Sample Category Title

USDCAD – Widening Daily Cloud Marks Strong Obstacle and May Limit Fresh Upside Attempts

The USDCAD edged higher and tests 1.2600 barrier (daily cloud base) at the beginning of US session on Monday.

The pair shows signs of regaining traction after strong upside rejection at 1.2687 and close in red on Friday, which signaled that recovery rally from 1.2248 (31 Jan low) might be running out of steam.

Daily cloud which twisted last week is widening and producing additional pressure, along with daily slow stochastic which is reversing from overbought territory.

On the other side, shallow dips on Friday/today were contained at 1.2555, with fresh attempts higher, suggesting that bulls did not completely run out of steam.

Bullish scenario requires lift above daily cloud (cloud top lies at 1.2637) and retest of pivotal 1.2663 barrier (Fibo 61.8% of 1.2920/1.2248 fall) to confirm continuation of recovery leg from 1.2248.

Otherwise, downside is expected to remain vulnerable while daily cloud caps, with increased risk on loss of 1.2555 handle and reversal signal on extension below 1.2520 (Fibo 38.2% of 1.2248/1.2687 upleg.

Res: 1.2606; 1.2637; 1.2663; 1.2687

Sup: 1.2555; 1.2520; 1.2490; 1.2468

Canadian Dollar Unchanged as Investors Search for Cues

The Canadian dollar has ticked higher in the Friday session. Currently, the pair is trading at 1.2609, up 0.05% on the day. On the release front, the focus is on Canadian employment indicators, with the release of Employment Change and the unemployment rate. Traders should be prepared for some movement from the Canadian dollar in the North American session.

This week's market selloff has boosted the US dollar, at the expense of the Canadian dollar and most other major currencies. The Canadian dollar has dropped 1.4% this week, and is down 2.5% in February, erasing the gains we saw in January. Interestingly, the catalyst for the current turbulence has been solid economic data in the US, namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

After some spectacular readings, Canada's economy is expected to show more modest job creation in January, with an estimate of 10.3 thousand. The unemployment rate is forecast to edge up from 5.7% to 5.8%. If these predictions are within expectations, the Canadian dollar could gain some ground on Friday, and end a tough week on a positive note.

EURJPY: Looks To Recovery Higher On Price Halt

EURJPY: The pair closed higher on price halt on Friday opening the door for more strength. On the downside, support comes in at the 133.00 level where a break if seen will aim at the 132.50 level. A cut through here will turn focus to the 132.00 level and possibly lower towards the 131.50 level. On the upside, resistance resides at the 133.50 level. Further out, we envisage a possible move towards the 134.00 level. Further out, resistance resides at the 134.50 level with a turn above here aiming at the 135.00 level. On the whole, EURJPY faces further bear threats

DAX Rebounds After Rough Week

The DAX index has started the week with gains in the Monday session. Currently, the index is trading at 12,303.00, up 1.63% since Friday's close. On the release front, there are no German or Eurozone indicators on the schedule.

Global stock markets were turbulent last week, and the DAX suffered sharp losses of 4.6%. US markets ended the week with gains, and Asian and European markets have followed suit on Monday. On Thursday, the DAX dropped to its lowest level since early September. It's been a rough February for the stock markets, and the DAX has shed 7.6% since the start of the month. Is the correction over? It's too early too tell, since much of the sell-off is related to investor concerns over possible interest rate hikes by major central banks. The Bank of England has said it could accelerate its pace of hikes, and the Federal Reserve could follow suit if inflation moves higher.

German President Angela Merkel has reached an agreement with the socialist SDP to form a new government, but the price was steep, as the SDP extracted major concessions from Merkel, notably control of the powerful finance ministry. This will likely mark a shift in Germany's eurozone policy, which had been marked by a conservative stance under former finance minister Wolfgang Schaeuble. The weaker members of the eurozone, such as Greece, will likely find a more sympathetic ear for financial help from the SDP than they did from Schauble. Many conservatives fear that the Olaf Scholz, who is expected to become finance minster, will not be as fiscally responsible as Schaeuble. On the weekend Scholz said that Germany should not dictate economic policies to other eurozone members. The coalition agreement still requires the consent of a majority of the 464,000 members of the SDP, and if the deal is rejected, Germany will likely be headed to new elections.

