Sample Category Title

EURUSD Pair Now Bullish Above 1.2290 Level

The euro has moved sharply higher against the U.S dollar, with price-action moving well above the key 1.2290 resistance area in early Tuesday trading. The EURUSD pair now trades around the 1.2320 region, with broad-based weakness in the U.S dollar index underpinning intraday strength in the single currency. With a lack of Eurozone macroeconomic data, traders will look to the 1.2332 level as the next upside barrier for the euro, and the key 89.00 handle on the U.S dollar index.

The EURUSD pair remains intraday bullish whilst trading above the 1.2290 level, further upside towards 1.2332 and 1.2364 now appears likely.

Should EURUSD price-action slip back below the 1.2290 level, we may see a downside correction back towards the 1.2255 and 1.2205 support levels.

USDJPY Further Bearish Below 108.29 Support

The USDJPY pair has moved back towards the price-lows of 2018, following U.S dollar index weakness, with the greenback dropping back below the 89.00 support level. The USDJPY pair currently trades around the 108.20 level after earlier breaking under the key 108.45 support level. Sellers are now looking to the 108.00 level as the next major technical region, with downside pressures likely to remain on the pair whilst the U.S dollar index trades well below the 89.00 technical level.

The USDJPY pair remains intraday bearish while price-action trades below the 108.29 level, further downside towards 108.00 and 107.84 levels may occur.

Should the USDJPY pair start to trade above the 108.29 level for an extended period, we may see a upside correction back towards the 108.45 and 108.98 levels.

Ripple Rises As It Partners With A UAE Remittance Firm

Yesterday, Ripple rose to a two-week high after the company announced a new partnership with UAE Exchange, a company that provides remittance services. It is a major company present in more than 21 countries, providing its service to more than 21 million people.

According to a statement, the company will use Ripple’s Ripplenet product to process cross-border transaction with the aim of reducing friction and costs.

This is a major deal for Ripple, which has in the past announced partnerships with other remittance companies like Western Union, MoneyGram, MercuryFX, and IDT Corporation.

After the announcement, the price of ripple rose to a high of $1.0507, which is its two-week high. The price is however significantly lower from Ripple’s all-time price of $3.299.

Ripple’s rise was not in isolation. It happened at a day when the prices of other cryptocurrencies were moving up.

As shown below, the pair is trading slightly lower than the 50 and 14-day SMA, with its RSI at 39.8. There are two potential scenarios. In the first, the price could correct slightly as traders move to lock in profits. This would see the pair drop to the $0.9178. Alternatively, traders can ride the momentum which would see the pair move higher.

UK Inflation Data Headline Tuesday Schedule

Investors can expect a steady pick-up in economic data on Tuesday following a slow start to the week, with reports on UK inflation set to dominate the headlines.

Action Begins at 07:45 GMT with France's quarterly nonfarm payrolls report. The data are expected to show a 0.2% increase in nonfarm jobs in October-December, following a 0.3% increase the previous quarter.

Switzerland will release headline producer inflation figures at 08:15 GMT. The producer price index (PPI) for January is forecast to climb 0.3% month-on-month, which translates into an annualized rate of 0.9%.

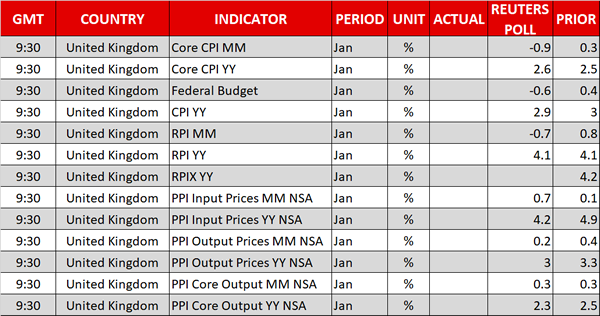

The UK Office for National Statistics will release a deluge of inflation data at 09:30 GMT, including the retail price index, producer price index and consumer price index. Consumer inflation in the UK is forecast to fall 0.6% in January, following a 0.4% increase the month before. In annualized terms, CPI is forecast to dip to 2.9% from 3%.

Core inflation, which strips away volatile goods such as food and energy, is projected to rise 2.6% year-over-year, up from 2.5%.

The Bank of England (BOE) risked over-inflated the economy when it decided to slash interest rates in the wake of the June 2016 Brexit vote. Central bankers voted to raise interest rates in November for the first time in more than a decade.

