Sample Category Title

Loonie Rallies on Inflation Data

Statistics Canada data this morning showed that headline inflation in Canada slowed last month, while measures of underlying prices strengthened to their highest level in 18-months.

Canada's consumer-price index rose +1.7% y/y in January, following a +1.9% advance in December.

Market expectations were for a +1.5% lift. On a month-over-month basis, prices rose +0.7% in January.

Digging deeper, today's report indicated underlying, or core, inflation strengthened in the month. Underlying prices rose in a range from +1.8% to +1.9%, for an average of +1.83% – the highest level since mid-2016. The average in the previous month was +1.76%.

The 'loonie' is up +0.51% against the U.S dollar, trading atop of C$1.2659. The CAD was trading north of C$1.2712 just before this morning's release.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2667; (P) 1.2709; (R1) 1.2748; More....

Breaching 1.2624 minor support suggests temporary topping at 1.2757. Intraday bias in USD/CAD is turned neutral first. Further rise will remain in favor as long as 1.2450 support holds. Above 1.2757 will target 1.2919 key near term resistance. We'd be cautious on strong resistance from there to limit upside. However, break of 1.2450 will argue that rebound from 1.2246 is completed and turn bias to the downside for this support.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2776), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Canadian Dollar Rebounds after Stronger than Expected CPI

Canadian Dollar rebounds in early US session after stronger than expected inflation data. CPI rose 0.7% mom, 1.7% yoy in January. The annual rate slowed from 1.9% yoy in December but beat expectation of 1.5% yoy. CPI core common accelerated to 1.8% yoy, up from 1.6% yoy. CPI core median was unchanged at 1.9% yoy. CPI core trim slowed to 1.8% yoy, down from 1.9% yoy. Canadian Dollar is now trading as the strongest one for today, and reversed some of earlier losses and be mixed for the week. Elsewhere in the forex markets, Dollar remains the strongest one for the week, followed by Sterling. Kiwi and Aussie are the weakest ones.

UK Prime Minister Theresa May will set out her visions regard post Brexit relationship with EU in a speech next Friday. The announcement came after May and her senior cabinet members met at Chequers to hammer out the position. May's spokesman said that "It was a very positive meeting and a step forward, agreeing the basis of the prime minister's speech on the future relationship." A sticky point is the rights of EU nationals during the transition period. May's proposing of them having fewer rights than those already in the UK prompted furious response from EU. Another point is what kind of trade relationship would UK want to have.

BoE Deputy Governor Dave Ramsden said that productivity growth is weak currently but will improve over the coming years. He emphasized that will be a key factor for monetary policy. He pointed to MPC's view that economy's speed limit is likely to be around 1.5 percent." And, "with very little spare capacity in the economy, even the unusually weak actual growth of around 1.75 percent over the forecast ... is still sufficient to generate excess demand." Ramsden was one of the two MPC members who dissented last November's rate hike.

On the data front, Eurozone CPI was finalized at 1.3% yoy in January, CPI core at 1.0% yoy. German Q4 GDP growth was finalized at 0.6% qoq. New Zealand retail sales rose more than expected by 1.7% qoq in Q4. Japan national CPI core was unchanged at 0.9% yoy in January, corporate service price rose 0.7% yoy.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2667; (P) 1.2709; (R1) 1.2748; More....

Breaching 1.2624 minor support suggests temporary topping at 1.2757. Intraday bias in USD/CAD is turned neutral first. Further rise will remain in favor as long as 1.2450 support holds. Above 1.2757 will target 1.2919 key near term resistance. We'd be cautious on strong resistance from there to limit upside. However, break of 1.2450 will argue that rebound from 1.2246 is completed and turn bias to the downside for this support.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2776), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Ex Inflation Q/Q Q4 | 1.70% | 1.30% | 0.20% | 0.30% |

| 23:30 | JPY | National CPI Core Y/Y Jan | 0.90% | 0.80% | 0.90% | |

| 23:50 | JPY | Corporate Service Price Y/Y Jan | 0.70% | 0.80% | 0.80% | |

| 07:00 | EUR | German GDP Q/Q Q4 F | 0.60% | 0.60% | 0.60% | |

| 10:00 | EUR | Eurozone CPI M/M Jan | -0.90% | -0.90% | 0.40% | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 1.30% | 1.30% | 1.40% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 1.00% | 1.00% | 1.00% | |

