Sample Category Title

AUDUSD Continues The Sell-Off, Next Critical Level 23.6% Fibonacci Mark

AUDUSD edged sharply lower over the previous six trading days, however, during yesterday’s session, the price snapped the steep losses and recorded a positive day, following the rebound on the lower Bollinger band around 0.7835.

Looking on the bigger picture, the pullback from the 32-month high of 0.8135 endorsed the bearish phase, while the short-term technical indicators are bearish and point to more weakness in the market. It is worth mentioning that the price has been holding within an ascending move since January 2016.

From the technical point of view, in the daily timeframe, the RSI indicator is pointing to the downside in the negative territory, while the MACD oscillator is falling in the bullish area with strong momentum, both suggesting further downside correction in the near-term.

Wednesday’s session started with a bearish movement and if price action holds below the 0.7900 critical level, there is scope to test the 23.6% Fibonacci retracement level at 0.7825 of the medium-term up-leg with the low of 0.6820 and the high of 0.8135. Clearing this key level could see additional losses towards the 0.7730 inside swing barrier.

In the event of an upside reversal, the 0.7950 resistance level, could as a barrier before being able to re-challenge the 0.8100 significant psychological level. A break above this level could drive aussie/dollar towards the aforementioned 32-month high.

Dollar Little Changed, US Equities Rebound But Is The Turmoil Over?

Here are the latest developments in global markets:

FOREX: The dollar index was marginally lower on Wednesday, experiencing little movement in the session, as investors' attention remained fixed on movements in stock markets.

STOCKS: US equity indices rebounded yesterday, temporarily alleviating some concerns that the sell-off seen earlier in the week would develop into something much bigger. The Dow Jones led the way, gaining an extraordinary 2.3%, while the Nasdaq Composite followed in its tracks, up by 2.1%. The S&P 500 rose 1.7%; the Dow and S&P experienced their best daily performance since January 2016 and November 2016 respectively, while the Nasdaq Composite climbed the most since October of last year. However, futures tracking the Dow, S&P and Nasdaq 100 are all currently in negative territory, suggesting that the recent volatility in stocks may not be over just yet. Japanese markets recovered today as well, but to a much smaller degree. The Nikkei 225 closed higher by only 0.2%, while the Topix gained 0.4%. The underperformance of Japanese indices may be owed to the recent safe-haven gains in the yen, as a stronger Japanese currency typically weighs on the profits of Japanese exporting firms. Turning to Europe, futures tracking the Euro STOXX 50 are currently up 1.2%, signaling that the rebound in the US may roll over into European trading too.

COMMODITIES: Oil prices recovered as well, with WTI and Brent crude being up 0.9% and 0.8% respectively. The modest rebound in oil prices was helped by the private API inventory data released overnight, which showed a drawdown in US stockpiles. Today, investors will turn their eyes to the official EIA inventory data – due at 1530 GMT. It will be interesting to see whether the recent surge in US oil rigs has started to translate into higher production. In precious metals, gold was up nearly 0.5%, as the broader market volatility heightened demand for the safe-haven asset.

Major movers: US stocks rebound; kiwi jumps ahead of RBNZ decision

Investors remained focused on US equity markets yesterday. After a very volatile session, the major US indices managed to assume a direction and close the day notably higher, recovering some of the losses they posted on Monday. Despite this rebound though, the turmoil may not be over yet, as futures tracking the major US indices are flashing red today.

Nonetheless, the fact that US markets closed positive yesterday is another factor reinforcing the argument that the recent tumble appears to be merely a correction following years of robust gains, and not the beginning of a bear market. Nothing major has changed fundamentally, with economic data and surveys confirming that the major economies are still on a very strong footing.

Kiwi/dollar jumped overnight, following the release of New Zealand's employment report for the fourth quarter, which was stronger than expected overall. Even though wages rose at the same pace as previously, the unemployment rate surprisingly fell, while the labor force participation rate rose by more than anticipated, showing that the nation's labor market continues to tighten at a rapid pace.

Despite the initial positive reaction in kiwi/dollar, the pair did not manage to maintain its upward momentum and gave back most of its gains in the following hours. A potential explanation for the pullback may be investors' jitters ahead of the RBNZ policy decision later today, at 2000 GMT. Although the Bank is likely to maintain a relatively neutral tone on policy amid mixed economic data (disappointing inflation, but strong labor market), it could toughen its language around the NZD, which has surged since the last meeting. Thus, investors may have opted to take some profits off the table ahead of the risk event and liquidate some of their long-NZD exposure.

