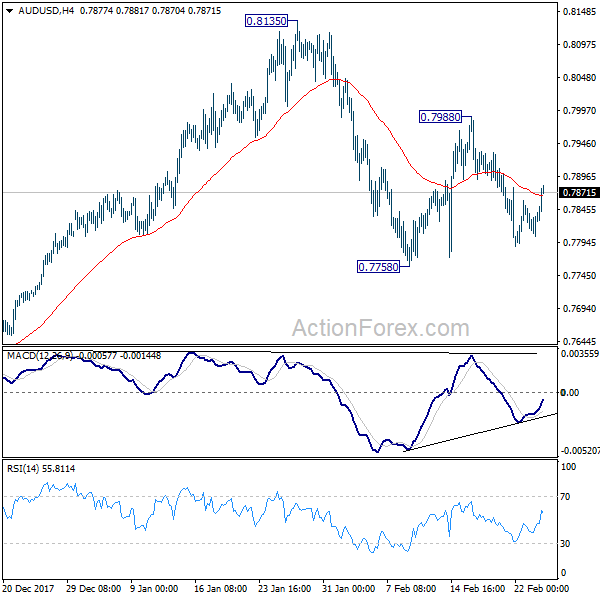

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7811; (P) 0.7829; (R1) 0.7853; More...

AUD/USD recovers today but it's staying in range of 0.7758/7988. Intraday bias remains neutral at this point. On the upside, above 0.7988 will extend the rebound to retest 0.8135. On the downside, below 0.7758 will resume the fall from 0.8135 and target 0.7500 key near term support. At this point, there is no strong case for a range breakout yet and 0.7500/8135 could hold for a while.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:30 | GBP | BBA Loans for House Purchase Jan | 37.2K | 36.1K | ||

| 15:00 | USD | New Home Sales Jan | 646K | 625K |

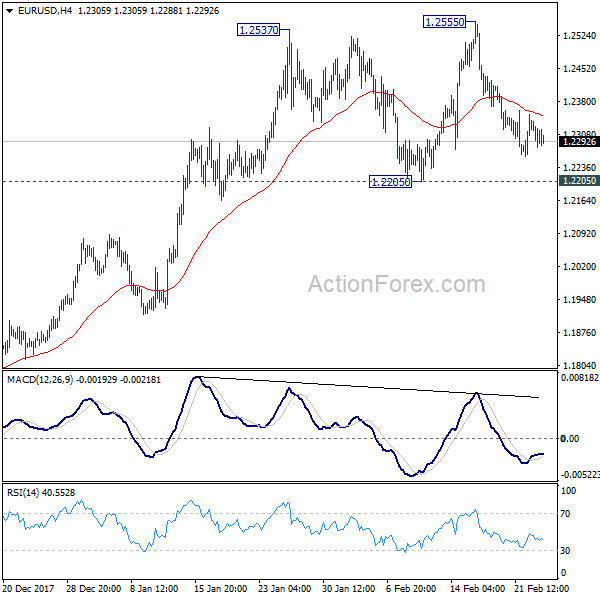

EUR/USD Trading Near Make-Or-Break Levels

Key Highlights

- The Euro declined this past week and broke the 1.2350 support against the US Dollar.

- There is a key bullish trend line forming with support at 1.2265 on the 4-hours chart of EUR/USD.

- The pair must break the 1.2350 and 1.2370 resistance levels to gain upside momentum.

- The Euro Zone CPI in Jan 2018 increased 1.3% (YoY), similar to the forecast.

EURUSD Technical Analysis

This past week was mostly bearish for the Euro as it moved below the 1.2350 support against the US Dollar. The EUR/USD pair is currently holding the 1.2250 support, but it remains at a risk of more declines.

The 4-hours chart suggest that the pair struggled to hold gains above the 1.2400 level and declined below the 100 simple moving average (red, 4-hour). The pair traded close to the 1.2250-60 support area and later is started consolidating losses.