| 13:30 | CAD | CPI M/M Jan | 0.70% | 0.50% | -0.40% | |

| 13:30 | CAD | CPI Y/Y Jan | 1.70% | 1.50% | 1.90% | |

| 13:30 | CAD | CPI Core - Common Y/Y Jan | 1.80% | 1.60% | ||

| 13:30 | CAD | CPI Core - Median Y/Y Jan | 1.90% | 1.90% | ||

| 13:30 | CAD | CPI Core - Trim Y/Y Jan | 1.80% | 1.90% |

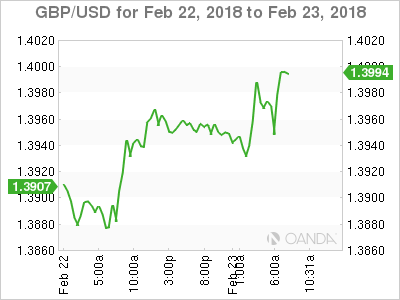

GBPUSD Bullish, Follows Through Higher

GBPUSD: The pair backed off lower prices to close higher on Thursday and was seen following through during Friday trading session. Support lies at the 1.3950 level where a break will turn attention to the 1.3900 level. Further down, support lies at the 1.3850 level. Below here will set the stage for more weakness towards the 1.3800 level. Conversely, resistance stands at the 1.4050 levels with a turn above here allowing more strength to build up towards the 1.4100 level. Further out, resistance resides at the 1.4150 level followed by the 1.4200 level. On the whole, GBPUSD looks to correct further higher on price halt.

Euro Pressured by Political Uncertainties; Canadian Inflation in Focus

Here are the latest developments in global markets:

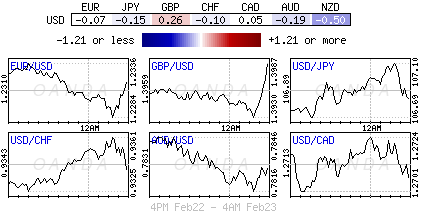

FOREX: Euro/dollar was under pressure during early European trading, trading lower at 1.2302 (-0.22%) as uncertainties in the political front loomed in the background ahead of the Italian general election and the German's polls on whether Merkel's Conservatives will formally lead the government under a coalition agreement with their former coalition partners, the SPD. Pound/dollar jumped to an intra-day high of 1.3993 (+0.14%). on hopes that the Bank of England would raise interest rates faster than expected according to the BoE Chief Economist, Andy Haldane's hawkish comments on Wednesday. Euro/pound crawled down to 0.8818 (-0.18%). The dollar index eased to 89.89, while the dollar/yen edged down to 106.88 but both remained up on the day, gaining 0.18% and 0.14% respectively. January's FOMC meeting minutes released on Wednesday indicated that policymakers were sanguine on the US economic performance and that inflation will likely rise further, enhancing the dollar's strength. Aussie/dollar and kiwi/dollar extended their losses towards 0.7812 (-0.47%) and 0.7290 (-0.65%) respectively, being the worst performers among the majors. Dollar/loonie was flat at 1.2710 (+0.03%).

STOCKS: European stocks were steady in early European trading as the strong fluctuations in the market seemed to calm down, while a mixed flow of earnings releases restricted stock movements. The pan-European STOXX 600 was slightly up by 0.03% at 1015 GMT, with the French auto part maker Valeo being the biggest loser among the companies listed in the index as the firm's profits plummeted in the second half of 2017 due to higher material costs and adverse exchange rate movements. However, rising shares in the telecommunication sector were able to offset this loss. The blue-chip Euro STOXX 50 was down by 0.05% driven by weaker healthcare and technology sectors. The Spanish IBEX 35 fell by 0.42% dragged by consumer cyclicals, while the Italian FTSE MIB rose by 0.22% after Telecom Italia chose Goldman Sachs and Swiss Credit to deal with the spin-off of the company which has been an unsolved issue for almost a decade. The German DAX 30 inched up by 0.01% and the UK's FTSE 100 declined by 0.30%. US stock futures were in the green.

