Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.57; (P) 150.66; (R1) 152.42; More...

At this point, intraday bias in GBP/JPY stays on the downside. The decline from 156.59 short term top should target 146.96 support. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 154.03 resistance is needed to confirm completion of the fall. Otherwise, outlook will remain cautiously bearish even in case of recovery.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal after rejection by 55 month EMA. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

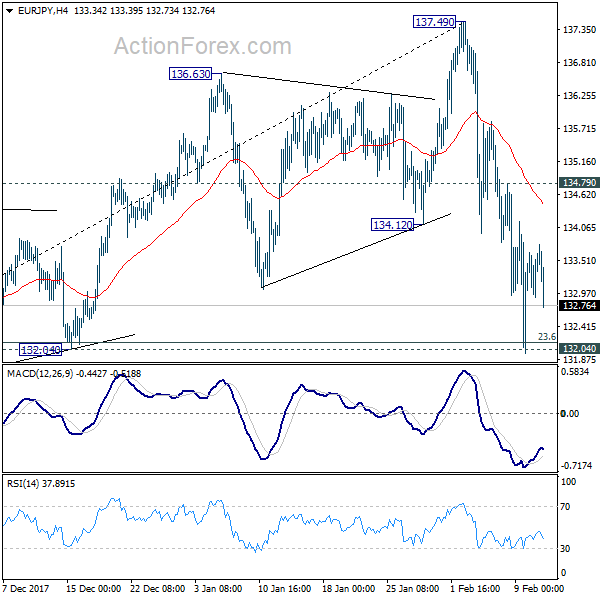

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.07; (P) 133.36; (R1) 133.82; More....

Intraday bias in EUR/JPY remains neutral for the moment. Deeper fall is still expected with 134.79 resistance intact. Decisive break of 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, outlook will be turned bearish for 38.2% retracement at 128.38 first. Nonetheless, rebound from 132.04 will retain near term bullishness. Break of 134.79 minor resistance will bring retest of 137.49 high instead.

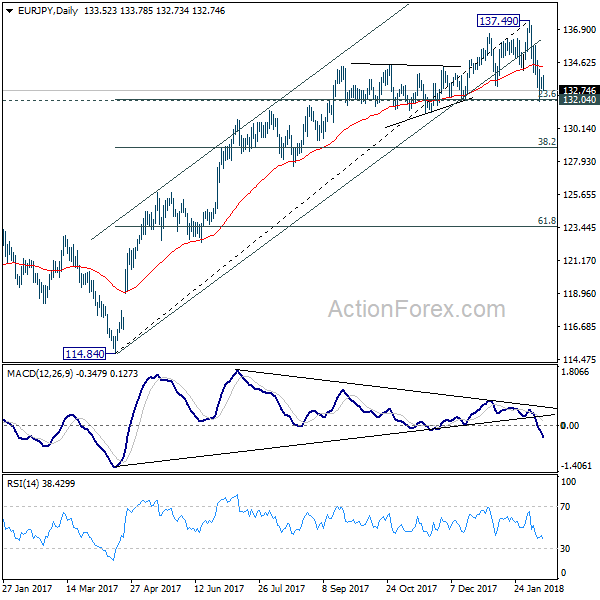

In the bigger picture, bearish divergence condition in week EMA indicates lost up medium term up trend momentum. But there is no clear sign of completion of up trend from 109.03 yet. Break of 137.49 will target 141.04/149.76 resistance zone. However, sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level.

