Sample Category Title

Currencies: USD Decline Slows, At Least For Now

Sunrise Market Commentary

- Rates: Room for consolidation ahead of Wednesday's FOMC Minutes?

We expect trading to be sentiment-driven and technically in nature today amid an empty eco calendar. Volumes will be low in absence of US traders (President's Day Holiday). Underlying sentiment remains bearish for core bonds, but we'd argue in favour of some consolidation in the run-up to Wednesday's FOMC Minutes. - Currencies: USD decline slows, at least for now

The dollar tested key support area's on Friday, but rebounded later in the session. The econ calendar is thin today. The rebound in equities went hand-in-hand with a weaker dollar recently. Will this link persist? At least this morning, there are tentative signs that it might become less tight

The Sunrise Headlines

- US stock markets ended near opening levels on Friday, but last week's performance was the strongest in 5 years. Asian risk sentiment is ebullient with China still closed for Lunar New Year.

- A Russian propaganda arm oversaw a criminal and espionage conspiracy to tamper in the 2016 US presidential campaign to support Donald Trump and disparage Hillary Clinton, said an indictment released on Friday.

- China warned it may hit back if the US implements aluminium and steel restrictions as recommended by the Commerce Department on Friday.

- Fitch upgraded the Greek rating from B- to B (positive outlook). Fitch expects reduced political risks, general government primary surpluses and legislated fiscal measures to improve Greece's general government debt sustainability.

- London's property market has moved out of its boom phase and home sellers need to be more realistic about their price demands, according to Rightmove. Asking prices were down 1% Y/Y, a sixth consecutive fall.

- Buoyant sales of cars and electronics led Japan's exports to a 14th straight month of growth in January (12.2% Y/Y). Imports increased by 7.9% Y/Y. The adjusted trade surplus rose more than forecast, to ¥373.3bn.

- Today's eco calendar contains only second tier EMU eco data. The Eurogroup choses the next ECB vice-president out of Spanish economy minister de Guindos and Irish ECB governor Lane. US markets are closed for President's Day.

Currencies: USD Decline Slows, At Least For Now

USD decline slows, at least for now

On Friday morning, the dollar remained under pressure, extending the established downtrend. Important USD support in EUR/USD and in the trade-weighted dollar caused USD selling to slow. Gradually, even a modest USD short-squeeze kicked in ahead of the long weekend in the US. US eco data were also again slightly USD supportive, even as we have to admit that didn't help the dollar much of late. EUR/USD finished the session at 1.2406 (from 1.2506). USD/JPY also rebounded off intraday lows well below 106 and finished the week at 106.21.

Overnight, several Asian markets are closed for the Lunar New Year Holidays. Japanese equities extend their rally. Japanese trade data (both exports and imports) were strong and equities are also supported by a slowing yen rally. USD/JPY tries to regain the 106.50 level. EUR/USD hovers in the low 1.24 area.

US markets are closed for President's Day holiday. The EMU eco calendar is thin. At the end of last week, the USD selling finally slowed. With US markets closed, we probably won't get a clear sign for USD trading. Later this week, the calendar remains uninspiring. The Minutes of the January Fed meeting and CB speeches have most market moving potential. Global risk sentiment remains a factor of importance, too. Of late, the risk rally went hand-in-hand with a USD decline. We look out whether this link holds. There are tentative signs this morning that a positive risk sentiment shouldn't cause further USD losses. From a technical point of view, EUR/USD 1.2555/98 (correction top, 62% retracement) remains key resistance. A break would indicate more trouble for the dollar. We don't see a need for such a break because of the economic fundamentals. However, dollar sentiment remains fragile. We keep the working hypothesis for EUR/USD to hold the 1.2598/1.2206 band. A downside break would call of the ST USD alert.

UK retail sales disappointed on Friday, but didn't hurt sterling much. UK PM May spoke with German Chancellor Merkel. There was no clear result of the talks, but maybe May gained support for some kind of a tailor-made solution. EUR/GBP declined slightly towards the end of the session. Rightmove house prices were higher than expected 0.8% M/M, but the London boom market was said to be over. We expect more consolidation in the 0.8690/0.8930 trading range. The day-to-day momentum became less skeptical on sterling