Major movers: US stocks rebound; kiwi jumps ahead of RBNZ decision

Investors remained focused on US equity markets yesterday. After a very volatile session, the major US indices managed to assume a direction and close the day notably higher, recovering some of the losses they posted on Monday. Despite this rebound though, the turmoil may not be over yet, as futures tracking the major US indices are flashing red today.

Nonetheless, the fact that US markets closed positive yesterday is another factor reinforcing the argument that the recent tumble appears to be merely a correction following years of robust gains, and not the beginning of a bear market. Nothing major has changed fundamentally, with economic data and surveys confirming that the major economies are still on a very strong footing.

Kiwi/dollar jumped overnight, following the release of New Zealand's employment report for the fourth quarter, which was stronger than expected overall. Even though wages rose at the same pace as previously, the unemployment rate surprisingly fell, while the labor force participation rate rose by more than anticipated, showing that the nation's labor market continues to tighten at a rapid pace.

Despite the initial positive reaction in kiwi/dollar, the pair did not manage to maintain its upward momentum and gave back most of its gains in the following hours. A potential explanation for the pullback may be investors' jitters ahead of the RBNZ policy decision later today, at 2000 GMT. Although the Bank is likely to maintain a relatively neutral tone on policy amid mixed economic data (disappointing inflation, but strong labor market), it could toughen its language around the NZD, which has surged since the last meeting. Thus, investors may have opted to take some profits off the table ahead of the risk event and liquidate some of their long-NZD exposure.

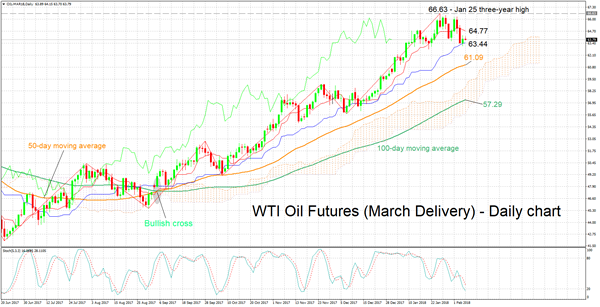

Technical Analysis: WTI oil futures retreat from 3-year high; bearish signal by stochastics in very short-term

WTI oil futures for March delivery have retreated a bit after hitting a more than three-year high of 66.63 on January 25. The Tenkan-sen line remains above the Kijun-sen, continuing to project a bullish picture in the short-term. However, the stochastics are giving a bearish signal in the very short-term as the %K line has crossed below the slow %D line and both lines are heading lower.

If the Energy Information Administration's weekly report shows a smaller-than-forecasted increase in crude stocks – or a drawdown of course – oil prices could head higher. In this case, resistance could come around the current level of the Tenkan-sen at 64.77. Stronger bullish movement would shift the focus to the late January high of 66.63.

Should crude inventories rise by more than projected however, then prices could weaken. In this scenario, the area around the Kijun-sen at 63.44 might provide support. Notice that price action is currently taking place not far above this level. A downside violation would turn the attention to the current level of the 50-day moving average at 61.09.

NZDUSD Intraday Analysis

NZDUSD (0.7306): The New Zealand dollar briefly tested the resistance level at 0.7333 which had previously served as support. The declines off this level could be validated on a close below the previous lows formed at 0.7257. A close below this level will indicate further bearish momentum that will see the Kiwi dollar targeting the next support at 0.7160. To the upside, in the event that NZDUSD closes above 0.7333, the consolidation near the top could continue.

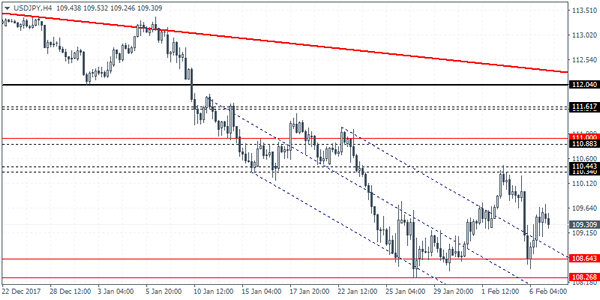

USDJPY Intraday Analysis

USDJPY (109.30): The USDJPY tested the support at 108.64 following the test of resistance at 110.44 - 110.34 previously. Following the rebound, USDJPY is seen forming a lower high which could indicate weakness in the currency pair. The declines could stall near the previous resistance level of 108.64. However, if price breaks down below this support further declines cannot be ruled out. To the upside, further gains are expected only on a breakout above 110.44 - 110.34 level. In the near term, USDJPY could be seen moving sideways within the range established.

