Sample Category Title

Summary 2/26 – 3/2

Monday, Feb 26, 2018

[php_everywhere] [/php_everywhere]

Tuesday, Feb 27, 2018

[php_everywhere] [/php_everywhere]

Wednesday, Feb 28, 2018

[php_everywhere] [/php_everywhere]

Thursday, Mar 1, 2018

[php_everywhere] [/php_everywhere]

Friday, Mar 2, 2018

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Lite On Economic Data, Heavy on Treasury Supply

U.S. Review

Lite On Economic Data, Heavy on Treasury Supply

- Existing home sales fell 3.2 percent in January following a 2.8 percent decline in December. Tight supply continues to play a role in holding back sales.

- The Conference Board's Leading Economic Index rose 1.0 percent in January following a 0.6 percent rise in December. The measure continued to support the case for continued robust GDP growth.

- The big story in Treasury markets this week was a sizable pickup in gross Treasury issuance. With larger budget deficits on the horizon, Treasury yields continue to move higher.

Lite On Economic Data, Heavy on Treasury Supply

It was a very light week for economic data, but the continued upward movement in Treasury yields has continued to dominate markets' attention. On the economic front, existing home sales tumbled again in January as a tight supply of existing homes held back sales. The Leading Economic Index posted another solid gain in January supporting our forecast for ongoing robust economic growth in the quarters ahead.

Existing home sales disappointed again in January, falling 3.2 percent to a 5.38-million unit pace with sales declining in all four regions of the country. The sluggish pace of existing home sales is tied to the fact that supply remains historically low. The inventory of existing homes on the market rose in January but remains 9.5 percent below last year's level. Existing home prices have continued to rise in light of the tight supply story and are now up 5.8 percent on a year-over-year basis. Even with the current tight supply situation and rising prices, we expect existing home sales to accelerate this year to a 5.65-million unit pace in 2018.

A 1.0 percent rise in the Leading Economic Index (LEI) in January marked the fourth consecutive month of increases in the index. The largest contributors to the headline reading were the interest rate spread, as yields moved higher for the month, and the Institute for Supply Management's new orders component. The solid LEI readings suggest that quarterly annualized GDP growth should continue in the 2.0-3.0 percent range over the first half of this year.

The story of higher Treasury yields has in part been driven by the recent barrage of news related to Treasury supply. Besides the passage of the $1.5 trillion tax package on December 20th of last year, there have been a number of other catalysts on the Treasury supply front that have played a role in moving yields higher. Many of these factors are related to an expected pickup in Treasury supply coming online at the same time that global demand for U.S. Treasuries has begun to wane. The first of these supply signals was the Quarterly Refunding Announcement (QRA) on January 31st which indicated that the Department of the Treasury intended to increase auction sizes for the two-year and three-year note by $2 billion per month, the five-year, seven-year and 10-year notes and 30-year bonds by $1 billion in order to service larger budget deficits and the reduction in reinvestments in the Federal Reserve's portfolio. Relative to market expectations the QRA put more weight on new issuance on the back-end of the yield curve. In addition, the Treasury signaled its intention to stabilize the weighted-average maturity of outstanding Treasury securities which implied that future front-end Treasury issuance would need to be balanced by issuing more longer-dated securities. The next wave to hit Treasury yields was the bi-partisan budget deal that passed on February 9th which will result in even larger budget deficits in the coming quarters. The same bi-partisan budget deal also suspended the debt ceiling until March 2019 which allowed the Treasury to begin replenishing its operating cash balance. Taken together these legislative actions and the resulting supply increases suggest some upside risks to our forecast for $1.126 trillion in net Treasury issuance this calendar year.

U.S. Outlook

New Home Sales • Monday

New home sales slipped in December to a 625K-unit pace, a drop of 9.3 percent from November. The end-of-year slip largely reflected a correction from October and November, which spiked following the hurricanes this summer. The South, which was impacted by storms, was behind much of the volatility. The lower sales volume during winter months makes for exaggerated movements in the seasonally adjusted readings.

Continued strengthening in the underlying domestic economy has fueled demand for home sales. Inventory of existing home sales remains very tight, so demand for new homes is elevated. The very positive readings in surveys of home builders' confidence supports the notion that sales in 2018 will be strong. Higher interest rates and changes in the tax law, however, may take a bite from the momentum, though the impact will likely be marginal.

Previous: 625K Wells Fargo: 665K Consensus: 650K

ISM Manufacturing • Thursday

The ISM manufacturing index showed the expansion in factory activity continued in the first month of 2018. The index was a strong 59.1 in January, slightly down from December but still among the highest readings of the cycle. Indices for production and new orders slipped very slightly but were still in comfortable expansion territory. Other components pointed to an uptick in backlogs and supplier delivery, which also shows a solid pipeline of future activity going into Q1.