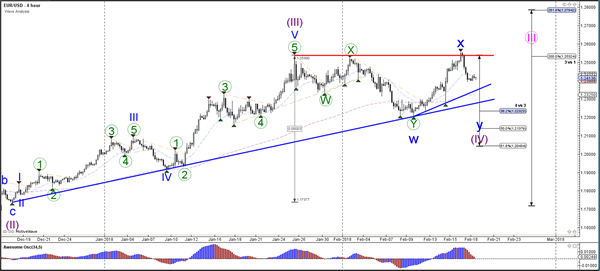

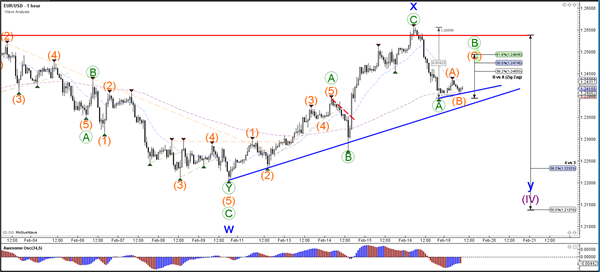

EUR/USD topside test rejected, for now

Daily Wave Analysis: EUR/USD Bearish Momentum After Failure To Break Above Top

Currency pair EUR/USD

The EUR/USD failed to break above the previous top (red) and the bearish bounce is showing strong momentum. This could indicate that there is an expansion of the corrective pattern via a WXY (blue) within wave 4 (purple). A new break above 1.25 however would still make an uptrend continuation more likely.

The EUR/USD seems to be building a bearish ABC (green) zigzag when considering the strong bearish price action in wave A (green). A break below the support trend lines (blue) could see price fall lower towards 1.2250-1.23.

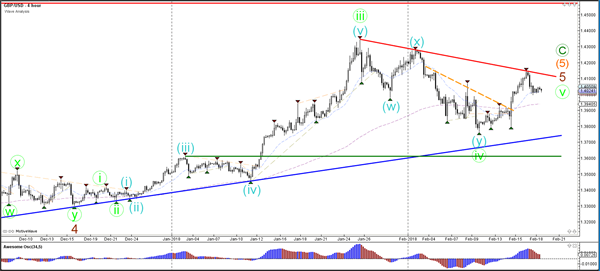

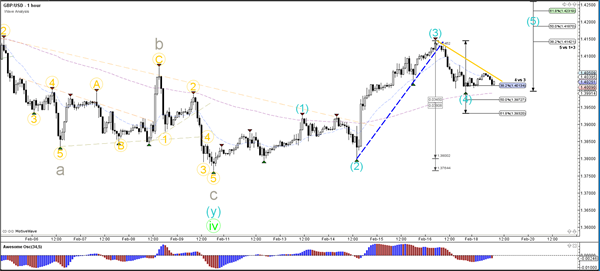

Currency pair GBP/USD

The GBP/USD is still testing the main resistance trend line (red). A bullish breakout could indicate a likely chance of continuation once price breaks above resistance

The GBP/USD is probably in a corrective wave 4 (blue) and could be in a wave 5 once price breaks above the resistance trend line (orange)

Currency pair USD/JPY

The USD/JPY came close to hitting the -61.8% Fibonacci target but missed it by a few pips. There is a chance that price will hit resistance and turn around to complete the target.

The USD/JPY seems to have completed a wave 3 (orange) and price is now building a potential corrective wave 4 (orange).

Aussie Reverses Its Previous Session Losses

For the 24 hours to 23:00 GMT, the AUD declined 0.63% against the USD and closed at 0.7902 on Friday

LME Copper prices rose 0.9% or $61.0/MT to $7159.0/MT. Aluminium prices rose 1.2% or $25.5/MT to $2189.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7926, with the AUD trading 0.3% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7883, and a fall through could take it to the next support level of 0.7841. The pair is expected to find its first resistance at 0.7978, and a rise through could take it to the next resistance level of 0.8031.

Amid no major macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving average.

Euro Trading Higher In The Asian Session

'

For the 24 hours to 23:00 GMT, the EUR declined 1.02% against the USD and closed at 1.2407 on Friday.

On the macro front, Germany's wholesale price index rose 0.9% on a monthly basis in January, beating market expectations for a rise of 0.2%. In the prior month, the wholesale price index had recorded a fall of 0.3%.

In the US, data showed that housing starts climbed more-than-anticipated by 9.70%, on a monthly basis, to an annual rate of 1326.0K in January, reaching its highest annual rate since October 2016 and compared to a revised level of 1209.0K in the previous month. Markets were expecting housing starts to rise to a level of 1234.0K. Additionally, building permits in the US unexpectedly rose 7.40%, on a monthly basis, to an annual rate of 1396.0K in January, hitting its highest level since June 2007. Building permits had recorded a revised reading of 1300.0K in the previous month, while investors had envisaged for a rise to a level of 1300.0K. Moreover, the flash Reuters/Michigan consumer sentiment index rose unexpectedly to 99.90 in February, marking its highest level in 14 years and higher than market expectations for a drop to a level of 95.40. In the previous month, the Reuters/Michigan consumer sentiment index had registered a reading of 95.70.