On the downside, there is a key bullish trend line forming with support at 1.2265 on the same chart. If there is a break below the trend line and support at 1.2250, there could be more losses toward the 1.2200 level.

On the upside, there is a connecting bearish trend line with resistance at 1.2330. Above 1.2330, the pair must break the 1.2350 and 1.2370 resistance levels to move back in the bullish zone.

Above 1.2370, the next major resistance is near the 50% Fib retracement level of the last decline from the 1.2555 high to 1.2260 low at 1.2407.

This past week, the Euro Zone saw the CPI report for Jan 2018 by the Eurostat. The market was looking for a rise of 1.3% compared with the same month a year ago. The actual result was similar, but the monthly CPI declined 0.9%, compared with the last +0.4%.

The report added:

The lowest annual rates were registered in Cyprus (-1.5%), Greece (0.2%) and Ireland (0.3%). The highest annual rates were recorded in Lithuania and Estonia (both 3.6%) and Romania (3.4%). Compared with December 2017, annual inflation fell in twenty-one Member States, remained stable in one and rose in six.

Overall, the Euro may find it hard to recover above 1.2350 in the near term. On the downside, the 1.2250 and 1.2200 levels are important supports.

Market Morning Briefing: The Dollar Index Tested Resistance On Daily Candles Near 90.1-90.2 Last Week

STOCKS

Dow (25309.99, +1.39%) is trading just below interim resistance near 25500. A break above 25500, if seen could take it higher towards 26000 else a fall back towards 24400 or lower is possible.

Dax (12483.79, +0.18%) is trying to move up gradually towards 12600 resistance which is likely to hold and push the index back towards 12400.

Levels near 106.50 is important on the Japanese Yen and while that holds, the Nikkei (22071.52, +0.82%) is likely to move up in the near term

towards 22500 levels. If the Japanese Yen sees further strength in the next few sessions, rise in Nikkei could be limited on the upside. Immediate target would be 22500 in the coming sessions.

3325-3350 could be an immediate resistance for Shanghai (3302.41, +0.41%) and while that holds, the index is likely to come off towards 3300 or lower again by end of the week of early next week.

Nifty (10491.05, +1.04%) and Sensex (34142.15, +0.95%) have risen from current support level as visible on the daily candles and while that holds, the indices may move up some more this week towards 10620 and 34500-34750 respectively. Immediate view is bullish.

COMMODITIES

WTI (63.84) and Brent (67.50) have risen from previous levels. WTI has broken above immediate resistance near 63 and while the rise continues, WTI may move up towards 65. Brent on the other hand, is likely to test 68 on the upside, break of which can lead to further rise towards 69-70 in the medium term.

Gold (1337) is holding above support near 1320 and while that holds, the price may move up towards 1350/60 again in the coming sessions. Near term looks bullish.

Copper (3.2170) is almost stable without any major movement. It is likely to move up to 3.15-3.30 levels in the near term.

FOREX

The Dollar Index (89.722) tested resistance on daily candles near 90.1-90.2 last week and if the ranging movement of the last 3 weeks continues, it is likely to dip this week towards support near 88.25 on the daily candles.

Euro (1.2318) has also been ranging for the last 3 weeks in the broad 1.22-1.255 zone and if the ranging continues this week, we could see another test of 1.25 sometime late in the week.

The Dollar-Yen (106.51) has some support near 106.25-106.5 on the 3 day line chart and the weekly candles. If it breaks this support, it could dip further to test 105.5 on weekly line chart which is a crucial support level (and had held last week).

The Euro-Yen (131.17) could find some support on daily candles near 131 in the near term. The downside target of 105.5 for Dollar Yen and the upside target of 1.25 for the Euro this week gives the probable target for Euro Yen as 131.87.

Pound (1.4008) could test resistance near 1.405-1.408 on daily candles in the next couple of sessions and dip from there.

Dollar-Rupee (64.735): Support likely at 64.60. If breached, see 64.45-30. Might go back up towards 64.80-90.