Factories are benefitting from the strong global demand, evidenced by a continued climb in the new export orders reading which is now tied with its cycle high first hit in 2010. Manufacturers are noting greater price pressure, which reinforces our view that inflation is firming to a trend that supports further tightening by the Fed.

Previous: 59.1 Wells Fargo: 58.1 Consensus: 58.6

Personal Income and Spending • Thursday

Income and spending growth were both on a positive trajectory at the end of the year, each posting a 0.4 percent increase during the month. Income growth has been robust in recent months, driven by rising wages and salaries. The job market continues to expand even as the unemployment rate drifts lower. Wages and salaries were up 0.5 percent in December, helping to push disposable income up by 0.3 percent. Wage and salary growth likely continued in January, as evidenced by that month's jobs report. Inflation as measured by the PCE deflator was benign, trimming 0.1 percentage point.

Real personal spending growth outpaced real disposable income growth in December, as consumers' savings rate drifted to a new cycle low. Consumers continue to finance consumption with a lower savings rate, which is a testament to consumers' optimism about the economic outlook and future income gains.

Previous: 0.4% & 0.4% Wells Fargo: 0.4% & 0.2% Consensus: 0.3% & 0.2%

Global Review

Weighing Their Next Moves, Central Banks Eye the Data

- In South America this week, data from the Brazilian central bank showed the economy strengthening in December. Taking a three-month moving average, the economic activity index is growing at its fastest year-ago pace in nearly four years.

- Weekly earnings growth in the United Kingdom picked up slightly to end 2017, but employment growth was slower-thanexpected and the unemployment rate ticked higher.

- Inflation data for Japan and Canada showed a gradual firming in price growth in January. December retail sales in Canada were a dud, however, with much of the weakness concentrated in housing-related sectors.

Weighing Their Next Moves, Central Banks Eye the Data

In South America this week, data from the Brazilian central bank showed the economy strengthening to end 2017. The central bank's economic activity index rose 1.4 percent over the month, topping the Bloomberg consensus. Taking a three-month moving average, the index is growing at its fastest year-ago pace in nearly four years, when the descent into recession began. A stronger global economy and a commitment by the central bank to reduce interest rates have helped drive positive momentum for the Brazilian economy. The main policy rate declined to 7.0 percent in December, a 725 basis point reduction since October 2016. Brazil will report its Q4 GDP figures on March 1st.

The U.K. labor market gave off mixed signals this week, as average weekly earnings growth pick up slightly at the end of last year (middle chart). The unemployment rate ticked higher from 4.3 percent to 4.4 percent, however, as employment growth over the October-December period disappointed, rising by 88,000 jobs relative to expectations for a gain nearly twice that size. The Bank of England noted in its most recent policy statement that the U.K. economy "has only a very limited degree of slack," and slowing job gains and rising wages would be consistent with minimal spare capacity in the labor market. As we have seen throughout the developed world this cycle, however, pay gains have been slow to materialize in the face of low unemployment. Though this week's strengthening in wage growth is encouraging, the lack of a truly robust print suggests the Bank of England will remain in wait and see mode for now as it weighs another rate hike.

Inflation data for Japan and Canada showed a gradual firming in price growth in January. The national CPI rose 1.4 percent in Japan on a year-over-year basis, up from 1.0 percent in December. Excluding fresh food and energy, CPI inflation rose 0.1 percentage point to 0.4 percent. Though far from mission accomplished for the Bank of Japan, this week's print brings core inflation up to its fastest pace in the past 18 months. In Canada, headline CPI inflation slowed slightly from December's pace, but by less than the Bloomberg consensus expected. Core inflation strengthened/held steady depending on which of three reported measures considered (bottom chart). On balance, however, the higher-than-expected print suggests some modest building price pressures in Canada.

Data on retail sales in the Canadian economy were also released this week, with a largely underwhelming result. Sales fell by 0.8 percent in December, a much larger decline than the 0.1 percent fall forecasted by the Bloomberg consensus. Housingrelated sectors saw some of the largest declines, with furniture & home furnishing sales falling 3.9 percent in December and electronics/appliance stores sales declining 9.1 percent in December. Building material sales were flat in the month. Some of this weakness was due to strength in October/November, and seasonal adjustment factors may have influenced these colder weather months. That said, given the concerns surrounding the hot Canadian housing market, sales in these sectors will bear close watching in the months ahead.