Shifting gears to North America, the National Federation of Independent Business (NFIB) will release its monthly US business optimism index at 11:00 GMT. The monthly report is not considered a major mover of financial markets but is used to gauge short-term trends in the active small business sector.

The American Petroleum Institute (API) will release its weekly crude inventory report at 21:30 GMT, which is a precursor to the official data provided by the US Energy Information Administration (EIA) the following morning.

In terms of monetary policy, Federal Open Market Committee (FOMC) member Loretta Mester will deliver a speech at 13:00 GMT.

EUR/USD

Europe's common currency bounced back on Monday, as the dollar drifted lower against a basket of world currencies. The EUR/USD briefly traded above 1.2300 but was last seen trading at 1.2286. The pair remains rangebound, with the 1.2200 handle providing the bottom.

GBP/USD

Pound sterling was confined to a narrow range on Monday, as investors turned their attention to UK inflation data. Cable was last seen trading at 1.3837, with the bulls eyeing a re-test of the psychological 1.4000 level.

US OIL

Crude prices are fresh off their worst week in two years, as prices crashed more than 10% in the wake of fresh inventory data and signs of surging US shale output. Markets flatlined at the start of the week but have since rallied amid renewed dollar weakness. US oil prices were last seen trading around $59.68 a barrel for a gain of 0.7%

Safe Havens Take Notice Of Turmoil, UK Inflation The Day’s Highlight

Here are the latest developments in global markets:

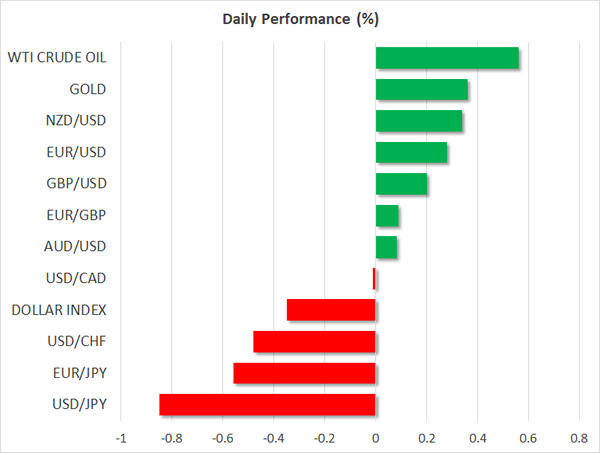

FOREX: The dollar index traded nearly 0.4% lower on Tuesday, as concerns over rising US deficits and the nation's long-term debt sustainability continued to pressure the world's reserve currency.

STOCKS: US stock indices advanced yesterday, recovering some of their recent losses. The Dow Jones led the pack, climbing 1.7%. The Nasdaq Composite rose by 1.6%, while the S&P 500 finished 1.4% higher. Despite the two consecutive days of recovery, markets still appear to be on shaky ground, as futures tracking the Dow, S&P, and Nasdaq 100 are all in the red, suggesting that these indices could open lower today. Investors will probably keep their eyes locked on the US inflation data that are due on Wedensday, as they could go a long way in determining whether the recent turmoil will intensify or subside. In Japan, the Nikkei 225 and the Topix closed lower by 0.65% and 0.9% respectively, possibly weighed on by the latest gains in the yen, as a stronger currency curbs the profits of Japanese exporting firms. In Hong Kong, the Hang Seng advanced by 1.5%, though in Europe, futures tracking the Euro STOXX 50 are in negative territory.

COMMODITIES: Oil prices gained somewhat, with WTI and Brent crude both being up 0.6% today, possibly supported by the recovery in risk sentiment and energy stocks. Despite this modest recovery though, the precious liquid has tumbled notably in recent days, weighed on by signs that US production is rising rapidly. In this respect, the IEA monthly oil report that is due out today will be closely watched. Any potential upward revisions in the US production forecasts could amplify the recent over-supply concerns and thereby, keep oil prices under pressure. In precious metals, dollar-denominated gold was nearly 0.4% higher, potentially boosted by the broader flight to safe assets as well as the tumble in the greenback.