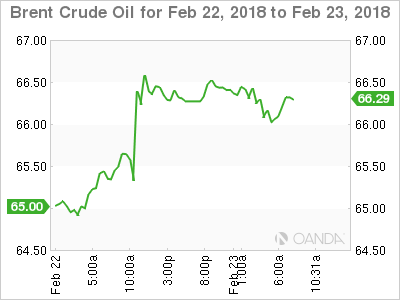

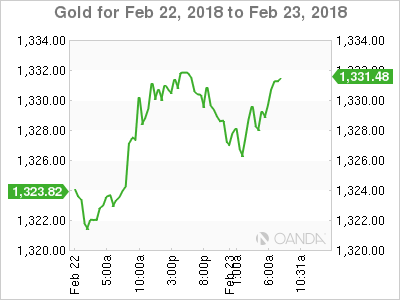

COMMODITIES: Oil prices were on the backfoot after the latest EIA report fueled concerns that OPEC's efforts to curb supply would get harmed by rises in US oil production. Particularly the EIA figures indicated that the US oil production hit a record high in monthly terms while the US oil exports jumped near to all-time highs. WTI crude declined by 0.66% to $62.39 per barrel and Brent retreated by 0.71% to $65.94/barrel. In precious metals, gold fell by 0.18% to $1329/ounce.

Day ahead: Canada releases inflation figures

At 1330 GMT, Canada will hand out data on consumer prices for the month of January, with analysts projecting the headline CPI to slip to 1.4% y/y after previously rising by 1.9%, holding within the Bank of Canada's target range of 1.0% – 3.0%. On the monthly basis, however, the gauge is expected to bounce by 0.4% following a decline by the same proportion in the preceding month. Measures of core inflation (that exclude volatility) preferred by the Bank of Canada, involving the trimmed-CPI, the median-CPI, and the common-CPI will be also in focus.

In oil markets, investors will be waiting for the Baker Hughes oil rig counts to give further clues on future US oil production at 1800 GMT. Note that, the number of active drilling rigs was rising the past four weeks, pressuring oil prices.

In terms of public speeches, the Bank of England's Deputy Governor, David Ramsden, will take part in a panel discussion on productivity and economic rebalancing at 1200 GMT. In the US, the New York Fed President, William Dudley (1515 GMT), the Boston Fed Governor, Eric Rosengren (1515 GMT), and the Cleveland Fed President, Loretta Mester (1830 GMT), will discuss on monetary policy before the 2018 US Monetary Policy Forum. The ECB board member, Benoit Coeure, will also join the event, giving a speech at 1830 GMT. Meanwhile, the president of the European Commission, Jean Claude Junker and the president of the European Council, Donald Tusk will be holding a news conference at 1700 GMT after the European Union heads of state and governments meet for an informal summit in Brussels.

In other areas of interest, Brexit news would attract attention the following days after the media reported that the UK Prime Minister, Theresa May backed those ministers who wanted the UK to take back control of its own regulations during yesterday's eight-hour meeting with the Cabinet. Next week, May will meet EU leaders, probably giving a clearer picture of the UK's stance over the country's partnership with the block.

GBPUSD Still Struggling With 1.4000 Level

The British pound has quickly given back intraday gains against the U.S dollar, as buyers again failed to move price-action above the key 1.4000 level this morning. Sterling earlier traded as high as 1.3994, before strong technical selling saw the pair dropping sharply to the 1.3904 technical level. Price-action now trades back above the pivotal 1.3938 level, with Brexit news and the U.S dollar index now driving the current trading sentiment surrounding the GBPUSD pair.

The GBPUSD pair only retains an intraday bullish bias whilst trading above the 1.3938 level, key intraday resistance is now found at the 1.3994 and 1.4008 levels.

Should GBPUSD price-action hold below the 1.3938 level on a higher-time frame basis, a further decline towards the 1.3901 and 1.3873 levels seems likely.

EURUSD Back Testing Key Support at 1.2292

The euro is losing bullish momentum against the greenback after earlier rallying to the 1.2351 level, as the U.S dollar index starts to move higher again. The EURUSD pair is currently trading back towards the key 1.2292 technical level, with sellers regaining control from the 1.2321 level during the European trading session. The U.S dollar index and volatile moves in the U.S treasury market remain the main drivers of EURUSD price-action on Friday.

The EURUSD pair remains under bearish pressures while trading below the 1.2292 technical level, further losses towards the 1.2259 and 1.2232 levels appear likely.

Should EURUSD price-action move back above the 1.2292 level, key intraday resistance is found at the 1.2310 and 1.2351 levels.

Fed Rhetoric to Dictate Dollar Direction

Friday February 23: Five things the markets are talking about

Ahead of the U.S open, Euro equities are struggling for direction after a positive Asian session as the market debates the outlook for central banks 'normalizing' their policies.