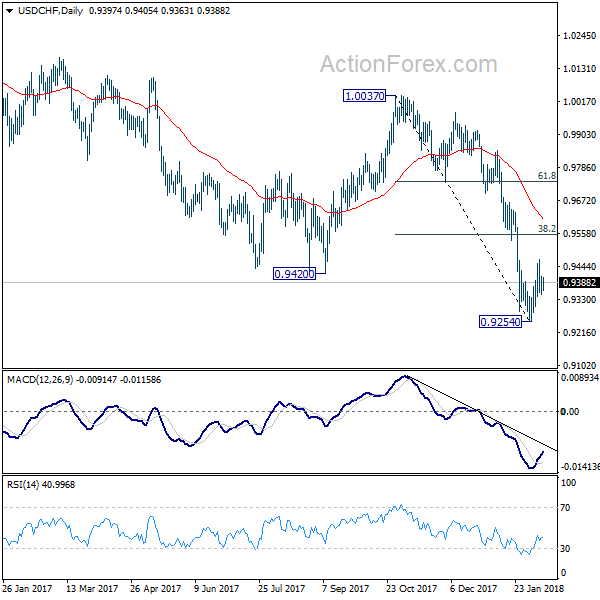

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9356; (P) 0.9382; (R1) 0.9416; More...

Intraday bias in USD/CHF remains neutral at this point. Also, note that there is no clear sign of trend reversal yet. Therefore, in case of another rise, we'd be cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring down trend resumption. On the downside, below 0.9339 minor support will turn bias to the downside for 0.9254. Nonetheless, firm break of 0.9553 will bring stronger rebound to 55 day EMA (now at 0.9616).

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.10; (P) 108.70; (R1) 109.36; More...

Intraday bias in USD/JPY remains mildly on the downside. The fall from 114.73 has just resumed. It's part of the pattern from 118.65 high and should target 106.48 fibonacci level. On the upside, break of 110.47 resistance is needed to indicate near term reversal. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

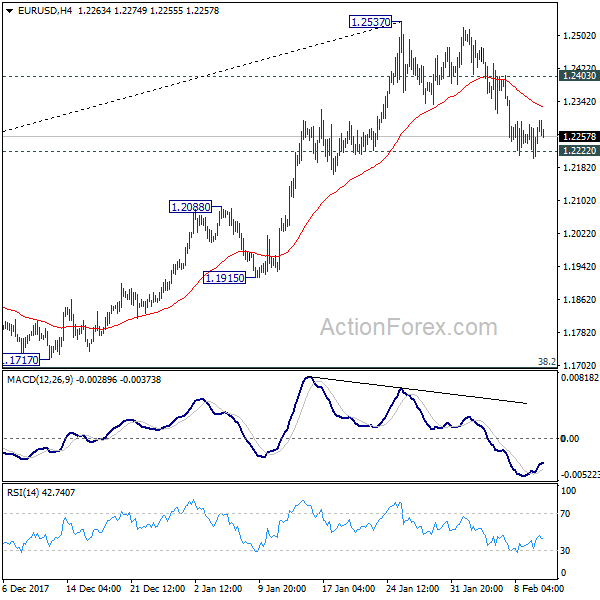

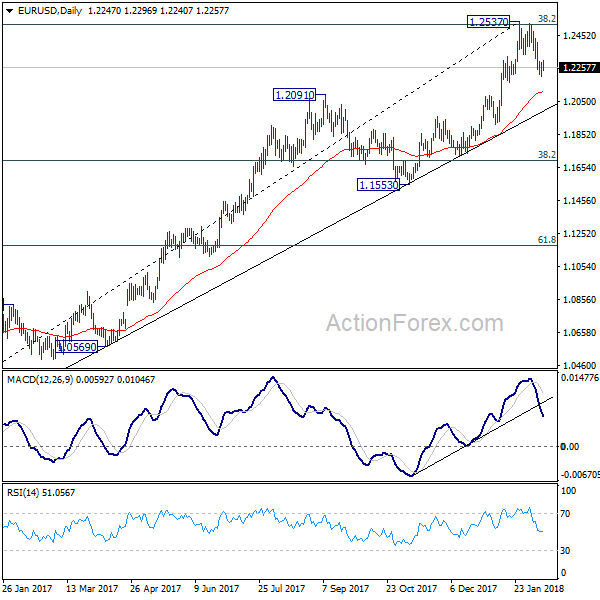

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2208; (P) 1.2248 (R1) 1.2290; More....

