Sample Category Title

Stock Bloodbath Continues In Full Swing, RBA Maintains Neutral Tone

Here are the latest developments in global markets:

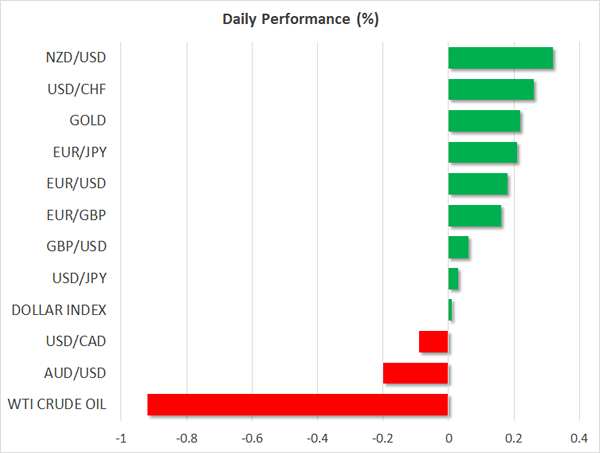

FOREX: The dollar index was practically unchanged on Tuesday, after posting some gains yesterday. The currency’s broader decline appears to have been halted, at least for now, as investors appear to be focused more on the collapse seen in stock markets.

STOCKS: US markets suffered one of their worst days on record yesterday. The Dow Jones led the collapse, falling by an astounding 4.6%. The S&P 500 was down 4.1%, its largest one-day decline since 2011, while the Nasdaq composite closed 3.9% down. According to futures, the Dow and the S&P could open lower today as well, though the same futures signal that the Nasdaq 100 may open slightly higher. The risk aversion rolled into the Asian trading session today as well. Japan’s Nikkei 225 and Topix indices fell by 4.7% and 4.3% respectively, while Hong Kong’s Hang Seng index is down 4.4%. European stocks are likely to feel the heat when they open today as well, with futures tracking the Euro Stoxx 50 currently down by 3.1%.

COMMODITIES: The energy market did not escape unscathed either. Both WTI and Brent crude are lower by 0.9% today, as the risk-off sentiment probably weighed on demand for the precious liquid. The safe-haven gold was one of the few winners today, up 0.2%, last trading near $1343 per ounce. Should risk aversion continue to prevail, the yellow metal could extend its gains. Immediate resistance may be found near $1350, with a potential upside break of that zone likely to open the way for gold’s recent highs at $1366.

Major movers: Equities suffer amid risk aversion; RBA stands pat

The collapse in major global equity markets accelerated yesterday. What is particularly interesting about the latest leg lower is that it appears to be driven primarily by risk aversion and a fear of loss, as opposed to rising US bond yields making bonds appear more attractive relative to equities. Whereas the last few days have been characterized by surging bond yields and falling equities, yesterday saw a simultaneous plunge in both stocks and Treasury yields. This implies that investors are becoming increasingly more concerned about the stock market and are seeking the safety of Treasuries, which is a typical market reaction in a risk-off environment.

Despite the big falls in major indices though, this still appears like a correction following an astonishing rally in equities, and not the beginning of a trend reversal. Indeed, it is not strange for stock markets to correct following such robust gains, especially as some investors may have taken the opportunity to take some profits off the table. The fact that it has been so long since a major correction occurred possibly plays into this as well.

The key question on everyone’s mind now should be: how low can equity markets go before willing buyers appear to halt the decline? It is important to note that with bond yields being on the rise overall, and equities falling, money is flowing out of both the bond and the stock markets. Thus, it appears some investors may be sitting on more and more cash, which will probably be looking to reenter the market at more favorable levels.

Overnight, the Reserve Bank of Australia (RBA) remained on hold, as was widely anticipated, and maintained a relatively neutral tone on policy. The Bank remains concerned with the high level of Australian household debts, particularly because incomes are growing very slowly. As for the AUD, the RBA did not appear worried, simply reiterating that an appreciating exchange rate would be expected to weigh on growth and inflation. Overall, the key message was that not much has changed, and that any potential rate hike later this year would be highly dependent on incoming data, particularly as they relate to wages. The reaction in aussie/dollar on the decision was somewhat limited, but the pair was already on the back foot beforehand, following disappointing Australian data.