Global Outlook

China Manufacturing PMI • Tuesday

Although Chinese manufacturing production has remained in expansion territory over the past couple of years, it continues to be relatively weak. According to the national manufacturing PMI as well as the Caixin manufacturing PMI index, manufacturing production is not showing signs of breaking out anytime soon.

On Tuesday, we will have a chance to look at the national manufacturing PMI for the second month of the year. Analysts are expecting it to come in a bit lower than the January print, but for it to remain above the 50 demarcation level.

On Wednesday we will also get the Caixin manufacturing index, which is also expected to come in a bit lower than the January print. Clearly, neither index will move the market if they come in as expected as the country's economy continues to slowly adjust to a lower, and sustainable, rate of growth.

Previous: 51.3 Consensus: 51.2

U.K. Manufacturing PMI • Thursday

The U.K. manufacturing sector has been expanding since early 2016 and analysts are expecting this trend to continue with the February number expected to be higher than January's 55.3 reading. The U.K. manufacturing sector is not alone in this strength as many developed economies, including the United States, have demonstrated robust performance for the manufacturing sector as the global economy continues to expand.

On Tuesday of next week we will also have a chance to look at the GfK consumer confidence index for February. The index has been on a downward trend since mid-2015 and recorded a value of -9 in January. However, the -9 reading was an improvement from the prior month so a continuation of this trend will definitely be positive news for the U.K. economy even if the number remains in negative territory.

Previous: 55.3 Consensus: 55.0

Brazil Q4 GDP • Thursday

Brazil is scheduled to release Q4 as well as whole-year 2017 GDP results on Friday and we expect the economy to have continued to slowly recover. Our forecast for the whole of 2017 is 1.0 percent growth, which is not great but markedly better than the economy's performance over the past two years.

Last week we had a peek at how the GDP release may look as Brazil released the monthly economic activity index which showed the economy to have increased also by 1.0 percent. This means that economic growth for the last quarter of the year is expected to come in a bit higher than 2 percent on a year-over-year basis. Analysts have bumped up economic growth expectations for Brazil for this year and for 2019, so the release will enable us to determine which sectors may be leading this relatively strong recovery after so many years in the red. Our take is that both domestic demand and external demand will continue to lead.

Previous: 1.4% Wells Fargo: 1.9% Consensus: 2.8% (Year-over-Year)

Point of View

Interest Rate Watch

When Inflation Models Don't Work

January meeting minutes showed Fed officials were a bit more upbeat about the near-term outlook for growth following the recently passed tax bill, although most members continued to advocate for only a gradual pace of tightening. While the committee generally agreed that inflation would move up over the next couple of years, members were split about the timing and whether the near-term risk was that inflation would soon overshoot the Fed's 2 percent goal or continue to fall short.

The persistent shortfall of inflation from the FOMC's target in recent years led to a staff briefing to review commonly used models of inflation. The discussion focused on two channels of inflation that have long held sway over policymakers—resource utilization and inflation expectations.

Traditional theory suggests that when resources become relatively scarce, price pressures follow. Yet, research presented by Fed staff highlighted the difficulty in measuring the magnitude and timing of slack on inflation. Making forecasting all the more difficult is that the relationship between slack and inflation appears to be nonlinear. In other words, inflation picks up more meaningfully once a certain threshold is crossed—but there is tremendous uncertainty over where that threshold lies.

Inflation expectations have been an important factor in forecasting given their role in businesses' decisions to change prices and labor's demand for wages. Steady inflation expectations make the FOMC's goal of "stable prices" easier, but expectations look too anchored in recent years. Through cyclical fluctuations, the trend in inflation has been stable at a little less than two percent, suggesting the Fed may need to un-anchor expectations if they are to help reach the Fed's 2 percent goal.

All told, the discussion highlights that policymakers are still struggling to understand the stubbornly low inflation environment of recent years. Without a firm grasp of what drives one of their two mandates, the current path outlined for the fed funds rate could change meaningfully as inflation developments unfold.

Credit Market Insights

Global Household Leverage Rising

Earlier this week, we released a report examining rising household debt and debt servicing ratios (DSR), and if this should be cause for concern in the global economy as many central banks normalize policy (Rising Household Leverage: Should We Be Worried?). In our view, rising household debt and DSRs is not a cause for concern of global recession.

Household debt-to-GDP has risen to 75 percent in advanced economies, up from just 60 percent at the turn of the century. However, this growth has not been broad based, with countries such as Norway, Canada and Korea increasing more than 20 percent, while the United States and Spain have each decreased by about the same magnitude. As global central banks are shifting towards more hawkish policy, the cost of debt will rise, which could cut into consumer spending. However, the significant decline in global interest rates since 2008 means most advanced economies have room to grow until surpassing prior DSR levels. Countries with the highest sensitivity of their DSR to interest rates, such as Denmark, Australia, Norway and Portugal have variable rate debt structures, whereas the United States, with low sensitivity, typically relies on fixed.

