Sample Category Title

GBPUSD Still Weekly Bearish Below 1.3892 Level

The British pound is struggling to find upside traction against the greenback, after being swiftly rejected from the 1.3870 region during the European trading session. The GBPUSD pair has broadened its daily trading range, with price-action now moving between the 1.3830 to 1.3870 technical regions. Financial markets are increasingly looking towards ongoing Brexit negotiations on Monday, with downside pressures prevailing while the pair trades clearly below the 1.3892 resistance level.

The GBPUSD pair remains bearish while trading below the 1.3892 level, further losses towards 1.3830 and 1.3775 seem possible.

Should the GBPUSD pair move above the key 1.3892 level, buyers may push price-action back towards the 1.3938 and 1.4000 levels.

USDJPY Still Bearish Below 108.98 Level

The U.S dollar remains on the back foot against the Japanese yen in early week trading, despite a return to risk-on trading sentiment in the broader market. The USDJPY pair is currently range-bound between the 108.50-70 region, as traders remain cautious ahead of the release of preliminary fourth quarter GDP numbers from the Japanese economy. Heading into today’s U.S trading session, downside pressures are likely to prevail whilst the pair trades below the key 108.98 level.

The USDJPY pair remains intraday bearish while trading below the 108.98 level, key downside support is located at the 108.28 and 107.80 levels.

Should the USDJPY pair start to trade above the 108.98 level for an extended period, we may see a correction back towards the 109.30 and 109.78 resistance areas.

FX And Equities Brace For A Bumpy Week

Monday February 12: Five things the markets are talking about

Investors are bracing for another bumpy ride this week after market volatility has returned with a vengeance, delivering the biggest rout in global stocks in a number of years.

Despite stocks getting a reprieve overnight, investor fears of interest rate hikes that started the market correction continues to persist.

Last week, the CBOE volatility index ended almost three times higher than its Jan. 26 level. The ten-year Treasury yield finished last week atop of where they started at +2.85%.

Stateside, this week's inflation report – U.S consumer-price data on Wednesday – could be the catalyst for a major struggle between equities and bonds that triggered the initial market turbulence.

Elsewhere, while the coming week is absent of G10 central bank meetings, there are a number of important economic indicators to be released. In the U.K, consumer and producer price indexes and retail sales for last month should be a challenge for the pound (£1.3560). While in Japan, its first estimate of Q4 growth along with last month's producer price index and December's machinery orders (a proxy for capital spending) should be capable of moving the yen (¥108.70).

Later today, President Trump will deliver his 2019 budget blueprint.

1. Stocks breath a 'sigh of relief'

Global equities overnight have found some temporary support while volatility remains elevated.

Note: In Japan, equity markets were closed due to a bank holiday Feb. 12, while Chinese New-Year celebrations for the 'Year of the Dog' begin (Feb 15-21) and follow across much of Asia, including Hong Kong, Taiwan, Singapore, Malaysia and Indonesia.

Down-under, the Aussie S&P/ASX 200 was down -0.6%, weighed down by a fresh -1.6% drop in the energy sector, while in S. Korea, the Kospi rallied +0.4%.

China and Hong Kong stocks rebounded after last week's aggressive sell-off. In China, the Shanghai Composite index was up +0.8%, while China's blue-chip CSI300 index was up +1.3%. In Hong Kong, the Hang Seng Index was up +0.71%.

In Europe, regional indices are trading sharply higher across the board following on from a sharp rebound on Wall Street Friday and positive Asian markets.

U.S stocks are set to open deep in the 'black (+1.2%).