Euro bonds have gained along with Treasuries, while the dollar steadies after yesterday's drop.

With no U.S data on the docket today, the market will shift its attention towards a plethora of Fed speakers doing the rounds.

First up will be New York Fed Chief, William Dudley, who kicks off proceedings at 10:00 am EDT as he addresses the "Monetary Policy Forum" in Chicago.

Note: Dudley is making his final rounds of appearances before his retirement.

Appearing at the same conference shall be Boston Fed President Rosengren, who is one of the Fed's more "dovish" members, but who is not a "voter" this year.

Ms. Mester, the President of the Cleveland Fed, will be speaking at the same conference this afternoon at 1:00 PM EDT. She is a "voter" this year and a "hawk."

Finally, Mr. Williams, the President of the San Francisco Fed, a "voter" on the FOMC this year and generally considered a "moderate," will be speaking to a group on the west coast on the economy and monetary policy at 03:40 pm EDT.

1. Stocks gain in thin trading

In Japan, stocks rallied in light trade as receding fears of more aggressive U.S interest rate hikes boosted sentiment. The benchmark Nikkei ended +0.7% higher. For the week, it was up +0.8%.The broader Topix gained +0.8%.

Down-under, Australia's S&P/ASX 200 closed +0.8% higher to cap its best week since Oct. In S. Korea, the Kospi had its best day since Oct. 10 rising +1.5%.

In Hong Kong, stocks rose overnight, capping a holiday-shortened trading week, as main indexes managed to recover much of the damage done during the recent rout. The Hang Seng index rose +1.0%, while the China Enterprises Index gained +1.7%.

In China, shares extended their rebound overnight, on sign's that the Chinese government is once again supporting the stock market. The blue-chip CSI300 index ended up +0.5%, while the Shanghai Composite Index gained +0.6% in a holiday-shortened week. Both indexes have rebounded over +7% from a low print on Feb. 9.

Note: One of China's largest insurance companies, Anbang Insurance Group, was seized as it violated laws and regulations that could seriously endanger the solvency of the company.

In Europe, regional indices trade mixed this morning with strength in the Italian MIB offset by weakness in the Spanish Ibex and FTSE.

U.S stocks are set to open in the 'black' (+0.3%).

Indices: Stoxx600 flat at 380.4, FTSE -0.2% at 7238, DAX +0.1% at 12470, CAC-40 flat at 5310, IBEX-35 -0.2% at 9858, FTSE MIB +0.4% at 22541, SMI -0.6% at 8917, S&P 500 Futures +0.3%

2. Crude oil prices rally, gold little changed

Crude oil prices remain better bid and range bound following the release of this week's EIA inventory report, which showed a somewhat surprising decline in crude oil inventories on the order of -2.3m barrels compared to the average increase of +3.4m barrels in the previous five-years.

U.S oil production last week was steady at +10.27m bpd, a record level, while crude exports jumped to more than +2m bpd, close to a record +2.1m hit in October.

Crude bulls are beginning to ask if the "bull" rally could fade away as the U.S. oil production undermines the OPEC production cut commitments.

Note: The decline in crude inventories was particularly acute in Cushing. U.S oil refineries averaged approximately +15.8m bpd during the week ending February 16 or about -330k fewer bpd than last week previous.

Ahead of the U.S open, gold prices are little changed, but the 'yellow metal' remains on track for its sharpest weekly drop in nearly three-months. Spot gold is down -0.1% at +$1,329.16 an ounce.

Note: Prices gained +0.6% Thursday, their biggest one-day percentage rise since Feb. 14. The precious metal remains on track for its biggest weekly fall since the week ended Dec. 8, 2017.

3. Sovereign yields fall

Capital markets remains somewhat sceptical that the recent streak of data on wage growth, consumer prices and producer prices points to a rapid acceleration in inflation on either side of the Atlantic.

Data this morning from the Eurozone showed that consumer price growth slowed slightly last month (see below), but the core-measure edged a tad higher for the first time in months.

The ten-year U.S yield has eased, but remains atop of their 2014 high print, while those on German bunds dropped to the lowest since early January.

The yield on 10-year Treasuries decreased -2 bps to +2.90%. In Germany, the 10-year Bund yield has fallen -2 bps to +0.70%, the lowest in four weeks. In the U.K, the 10-year Gilt yield has declined -2 bps to +1.546%. In Japan, 10-year JGB's yield has dipped less than -1 bps to +0.05%, the lowest in more than seven-weeks.