INTEREST RATES

US 10 Year Yield (2.8532), US 30 year Yield (3.1448), US 5 year yield (2.6015), US 2 year yield (2.23) : As predicted last Friday, the 10 Yr yield has indeed come back below 2.9% again and the Feb ranging between 2.85% and 2.95% continues. Similarly, the other yields have also dipped slightly and have come nearer to their long term resistance levels.As mentioned last week, a test of 3% for the 10 Year yield still looks to be few weeks away.

(Long term resistance levels for the 4 yields earlier mentioned are as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively - we have been expecting these levels to hold in this month.)

The German-US 10 Yr yield spread (-2.2) is near support and could see a bounce in this week / next week. Note that the German 10 Yr yield (0.65%) has dipped below support near 0.7% and hence a bounce in the German-US yield spread could be led by a further dip in US 10 Yr yield.

GOLD – Sees Price Hesitation But With Recovery Risk

GOLD - The commodity may have closed lower the past week but a recovery higher threat. On the downside, support comes in at the 1,320.00 level where a break will turn attention to the 1,310.00 level. Further down, a cut through here will open the door for a move lower towards the 1,300.00 level. Below here if seen could trigger further downside pressure towards the 1,240.00 level. Conversely, resistance resides at the 1,350.00 level where a break will aim at the 1,360.00 level. A turn above there will expose the 1,370.00 level. Further out, resistance stands at the 1,380.00 level. All in all, GOLD looks to weaken further

EURUSD – Consolidates But With Recovery Risk

EURUSD - With the pair seeing price hesitation the past week, a directional move is a challenge. On the upside, resistance comes in at 1.2350 level with a cut through here opening the door for more upside towards the 1.2400 level. Further up, resistance lies at the 1.2450 level where a break will expose the 1.2500 level. Conversely, support lies at the 1.2250 level where a violation will aim at the 1.2200 level. A break of here will aim at the 1.2150 level. Below here will open the door for more weakness towards the 1.2100. All in all, EURUSD faces further bear threats on correction.

What’s GBPCAD Going To Do Here?

As shown in the weekly chart below, it looks as though something is on the horizon for GBPCAD as price lingers around some pretty heavy resistance.

We're presented with two possible scenarios – Price either gets rejected, or we see price breaking through resistance. Let's go down to a daily chart for further analysis.

It looks as though momentum has slowed significantly at our resistance area, which is holding for now. If price can break through our minor support area of 1.75ish we could possibly see a move to 1.73 where it would likely encounter more support, or even a further move through to the 1.68 area. A suitable stop loss area could be just above the recent high, presenting a good R:R ratio. The alternative possibility is that price breaks through resistance.

A New Sheriff In Town

The markets are increasingly challenging to define as storylines shift from ECB and BoJ policy normalisation to the problematic US twin deficits and inflation. However, the dollar has remained bid against most G10 currencies of late. As equity markest near another significant inflexion point as bond yields look poised to move higher, however, fixed income was exceedingly bid entering weeks end. Regarding an outright spark in Fixed income, which is driving the bus these days, there are no easy answers. Most are pointing to positioning adjustment ahead of the weekend and other events on the near horizon. Jerome Powells Humphrey Hawkins testimony and the Italian elections do strike a chord, while others point to growing signs that all is not doom and gloom in the bond pits and tactical buying is re-emerging.

Both economic and political worlds collide this week with the lion's share of attention falls on The New Sheriff in Town, Powell's testimony, however, I suspect we will end up with more emphasis on Europe and the Italian elections.

Let's face it, Italy is not known for political stability, as governments change about as often as the weather does. And on cue, protests have broken out across Italy over the weekend on both sides of the political spectrum. Expect a messy affair, and it will be difficult for any of the primary political parties to form a new government in what is shipping up to be one of the most unpredictable calls.Complicating matters is the high number of undecided votes which could be as high as 45% if current polls are accurate. And while xenophobia runs rampant amongst the electorate, political leader are easing their Euroskeptic perimeters so all may not as bad as it seems. Given Italy's history of encouraging coalition government, why should we expect anything different?Electoral shocks should be isolated, and the fear of political contagion should remain muted.