Indices: Stoxx600 +1.5% at 374.1, FTSE +1.2% at 7181, DAX +1.9% at 12336, CAC-40 +1.5% at 5153, IBEX-35 +1.5% at 9785, FTSE MIB +1.1% at 22404, SMI +1.8% at 8831, S&P 500 Futures +1.2%

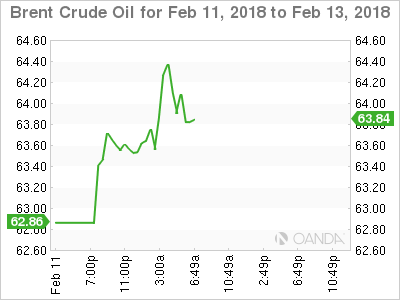

2. Oil prices rally +1%, gold higher

Oil prices start the week better bid, recovering some of this month's steep losses as global equities find some firm footing after last week sea of red.

Brent crude futures are at +$63.54 per barrel, up +75c, or +1.2% from Friday's close. U.S West Texas Intermediate (WTI) crude futures are at +$60.04 a barrel – that's up +84c, or +1.4% from the close.

The stronger prices came after crude registered its biggest loss in two years last week as global stock markets slumped.

Nonetheless, rising U.S production continues to undermine the efforts led by the OPEC and Russia to tighten markets and prop up prices.

Note: U.S oil production has rallied above +10m bpd, overtaking top exporter Saudi Arabia and coming within reach of top producer Russia.

There are also strong signals the output will rally further. Data on Friday showed that U.S energy companies added 26 oilrigs looking for new production, boosting the count to +791, the highest since April 2015.

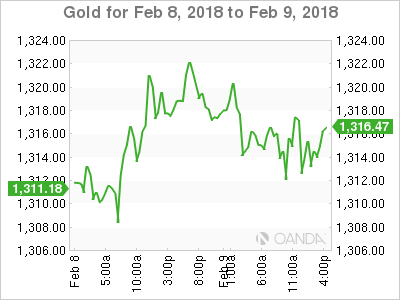

Ahead of the U.S open, gold prices have edged a tad higher as the dollar eased against G7 currency pairs after last week's rally. Expect investors to take their cues from this weeks U.S inflation data. Spot gold is up +0.3% percent at +$1,320.19 an ounce.

Note: Prices touched their lowest since Jan. 4 at +$1,306.81 last week.

3. Sovereign yields creep higher

U.S and eurozone government bond yields have edged higher overnight, heading back towards multi-year highs on unease that a pick up in inflationary pressures globally and a strong domestic economy will encourage the ECB and the Fed to signal to be more aggressive than originally priced in at the beginning of the year.

In Europe, bond yields across the bloc were +1-2 bps higher in early trade, while in the U.S the 10-year note trades atop of its four-year highs.

In Germany, the 10-year Bund yield is up almost +2 bps at +0.77% and within sight of its nearly three-year high hit last week at around +0.81%. The yield on the U.S 10-year note has rallied +4 bps to +2.90%, the highest in more than four years, while in the U.K, the 10-year Gilt yield has gained +4 bps to +1.605%.

4. The U.S dollar's quiet trading session

A broad-based flight to safe haven, such as U.S treasuries or the Japanese yen (¥108.70), has not happened to date despite the recent turmoil on equity markets.

The dollar 'bulls' are looking for the USD to rally this week, despite financial market volatility to remain high near-term as looser U.S fiscal policy and upside risk to U.S. inflation raises concerns.

Overnight, FX saw a quiet session ahead of some key inflation data this week (U.K Jan CPI Feb 13 and U.S Jan CPI on Feb 14).

Note: The recent pick up in global bond yields has been led stateside, while capital market wait for more details from President Trump's budget and his infrastructure plan.

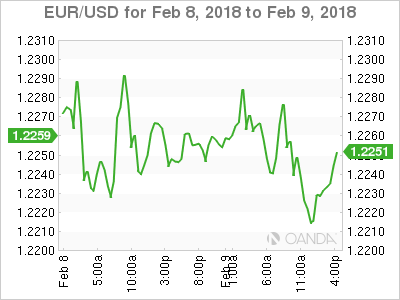

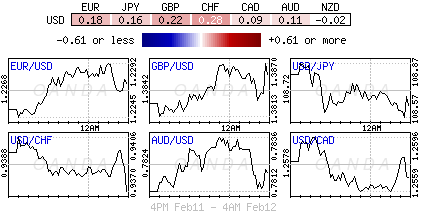

EUR/USD (€1.2272) is little changed, but holding below the psychological €1.23 handle. On the weekend, ECB's Nowotny (Austria) reiterated the concerns about attempts by the U.S to politically influence the exchange rate.