4. Dollar on the back foot

The U.S dollar is modestly weaker as the market is apparently ready to accept as a given that the Fed shall move at least three times this year to tighten monetary policy and to raise the overnight fed funds rate. The only question is whether the Fed shall move for a fourth time and by how much?

For the 'single' unit, it's not only next weekend's Italian general election (Mar 4) that poses a risk to the EUR (€1.2313), but also Sunday week is the same date that Germany's SPD party members will vote on the proposed CDU/SPD coalition. The market is currently pricing in a +40-50% chance of a rejection, a result that could see Chancellor Angela Merkel step down.

Elsewhere, the pound (£1.3950) has edged a tad higher after U.K's PM Theresa May won the backing of her divided Brexit "war cabinet" to ask for an ambitious trade deal with the E.U.

The SEK (€10.0388) is a tad softer outright as the market felt that the Riksbank Feb minutes this morning were on the softer side with concerns lingering over inflation and the exchange rate given the recent negative surprise with Jan CPI data.

5. Eurozone Jan CPI unrevised, but still a distance from target

Eurostat said consumer prices in the 19 countries sharing the 'single unit' fell -0.9% m/m in January for a +1.3% y/y increase.

Ex-food and energy, or core-inflation, fell -1.3% m/m and rallied +1.2% y/y, accelerating from +1.1% in the previous three months.

An even broader measure of core inflation, which in addition excludes alcohol and tobacco prices, also increased to +1.0% y/y in January from +0.9% in the previous three-months.

Canadian Dollar Unchanged Ahead Of CPI

The Canadian dollar is drifting in the Friday session. Currently, USD/CAD is trading at 1.2707, up 0.01% on the day. On the release front, Canada will release a host of CPI indicators, led by CPI. This key indicator is expected to rebound with a gain of 0.4% in January. In December, CPI declined 0.4%, its first decline in six months. In the US, there are no data releases, but we'll hear from three FOMC members – William Dudley, Loretta Mester and John Williams.

Canadian retail sales reports, released on Thursday, were dismal in December. Core Retail Sales plunged 1.8%, well of the estimate of +0.1%. This marked the sharpest decline since January 2015. It was a similar story with Retail Sales, which fell 0.8%, missing the estimate of 0.0%. This was the indicator's worst showing since March 2016. The soft readings pushed USD/CAD as high as 1.2754 on Thursday, its highest level since late December. The Canadian dollar has dropped 1.2% this week, and if CPI also misses expectations, the slide could continue.

Investors remain wary after the recent stock market turbulence, which wiped off some $4 trillion in valuations. A key factor in the sharp correction was investor concern that higher inflation in the US would trigger more interest rate hikes. This has led to close monitoring of any releases connected to the Federal Reserve, and led to high anticipation ahead of the release of the January minutes on Wednesday. There were no major revelations in the minutes, and policymakers did not discuss a quicker pace of rate hikes. Still, policymakers hinted that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers “anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further”. At the December meeting, the Fed penciled in three rate hikes in 2018, but there is growing sentiment in the markets that the Fed may have to raise rates four or even five times this year. As for inflation, the minutes did not reveal any concern, with most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent.

EURCAD Trades Around 2-Year High, Bullish Bias But Possibility Of Overstretched Rally

EURCAD has advanced considerably since roughly the beginning of the year, hitting a two-year high of 1.5687 during Thursday's trading. Price action is at the moment taking place not far below this peak.

The Tenkan-sen line being above the Kijun-sen one is pointing to a bullish short-term momentum. However, the Chikou Span suggests that the recent rally might be overextended, rendering a pullback in the near-term a possibility.

Price advances could meet resistance around yesterday's high of 1.5687 – including the 1.57 handle that may be of psychological importance – with stronger bullish movement turning the attention to the 1.58 level that could also hold psychological significance.

On the downside, the area around the current level of the Tenkan-sen at 1.5569 might offer support, with a violation of this area increasingly bringing the Kijun-sen at 1.5433 into focus.

The medium-term picture is positive: price action is taking place above both the 50- and 100-day moving averages, as well as the Ichimoku cloud. In addition, both MA lines maintain a positive slope.

Overall, both the short- and medium-term outlooks are looking bullish, with the possibility of an overstretched market in the short-term being in place.