In all, rising household leverage in the midst of a reversal of accommodative global central bank policy should not sound the alarm for global recession, at least not at this time. It is more likely that this issue will be contained to individual nations.

Topic of the Week

Americans & Housing According to the 2016 SCF

Homeownership among Americans today remains well below peak levels seen in 2004. According to the results of the 2016 Survey of Consumer Finances (SCF), only 63.7 percent of all U.S. families owned a home in 2016, down from 65.3 percent for the 2013 survey and from the all-time high of roughly 69 percent during the 2004 survey (top graph). Meanwhile, both the median and the mean value of homes for families with holdings were reported to still be recovering from the heights that existed prior to the Great Recession.

In specifically addressing the survey results pertaining to the evolution of homeownership rates, we evaluate the rate of homeownership by reviewing the different segmentations (either by income, age cohort, family structure, or by education) that the survey has utilized in quantifying overall housing market conditions.

We find that, according to the SCF, it is clear that no matter how we segment and assess American families, families continued to shy away from owning a home until 2016. These subdued levels of homeownership since the Great Recession are perhaps a lingering consequence of not only the run-up, but, more fundamentally, of the collapse in the housing market. As the next (2019) SCF will not be published until 2021, we will review additional indicators and try to assess the current consumer view in its relation to the housing market and particularly to the homeownership rate.

However, despite the continuous decline seen in the U.S. homeownership rate since just before the Great Recession, it appears that the rate of homeownership has finally turned a corner since 2016 (bottom graph). As home prices have continued to move higher, and homeownership continues to be a big component of many Americans net worth, we suspect that the homeownership rate will continue to rise slowly over the next several years.

The Weekly Bottom Line: More Rate Hikes Incoming

U.S. Highlights

- A holiday-shortened trading week light in economic data left markets to focus on communications from the Federal Reserve.

- U.S. existing home sales slumped in January, beleaguered by low inventories and deteriorating affordability.

- The FOMC minutes revealed a Fed busy revising up economic projections, suggesting that further gradual policy firming is warranted.

Canadian Highlights

- The December 2017 data continued to disappoint, with declines in retail and wholesale trade joining earlier softness in trade and manufacturing.

- Real GDP in 2017 as a whole likely saw a robust 2.9% expansion, with a respectable 2.0% pace of growth expected for Q4. The December softness and weaker housing market activity in January suggest a further deceleration is likely, leaving 2018 to start-off on a softer note.

- Noise can mask the trend, which can hardly be defined by a few months' data. Prudence in the face of domestic and external risks suggests that the Bank of Canada is likely to stand pat until mid-year, when it is better able to assess the underlying Canadian growth trend.

U.S. - More Rate Hikes Incoming

A holiday-shortened trading week coupled with light data left markets with just the minutes from the January FOMC meeting and the words of wisdom from a slew of Federal Reserve speakers this week to digest.

Existing home sales for January revealed a market that is still beleaguered by low inventory, which exacerbates deteriorating housing affordability in many U.S. cities. January's decline in existing home sales was broad-based, and concentrated in the larger single-family segment (Chart 1). Unsurprisingly, rising prices and borrowing costs are deterring first-time buyers from buying, as they accounted for only 29% of sales in January, down from 33% a year ago. Looking ahead, job gains and an optimistic outlook for after-tax earnings growth should support a rebound in home sales. What's more, housing starts ticked up in January, possibly providing some respite for buyers particularly in those markets with a low supply of existing homes.

Fed speakers this week remained broadly optimistic about the outlook for the economy, while also revealing very little news about the number of rate hikes this year. In the December Summary of Economic Projections (SEP), the FOMC communicated that it would likely raise rates three times. Since then, the U.S. Congress approved of a massive tax reform package, and just a few weeks ago an additional package of spending that is expected to provide a substantial lift to U.S. growth (Chart 2; read our report on U.S. fiscal stimulus).

The firmer U.S. growth outlook has raised questions about how tolerant a Powell-led Fed would be of above-target inflation. Perhaps one of the most surprising admissions this week was from FRB Philadelphia President Harker, who is not a voting member of the FOMC but a contributor to the quarterly economic projections. He mentioned in a speech on Wednesday that he was comfortable penciling in just two rate hikes for this year, but may adjust if the evolution of the data requires it. This is somewhat counter to what most economic models would suggest, and even an often pessimistic market has moved to price-in about three rate hikes for 2018. Some economic forecasters have penciled in four rate hikes for 2018 after fiscal stimulus was announced.