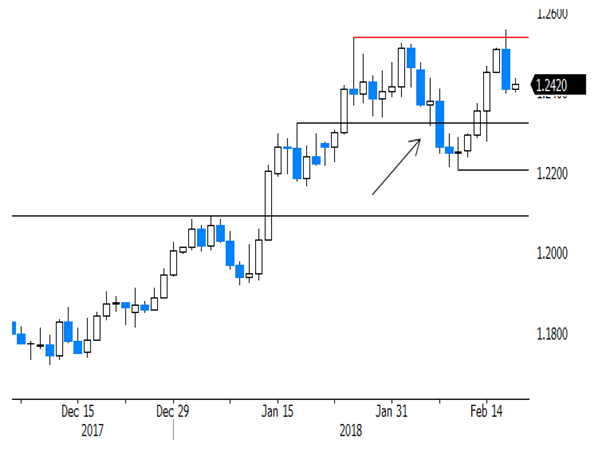

In the Asian session, at GMT0400, the pair is trading at 1.2421, with the EUR trading 0.11% higher against the USD from Friday's close.

The pair is expected to find support at 1.2358, and a fall through could take it to the next support level of 1.2296. The pair is expected to find its first resistance at 1.2519, and a rise through could take it to the next resistance level of 1.2618.

Going ahead, traders would keep a close watch on Euro-zone's current account balance and construction output data, both for December, slated to release in few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving average.

UK’s Retail Sales Rises Less Than Expected In January

For the 24 hours to 23:00 GMT, the GBP declined 0.76% against the USD and closed at 1.4013 on Friday, after data showed that UK's retail sales came in worse-than-expected in January. Britain's retail sales grew at a slower than expected pace of 0.1% on a monthly basis in December, as a rise in inflation weighed on consumer spending. Retail sales had registered a revised drop of 1.4% in the prior month, while markets were anticipating for a gain of 0.5%.

In the Asian session, at GMT0400, the pair is trading at 1.4040, with the GBP trading 0.19% higher against the USD from Friday's close.

Overnight data showed that UK's Rightmove house price index rose 0.80% on a monthly basis in February, after recording a gain of 0.7% in the previous month.

The pair is expected to find support at 1.3976, and a fall through could take it to the next support level of 1.3913. The pair is expected to find its first resistance at 1.4124, and a rise through could take it to the next resistance level of 1.4209.

With no major macroeconomic releases in the UK today, investor sentiment would be determined by global macroeconomic news.

The currency pair is showing convergence with its 20 Hr and trading below its 50 Hr moving average.

Japan’s Trade Surplus Widened Above Expectations In January

For the 24 hours to 23:00 GMT, the USD rose 0.23% against the JPY and closed at 106.36 on Friday.

In the Asian session, at GMT0400, the pair is trading at 106.33, with the USD trading 0.03% lower against the JPY from Friday's close, after overnight data showed that Japan's adjusted merchandise trade surplus widened more-than-anticipated to ¥373.3 billion in January, after recording a surplus of ¥86.8 billion in the previous month. Markets were anticipating the country's adjusted merchandise trade surplus to drop to ¥143.9 billion. The nation's exports advanced 12.2% on an annual basis in January, higher than market expectations for a gain of 9.4%. In the previous month, exports had risen 9.3%. Also, the nation's imports climbed 7.9% YoY in December, beating market estimates for a rise of 7.7%. Imports had advanced 14.9% in the prior month.

The pair is expected to find support at 105.79, and a fall through could take it to the next support level of 105.24. The pair is expected to find its first resistance at 106.64, and a rise through could take it to the next resistance level of 106.94.

Going ahead, traders would focus on Japan's machine tool orders for January, scheduled to release tomorrow.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving average.

Swiss Franc Trading Marginally Firmer

For the 24 hours to 23:00 GMT, the USD rose 0.78% against the CHF and closed at 0.9281 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9276, with the USD trading 0.05% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9213, and a fall through could take it to the next support level of 0.9151. The pair is expected to find its first resistance at 0.9313, and a rise through could take it to the next resistance level of 0.9351.

The currency pair is trading above its 20 Hr and 50 Hr moving average.

Loonie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.67% against the CAD and closed at 1.2560 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.2536, with the USD trading 0.19% lower against the CAD from Friday’s close.

The pair is expected to find support at 1.2469, and a fall through could take it to the next support level of 1.2402. The pair is expected to find its first resistance at 1.2585, and a rise through could take it to the next resistance level of 1.2634.