Major movers: Trump proposes higher deficits; yen gains amid flight to safety

The Japanese yen surged during the early European morning Tuesday, with dollar/yen and euro/yen falling by 0.8% and 0.6% respectively, with no clear fundamental catalyst behind the move. A possible explanation is that investors are moving into safe haven assets like the yen, given that the stock market turbulence does not appear to be over yet. This view is amplified by the fact that other safe haven assets, such as the swiss franc and gold, are higher today as well. It is important to note that the aforementioned safe havens did not react much to the equity turbulence in recent days, perhaps because investors viewed the selloff as a “healthy” correction in overvalued stocks. However, the longer the uncertainty and the volatility last, the more likely it becomes that investors will seek the safety of these assets.

Yesterday, the US administration unveiled its budget proposal for the fiscal year 2019. This budget seeks to increase spending on infrastructure and the military, while it would cut the funding of popular health care programs like Medicare. Overall, the proposal would widen the federal budget deficit even further, making the long-term debt trajectory of the US economy even more unsustainable. It should be noted though, that this is simply an initial proposal that lays the foundation for a budget discussion between the White House and Congress, and thus is highly unlikely to pass Congress in its current form. Still, it shows that the already-large US budget deficit could widen further, a factor that is likely to keep bond investors on edge and the yields on US Treasuries elevated.

Elsewhere, Reserve Bank of Australia Assistant Governor Luci Ellis said overnight that policymakers are a little more confident that wages and inflation will eventually pick up some speed. However, she also noted that the up-to-now weak income growth is very risky given the high debt levels of Australian households. Nonetheless, the aussie reacted little to her comments.

Day ahead: All eyes on UK inflation

UK data and specifically inflation figures for the month of January are dominating attention in Tuesday's economic calendar. Those are due at 0930 GMT and undoubtedly have the capacity to lead to positioning on sterling, by among others shifting market expectations as regards the timing at which the Bank of England will deliver additional interest rate increases.

On a monthly basis, headline CPI is projected to contract by 0.6% – with the fall being attributed to seasonal factors – and on a yearly basis to expand by 2.9%, continuing to ease after hitting a near six-year high of 3.1% in November and lending support to those saying that it will start to gradually slow, moving towards the BoE's target for annual inflation of 2%; though it might be early to conclusively state that a gradual slowdown is taking place. Core inflation, which excludes prices of energy, food, alcohol and tobacco, will also be attracting interest. Annually, it is expected to grow by 2.6% versus 2.5% in December.

Data on January's producer prices and retail price inflation – a measure used to calculate payments on instruments such as index-linked government bonds and other contracts such as indexed-pensions – will also be released alongside CPI figures; another important release out of the UK later in the week (Friday) are retail sales for the month of January.

Cleveland Fed President Loretta Mester will be speaking on the US economic outlook at 1300 GMT. She holds voting rights within the FOMC in 2018.

In oil markets, the API report including information on crude oil stocks is due at 2135 GMT, while the IEA monthly report that cover issues affecting the world oil market is scheduled for release at 0900 GMT.

In equities, the earnings season continues to gather attention, having the potential to affect market sentiment.

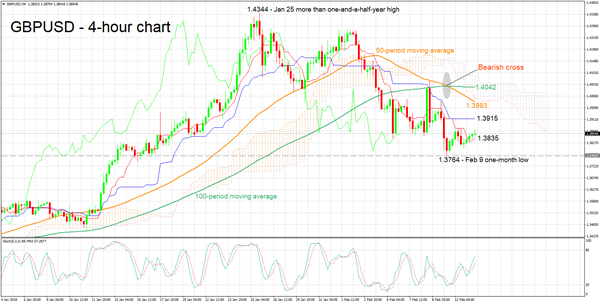

Technical Analysis: GBPUSD further distances itself from 1½-year high; bullish signal by stochastics in very short-term

GBPUSD has lost ground after hitting a more than one-and-a-half-year high of 1.4344 on January 25, eventually recording a one-month low of 1.3764 last week.

The Tenkan- and Kijun-sen lines are negatively aligned on the four-hour chart, projecting a negative picture in the short-term. However, the Tenkan-sen has started heading higher and the Kijun-sen has flatlined. These could be early signs of a change in momentum. Moreover, the stochastics are giving a bullish signal in the very short-term, as the %K line has moved above the slow %D one, and both are advancing higher.

Should UK data on inflation support the case for a rate hike by the BoE sooner rather than later, then the pair is anticipated to post gains. The area around the Kijun-sen at 1.3915 could act as a barrier to the upside in this case, with stronger bullish movement shifting the focus to 50-period moving average at 1.3983 – the range around this point also encapsulates the lower Ichimoku cloud (1.3997) and the 1.40 handle, a potential psychological level.