Intraday bias in EUR/USD remains neutral for the moment. Focus stays on 1.2222 support. Sustained break there should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

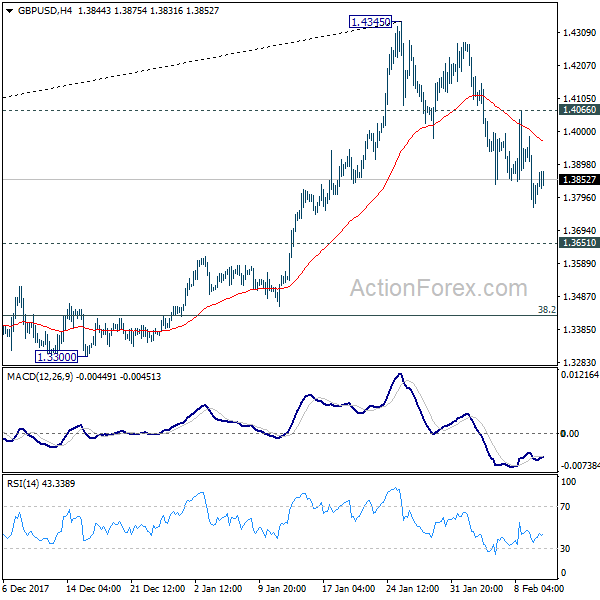

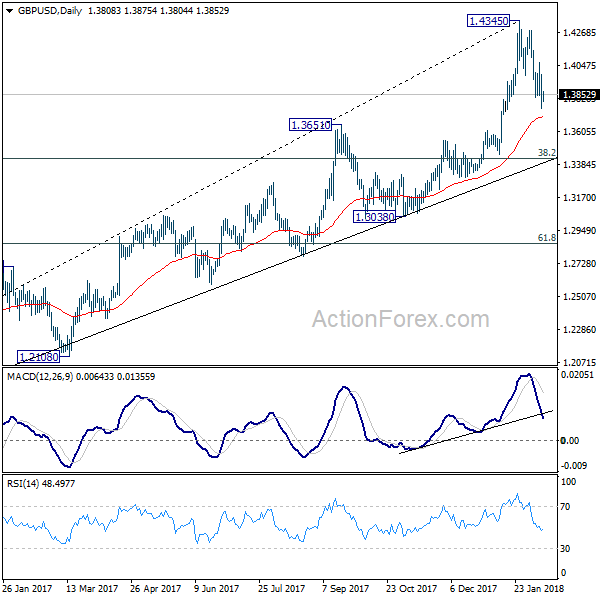

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3814; (P) 1.3940; (R1) 1.4035; More.....

At this point, intraday bias remains on the downside. The decline from 1.4345 is still in progress for 1.3651 resistance turned support. It's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. For the moment, further decline will remain expected as long as 1.4066 minor resistance holds.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Forex in Tight Range as Global Markets Recover

Global markets are generally in recovery mode today. European indices are all in black at the time of writing. US futures also point to higher open as markets await Trump's infrastructure plan. Major forex pairs and crosses are staying gin Friday's range, except AUD/NZD. But it should be noted that the retreats in Dollar and Yen are shallow and weak so far. There could be renew interests in these two currencies if risk sentiments turn sour again later in US session.

Trump to unveil USD 1.5T infrastructure plan

In the US, President Donald Trump is set to unveil an infrastructure plan today. Under the proposal, the government will spend USD 200b over 10 years, inform of grants to encourage states and cities to start their projects on infrastructure, including rebuild of highways, bridges, railroads, airports etc. . And, the White House estimated that would eventually results in USD 1.5T in new investments. However, it's believed that the plan itself will start facing big hurdles. Thee two main problems are firstly, it's not as much as the Democrats want, and secondly, there is not clear information on how to pay for the funding.

BoE Haldane in no rush to hike

Over the weekend, BoE chief economist Andy Haldane said that the central bank is in no rush to rate hikes. Haldane did acknowledge that inflation developments are "currently ahead of our target" and "on the balance of probabilities, it seems likely that some further tightening of policy might be needed over the period ahead." Nonetheless, he added that "we're in no rush, rates won't remotely go back to levels we've seen in the past, but nonetheless keeping the cost of living under control is, we think, the single best and most important thing we can do to help the economy."

BoE MPC member Gertjan Vlieghe sounded upbeat today and said there was "increased evidence that tight labour markets are finally starting to have some upward effect on wages". Also, "if there is less credit headwind to UK economy, then maybe ready for higher rates.,"

ECB concerned with US political influence on exchange rate

ECB Governing Council member Ewald Nowotny said the central bank is "certainly concerned about attempts by the United States to politically influence the exchange rate." And he added "that was a theme of economic discussions in Davos, where the ECB addressed this, and it will certainly be a theme at the upcoming G20 summit." Regarding the US economy, Nowotny said that President Donald Trump "started with a good inheritance" from the pervious government. And the current low unemployment, robust growth and tame inflation stem from Trump's predecessor, not his own policies.