In absence of any macroeconomic releases in Canada today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving average.

Asian Equity Market Gains And The U.S. Dollar’s Weakness

Asian equity markets continued to build on last week's gains, after U.S. stocks capped their best week since 2013. Investor sentiment has gradually improved after fears of rising inflation sent most global indices into correction territory. The Cboe's Volatility Index (VIX) ended Friday's session below 20, suggesting that indictments from Special Counsel Robert Mueller against 13 Russian nationals for alleged interference in the 2016 elections did little to impact investor decisions. With the U.S. markets closed on Monday for President's Day and the Greater China region remaining offline for the Lunar New Year, expect trading volumes to be below average.

The U.S. Dollar's weakness remained a bit of a mystery for many currency traders, as it is supposed to follow differential in yields. The gap between U.S. and German 10-year yields widened to 217 basis points, and had gained 28% since mid-July 2017. Similarly, U.S. – Japan 10-year yields widened 285 basis points, the highest increase since 2007. Still, the Dollar declined against the Euro, Japanese Yen and all other major currencies.

One explanation for why the correlation between the Dollar and yield differentials has broken recently, is that financial market participants are forward-looking. Investors believe that rising inflation in the U.S. will spread to other economies, leading to tighter monetary policies elsewhere. When major central banks such as the European Central Bank, Bank of England and Bank of Japan begin normalizing policies, rate differentials will narrow at a fast pace, given that they are starting from a very low base.

Yields in the U.S. are not just rising because of higher inflation expectations, but also due to rising twin deficits – the fiscal and current account. This should make U.S. debt less attractive, and gold will likely become the primary beneficiary as it continues to benefit from inflationary pressures and budget deficit worries.

However, this view may change if the Fed decides to take a more aggressive approach in fighting inflation. Wednesday's FOMC minutes will likely reveal fresh hawkish insights, but for the dollar to make a U-turn, it requires the Fed to tighten policy faster than previously estimated. Any indication of four rate hikes instead of three in 2018 will do the trick, but this is unlikely to appear in Wednesday's minutes, and investors will probably need to wait until the March meeting.

USD/JPY Broke Below 106

Market movers today

We start the week in a quiet fashion on the data front . The main events will be the minutes of the latest Fed meeting on Wednesday, including the Fed governor’s view on inflation and impending fiscal expansion, as well as the ECB minutes on Thursday. Another highlight this week will be PMI and IFO releases in the euro area and Germany on Wednesday and Thursday, respectively, which will give signs of the continued momentum in the euro area economy.

The Eurogroup will convene today and recommend one candidate to replace Vítor Constâncio as the ECB’s Vice President in June. It is a race between the favourite, Spain’s Economy Minister Luis de Guindos and the Irish Central Bank Governor Phillip Lane. As the Eurogroup decides on the next Vice President , attention turns to Mario Draghi’s successor as President with a recent Bloomberg survey of economists showing Germany’s Jens Weidmann (über hawk) as the clear favourite. See the poll here.

In Sweden, we get data on residential permits, starts and completions

Selected market news

Japanese shares rose this morning, leading Asian stocks higher, while Brent oil advanced above USD65/bbl. Robert Mueller, the Russia probe special counsel, indicted 13 Russian individuals and three Russian entities for allegedly interfering in the 2016 US presidential election through an elaborate social media campaign to help Donald Trump. The indictment means that Trump can no longer credibly cast doubt on alleged Russian election meddling, although he continues to deny the allegations. On Friday, the S&P 500 erased a gain that reached 0.9% following the news, while 10-year Treasury yields fell below 2.9%. Nevertheless, US equity index futures climbed this morning, although sett ement will be delayed due to the Presidents’ Day holiday .

The US Commerce department recommended the Trump administration to impose steep tariffs of 24% on steel and 7.7% on aluminium imports on national security grounds. China has already threatened retaliation to such measures, risking further escalation of trade tension between the world’s top two economies.

On Friday, the Japanese government officially reappointed Bank of Japan governor Haruhiko Kuroda for another five-year term and chose an advocate of bolder monetary easing as one of his deputies in a strong signal to investors that policy makers are in no rush to end the stimulus programme. A vote in parliament on the appointments could happen before the end of the month. On the news, USD/JPY broke below 106, triggering a linguistic tweak by Finance Minister Taro Aso, who said the government will act when needed, a day after stating there is no need for intervention.

Supported by tax cuts and a strong jobs market , US consumer confidence rose further in January to the second highest level since 2004. This supports our view that private consumption will remain the main growth driver in the US, although long-term inflation expectations remained unchanged at 2.5%.