If, on the other hand, the figures push expectations for additional BoE tightening back in time, then GBPUSD is likely to decline. In this scenario, immediate support might come around the Tenkan-sen at 1.3835 – price action is currently taking place not far above this level – while further below the attention would fall on last week's one-month low of 1.3764.

Technical Outlook: USDJPY – Fresh Bears Broke Below 108 And Pressuring Key Support At 107.31

The pair accelerated lower in late Asian/early European trading and eventually broke below strong 108.28/00 support zone. Fresh weakness of the dollar comes on signs of stabilization in global equity market which prompted investors into riskier assets. Broader bears resume after being interrupted by 108.28/110.48 correction and pressuring key m/t support at 107.31 (08 Sep low/bull-trendline drawn off Sep 2012 low at 77.12. Break and close below 107.31 will be strong bearish signal for extension of larger downtrend from 118.66 (15 Dec 2016 peak) towards next significant point at 106.51 (Fibo 61.8% of 98.99/118.66, June/Dec 2016 rally). Overall structure is bearish and favors further weakness, however, bears may show stronger signs of hesitation at 107.31 support as daily RSI and slow stochastic are about to enter oversold territory while 14-d momentum is moving sideways in deep negative zone. Former pivotal supports now act as initial barriers at 108.00/28, followed by session high at 108.77 and falling 10SMA (109.05) which is expected to keep the upside protected.

Res: 108.00, 108.28, 108.77, 109.05

Sup: 107.31, 107.00, 106.51, 106.00

Elliott Wave View: Calling The Low In Placed In Bitcoin

Bitcoin ticker symbol: ( BTCUSD ) Short Term Elliott Wave view suggests that the decline from December 17.2017 peak to February 05.2018 low (5920.72) ended the Super Cycle wave “(b)” lower. Above from there, the rally is unfolding as a leading diagonal Elliott Wave structure. Where Intermediate wave (1) ended at 9090.8 high as Elliott Wave Double three structure. Where internals of Intermediate wave (1) ended in Minor wave W at 8648.9 high and Minor wave X at 7543.3 low.

Below from 9090.8 high, the pair ended it’s short-term correction against 2/05 cycle in Intermediate wave (2) low at yesterday’s low 7820. The internals of Intermediate wave (2) unfolded as Elliott Wave Zigzag correction, where Minor wave A ended at 8170.9 and Minor wave B ended at 8589.1 high. Above from there, the pair is expected to resume the upside. However, a break of 9090.8 high remains to be seen to avoid the double correction lower in Intermediate wave (2) dip. Up from 9090.8 low, the rally is unfolding as Zigzag Elliott wave structure. Where Minute wave ((a)) ended in 5 waves at 8992.9 high, below from there, the pair is doing a short-term correction against 7820 low in 3, 7 or 11 swings within Minute wave ((b)) dip. Near-term, while dips remain above 7820 low and more importantly the pivot from 5920.72 low remains intact during the dips pair is expected to resume higher. We don’t like selling it into a proposed pullback.

BTCUSD 1 Hour Elliott Wave Chart

GBPUSD Bearish Phase Continues, Momentum Indicators Look Negative

GBPUSD fell as low as 1.3770, a level that has been standing near the 40-day simple moving average during the past week. Since yesterday, the price has been trading slightly higher and successfully surpassed the 23.6% Fibonacci retracement level near 1.3820 of the last upward movement with the low of 1.2100 and the high of 1.4345.

Looking at the daily timeframe, the aggressive sell-off started after the pullback on the 1.4280 strong resistance level and the bearish correction is still in progress. The Relative Strength Index (RSI) is holding in the negative zone and is flattening, while the MACD oscillator is falling below its trigger line in the bullish territory.

Remaining in the same timeframe, if price continues the downside retracement and extends its losses below the 1.3770 support level, it could open the door for the 1.3660 barrier. If there is a fall below the latter level, there would be scope to test the 38.2% Fibonacci mark of 1.3490, which is near to the 11-month ascending trend line.

To the upside, the cable it could move towards the 1.4000 handle, which overlaps with the 20-day SMA at the time of writing. A break above the aforementioned obstacle could take the price towards the 1.4070 resistance level.

Currencies: USD Rally Running Into Resistance?

Sunrise Market Commentary

- Rates: Core yields holding near recent top head of US CPI

Yesterday, core bond yields held tight ranges near the recent peak as equities rebounded from last week's sell-off. Today, the calendar is again thin. More technical trading might be on the cards as markets look forward to tomorrow's US CPI. Global risk sentiment remains a wildcards. - Currencies: USD rally running into resistance?