Elsewhere, in Germany, headlines yesterday suggested that the two major parties are very close to finalizing a coalition deal. The talks are expected to conclude today, with a potential coalition likely to alleviate some of the uncertainty surrounding the European political scene.

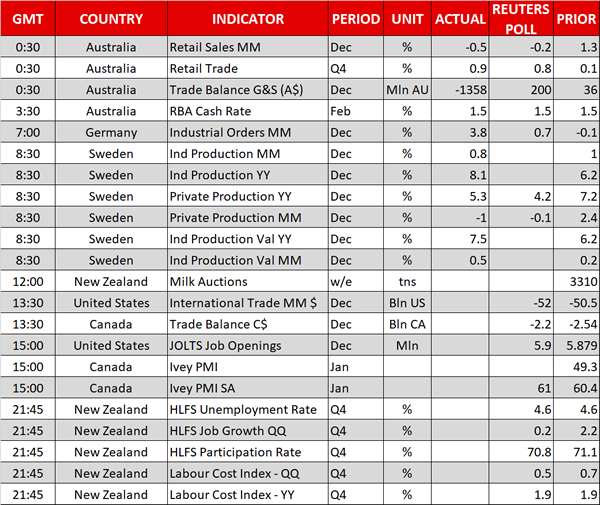

Day ahead: Busy day for kiwi traders as milk auction & jobs data are due; trade data out of US and Canada, with US JOLTS job openings also on the agenda

Kiwi traders will be paying attention to the outcome of the bi-weekly milk auction – New Zealand is a major dairy exporter – that is set to take place on Tuesday around 1400 GMT; the release is tentative, lacking a fixed time of release. Kiwi pairs will again come in the spotlight at 2145 GMT when New Zealand releases its Q4 2017 Household Labour Force Survey. The jobless rate is forecast to remain at 4.6% – its lowest since Q4 2008 – while jobs growth is expected to stand at 0.2% on a quarterly basis – this compares to 2.2% in Q3 – and the participation rate is projected to tick down. Data on labour costs will also be in focus.

The US and Canada will see the release of international trade data and trade balance figures for the month of December respectively at 1330 GMT. December’s JOLTS job openings out of the US and January’s Ivey PMI out of Canada both due at 1500 GMT will also attract attention.

St. Louis Fed President James Bullard is scheduled to give a presentation on the US economy and monetary policy before the 29th Annual Gatton College of Business and Economics Economic Outlook Conference at 1350 GMT.

API weekly data on crude oil stocks are due at 2135 GMT.

In equity markets, the earnings season continues amid the broad equity selloff.

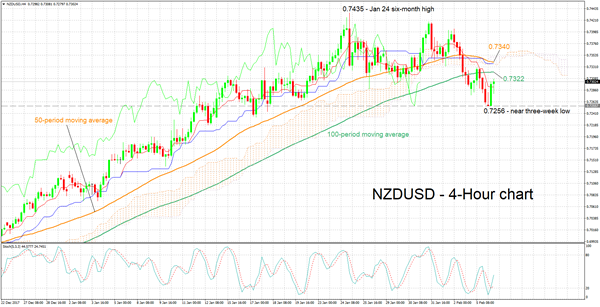

Technical Analysis: NZDUSD posts three-week low; stochastics give bullish signal in very short-term

NZDUSD is trading roughly 50 pips above a near three-week low of 0.7256 hit earlier on Tuesday. The negatively aligned Tenkan- and Kijun-sen lines on the four-hour chart are projecting a negative picture in the short-term. However, notice that the two have flatlined, this potentially being a sign that negative momentum has come to a halt. Also, the stochastics are giving a bullish signal in the very-short term, as the %K line has moved above the slow %D one.

Strong jobs data out of New Zealand later on Tuesday are expected to lead to long positions, pushing the pair higher. In this case resistance could be met around the 100-period moving average at 0.7322. Not far above this level lie the 50-period MA, Kijun-sen line and the Ichimoku cloud.

On the downside and in case of weaker data out of New Zealand, some support could come around the Tenkan-sen which failed to provide resistance on the way up and could instead act as support. Further below, the focus would shift to the low of 0.7256 recorded earlier in the day.