GBP/USD (£1.3860) trades atop of Friday's close despite the BoE having turned more rates 'bullish' last week. Dealers are now putting more weight on Brexit concerns as the U.K previously admitted that the growth potential of the economy had declined.

USD/JPY (¥108.70) is steady as Japanese markets were closed for a bank holiday.

5. Swiss inflation still super low

Data this morning showed that Swiss consumer prices slid -0.1% in January from December leaving the annual inflation rate at +0.7% and slightly below expectations.

Digging deeper, the decrease compared with the previous month is due in particular to the decrease in prices for outpatient hospital medical services. Prices for air transport also declined, along with prices for clothing and footwear, in particular because of sales. In contrast, prices for overnight stays in hotels, heating oil and electricity increased.

Inflation is still low despite the Swiss National Bank's (SNB) efforts to raise it through negative interest rates and a willingness to intervene in currency markets.

Euro Quiet At Start Of Week

The euro has posted small gains in the Monday session. Currently, the pair is trading at 1.2266, up 0.12% on the day. It’s a light economic calendar to start the week, with only one release on the schedule. The US federal budget is expected to rebound and show a large surplus of $50.2 billion. This would mark the first surplus since September. There are no major indicators until Wednesday, when Germany releases Preliminary GDP and Final CPI, and the eurozone releases Flash GDP.

A rebound in the global economy has been a boon for eurozone exports, and this has boosted the bloc’s manufacturing sector. This was underscored by strong manufacturing reports out of France and Italy in December, which were released on Friday. Industrial production in both countries improved compared to November, beating the estimates. The Italian reading of 1.6% marked the strongest gain since August 2016. We’ll get a look at Eurozone Industrial Production on Wednesday. The November reading surged to 1.0%, marking a 3-month high. However, the markets are expecting a small gain of 0.1% in December.

German President Angela Merkel has reached an agreement with the socialist SDP to form a new government, but the price was steep, as the SDP extracted major concessions from Merkel, notably control of the powerful finance ministry. This will likely mark a shift in Germany’s eurozone policy, which had been marked by a conservative stance under former finance minister Wolfgang Schaeuble. The weaker members of the eurozone, such as Greece, will likely find a more sympathetic ear for financial help from the SDP than they did from Schauble. Many conservatives fear that the Olaf Scholz, who is expected to become finance minster, will not be as fiscally responsible as Schaeuble. On the weekend Scholz said that Germany should not dictate economic policies to other eurozone members. The coalition agreement still requires the consent of a majority of the 464,000 members of the SDP, and if the deal is rejected, Germany will likely be headed to new elections.

Oil And Gold Both Higher, As Stock Markets Remain On Radar

Investors around the globe will closely monitor how the stock markets perform throughout trading today, following the rollercoaster ride that the financial markets experienced last week.

Although it would not be an understatement to suggest that volatility in global stock markets has reached intense levels, I don’t think there is a reason to be overly concerned by the recent market fluctuations. Similar levels of volatility were not seen in other asset classes such as the currency markets, suggesting that this is a stock market story and not a sign of concern over global economic health.

It has been warned for quite some time that stock market valuations were over-stretched, therefore the sell-off was quite likely just a market correction.

USD looking at risk to slipping lower

The Dollar is appearing at risk to withdrawing some of its gains over the past week, as investors eagerly await the upcoming inflation data release due from the United States on Wednesday.