Nonetheless, the FOMC minutes from its January meeting revealed a Fed busy revising up economic projections for the U.S. economy, and therefore confident that further gradual policy firming is warranted. While there is a lot of room for interpretation on what "further" implies, it's safe to conclude that rates will rise this year. To be clear, we have stuck with our view from this past December that the economic outlook and balance of risks are consistent with three rate hikes by the Fed this year. However, the additional stimulus from the recently announced fiscal program pushes up our rate hikes for 2019 to three from two. This places the fed funds rate at 3.0% at the end of 2019, and about 20 basis points above the FOMC's longer-run expectation.

Canada - Clouds on the Horizon?

This week delivered the last few 'puzzle pieces' ahead of next week's GDP report for the final quarter of 2017. Capturing most of the attention was the fairly weak retail sales report, which saw both the dollar value and volume of transactions decline in December (Chart 1). Retail sales joined a generally middling slate of December data: wholesale trade, also reported this week, was down slightly, joining soft trade figures and a mediocre manufacturing report (both released earlier in the month).

In many cases, notably manufacturing and retail sales, December's weakness comes after stronger performances earlier in the quarter, and in the case of the latter, it is possible that shifts in holiday spending habits (towards Black Friday/Cyber Monday) may not be fully reflected in the seasonally adjusted data. It also bookended a great year overall – 2017 was the best year for retail sales growth since 1997.

All this is to say that fourth quarter growth is likely to come in at a respectable pace of about 2% (q/q annualized) that, while disappointing our early expectations, is still above Canada's underlying trend. Indeed, growth for 2017 as a whole is likely to mark a 2.9% pace of expansion, its best performance since 2014. This robust performance can be seen in the Bank of Canada's measures of underlying price pressures (Chart 2). Core inflation has both trended higher in the back half of last year, and the range of measures have tightened up, suggesting that the Bank of Canada's three rate hikes were likely necessary for the achievement of their 2% inflation target.

Of particular note in the inflation data was the seeming impact of minimum-wage hikes. While they may not have had a significant impact on the aggregate wage data (yet), these hikes made themselves felt in key categories that tend to be associated with minimum wage employment, such as food purchased from restaurants and child care/housekeeping.

Looking ahead, the robust growth of 2017 is likely to fade into the rear-view mirror. December's soft showing may not have a major impact on Q4, but suggests a softer start to 2018. To be clear, one month hardly makes a trend, but the softened momentum in the December data comes alongside a significant weakening of housing activity in January (See commentary). As expressed in a recent report, the regulatory changes behind January's weakness are not likely to drive Canadian home markets into a tailspin, but near-term softness is likely to make itself felt in the economy more broadly.

What does all of this mean for the Bank of Canada? At the risk of sounding like a broken record, likely not too much. Near-term growth appears likely to disappoint their expectations, but a continued rising pace of inflation, particularly in their core measures, will provide re-assurance that economic slack has been absorbed and historically low interest rates are no longer required. With risks abounding, both domestic and external, a near-term 'wait and see' approach seems most likely. By mid-year, Governor Poloz and company should have a clearer sense of the trend lying beneath recent near-term noise, and feel comfortable that the Canadian economy can withstand another policy interest rate increase.

U.S.: Upcoming Key Economic Releases

U.S. Personal Income & Spending - January

Release Date: March 1, 2018

Previous Result: Income 0.4% m/m, Spending 0.4% m/m

TD Forecast: Income 0.2% m/m, Spending 0.2% m/m

Consensus: Income 0.3% m/m, Spending 0.2% m/m

Headline PCE inflation is expected to slip back to 1.6% y/y in January, reflecting a 0.3% m/m rise in prices. The rise reflects higher gasoline prices along with a solid firming in the core. However, we expect core PCE to undershoot the strength recorded in the core CPI and register a 0.2% m/m increase (vs 0.3% m/m in the CPI). This is largely due to the healthcare services component, which we expect to post a more modest uptick than in the CPI report. PCE healthcare prices more closely follow producer level prices, and while the latter rose on balance, the increase was concentrated mainly in hospital outpatient care services. As a result we expect core PCE inflation to be stable at 1.5% y/y.

Nominal PCE (personal spending) is expected to rise 0.2% in January, implying a 0.1% decline in real spending. The weak footing in Q1 would be consistent with real PCE tracking near a relatively modest 2.0%. We expect January spending gains to be driven by services, with a neutral contribution from nondurables and a decline in durable goods spending. We also expect a soft 0.2% increase in December personal income.