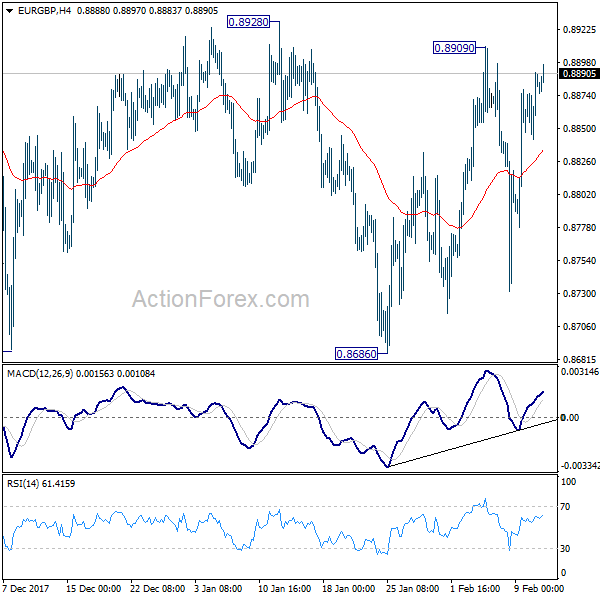

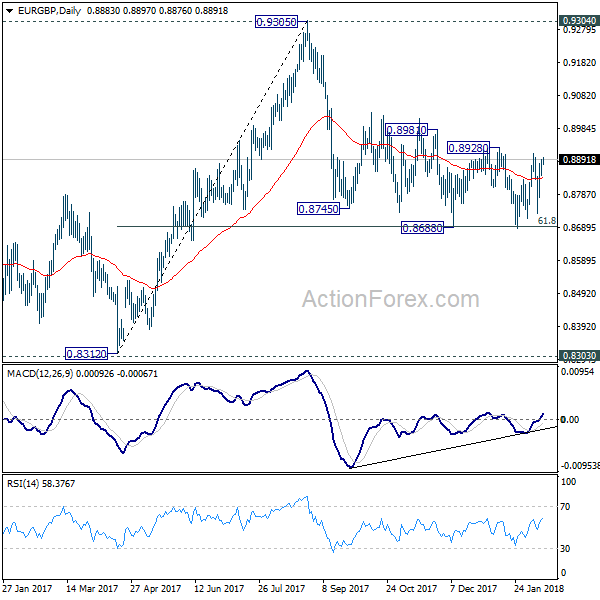

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8852; (P) 0.8871; (R1) 0.8901; More...

Intraday bias in EUR/GBP remains neutral as range trading continues. Near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

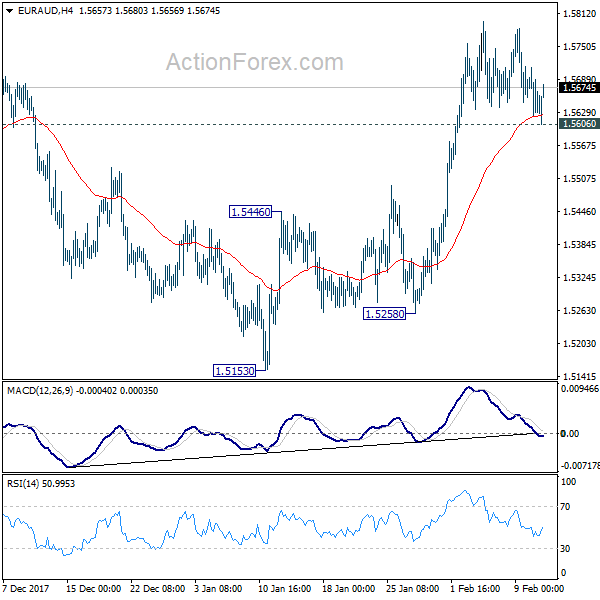

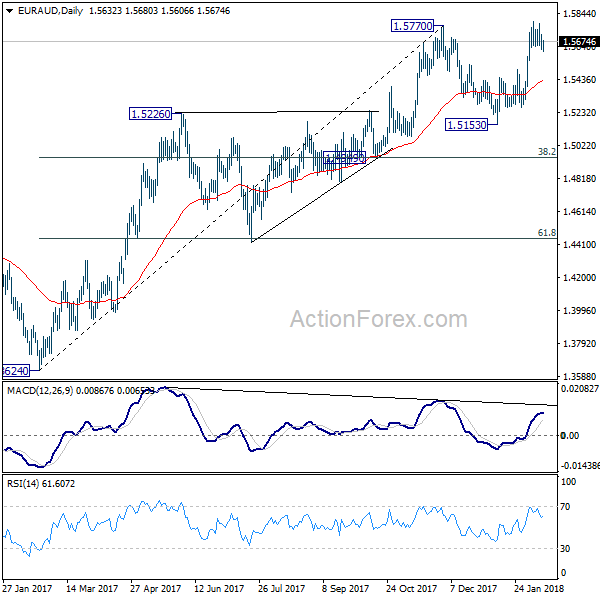

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5599; (P) 1.5655; (R1) 1.5687; More....