Investors are already expecting a probable US interest rate increase from the Federal Reserve over the next couple of months, meaning that a positive inflation reading on Wednesday would likely provide investors with assurances that another increase in US interest rates is around the corner.

Whether more assurances that the Federal Reserve will resume its commitment towards higher US interest rates is enough to convince investors to re-purchase the Dollar at these lower levels remains to be seen, because I feel that investors will be paying more attention towards whether a possible rise in global inflation expectations accelerates the motives of other developed central banks to raise their own interest rates.

Increased US interest rates were priced into the Dollar a very long time ago, and I feel that investors are instead more enthusiastic about the prospect of higher interest rates from the Bank of England and European Central Bank.

Gold attempting to recover momentum

One of the main reasons why I am not concerned that the stock market sell-off from last week was a sign of mass panic from investors is because of the limited buying interest in Gold, in spite of the heightened stock market volatility. Gold usually benefits from an increase in interest as a safe haven instrument during uncertain times in the market, but the lack of interest in Gold over the past week has surprised a few in the market.

I personally think that the losses in Gold last week can be seen as a positive factor, because it provides more confidence to investors that the sell-off in the markets was a correction, and not a sign of panic over the global economy.

WTI Oil finding support at $60

With the global financial market headlines over the past week focusing on stock market volatility, it has slipped under the radar that increased volatility in Oil saw the commodity suffer its worst decline in two years. Rising concerns over an increase in US production and a recovering Dollar have weighed heavily on the price of Oil.

Anxiety that OPEC members might soon announce an intention to consider increasing production output following optimism that the market oversupply has rebalanced could now come under question, following the recent indications of increased production from the United States. This could leave to the price of Oil finding support somewhere around $60 for the time being.

Technical Outlook: SPOT GOLD Bounces On Monday But Recovery Was So Far Limited, US Data Eyed For Fresh Signals

Spot Gold is in recovery mode at the beginning of the week and attempting to break above two-day congestion on Thu/Fri which was shaped in double-Doji.

Weaker dollar on signs of stabilization in global stocks inflated the yellow metal, but recovery attempts were so far limited.

Mixed studies on daily chart show lack of clearer near-term direction signal, as slow stochastic reverses from oversold territory, generating bullish signal, while 10/55SMA is forming above and increasing pressure.

Gold will be looking for further signals which could be provided from a number of economic indicators from the US which will be released this week.

US inflation numbers are in focus (due on Wednesday), as it is expected to provide further clues about the pace of raising US interest rates this year.

Stronger than expected CPI numbers would be an additional support to the Fed to accelerate rate hikes in 2018 and would put the yellow metal’s price under fresh pressure, while gold price could rise if inflation remains low.

Res: 1326, 1330, 1334, 1337

Sup: 1316, 1314, 1311, 1307

CRUDE OIL Decline Maintained

Crude oil slowly continues its fall, heading below the 60 range. Hourly resistance at 64.77 (11/01/2017) is distanced while supports stand at 55.82 (07/12/2017 low) and 53.89 (01/11/2017). Strong support is located at 55.82 (06/12/2017 low). Expected to keep increasing as demand remains strong.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Riding Higher

Silver reverses pattern, heading toward 16.50 The short-term technical structure is however negative oriented. Silver trades between hourly resistance at 17.07 (09/11/2017 high) and support at 16.03 (05/12/2017 low). The technical structure suggests further short-term decrease.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Slight Increase

Gold is recovering after its recent strong sell-off. Resistance is located at 1337 (12/09/2017) while further resistance remains at 1358 (08/09/2017). Supports are given at 1306 (04/01/2018 low) and 1290 (16/10/2017). The technical structure suggests however further downside moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Higher Push Maintained

Bitcoin is now retracing above 8200. Strong support stands at 5605 (13/11/2017 low).Hourly resistance remains at 12130 (18/01/2018 high). The short-term technical structure suggests further upside moves.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading above its 200 DMA (6'000 range)