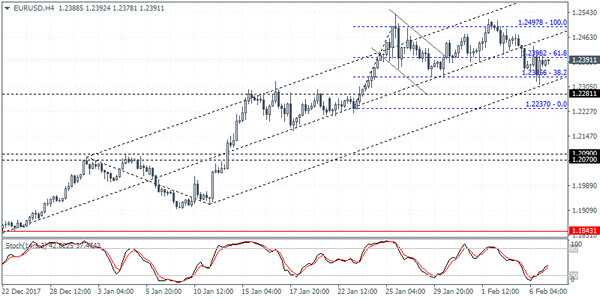

EURUSD Intraday Analysis

EURUSD (1.2391): The EURUSD formed a doji following two days of declines on the daily session. Price action suggests the potential for an upside move in the near term. The reversal comes as the EURUSD was seen briefly falling to the 1.2336 level. We expect to see some sideways consolidation taking place with the upside move likely to be limited. A lower high is expected on the 4-hour chart time frame for EURUSD to confirm the correction to the rally. As long as the previous highs at 1.2497 hold, we expect EURUSD to remain biased to the downside.

New Zealand Unemployment Data Slightly Better Than Expected

The equity market selloff extended to the Asian and then to the European session yesterday. However, the selling was subdued towards the U.S. session close. The volatility index (VIX) however remains elevated. The U.S. dollar was little changed on the day.

On the economic front, UK's services PMI data released yesterday showed a decline in the sector. Overall, with the UK's manufacturing and construction sectors also coming out weaker, the data indicated that the UK's economy got off to a subdued start in January. The Bank of England will be meeting this Thursday.

In the overnight session, New Zealand's unemployment data showed that the unemployment rate fell to 4.5% beating estimates of an increase to 4.7%. The quarterly employment change rose 0.5% which was a slower pace compared to a 2.2% increase in the previous quarter.

Looking ahead, the RBNZ will be holding its monetary policy meeting later this evening. No changes are expected to interest rates at today's meeting.

Currencies: EUR/USD Downside Test Rejected, At Least For Now

Sunrise Market Commentary

- Rates: A balancing act

Core bonds are looking for a new equilibrium after the past days heavy volatility. The US 10-yr yield tested the previous range top, but easily rebounded confirming that bond sentiment remains negative in the medium term. Fed speakers are wildcards today. What do they think about asset valuations and what are possible ramifications for monetary policy? - Currencies: EUR/USD downside test rejected, at least for now

Major FX cross rates are only modestly affected by the recent spike in global volatility. EUR/USD tested the 1.2323/35 support, but a break didn't occur. For now, there is no clear trigger for a directional move. The yen is unable to play its usual safe have role due to ‘verbal monetary interventions' from the BOJ

The Sunrise Headlines

- US stocks markets rebounded around 2% yesterday after a heavy two-day sell-off. Asian stock markets started on a strong footing this morning, but gains are evaporating towards the end of the trading session.

- The House passed a temporary spending bill Tuesday to keep the US government open until March 23 and fund the Defence Department through September as congressional leaders closed in on a longer-term agreement.

- CBOE Global Markets has defended its flagship Vix volatility index, after investors and analysts blamed products that seek to track the measure for exacerbating this week's ructions across global stock markets.

- New Zealand employment growth (0.5% Q/Q) slowed less than projected in Q4 2017, when a change of government caused a slump in business confidence and made firms more cautious about hiring. The jobless rate fell to a 9-yr low (4.5%).

- Wages of Japanese workers fell in December at their fastest pace in five months, in a possible sign that consumers could cut back on spending and further complicate the central bank's quest to reach its 2% inflation target.

- The UK economy is being bailed out by stronger growth in the euro area and the rest of the world, according to the NIESR. A better-than-expected global expansion accounted for about a third of the increase in UK GDP last year.

- Today's eco calendar only contains second tier EMU eco data. Fed governors Dudley, Kaplan, Evans and Williams are scheduled to speak. The US and Germany tap the market. The EC publishes new forecasts

Currencies: EUR/USD Downside Test Rejected, At Least For Now

EUR/USD downside test rejected, at least for now

Moves in USD remained modest yesterday given global volatility. EUR/USD dropped briefly below 1.2323/35 support in technical trade, but the pair rebounded as risk sentiment improved in US dealings. The pair closed at 1.2377. USD/JPY touched a ST correction low below 108.50 in Asia, but rebounded later as volatility eased. The intraday rebound of core yields was also a yen negative as the BOJ repeated that monetary conditions will remain extremely loose in the foreseeable future. USD/JPY closed the session at 109.56.