Yesterday, the dollar lost slightly ground as sentiment on risk turned further positive. This morning, the US currency feels further selling pressure, with USD/JPY taking the lead. We expect more technical trading in the EUR/USD 1.22/24 trading range. EUR/GBP is nearing the 0.89 level. Today, UK CPI data might set the tone for GBP-trading

The Sunrise Headlines

- US equities continued Friday's comeback, closing the day with gains between 1.40% and 1.70%, the Dow Jones outperforming. Most Asian indices are also trading with good gains this morning. Chinese equities outperform. Japan trades in slightly negative territory as markets reopen after a long weekend.

- On Monday, President Donald Trump proposed a budget that calls for cuts in domestic spending and social programs such as Medicare and seeks a sharp increase in military spending and funding for a wall on the Mexican border..

- South Africa's ruling African National Congress decided to tell President Jacob Zuma to step down after he refused the top party leadership's request for him to resign voluntarily, according to five people familiar with the matter.

- Assistant governor of the Rank of Australia, Luci Ellis, said any pick up in wage growth was likely to be slow and protracted, weighing on household incomes and spending power amid high levels of debt. Australia still has more spare capacity than other developed countries, meaning it would take longer for wages and inflation to accelerate.

- The Japanese government wants Kuroda to serve another term as governor, according to a senior government official. PM Abe said he hasn't decided yet who to pick as next BOJ governor, but rebuffed calls from an opposition lawmaker to replace Kuroda given the pain the BOJ's negative interest rate policy was inflicting on commercial banks.

- Today's eco calendar is again thin in Europe. In the US, the NFIB small business confidence will be published. In the UK, the January price data take centre stage. Fed's Mester will speak on monetary policy and on the economic outlook. Italy will sell bonds of different maturities

Currencies: USD Rally Running Into Resistance?

USD rally running into resistance?

Last week, USD trading was only modestly affected as global volatility rose sharply. Yesterday, USD trading develop along the same lines. Equities recouped part of last week's sell-off. The dollar lost slightly ground against the euro, but the EUR/USD rise was capped near 1.23. USD/JPY was also little affected by the risk rebound, hovering in a tight range in the 108 big figure. The price action mainly occurred in equities with little impact on bonds and even less on the major USD cross rates. USD/JPY closed the day at 108.66. EUR/USD finished at 1.2292.

Asian equities mostly join the rebound from WS yesterday, with China outperforming. However regional indices are giving up part of the earlier gains toward the end of the session. Japanese equities are trading in negative territory as markets reopen after a long weekend. The dollar is ceding ground, with USD/JPY taking the lead. The pair trades in the 108.10 area. EUR/USD tries to regain the 1.23 mark. The USD correction occurs as US yields ease slightly this morning.

Today, the calendar is again thin. US NIFB small business confidence is expected to rebound from 104.9 to 105.3 after a decline last month. Fed's Mester will speak on Monetary policy (with Q&A). Will she give her view on recent market developments? FX traders will also keep an eye on bond and equity markets, even as they had little impact on the dollar of late. This morning, the dollar is ceding ground. This decline is a bit ‘strange' given the intraday price development on Asian equity markets. Even so, we assume EUR/USD to maintain a wait-and see modus in the 1.22/1.24 area going into tomorrow's US CPI release. Technically, the dollar decline slowed. EUR/USD dropped below the 1.2323/35 support but follow-through price action was modest. A break below 1.2165 would call off the ST downside alert (for USD).

Yesterday, BoE's Vlieghe reiterated that probably slightly more than three rate hikes are needed to keep inflation on target. It didn't help sterling. EUR/GBP closed at 0.8884. Today, the UK price data will be published. Headline CPI is expected to ease to 2.9% Y/Y, but other price indicators might paint a slightly different picture. A big positive surprise is probably needed to trigger a sustained comeback of sterling. Brexit uncertainty remains a sterling negative. EUR/GBP is trending higher in the 0.8690/0.9033 trading range, with intermediate resistance at 0.8930. We hold our view that the 0.8690 support probably won't be easy to break without big progress on Brexit.

USD trade-weighted (DXY): dollar rebound running into resistance?