The milk auction that is due before the labour market data also has the capacity to spur movements in the pair

Technical Outlook: AUDUSD Fell Further After Downbeat Data/RBA Staying Pat, But Bears Show Signs Of Hesitation

The Australian dollar dipped to new nearly one month low at 0.7835 on Tuesday, extending steep pullback from 0.8135 peak into seventh consecutive day. The Aussie remains under pressure which increased on Friday after solid US jobs data inflated the greenback, with fresh pressure coming from downbeat Australian data on Tuesday. Australian central bank left the benchmark interest rates unchanged at 1.5% in a widely expected action and showing more positive stance regarding global and domestic growth, but remains concerned about low inflation and signaled that they may stay on hold for some time. Australian retail sales fell below expectations in December (-0.5% vs -0.2% f/c and upwards-revised previous month’s release at 1.3%), while a separate report showed Australia’s trade balance hit deficit of A$1.36 billion in December, vs forecasted surplus of A$0.25 billion and previous month’s surplus of A$0.03 billion. However, the Aussie shows signs of hesitation above new low as daily slow stochastic is deeply oversold and suggesting correction, while RSI turned from descend to sideways mode and supporting the notion. Bull-cross of 55/100SMA is forming below and also underpins. On the other side, broken 10SMA turned south and heading towards 20SMA in sideways mode, maintaining pressure. Former pivotal support, now resistance, at 0.7892 (Fibo 38.2% of 0.7500/0.8135 rally) caps for now and firm break here is needed to sideline immediate downside risk and generate stronger correction signal. Broken 30 SMA marks next barrier at 0.7927, followed by 20SMA (0.7983) and 10SMA (0.8013) regain of which would confirm an end of corrective phase. Conversely, repeated failures at 0.7892 would keep in play risk of extension towards 0.7778 (converged 55/100SMA) and 0.7743 (200SMA / Fibo 61.8% of 0.7500/0.8135 rally).

Res: 0.7892, 0.7927, 0.7953, 0.7984

Sup: 0.7835, 0.7817, 0.7778, 0.7743

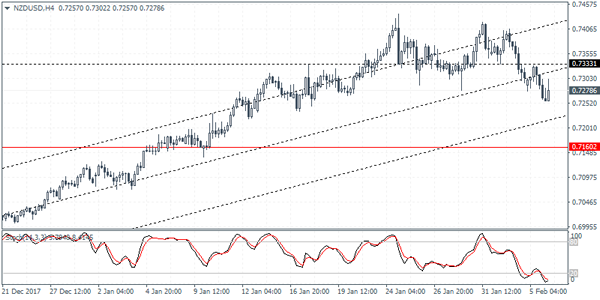

NZDUSD Intraday Analysis

NZDUSD (0.7278): The NZDUSD currency pair gapped lower on the day. Intraday retracement saw prices retracing back to fill the gap but eventually price settled lower. This marks a second consecutive session of a bearish decline in price. On the 4-hour chart, with NZDUSD breaking below the 0.7333 level, we expect to see a short term consolidation at this level. If 0.7333 is retested for resistance then we can expect to see further declines for the Kiwi dollar. The NZDUSD will be seen falling towards the first support level at 0.7160. Alternately, in the event that price manages to reclaim the 0.7333 level, we could expect to see some upside momentum being built up.

USDJPY Intraday Analysis

USDJPY (108.60): The USDJPY currency pair posted sharp declines late yesterday as price action was seen falling back to the 108.64 level of support. This marks a retest of the previously established support level. A rebound off this level is required in order to put the bias to the upside. However, the resistance level that has held up around 110.44 - 110.34 could be seen stalling the gains once again. To the downside, if the declines extend below 108.26 then USDJPY could be seen falling to the 108.00 level eventually.

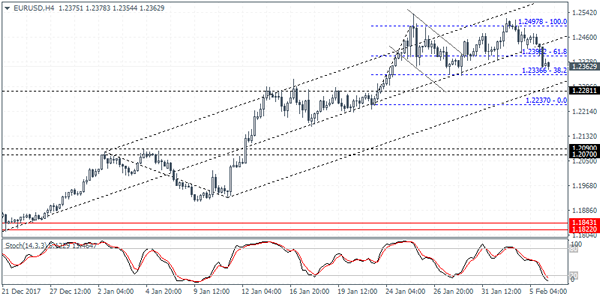

EURUSD Intraday Analysis

EURUSD (1.2362): The EURUSD has confirmed the failed bullish flag pattern with price action failing to breakout above the 1.2497 level. The declines yesterday pushed the euro to the previous support formed at 1.2398. A break down below this level is required for the EURUSD to confirm the downside. Initial support is seen at 1.2281 which could be tested in the near term. Following this, EURUSD could be extending the declines to the lower support level at 1.2090 - 1.2070 area of support which is pending a retest.