Equities opened with decent gains overnight, joining the rebound on WS, but positive momentum dwindled. So, the jury is still out whether the risk-off correction is really over. Japanese real wages declined 0.5% Y/Y in December, reinforcing the BOJ's case to maintain its ultra-easy policy. The data didn't cause any further yen losses. USD/JPY is drifting back south in the 109 big figure. EUR/USD is holding near 1.2375.

There are few data with market moving potential today. The forecasts from the European commission will confirm bright prospects for the European economy in 2018, but shouldn't have a big impact on markets.

Over the previous days, FX markets were relatively little affected by the rise in global volatility. The yen was unable to play its safe haven role the way it did in the past, as the BOJ stressed it won't join the global monetary normalization anytime soon. A break below USD/JPY 108.28 would indicate that markets are question the BOJ's approach. EUR/USD showed no clear pattern, holding a sideways trading range. For now, there is no obvious trigger to push the pair out of this range. For a downside break, EUR/USD probably needs the help of correction in EUR/JPY, even as yen gains don' t look easy currently. Technical picture: the dollar decline slowed of late, but no meaningful rebound occurred. EUR/USD 1.2537/98 remains the first topside resistance. A break would signal more trouble for USD short term. The 1.2323/35 support was tested yesterday , but no sustained break occurred. A break below 1.2165 would call off the ST downside alert (for USD).

EUR/GBP traded temporary north of 0.89 yesterday. Uncertainty on Brexit and technical considerations weighed on sterling. There are no important UK eco data today. Investors look forward to tomorrow's BoE meeting. A break above 0.8928 would deteriorate the ST picture for sterling, opening the way for a return to the 0.9000/0.9033 range top.

EUR/USD: first test of 1.2323/35 support rejected

Stock Market Recovery On Tuesday Still Tepid

Global Stock exchanges recovered somewhat on Tuesday, but as Asia closes, its equity markets are ending the session on the lows of the day, with the Japan 225 down to the 21600.00 area from a high of 22350.00. Whether this pattern continues into Europe remains to be seen. This switch back to risk-off mode has led to a demand in Yen, with USDJPY topping out at 109.708 before slipping to 109.131. Gold has recovered from a low of 1320.10 to 1330.30. Today, the focus of traders will be on Central Bank Decisions in New Zealand this evening and Central Bank speakers through the day. The economic calendar is light on market-moving data today, so expect another day of emotional trading.

US Fed’s Bullard spoke at an event in Kentucky on Tuesday. He noted that the link between the jobs market and inflation has broken down. He said that monetary policy today was closer to neutral. The Phillips curve effects are weak and the latest jobs report was good. The inflation scare triggered some of the market selloff. He said the Fed doesn’t need to do much now on key interest rates. Nominal wages aren’t good at predicting inflation. According to him, valuations look high compared to historic norms, especially in the tech sector. The market selloff was fast, possibly aided by technical trading and this was the most predicted market selloff of all-time. The Fed doesn’t need to do much now on interest rates. He also said, in relation to the Fed, the dot plot may be less useful now. USD crosses could experience volatility around this time in reaction to his comments.

US Trade Balance (Dec) was $-53.1B v an expected $-52.0B, from a previous $-50.5B, which was revised up to $-50.4B. EURUSD went to a high of 1.23469 and then sold off to 1.23251 when this data came out.

Canadian International Merchandise Trade (Dec) was $-3.19B v an expected $-2.20B, from a prior reading of $-2.54B, which was revised down to $-2.71B. USDCAD reached a high of 1.25663 before selling off to 1.25046 following this release.

Canadian Ivey Purchasing Managers Index (Jan) was 51.3 from 49.3 previously. Ivey Purchasing Managers Index s.a. (Jan) was 55.2 against an expected 61.0, from a previous 60.4.

New Zealand Unemployment Rate (Q4) was 4.5% v an expected 4.6%, from a prior 4.6%. Employment Change (Q4) was 0.5% v an expected 0.2%, from a prior 2.2%. Participation Rate (Q4) was 71.0% v an expected 70.8%, from a prior 71.1%. NZD can see a spike in volatility after this data is released.