Canada: Upcoming Key Economic Releases

Canadian Real GDP - Q4 & December

Release Date: March 2, 2018

Result: 1.7% q/q ann, 0.4% m/m

TD Forecast: 2.0% q/q ann, 0.1% m/m

Consensus: 2.1% q/q ann, 0.1% m/m

The robust start to 2017 is expected to have given way to a more sustainable close, with fourth quarter GDP growth of 2.0% (q/q, annualized) expected. Net trade is likely to again subtract from growth due to a November surge in goods imports that far outpaced more meagre export gains. Consumer spending should remain healthy, supported by solid aggregate income gains and decent retail sales volumes early in the quarter. Important but difficult-to-pin-down spending on services is expected to have decelerated somewhat from Q3's 5.3% pace, to 3.6%. Total private investment is expected to remain solid at 2.5%, helped by an expected continuation of business investment (albeit at a relatively more modest 2.7% pace), as well as a pulling-forward of residential activity ahead of January's B-20 underwriting guideline changes.

Industry-level growth is forecast to rise 0.1% in December. Following a number of downbeat data releases, we expect utilities and a short-term boost from real estate to drive growth. Details should reveal a mixed performance in both goods and services, with the former helped by increased utilities output while a pullback in housing starts and softer manufacturing sales will exert a drag on growth. For services, weaker wholesale and retail sales will weigh on the sector as a whole but we expect a larger contribution from real estate as homebuyers try to circumvent new mortgage rules, though this will unwind next month. In addition to the slowdown in housing, the poor handoff from December will create a more challenging growth environment in Q1.

Week Ahead – Markets Look to Powell Testimony for Fed Guidance; Japan and US Data to Dominate

Economic data from Japan and the United States will comprise the bulk of next week's releases. Australia, Canada, the Eurozone and the United Kingdom will also see important data releases. But the main focus will be on Fed Chair Jerome Powell's first semi-annual testimony before Congress. Anxious market participants will be seeking clarity on Fed policy as stock markets are still reeling from the sharp sell-off in early February, while the dollar continues to defy rising US yields by showing no sign of breaking out of its downtrend.

Australian capex figures eyed for GDP clues

Data on capital expenditure due out of Australia for the fourth quarter will be watched on Thursday as it is usually a good indication of GDP growth. Private sector lending numbers for January on Wednesday will also be important.

Over in New Zealand, investors will too get the chance to bet on fourth quarter GDP performance as data on the country's terms of trade are published on Thursday. Monthly trade numbers are also out, due on Monday.

Surprises in the data may cause some limited fluctuations in the local dollars but are unlikely to alter the outlook for interest rates in the respective countries, while in the short term, the greenback and global risk sentiment are bigger drivers for both the aussie and the kiwi.

Loonie looks to Canadian GDP for relief

The Canadian dollar has taken a battering over the past month, tumbling from a 4-month top to a 2-month trough during the period. An anticipated slowdown in economic growth in the final three months of 2017 has been one of the main reasons for the loonie's decline. However, the interest rate outlook could be subject to a dramatic shift on Friday if the fourth quarter GDP figures were to come in above expectations. A weak reading on the other hand could extend the loonie's decline.

Japanese job market to tighten further

Japan will come under the spotlight next week as a number of key economic indicators are due. The first batch of data is out on Wednesday, which will consist of industrial output and retail sales numbers. Industrial output is forecast to drop by 4.2% month-on-month in January – the first contraction in four months. Retail sales during the same period are expected to record annual growth of 2.1%. On Thursday, fourth quarter data on capital expenditure will attract attention as it's a major component of Japanese GDP calculations.

The January jobless numbers and household spending figures will round up the week on Friday. The unemployment rate is forecast to inch down to 2.7% from 2.8%, while the jobs/application ratio is expected to point to further tightening in the labour market, rising to a fresh 44-year high of 1.6%. The Bank of Japan will be looking at the job numbers closely as it is counting on the country's labour shortage to spur wage growth, but with yet no evidence of this, the data is unlikely to generate much reaction from the yen.

Eurozone flash CPI to head lower again

The economic sentiment survey (Tuesday) and flash inflation data (Wednesday) will be the main releases out of the Eurozone in the next seven days, but the highlight could come from ECB President Mario Draghi's testimony before the European Parliament's Economic and Monetary Affairs Committee on Monday. The ECB has so far resisted calls to signal an end to its stimulus program as inflation appears to be trending down again. The preliminary CPI print is expected to confirm this trend with the annual rate of inflation easing from 1.3% to 1.2% in February. Other data to watch out of the Eurozone are Thursday's unemployment rate and Friday's producer prices, both for January. The euro took a bit of a knock over the past week as business confidence gauges for February have so far disappointed. More data misses could extend the single currency's consolidation.