Despite breaching 1.5633 minor support, EUR/AUD quickly recovered, as supported by 4 hour 55 EMA. Intraday bias stays neutral and another rise is still in favor. Sustained break of 1.5770 resistance will confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. However, below 1.5633 minor support minor support will dampen this bullish case and turn bias to the downside.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

The Most Important Release Is The UK CPI Inflation

Market movers today

The calendar is thin again today and overall focus remains on market sentiment . US stocks closed higher for the second consecutive day yesterday.

The most important release is the UK CPI inflation. We estimate CPI inflation fell from 3.0% in December to 2.9% in January, driven mainly by a smaller contribution from the energy component , as a big monthly increase in January 2017 falls out , and food. We estimate CPI core inflation rose from 2.5% to 2.6%. CPI inflation remains one of the key release after Bank of England turned more hawkish at last week’s meeting,

Despite being a tier-2 release, look out for the US NFIB small business optimism for January. Business optimism is very high at the moment indicating increasing growth in business investments.

IEA will publish its monthly oil market report today. Following the recent rise in the US oil rig count , oil market fundamentals have come back into focus and the market will watch out for revisions in particular to US output forecast .

Selected market news

Asian stocks are advancing for the second day, after the S&P 500 jumped by 1.4% yesterday and volatility retreated, with VIX falling below 26. EUR/USD and 10-year US Treasuries are little changed this morning, while oil crept higher. The rand slipped after South African President Zuma defied calls by his party to resign.

In the US, the White House yesterday unveiled its federal budget proposal for the fiscal year 2019, including a proposal of USD1,500bn spending on infrastructure (USD200bn of which being Federal funds). Democrats needed to enact any legislation have already dismissed the proposal due to lack of significant federal spending, while many Republican fiscal hawks are wary of any big spending bill. The proposal would see the deficit almost double from projections last year despite cuts to domestic programmes and foresees the budget in deficit until the fiscal year 2039. Overall, the proposal would only worsen the already unsustainable debt path and we remain sceptical that any such legislation will actually pass Congress.

On the foreign policy front , Washington signalled readiness for direct talks with Pyongyang after reaching a deal with South Korea on a diplomatic approach to North Korea. However, despite possible negotiations, the Trump administration intends to maintain the pressure on the North Korean regime with more sanctions still to come, according to US Vice-President Mike Pence.

Danish inflation surprised on the downside yesterday falling from 1.6% y/y in September to 0.7% in January. A mix of longer lasting and more volatile factors caused the fall, but overall this has caused us to revise down our inflation out look to 0.9% in 2018 and 1.4% in 2019 – an out look that was already at the low end versus other forecasts. See more in Flash Comment Denmark: January surprise paves way for another year of muted inflation - we revise down our forecast, 2 February.

GBP Under Brexit Pressure

The British pound is recovering after a massive selloff that occurred a while ago. GBP is looking for reasons for becoming stronger, but is somewhat calm for now.

Brexit talks between the United Kingdom and the European Union have been back since last week, and the new phase traditionally began with discussing EU claims. Michel Barnier, a key representative of the EU party of the talks, made a statement that sent the pound lower.

Barnier emphasized that the parties may still not come to an agreement. The problem is that the UK is all for the 'mild' Brexit scenario, while the EU is insisting on 'hard' Brexit, which could become far more painful for London. The parties have not yet agreed on the European Court role after the UK leaves the Union, as the civil right acts passed by the EU are here to stay. The parties have no intention of putting each other's interests at any disadvantage, but as long as there's no clear policy specified, it is a reason for the EU to suspend the talks.

The market are discussing whether the 'mild' Brexit is feasible or only the 'hard' scenario is now viable. The UK is still making it clear and consistent, but this does not support the British pound at all.

The Brexit uncertainty makes the fundamentals a bit frightening. The manufacturing production in December dropped by 1.30% MoM, which appeared to be a 10-month low. Meanwhile, the PMI went from 54.20 to 52.00, that being a 18-month low.