Australian AiG Performance of Construction Index (Jan) was 54.3 from 52.8 previously. AUD can move to test key levels with this data acting as a catalyst.

Japanese Leading Economic Index (Dec) was 107.9 v an expected 108.1, from 108.3 previously. Coincident Index (Dec) was 120.7 v an expected 118.2, from 117.9 prior.

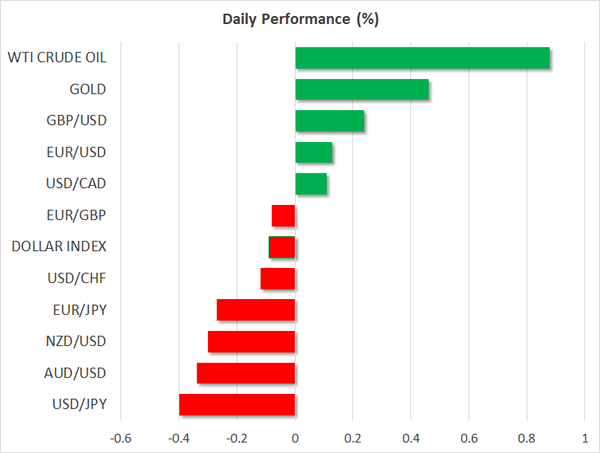

EURUSD is up 0.14% overnight, trading around 1.23942.

USDJPY is down -0.33% in the early session trading at around 109.200.

GBPUSD is up 0.13% to trade around 1.39630.

USDCAD is up 0.13% overnight, trading around 1.25064.

AUDUSD is down -0.41% overnight at around 0.78732.

Gold is up 0.49% in early morning trading at around $1,330.70.

WTI is unchanged this morning, trading around $63.71.

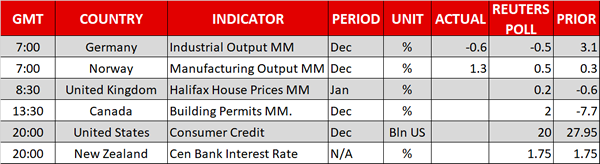

Major data releases for today:

At 08:00 GMT, ECB Non-monetary policy meeting.

At 09:00 GMT, ECB’s Lautenschlager will be speaking with his comments having the potential to influence trades on Euro and European assets.

At 13:30 GMT, US Fed’s Dudley will be speaking at an event about Banking Culture, jointly hosted by Thomson Reuters and the European American Chamber of Commerce in New York. USD crosses could experience volatility around this time in reaction to his comments and audience questions.

At 20:00 GMT, US Consumer Credit Change (Dec) is expected to be $20.00B from a previous $27.95B.

At 20:00 GMT, Reserve Bank of New Zealand Interest Rate Decision is expected to be left unchanged at 1.75%. The Rate statement and the Monetary Policy Statement will be released at the same time. NZD could see a spike in volatility after this data is released.

At 21:00 GMT, there will be a New Zealand RBNZ Press Conference discussing the rate decision and monetary policy statement.

At 22:20 GMT, US FOMC Member Williams will be speaking at a community leader’s luncheon in Honolulu, Hawaii. USD crosses and US assets may experience volatility around this time in reaction to his comments and audience questions.

At 22:30 GMT, Japanese Foreign Bond Investment (Feb 2) will be released, with a previous value of ¥41.1B. Foreign Investment in Japanese Stocks (Feb 2) was ¥-300.5B previously. JPY could move to test key levels with this data acting as a catalyst

Daily Wave Analysis: EUR/USD, GBP/USD Bullish Reversals At Fibonacci Support Levels

Currency pair EUR/USD

The EUR/USD bounced at the support trend line (green), which could indicate that the WXY (blue) correction within wave 4 (purple) has been completed. A break above the resistance trend lines (red) would confirm the end of wave 4 and could indicate an uptrend continuation within wave 5 (purple).

The EUR/USD The EUR/USD seems to have completed a bearish ABC (green) correction within wave 4 (purple). The bullish bounce at support (green) could indicate a wave 1 (blue) and the start a continuation of the uptrend. A break below the 100% Fib would invalidate the wave 1-2 pattern. be building a bearish ABC (green) correction within wave 4 (purple). A bullish bounce at support (green/Fibs) and bullish break above resistance (red) could start a continuation of the uptrend.