May to outline "way forward" Brexit speech

The UK economic calendar will be a lighter one in the coming week with Markit/CIPS's manufacturing and construction PMIs being the only major data. The manufacturing PMI is due on Thursday and is expected to moderate further in February from 55.3 to 55.0. Friday's construction PMI is forecast for a slight improvement though.

Worse-than-expected figures could pressure the pound, however, investors will likely be more focused on the next instalment of Theresa May's "Road to Brexit" speeches. The Prime Minister is expected to set out the "way forward" for the Brexit negotiations in a speech on Friday. It follows a cabinet meeting this week where senior ministers held talks to resolve their differences over key issues in a bid to form a united front over the government's Brexit strategy.

US data likely to be eclipsed by Powell testimony

There will be a barrage of indicators out of the United States next week as the month comes to an end, but a bigger concern for the markets will be the new Fed Chair's views on the economy. Housing data will comprise a bulk of the data, including new home sales on Monday and pending home sales on Wednesday. On Tuesday, durable goods orders and the advance trade balance for January, as well as the Conference Board's consumer confidence index will be watched. The consumer confidence index is expected to rise to 126.2 in February, moving closer to November's 18-year high.

The second estimate of GDP growth in the fourth quarter is due on Wednesday. The preliminary reading put annualized quarterly growth at 2.6%. This is expected to be revised marginally lower to 2.5%. On Thursday, all eyes will be on the personal consumption expenditures report. Personal income and spending are both forecast for further gains in January, while the Fed's favourite inflation measure, the core PCE price index, is expected to remain unchanged at 1.5% year-on-year in January. Also important on Thursday will be the ISM manufacturing PMI.

The data could get overshadowed however by Jerome Powell's first semi-annual monetary policy testimony before Congress on Tuesday. The hearing comes at a sensitive time for the markets following the recent volatility in equities. With just a few weeks into the job, Powell will need to be careful not to trigger another bond and stock sell-off by sounding too hawkish. The US dollar is also heading for a tricky week as it's modest recovery over the past few days could easily falter if reassuring words from Powell drive down Treasury yields.

Fed Rhetoric to Drive Dollar

US central bank members in full force on Friday

The USD appreciated during the week against major pairs. The currency got a boost from the release of the minutes from the January Federal Open Market Committee (FOMC) meeting. The brief statement was slightly hawkish, but the full notes from the meeting revealed the US central bank upgraded its economic projections from those made in December and expects the 2 percent inflation target to be met in the mid term. The meeting marked the end of the Janet Yellen era at the helm of the Fed, Jerome Powell will chair the central bank with his inaugural testimony in Washington on February 28 at 8:30 am EST.

- Fed speakers and FOMC minutes to make way for inflation data

- Fed Chair Jerome Powell to deliver semiannual monetary policy report

- Canadian Monthly GDP to give full view of 2017 growth

Dollar Gains After Hawkish FOMC Minutes

The EUR/USD lost 0.83 percent during the week. The single currency is trading at 1.2306 after the notes from the European Central Bank (ECB) and the U.S. Federal Reserve policy meetings in January were released. While the Fed added more details to its hawkish statement the ECB continued to signal inflation in the Eurozone is not strong enough to normalize its monetary policies. The governing council is not taking off the table that this could not change soon but are worried about the market's reaction. Communication has been an issue for the ECB and not all the kinks have been worked out as the market expects a reduction in stimulus, but the majority of ECB members see this as premature. Fed Chair Powell will present the Semiannual Monetary Policy Report before the House Financial Services Committee and will take questions. The Fed is expected to lift interest rates at the March Federal Open Market Committee (FOMC) meeting and investors will be following Powell's testimony for clues about the Fed's rate hike path.

European Central Bank (ECB) Mario Draghi will also be active during the week when he testifies before the European Parliament Economic and Monetary Affairs Committee. The EUR has appreciated during the start of the year as European growth expectations could finally be at a point where the ECB feels confident scaling back its stimulus program. With US growth and higher interest rates already priced into the USD the EUR had more upside, but as the ECB hesitates to signal a clear end to its QE program and higher rates in 2018 the single currency could suffer.

Fed members were in full force during the week picking up on the trends set down by the FOMC minutes. Growth projections have improved and fiscal policies are anticipated to have a short term positive effect. The CME FedWatch tool is showing a 83.1 percent probability of a rate hike during the March 21 Fed meeting.