BoJ Kuroda will get a second term

In Japan, it's reported that Prime Minister Shinzo Abe has finally made up his mind to give BoJ Governor Haruhiko Kuroda a second five-year term. And if that happens, Kuroda will be the first BoJ Governor to server two consecutive terms since Masamichi Yamagiwa, back in 1956 to 1964. Recent global stock market crash could be the trigger for Abe as stability is all that important for him to continue with his Abenomics. And this would be a strong message that BoJ will continue with it's massive stimulus, and more importantly, in a cautious way. Barring another disastrous day from US, Tokyo will likely open with a positive note in the upcoming Asian session, back from holiday.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3814; (P) 1.3940; (R1) 1.4035; More.....

At this point, intraday bias remains on the downside. The decline from 1.4345 is still in progress for 1.3651 resistance turned support. It's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. For the moment, further decline will remain expected as long as 1.4066 minor resistance holds.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 8:15 | CHF | CPI M/M Jan | -0.10% | -0.20% | 0.00% | |

| 8:15 | CHF | CPI Y/Y Jan | 0.70% | 0.80% | 0.80% | |

| 19:00 | USD | Federal Budget Balance Jan | 50.2B | -23.2B |

European Equities Broadly in the Green; Wall Street Looks Set to Open Higher

Here are the latest developments in global markets:

FOREX: The US currency remained lower on the day, with its broader gauge, the dollar index, being down by 0.3% around midday. The euro and sterling were advancing versus the greenback, after declining notably in the preceding week and recording multi-week lows. Specifically, euro/dollar shed 1.6% during the week ending February 9, experiencing its worst weekly performance since November 2016. Euro/dollar and pound/dollar were up by 0.3% and 0.2% at 1.2269 and 1.3869 respectively. Dollar/yen was 0.15% down at 108.62. This compares to Friday's five-month low of 108.03.

STOCKS: European equities were in the green, with every single major blue-chip index being comfortably in positive territory. The UK's FTSE 100, German DAX and French CAC 40 were up by 1.2%, 1.8% and 1.45% respectively after last week's sell-off that saw them post multi-month lows. Even the Italian FTSE MIB, which underperformed, was up by a hefty 0.8%. The pan-European Stoxx 600 was up by 1.5% at 374.04 and at a relative distance to Friday's five-month low of 367.50, with all sectors comprising the index being in the green. Meanwhile, the blue-chip Euro Stoxx 50 traded higher by 1.5% as well. Also, the eurozone volatility index declined from the peaks hit last week. Futures on the Dow, S&P 500 and Nasdaq 100 traded higher by 1.1%, 1.1% and 1.0% respectively, pointing to a higher open on Wall Street. It remains to be seen whether positive momentum will be maintained or whether this is a knee-jerk "buy the dip" reaction, with more weakness following in the days to come.

COMMODITIES: WTI and Brent crude were up by 1.75% and 1.3% respectively. The notable gains for the two benchmarks come after considerable declines in previous days that saw them touch a one-and-a-half-month and a two-month low of $58.07 and $61.77 per barrel respectively on Friday. The fall in preceding days came on the back of increasing expectations of US production strongly reentering the market, curbing efforts by OPEC as well as some non-OPEC members to tackle oversupply issues that acted as a drag on prices in the past. Monday's rise saw WTI recapture the $60/barrel level. Gold traded higher by 0.3%, at $1,320.76 an ounce. Last week, the precious metal touched a one-month low of $1,306.81.

Day ahead: Stocks remain in focus; US Federal Budget balance and OPEC monthly report due

Equities are gathering the lion's share of attention during Monday's trading, following last week's unrest that saw US stocks recording their worst weekly performance in around two years. The absence of significant releases out of major economies as well as the earnings season which remains underway, are additional factors keeping investor focus in stock markets.

The US's Federal Budget balance for the month of January is due at 1900 GMT. A budget surplus of $51 billion is anticipated during the month after a $23bn deficit in December. Discussions on the budget balance and debt sustainability are receiving renewed interest in the world's largest economy, especially after the Trump administration ratified a package of tax cuts that will add $1.4 trillion over 10 years to the national debt which currently stands around $20tr. According to some forecasters, general gross government debt to GDP is estimated to stand around 120% in 2018.

Policymakers' appearances as the day unfolds include Bank of England Monetary Policy Committee (MPC) member Ian McCafferty, who is scheduled to speak at 1630 GMT, and Reserve Bank of Australia Assistant Governor Luci Ellis who will be giving a speech at a forecasting conference at 2150 GMT.

In energy markets, OPEC's monthly report due later on Monday could attract some interest. The release covers major issues affecting international oil markets, looking at key developments as well as supply and demand considerations, and providing an outlook for the coming year. The report lacks a fixed time of release.