RBA Keeps Interest Rates Unchanged

The U.S. dollar was seen strengthening yesterday. Data from the U.S. showed that the ISM nonmanufacturing PMI rose to 59.9 beating estimates of 56.5. January's PMI data was also stronger than December's print of 55.9.

In the UK, the services PMI came out slightly better than expected. The services sector activity rose to 54.7 in January, beating forecasts of 53.6 and accelerating slightly from December's 53.9.

Earlier today, Australia's retail sales figures showed a 0.5% decline on the month. This was a bigger than expected decline of 0.2%. However, revisions to previous month's data showed an increase of 1.3%. The RBA's monetary policy meeting was also held earlier today. The central bank kept interest rates unchanged at 1.50%.

Looking ahead, New Zealand's unemployment data will be released later this evening. Estimates point to an increase in New Zealand's unemployment rate at 4.7% while the quarterly employment change is expected to rise at a slower pace of 0.4%

GBPUSD Bears Drive The Market, Downside Correction In Progress

GBPUSD fell as low as 1.3936, a level that is standing near the 20-day simple moving average during today’s Asian session. The pair tumbled aggressively in the last couple of days and the risk is still to the downside as price continues to move with weak movement. Also, the short-term technical indicators are bearish and point to more downside correction in the market.

In the daily timeframe, the parabolic SAR indicator is signaling further losses as the price is trading below it. The RSI indicator completed a steep downside movement, however, currently is pointing slightly to the upside. The MACD oscillator is heading down and posted a bearish crossover with its trigger line in the positive territory.

Remaining in the same timeframe, the bearish phase remains in play especially if cable continues to trade below the 1.3980 resistance level. The next pause to have in mind is the 23.6% Fibonacci retracement level at 1.3817 of the upleg from 1.2100 to 1.4345. A slip below that level could open the door for the 1.3660 support barrier, which is near the 40-day SMA.

To the upside, if price surpasses 1.3980, it could move towards the 1.4280 barrier. A break above the aforementioned obstacle could take the price towards the 1.4345 strong resistance level, the highest level since June 2016.

Currencies: USD Little Affected By Global Risk-Off Correction

Sunrise Market Commentary

- Rates: Huge sell-off on US stock markets triggers short squeeze in bonds

The sell-off on US stock markets accelerated yesterday evening (-4% and more) and caused a huge short squeeze in an oversold US Treasury market with yields ending up to 15 bps lower. Risk aversion could support core bonds somewhat short term and cause a revisit of previous range tops in yield terms. Any downleg in yields is expected to stop there. - Currencies: USD little affected by global risk-off correction

The focus for global trading remains on equities and bonds/yields. FX markets are little affected by the aggressive risk-off correction. EUR/USD stays within the established range. The euro is holding strong. USD/JPY loses slightly ground, but yen gains are still blocked by ongoing verbal monetary interventions from BOJ officials

The Sunrise Headlines

- US stocks suffered their worst fall in more than six years (-4% to -4.5%), erasing gains for the year. Asian equity indices can't escape the sell-off this morning and record losses of 3% to 5% (Japan).

- Industrial workers and employers in southwestern Germany struck a deal on pay and working hours, setting a benchmark for others. The agreement foresees a 4.3% raise from April and other payments spread over 27 months.

- ECB Draghi warned that the euro's recent surge creates 'new headwinds' and should be closely watched. The comments are the latest sign that a stronger euro could slow ECB efforts to unwind its giant monetary stimulus program.

- The Australian central bank kept its policy rate unchanged at 1.5%. RBA governor Lowe reiterated that a return of rapid wage growth remains a distant prospect despite strengthening business investment and a hiring bonanza.