But let us not lose sight that On Friday, the postal ballot to ratify the Grand Coalition proposal with Merkel's CDU/CSU group ends. SPD members, who have the final say on the coalition agreement for Europe's largest economy, must vote by March 2 in a postal ballot, with results to be made public on March 4.

While the markets should get through these treacherous political storms, but obviously, it's wise to respect the fact that any failure to bring the EU political environment into equilibrium could send shockwaves through the union and beyond.

With so much hype over the new Fed Chair Powell's Humphrey Hawkins testimony, it's bound to disappoint. The bar is towering for a hawkish surprise as the prepared statement is likely to be salted with familiar FOMC repetition, similar to the recent FOMC Minutes for fear of sending equity market into a tailspin given the bearish bond market overtones.

There is no incentive for Powell to pre-signal any shift in the Fed narrative instead he will probably let traders do the Fed's heavy lifting this quarter as market risk is becoming more aligned to the reality that fiscal expansion could nudge US interest rates higher this year. With that said, there little to suggest this new Fed chair will be any less dependent on economic data than his predecessor, so the jury should remain out about a quicker pace of interest rate normalisation as the market remains comfortably parked in the three rate hike camp.

From the Fed's perspective, there is nothing gained by feeding the volatility beast. But no doubt, some skillfully placed partisan questions designed to trip up the new Chair during Q and A could be useful for a kneejerk or two.

Oil Markets

Markets are coming off whippy week for crude benchmarks, but conviction and sentiment should continue to rise after a surprisingly robust EIA drawdown in oil inventories However as briefly this may last, the stars are aligning for Oil bulls as U.S. oil production also remained flat while US exports surged. Also, momentum traders caught an updraft from yet another supply outage, this time from Libyan El Feel oilfield closure due to support workers wage disputes.

We continue to get positive news from OPEC compliance cementing the floor at WTI 60.00 per barrel which is creating a positive wave of conviction that investors appear keen to ride.

Uncertainty ahead of Powell testimony could lead to some position adjustments but unlikely to change the current bullish narrative.

From a technical perspective, with the futures markets in backwardation its suggests inventories could run leaner for some time but as we move deeper into global refinery maintenance season, US crude export could face some possible headwinds balancing each others impact.

Gold Markets

Gold continues to act as less of a haven hedge and more as a proxy for USD sentiment so we could be facing a critical week for Gold prices as the USD will come under the microscope as new Fed Chair Powell takes centre stage.

But with US's runaway deficit spending train stoking inflationary fears, Gold remains a crucial buy on dip strategy not only to hedge against inflation but also against another untimely correction in equity markets. With uncertainty surrounding the toxic elixir of higher inflation and the expected USD headwinds from record US debt, gold's appeal should remain healthy over the near term.

Currency Markets

On the surface, there is two-way risk heading into Powell's testimony, but likely nowhere near the level investors are positioning for a hawkish retort. But It would be a massive surprise if he departed from his predecessor script and we should expect a Yellen 2.0 delivery.

Fed Powell's testimony to the House Financial Services Committee has been moved up from Wednesday to Tuesday at 10:00 EST

In addition to this news, Bloomberg also confirms that his prepared remarks will be released at 8:30 EST Early release is not uncommon and allows both the markets and Congress to digest the statements,

Powell will then hold his Senate testimony on Wednesday.

There will be subtle nuances for the market to digest the day.While prepared remarks might help to establish how dovish or hawkish Powell is, many traders feel that Senators tend to ask more relevant questions for the market than the House. Therefore, the market might shade Tuesday's remarks with a bit of caution but will react after confirmation from Senate session on Wednesday.

However, given the policy mess Powell has inherited what should be crucial for the USD is how the Fed moves forward with the unenviable task of QE tapering while massive waves of Treasury notes come online. This burdening task should give the Chairman more cause to tow current policy lines while avoiding any hawkish surprises. Regardless, it's clear that most traders are preferring to wait until Powell's ” coming out” to re-engage with USD shorts in size.