Technically, there are several trends dominating in GPB/USD. The major trend is still ascending, while the mid-term one is a correctional downtrend with the target at the major channel support, or at 1.3650. The short term trend is also descending and is a part of the mid-term impulse. This short term movement may become the final component of the internal correction. After the price achieves 1.3650, it may bounce off to the mid-term descending channel resistance at 1.3890, and then head towards the upper projection channel at 1.4060

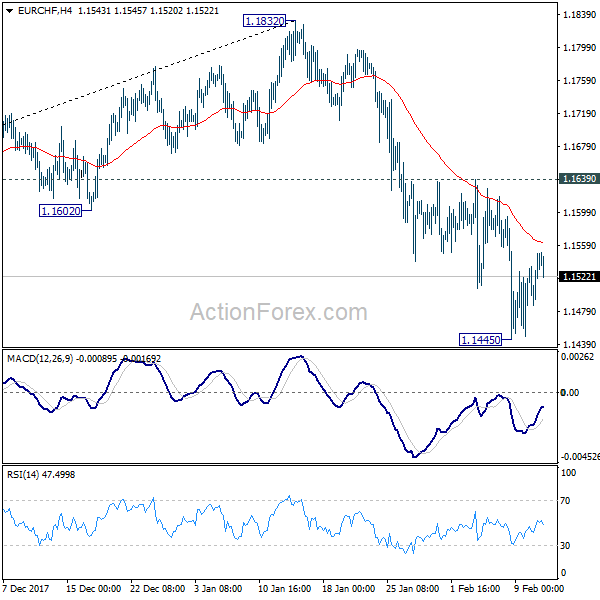

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1503; (P) 1.1526; (R1) 1.1566; More...

Intraday bias in EUR/CHF remains neutral for consolidation above 1.1445 temporary low. As long as 1.1639 resistance holds, further decline is expected. Below 1.1445 will extend the corrective fall from 1.1832 to 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Daily Wave Analysis: EUR/USD Bullish Breakout Above 1.23 Resistance And Bearish Channel

Currency pair EUR/USD

The EUR/USD broke above the resistance (dotted red) of the bearish trend channel after bouncing at support trend lines (blue), which could indicate the end of the wave 4 (purple) correction. A bullish continuation could indicate the start of wave 5 (purple) within wave 3 (pink).

The EUR/USD broke above the resistance levels and fractals of wave 4 (orange) and the top of wave 1 (blue). The bullish breakout could be part of a wave 3 (blue). This wave count could get confirmed if price manages to reach the 161.8% Fibonacci target at the minimum before building a wave 4.

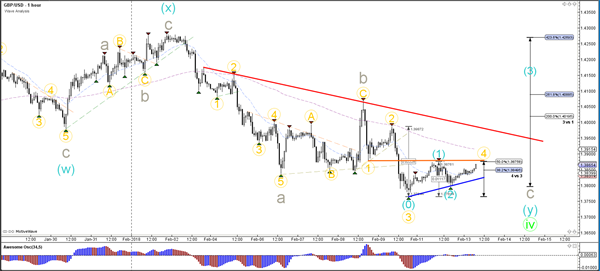

Currency pair GBP/USD

The GBP/USD failed to break below the previous low which indicate failure to continue with the downtrend. The Cable could be respecting the Fibonacci levels of wave 4 vs 3 (green) and a bullish breakout could indicate the start of wave 5.

The GBP/USD is at crossroads. It could break above resistance (orange) and invalidate the wave 4 correction (orange), which means that a bullish wave (blue) could start. Or price will bounce again at resistance and complete the 5th bearish wave (orange) before completing wave C (grey).

Currency pair USD/JPY

The USD/JPY is retesting a strong support zone again (green/blue). A break below this support zone could indicate a bearish continuation within wave 2/B (light purple) whereas a bullish bounce could see price complete the wave B/2.

The USD/JPY is showing strong bearish breakout candles below the support trend line (dotted blue). A break below the 100% Fib invalidates the wave 1-2 reversal.

Market Update – Asian Session: Equities Continue To Follow Wall Stlead

Headlines/Economic Data

General Trend: Equities in China and Hong Kong outperform

Kospi supported by gains in chip sector

In Asia, S&P500 and Nasdaq Futures move between gains and losses

Nikkei pares opening gains

Shanghai Property Index rises over 3%, later pares gain

China PBoC said to ask banks to temporarily halt new loans after Jan New Yuan Loans hit record high

PBoC offers 1-year medium-term lending facility (MLF) ahead of Chinese Lunar New Year

USD/JPY declines as Japanese traders return from holiday

Japan Q4 Prelim GDP data due on Wednesday

Japan

Nikkei 225 opened +1.2%; closed -0.7% (was closed on Monday for holiday)

TOPIX Iron & Steel Index -1.2%

Pioneer [6773.JP] Declines over 9% after cutting FY forecast

Renesas Electronics [6723.JP] Declines over 2%, guided Q1 semiconductor sales lower q/q