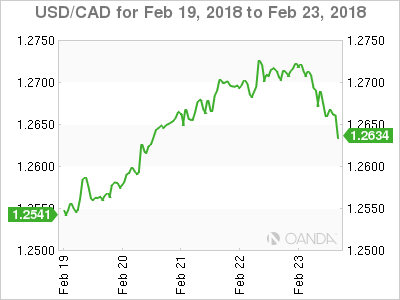

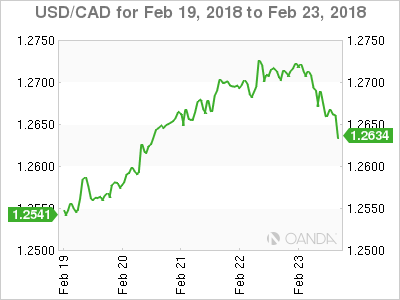

The USD/CAD gained 0.79 percent during the last five trading days. The currency pair is trading at 1.2684 on Friday after the higher than expected consumer price index (CPI) released at 8:30 am EST. Inflation in Canada was 1.7 percent in January a slowdown from the 1.9 percent reading in December, but is still posting to an upward trend in consumer prices. The Bank of Canada (BoC) hiked interest rates three times in 2017 and with inflationary pressures it is expected to hike another three in 2018.

Disappointing retail sales in December and other economic indicators have weighed more heavily on the loonie than the higher oil prices that have remained above $60 per barrel despite the present threat of higher production from Canada, Brazil and the US. Higher inflation provided a breather for the CAD as it regained some ground versus the USD appreciating 0.39 percent, but not enough to end on a positive note for the week. NAFTA uncertainty still weighs heavily on the Canadian currency with the trade pact renegotiation still with little to show for it as the end of the talks is fast approaching and with elections in Mexico and the United States the trade deal could be further politicized further complicating a three way agreement this year. Negotiators being the second to last round of talks in Mexico city on Feb 25 until March 5.

Oil prices rose in weekly trading for a second week in a row. West Texas Intermediate is trading at $63.69 on Friday. Weekly inventories in the US surprised with a a drawdown of 1.6 million barrels when the forecast called for a rise in crude stocks of 1.9 million barrels. The main factor keeping prices at current levels is the anticipated ramp up in production from US shale companies. Demand for the black stuff has not kept up with supply which is what caused the commodity prices to free fall three years ago until the Organization of the Petroleum Exporting Countries (OPEC) got together with major producers to sign an agreement to limit production. The timing has not worked out for US shale with weather factors holding back higher rig counts.

The softer dollar in the beginning of 2018 also contributed to higher oil prices, but as the greenback is finding its feet as fiscal and monetary policy aligns for higher growth it could also weigh on the price of crude.

Market events to watch this week:

Monday, February 26

- 9:00am EUR ECB President Draghi Speaks

Tuesday, February 27

- 8:30am USD Core Durable Goods Orders m/m

- 10:00am USD CB Consumer Confidence

- 7:00pm NZD ANZ Business Confidence

Wednesday, February 28

- 8:30am USD Fed Chair Powell Testifies

- 8:30am USD Prelim GDP q/q

- 10:30am USD Crude Oil Inventories

- 7:30pm AUD Private Capital Expenditure q/q

Thursday, March 1

- 4:30am GBP Manufacturing PMI

- 10:00am USD ISM Manufacturing PMI

Friday, Mar 2

- Tentative GBP Prime Minister May Speaks

- 4:30am GBP Construction PMI

- 8:30am CAD GDP m/m

*All times EST

Weekly Focus: Global Growth Set to Remain Strong but Signs Acceleration Phase is Over

Market movers ahead

- In the US, January PCE inflation figures are due next week and we have several speeches by FOMC members in the calendar, along with the Fed Chair Jerome Powell hearing before the Financial Services Committee.

- In the euro area, February HICP inflation is due for release on Wednesday. We do not believe underlying wage pressure will be enough to lift core inflation much higher than the 1.0-1.2% level in 2018, despite the strong growth momentum.

- Other global data releases to watch are US ISM manufacturing and core capex figures, UK and Chinese PMIs and Japanese industrial production.

- In Sweden, we get the first estimate of Q4 GDP. Q4 is probably too soon to see the negative effects of the housing market and we estimate GDP rose by 0.7% q/q and 3.2% y/y.

Global macro and market themes

- European PMIs support our view that the acceleration phase is over. Global growth is set to remain strong, supporting equities.

- Donald Trump is slowly getting more protectionist, with a decision looming on steel and aluminium tariffs/quotas.

- The Fed is more confident on its economic outlook, not more hawkish – at least for now.

- Yields are set to move higher and we target EUR/USD at 1.28 in 12M.