Across the pond, ECB President Draghi will deliver his usual testimony to the European Parliament Monday. Softer economic data continues weighing on near-term sentiment, but political considerations dwarf all else.

G-10 Currencies

The British Pound

Most of this mornings focus has been on the pound after Sir Dave Ramsden sees a faster pace on interest rate normalisation. A bit of departure from usual decorum for a centeral banker to lay his cards on the table with regards to interest rates.But perhaps more significant, until now one of the most active doves on the Bank's monetary policy committee (MPC). But The general market drift is to fade GBP rallies into March EU summit given rate expectations are firmly entrenched, and hawkish expectations could leave GBP vulnerable to Brexit headline noise and the recent soft patch in data. So the markets are tentatively fading this morning opening move higher

The Japanese Yen

The Yen traded heavy on Friday, but with everyone watching the intraday support level at 106.60 on a closing basis, the pairs bounced off session lows into the close, finishing the week at 106.90. Although the reappointment of dovish Kuroda should keep YCC tweak rumours at bay, for now, the USDJPY was trading with higher sensitivity to US yields ahead of Powell testimony so it should be interesting to see if this holds true later in the week. But we expect today's session to be more about position prepping ahead of Powell testimony

While the focus is squarely on Jerome Powell this week, but with the recent decoupling of Yen's movements to US 10 year bond yields, the market could be looking for different triggers. While uncertainty over equity market keeps dollar bulls at bay, the USD selling requirements from exporters as we near Japanese fiscal year end and bond funds looking to adjust dollar hedges against the prospect of a broader US dollar sell-off could pressure the USDJPY despite the possibility of higher US interest rates. As we pointed out last week, the supply of dollars to go between 107.50 -90 remains large and while this continues to be the case, USDJPY shorts should stay in favour.

The Euro

It's tough trading the Euro with much conviction these days ahead of the Italian election as the market remains very wary of building longs ahead of the vote. And while the short-term market is favouring the propensity to sell EUR on rallies, the lack of downside break out makes jobbing the Euro even less appealing.

The Australian Dollar

The USD doesn't want to give it up yet, and while the small uptick in quarterly wage growth was encouraging for Aussie bulls, the markets quickly deduced this would not alleviate RBA's concerns. Overall the USD should continue to dominate near-term price action, but the prospects of another equity market wobble should keep topside Aussie momentum in check. But longer term and given the likely hood for dollar weakness to re-emerge as intense focus falls the duelling twin US deficits, interest rate differentials will be a less significant part of the equation, and the Aussie will outperform and a weaker USD narrative alone.

Asia FX

Stronger local FX and stable US treasuries are providing some breathing room for regional investors and providing a bit of a relief rally in equities. On the currency front, there was a rapid unwind of freshly minted US longs as regional capital market returned to form on the softer US yields.

The threat of US trade sanctions was brushed off as more bark than bite and had muted impact on markets

On the tariff and trade front Liu He, the Chief Economic advisor to the Gov and of the most potent advisors in the Politburo will visit Washington sometime between 27th Feb and March 2nd with their primary task of defusing trade agitation

The Malaysian Ringgit

Bonds are consolidating at current levels, but unless there a robust unexpected move in US rates this week, we should expect higher foreign interest as the local bond yields are at some attractive levels. The next MGS auction is Feb 27 where 3.5bioMYR go up for sale. With MGS 10y yields at 4.08 %, so long as US bond market remains in check, the MYR should get a boost from foreign demand given the attractive returns.

Oil prices should remain firm given OPEC's production cut compliance which should continue to provide a boost to the Ringgit's fortunes

The Chinese Yuan

Given the upcoming trade meeting in Washington, the Pboc will be more inclined to temper the RMB complex upside if the USD exhibits any strength this week. But local traders will likely remain in stasis ahead of The National People's Congress (NPC) will start on March 5. Premier Li will present a draft of his work plan for 2018 on March 5, which will be discussed and revised at the NPC.