Fujifilm [4901.JP]: Declines over 1% as activist Carl Icahn urged Xerox to vote against planned merger

Toyota Motor declines over 1% amid stronger yen

(JP) Japan Fin Min Aso: Trying to promote new type of tax free NISA program

(JP) Japan Jan PPI (CGPI) M/M: 0.3% v 0.3%e; Y/Y:2.7% v 2.7%e

(JP) Japan Econ Min Motegi: PM Abe stance on monetary policy must be maintained- answer when asked about Gov Kuroda being reappointed

(JP) Japan PM Abe: Undecided on next BoJ Gov

(JP) Bank of Japan (BOJ) Gov Kuroda: Reiterates must maintain 'powerful' easing for economy, still distant to price target -speaking in parliament

Korea

Kospi opened +0.7%

Chip makers gain: Samsung Electronics and Hynix rise over 3%

Coway [021240.KR]: Declines over 6% after reporting FY earnings

Kangwon Land[035250.KR]: Declines over 1% as Q4 Op profit missed ests

(KR) South Korea Jan Export Price Index M/M:-0.4% v -1.5% prior; Y/Y: -3.5% v -2.0% prior; Import Price Index M/M: +0.7% v -0.7% prior; Y/Y:-2.4% v -0.9% prior

(KR) South Korea economist are worried about the fallout from a reversal ofcorporate tax rates and interest rates in Korea and the US; when the Fed raisesrates next time, it will create the first rate reversal between the twoeconomies in 11 years - Korean press

China/Hong Kong

Hang Seng opened +1.3%, Shanghai Composite +0.7%

Hang Seng Info Tech Index +3.5%, Materials +3%, Industrial Goods +2.8%, Consumer Goods +2.5%, Property/Construction +2.3%, Financials+2.3%, Services +2.3%

(CN) China PBOC has asked banks to defer new loans until after Feb 15th (start of Lunar New Year)

(CN) CHINA JAN NEW YUAN LOANS (CNY): 2.900T V2.050TE (fresh record high) after the closeyesterday

(CN) CHINA JAN M2 MONEY SUPPLY Y/Y: 8.6% V 8.2%E; M1 MONEY SUPPLY Y/Y: 15.0% V13.5%E after the close yesterday

(CN) CHINA JAN AGGREGATE FINANCING (CNY): 3.060T V 3.200TE afterthe close yesterday

USD/CNY (CN) PBOC SETS YUAN REFERENCERATE AT 6.3247 V 6.3001 PRIOR

(CN) CHINA PBOC LENDS CNY393B V CNY398B PRIOR IN 1-YR MEDIUM-TERM LENDINGFACILITY (MLF) AT RATE OF 3.25% V 3.25% PRIOR

(CN) PBoC: Skipped Open Market Operation (OMO) for 15th straight session

(CN) China Insurance Regulator (CIRC): Insurance firms offshore financingbalances backed by domestic guarantees cannot exceed 20% of net assets at endof prior quarter

Sunny Optical, 2382.HK Reports Jan handset lens setsshipments +19.6% y/y; Guides FY17 Net to rise more than 120% y/y

HNA unit HKICIM to sell Kai Tak sites to Henderson Land for HK$16.0B

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.6%

ASX 200 Telecom Index +0.7%, Resources +0.8%, Financials +0.4%

(AU) RBA's Assistant Gov Ellis: Retail competition to work against wage pressures, no reason yet to change full employment est from 5%

(AU) Australia Bureau of Agricultural and Resource (ABARES): Total area plantedto summer crops is estimated to have increased by 2% in 2017-18 to 1.3M hectares,-9% from Dec forecast

(AU) Australia sells A$150M v A$150M indicated in Nov 2027 indexed bonds, bidto cover 4.20x, avg yield 0.85333%

(AU) Australia Jan NAB Business Confidence: 12 v 10 prior; Conditions: 19 v 13prior

PilbaraMinerals (+10%), PLS.AU Reports Pilgangoora Project Pre-Feasibility Study results, DefinitiveFeasibility Study to complete by mid 2018

(NZ) New Zealand Government 6-Month FinancialStatements; Budget Surplus NZ$1.09B, +NZ$779M more than forecasted

Other Asia

(TW) Taiwan Final Q4 GDP due for release during European session

North America

US equity markets ended broadly higher: Dow +1.7%, S&P500 +1.4%, Nasdaq +1.6%,Russell 2000 +0.9%