- The House intelligence committee voted to release a memo that rebuts Republican criticisms of the FBI probe into Russian interference in the 2016 election, setting the stage for a potential clash with President Trump.

- German coalition negotiations were extended for a second day as SPD leaders seek to wring concessions on labor and health-insurance rules from Merkel's Christian Democratic-led bloc. A yes-or-no decision is expected today.

- Today's eco calendar contains the US trade balance. Austria, Germany, Greece (?), Finland (?) and the US tap the market. ECB Weidmann and Fed Bullard are scheduled to speak

Currencies: USD Little Affected By Global Risk-Off Correction

USD little affected by global risk-off correction

Equity sentiment turned negative in Europe yesterday, but the decline developed orderly. Bonds rebounded off last week's lows. The dollar continued trading mixed, gaining slightly ground against the euro, but struggling against the yen. Even so, the rise of the yen was hampered by soft comments from Japanese officials. This trading pattern basically persisted in US dealings as equities nosedived and as yields declined sharply. EUR/USD finished the session at 1.2367. The yen finally attracted some safe haven flows. USD/JPY closed at 109.09 (from 110.17 on Friday). Still, the rise of the yen was modest given global panic.

In extremely volatile trading, Asian equities are losing up to 5% (losses were even bigger earlier in the session). US yields decline further, but the pace slows. EUR/USD (currently near 1.2375) still holds a tight range. Yen gains remain modest. USD/JPY dropped to the mid-108 area, but already rebounded slightly. The swings on other markets (e.g commodities) are also modest. The Reserve bank of Australia kept its policy unchanged. Economic growth remains on track, but the RBA maintains a wait-and- see approach. AUD/USD (0.7850 area) lost further ground, but this is probably due to the risk-off sentiment.

Today's eco calendar is thin. The US trade deficit is expected at a huge $52.1 bn. Trade imbalances might become more important for FX trading but today's data will be overshadowed by the equity story. Current volatility is in the first place an equity correction. The impact on FX is modest. Dollar bulls/euro bears might be disappointed that risk-off didn't help the dollar more against. At the same time, investors are cautious to row against verbal monetary interventions from the BOJ, preventing further JPY gains. Over the previous days, we were looking for a technical sign in EUR/USD. This sign isn't there yet despite big swings on other markets. It suggests that the downside in EUR/USD remains quite solid for now. Technical picture: the dollar decline slowed of late, but no meaningful rebound occurred. EUR/USD 1.2537/98 remains the first topside resistance. A break would signal more trouble for USD short term. EUR/USD 1.2323/35 is a minor support A break below 1.2165 would call off the ST downside alert (for USD).

The sterling correction accelerated yesterday. Brexit noise, global risk-aversion and a disappointing services PMI were to blame. EUR/GBP rebounded to the 0.8870 area. Sterling's decline against the euro might slow ahead of the BOE meeting. EUR/GBP 0.8928 is first resistance.

EUR/USD: holding a tight range despite rise in global volatility

Volatility Continues As Risk-Off Reigns

The shock in stock markets continues, as yesterday was the worst since August 2011. US stock markets were some of the worst hit, with the US 30 (DOW) falling -4.60% or 1175.2 points. WTI Crude Oil futures fell 2.70% or $1.82, while Gold has a modest rise given the volatility, up $5.88 or 0.44% to $1339.00. Bitcoin was down again, at $7175, dropping $890, with a close below its 200-Day moving average. The USD strengthened along with the JPY, which outperformed all comers. Safety was sought in US Debt with yield moving lower, 10-year by 2.709%, -13.1 basis points. The high yield reached 2.8831%.

Spanish Markit Services PMI (Jan) was 56.9 v an expected 55.4, from a prior reading of 54.6.

German Markit PMI Composite (Jan) was 59.0 v an expected 58.8, from a previous reading of 58.8. Markit Services PMI (Jan) was 57.3 v an expected 57.0, from a previous reading of 57.0.

Eurozone Markit PMI Composite (Jan) was 58.8 v an expected 58.6, from a previous reading of 58.6. Markit Services PMI (Jan) was 58.0 v an expected 57.6, from a previous reading of 57.6. EURUSD fell to 1.24559 before recovering to 1.24746, while the Germany 30 Index fell to 12708.00 and then recovered to 12755.20 due to this data release.