The Philippine Peso

The current account weakness has been the primary driver of Peso's underperformance a surge in imports, which has led to a widening of the country's trade deficit and helped push the current account into the red. But with the markets more worried about the BSP falling behind the curve, shaving the countries RRR reinforced that sentiment and this has been the primary driver for the last leg of weakness. But with the Philippine central bank call to action last week by selling dollar to curb excessive peso volatility, perhaps the view of a hands-off central bank may be changing.But for those that follow my blog, you should know my long-standing belief when it comes to centeral bank intervention to curb local currency weakness; it accomplishes little more than eroding precious reserves while providing the market with better level to buy the dollar after the broader long USD Macro positions unwind.

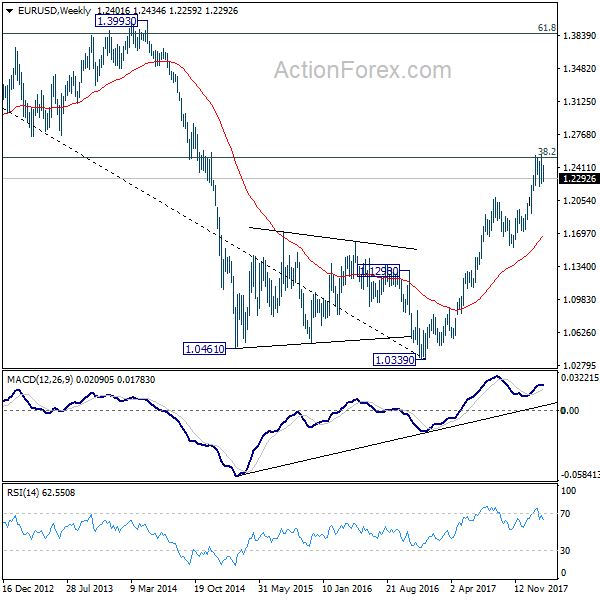

EUR/USD Weekly Outlook

EUR/USD still struggled to sustain above 1.2516 key fibonacci level and stayed in range last week. Initial bias remains neutral this week first. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

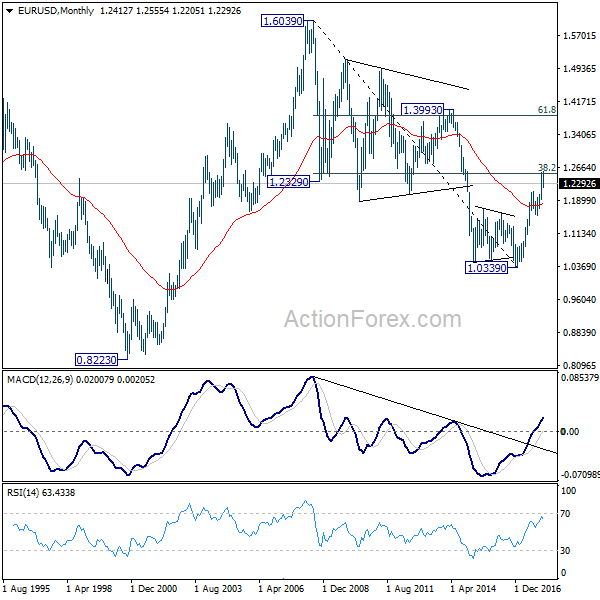

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

In the long term picture, 1.0339 is seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action from 1.0339 is developing into a corrective or impulsive pattern. Reaction to 38.2% retracement of 1.6039 to 1.0339 at 1.2516 will give important clue to the underlying momentum.