S&P500 Materials +2%, Technology +1.8%

(US) White House released 2019 budget plan: seeks$1.7T of cuts to mandatory spending and receipts

AmerisourceBergen (ABC) Walgreens said to be in early stage talks to acquire the company - US financial press

GM GM Korea to shut down one of its factors; Confirms that it needs support from stakeholders to normalize its business in South Korea; to take charges of up to $850M

Wynn Resorts [WYNN]: Special Committee retains law firm Gibson, Dunn & Crutcher LLP and expands review

Looking Ahead: US Weekly API Crude Oil Inventories due later today

Europe

(UK) BOE’s McCafferty (dissenter): interest rates will have to rise gradually - press interview; UK economy is holding up relatively well,so rates will probably start rising sooner than previously thought

(SA) South Africa's Zuma reportedly wants 3-month notice period before resigning – press; Reportedly Zuma was given 48 hours to resign

Michelin[ML.FR]: Reports FY17 Op Net €2.74 v €2.75Be, Rev €22.0B v €20.9By/y; Guides initial FY18 Recurring Op income higher y/y, FCF over €1.1B

Looking Ahead: UK Jan CPI data due later today, along with the IEA Monthly report

Levels as of 01:00ET

Nikkei225 -0.7%, Hang Seng +1.6%; Shanghai Composite +1.1%; ASX200 +0.6%, Kospi +0.7%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.2%,Dax -0.2%; FTSE100 -0.2%

EUR 1.2312-1.2284; JPY108.78-108.24; AUD 0.7874-0.7848;NZD 0.7272-0.7247

Apr Gold +0.2% at $1,328/oz; Mar Crude Oil +0.6% at $59.62/brl; Mar Copper +0.9% at $3.11/lb

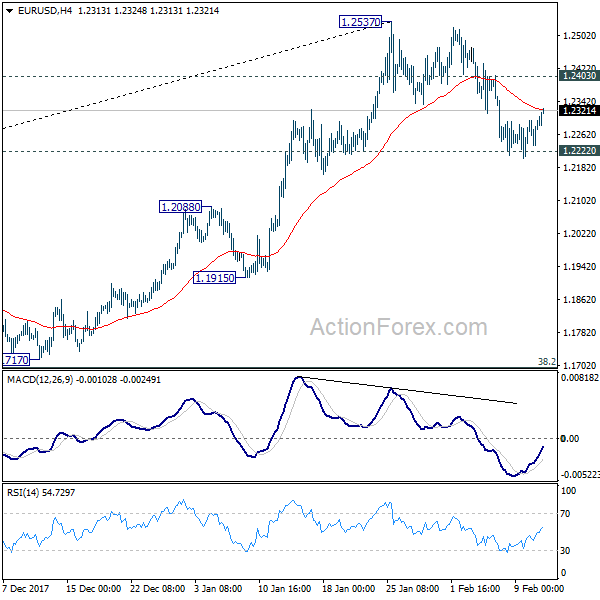

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2250; (P) 1.2274 (R1) 1.2313; More....

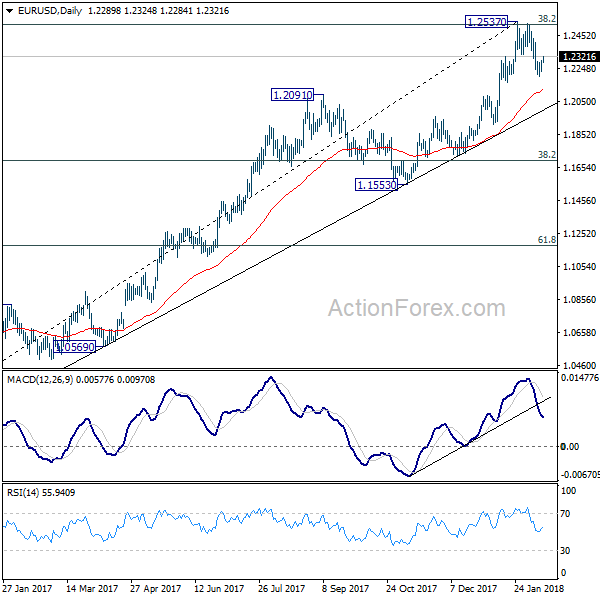

Intraday bias in EUR/USD remains neutral with focus on 1.2222 key near term support. Sustained break there should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.