Central Bank Speakers Start A Quiet Week In FX

Swiss Consumer Price Index (YoY) (Jan) was 0.7% v an expected 0.8%, from a previous 0.8%. Consumer Price Index (MoM) (Dec) was as expected at -0.1% from 0.0% previously. USDCHF fell from 0.93976 to 0.93664 after the data was made public.

UK MPC Member Vlieghe spoke at the Resolution Foundation in London. Some of the comments made were: If there is less credit headwind to the UK economy, then we may be ready for higher rates. There is increasing evidence that tighter labour markets are beginning to have an upwards effect on wages. The rise in the UK debt burden is not sustainable if it continues for many years. Households are leveraging up when there is not much slack in the economy. MPC should take an interest in that matter. Vlieghe says that the central bank is doing macro-prudential tightening but it is also appropriate to raise rates. Nothing has happened to challenge the BOE’s view about raising rates before reversing QE. The BOE has discovered it can cut rates lower than 0.5% since it gave guidance of a 2% threshold for reversing QE. The US Fed’s experience of reversing QE will also influence the level of rates at which BOE starts to reverse QE. The UK rate outlook depends on the uncertain economic outlook over next few years and the neutral UK interest rate is also very uncertain. GBPUSD made a low of 1.38319 before moving higher to 1.38738 during the speech.

UK MPC Member McCafferty spoke on the economic outlook and monetary policy. Some of the comments made were: It is quite likely that rates will move up slightly faster. The market is expecting three hikes over the next three years. There is a need for hikes because growth is strong and inflation is above target. Rates will have to go up gradually and the BOE will be watching data and making decisions on a month by month basis. The desire is to get rates to a place where they could be cut if it became necessary. EURGBP moved lower from 0.88887 to 0.88739 during the speech.

US Monthly Budget Statement (Jan) was $49.0B v an expected $51.0B, from a previous reading of $-23.0B.

Australian RBA Assistant Governor Ellis spoke about the economic outlook at the Australian Business Economists Forecasting Conference, in Sydney. Some of the comments made were: weak income growth very risky given high debt levels. The RBA is a bit more confident about the pickup in wages and inflation. Progress is, however, expected to be gradual and to lag other advanced economies. Central estimate is that NAIRU in Australia is still around 5 pct. Risk unemployment could fall further before stoking wages. No immediate pick up in wage growth is expected but a gradual rise is expected over time. Recent enterprise agreements to weigh on wage growth for a while. Retail competition to work against a rise in inflation and household income growth has been particularly weak in Australia. Households could curb spending if weak income growth becomes seen as permanent.

EURUSD is up 0.20% overnight, trading around 1.23153.

USDJPY is down -0.51% in early session trading at around 108.086.

GBPUSD is up 0.12% to trade around 1.38524.

AUDUSD is up 0.06% overnight, trading around 0.78630.

Gold is up 0.25% in early morning trading at around $1,325.75.

WTI is up 0.20% this morning, trading around $59.58.

Major data releases for today:

At 09:30 GMT, UK Consumer Price Index (YoY) (Jan) is expected out at 2.9% v 3.0% previously. Core Consumer Price Index (YoY) (Jan) is expected at 2.6% from 2.5% prior. Consumer Price Index (MoM) (Jan) is expected at -0.6% from 0.4% prior. Producer Price Index – Output (MoM) n.s.a. (Jan) is expected at 0.2% from 0.4% previously. Producer Price Index – Output (YoY) n.s.a. (Jan) is expected at 3.0% from 3.3% previously. Producer Price Index – Input (MoM) n.s.a. (Jan) is expected at 0.7% from 0.1% previously. Producer Price Index – Input (YoY) n.s.a. (Jan) is expected at 4.2% from 4.9% previously. PPI Core Output (MoM) n.s.a. (Jan) is expected to be unchanged at 0.3%. PPI Core Output (YoY) n.s.a. (Jan) is expected at 2.3% from 2.5% previously. Retail Price Index (MoM) (Jan) is expected at -0.7% from 0.8% previously. Retail Price Index (YoY) (Jan) is expected to be unchanged at 4.1%. GBP crosses could be moved by the data released at this time.

At 13:00 GMT, US FOMC Member Mester will speak about the economic outlook and monetary policy at the Dayton Area Chamber of Commerce Government Affairs Breakfast. Audience questions are expected to follow and this may impact US Assets and USD crosses.

At 23:30 GMT, Australian Westpac Consumer Confidence (Feb) will be released, with a prior reading of 1.8%. This could affect AUD crosses.