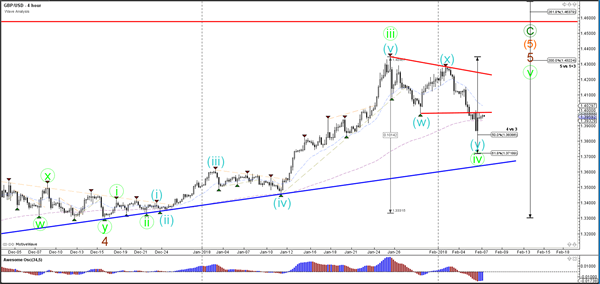

Currency pair GBP/USD

The GBP/USDbounced at the 50-61.8% Fibonacci zone which could still be part of a wave 4 (green) correction. A break above the previous top (red) could indicate a continuation rally.

The GBP/USD has probably completed a bearish ABC (grey) zigzag correction and is now building a wave 1-2 (blue) pattern.A break above resistance (red) could indicate the start of wave 3 (blue)

Currency pair USD/JPY

The USD/JPYis trapped betweenstrong support (green/blue) and resistance (red/orange). For the moment, a wave 1-2 (purple) seems the most likely but a bearish break below the bottom and 100% Fib invalidates the wave 2 (purple).

The USD/JPYneeds to break above resistance (red) before an uptrend continuation is likely.

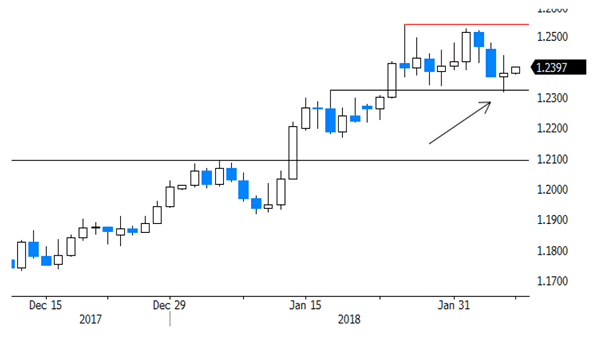

EUR/USD Has Stabilised At 1.2388

Market movers today

The general market conditions continue to be the main focus. Yesterday we saw the first signs of stabilisation – see more below.

In terms of economic data releases it is a quiet day but we have a series of Fed speeches today with the outgoing vice-chairman Bill Dudley (voter, neutral) being the most interesting. He will speak in a moderated Q&A and will probably get quest ions on the current market situation and hopefully he will shed light on whether the Fed has become more hawkish or just more confident in its out look, including its three hikes signal for 2018 after inflation and wage growth surprised slightly to the upside. T he Fed's Evans, Kaplan and Williams also speak.

German industrial production for January should be robust following strong factory orders data yesterday. Chinese FX reserves should show a decent increase due to valuation effects as the USD weakened sharply in January (raising the value of non-USD reserves).

In Europe , the EU Commission publishes new economic forecasts at 12:00.

In Scandi it is time for Norwegian and Danish industrial product ion (see next page).

Selected market news

After a rollercoaster day, S&P500 closed 1.75% higher yesterday after the big correcion Monday and the improved sentiment is also reflected in Asian markets, where most equity indices are flashing green (although the indices in Japan and Hong Kong fell during the night after a very strong opening). S&P500 future for March is trading unchanged this morning. Also VIX recovered after a bumpy day and is now at 30, which is st ill elevated compared to what we are used to but below the 50 peak yesterday. It is worth noting that the higher equity volatility has not spilled over significantly to other markets yet – the reason is probably that investors betting on calm markets (low VIX) have lost money causing VIX to rise even further. US 10- year Treasury yield has declined a few bp this morning to 2.78% after it recovered to 2.80% yesterday. Brent oil is trading at 67.4 dollars per barrel and EUR/USD has stabilised at 1.2388.

While it is difficult to say whether the market turmoil is over for now, we still believe that the correction is more technical than fundamental and we remain overweight in equities. The business cycle st ill looks strong, as PMIs are st ill high and optimism is high among businesses and consumers. We st ill believe the central banks will only tighten monetary policy gradually despite increasing concerns in the markets that inflation is on the rise. After having struggled with low inflation for so long, central banks will likely welcome higher inflation if it comes true.

In Germany, the IG Metal l agreed to a wage settlement yesterday, which shows that wage pressure is increasing but not going through the roof yet .

The US House of Representatives passed another short-term funding bill, as the current funding bill expires tomorrow, meaning the government may shut down again on Friday. While the bill is dead on arrival in the Senate, the Senate is working on a two-year funding bill, which may be put to a vote today or tomorrow. Overall, political analysts see the risk of a government shutdown as low.