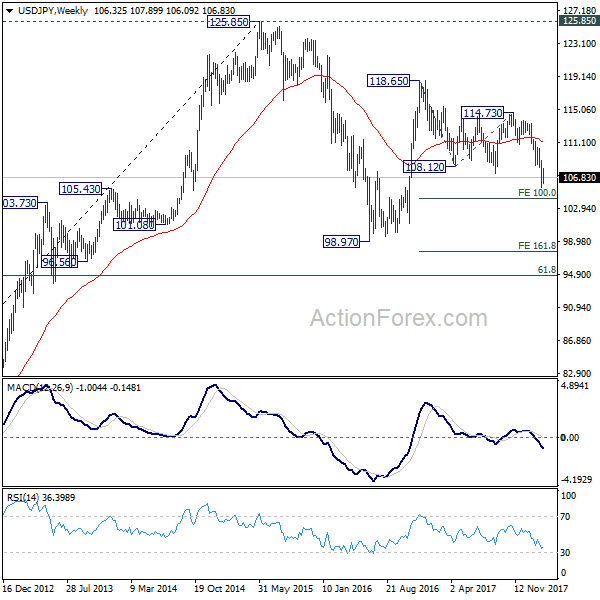

USD/JPY Weekly Outlook

USD/JPY stayed in consolidation above 105.54 last week and outlook is unchanged. Initial bias remains neutral this week first. With 108.27 resistance intact, deeper fall is expected. On the downside, break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

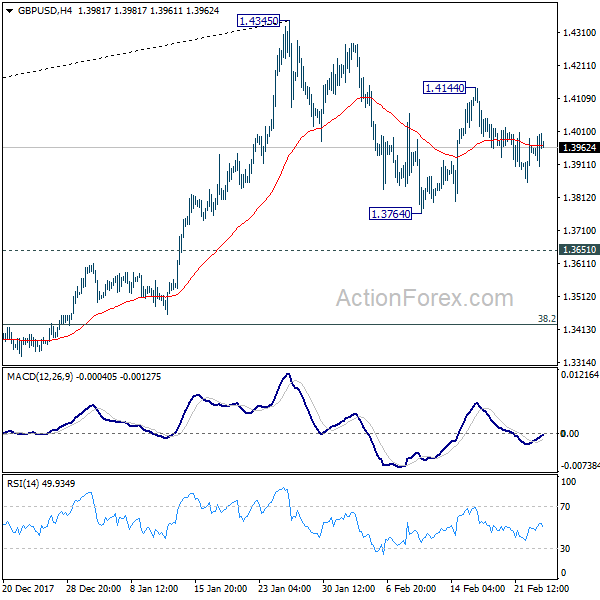

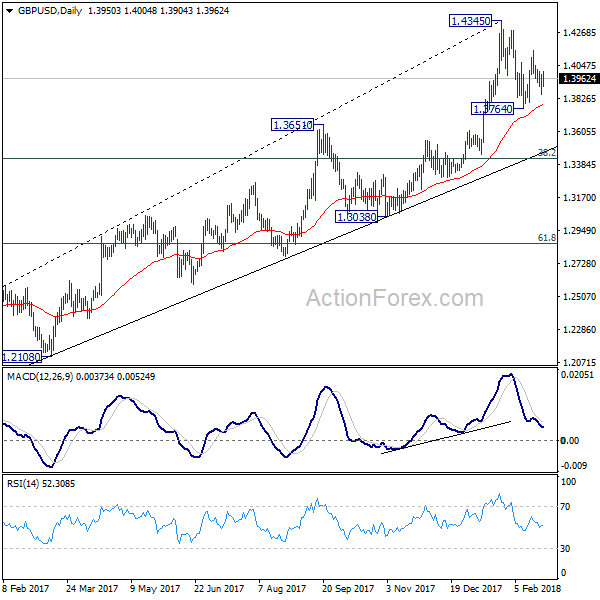

GBP/USD Weekly Outlook

GBP/USD stayed in range below 1.4144 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, break of 1.4144 will extend the rebound from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

In the longer term picture, rise from 1.1946 should at least be correcting the whole long term down trend form 2.1161 and should target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. It too early to tell if it's developing into a long term up trend. We'll monitor the upside momentum and reaction to 1.5466 to decide later.