UK Markit Services PMI (Jan) was 53.0 v an expected 54.3, from a prior reading of 54.2. GBPUSD closed at a daily high of 1.41501 just before the release of this data and started its decline when the data was released to reach a low of 1.39867 some hours later.

US Markit Services PMI (Jan) was as expected, unchanged at 53.3. Markit PMI Composite (Jan) was 53.8 v an expected 53.9, from a previous reading of 53.8. US ISM Non-Manufacturing PMI (Jan) was 59.9, beating the expected 56.5, from 56.0 previously, which had been revised up from 55.9. USDJPY continued its climb higher to 110.259 before selling off.

Australian Retail Sales s.a. (MoM) (Dec) was -0.5% v an expected -0.2%, from a prior 1.2%, which was revised up to 1.3%. Trade Balance (Dec) was -1358M, a large miss compared to the expected 200M, from a previous -628M, which was revised up to 36M. Imports (Dec) were 6% from 1% previously. Exports (Dec) were 2% from 0% previously. AUDUSD dropped from 0.78898 to 0.78692 following the data release.

Royal Bank of Australia Interest Rate Decision was left unchanged at 1.5%. The Rate statement was released at the same time. RBA said that AUD remains within the range it has been in over the past two years on a trade-weighted basis. Rising AUD would result in a slower economy and inflation. AUDUSD was moved down from 0.78740 to 0.78351 by this release.

EURUSD is up 0.10% overnight, trading around 1.23790.

USDJPY is down -0.14% in the early session trading at around 108.898.

GBPUSD is up 0.11% to trade around 1.39722.

USDCAD is unchanged overnight, trading around 1.25390.

AUDUSD is down -0.33% overnight at around 0.782881.

Gold is up 0.28% in early morning trading at around $1,342.99.

WTI is down -0.09% this morning, trading around $63.24.

Major data releases for today:

At 09:00 GMT, German Bundesbank President Weidmann will speak in Frankfurt. He will deliver opening remarks at a Buba lecture.

At 13:30 GMT, US Trade Balance (Dec) is expected to be $-52.0B from a previous $-50.5B.

At 13.30 GMT, Canadian International Merchandise Trade (Dec) is expected to be $-2.20B from a prior reading of $-2.54B.

At 13:50 GMT, US Fed’s Bullard will be speaking. USD crosses could experience volatility around this time in reaction to his comments.

At 15:00 GMT, Canadian Ivey Purchasing Managers Index (Jan) was 49.3 previously. Ivey Purchasing Managers Index s.a. (Jan) is expected at 61.0 from a previous 60.4. CAD pairs may be moved by this release.

At 21:45 GMT, New Zealand Unemployment Rate (Q4) is expected to be unchanged at 4.6%. Employment Change (Q4) is expected to be 0.2% from a prior 2.2%. Participation Rate (Q4) is expected to be 70.8% from a prior 71.1%. NZD can see a spike in volatility after this data is released.

At 22:30 GMT, Australian AiG Performance of Construction Index (Jan) will be released, with a prior value of 52.8. AUD can move to test key levels with this data acting as a catalyst.

The Higher VIX Leads To A Big Fall In Short VIX Products

Market movers today

The key focus in markets will continue to be the recent market rout and how far it can go.

German factory orders should confirm the picture of robust manufacturing growth. The data is very volatile though, so one should looked at the smoothed trend rather than one month's data.

US trade balance may come into focus as we get the December number and thus have the total for all of 2017. It may reveal that the trade deficit with China has reached a new high, triggering further ammunition for Trump to take protectionist measures against China.

In the afternoon, the Fed's Bullard (non-voter, dovish) will speak on the US economy and monetary policy. Bullard has proven one of the most dovish members of the Fed and cautioned against too aggressive rate hikes. He will vote on policy next year.

In Scandi, we get releases for Swedish industrial orders as well as Danish house prices.

Selected market news

Yesterday, we experienced a major risk off day in the financial markets. S&P500 fell 4.1% (the biggest decline since August 2011) erasing the gains in January thus ending the ‘honeymoon phase' in the stock markets where we have not seen a big market correction since Brexit. In Asia, it was also red across the board this morning. S&P500 futures have recovered slightly but are still down around 1%. US 10-year Treasury yields have continued to fall overnight and are now trading at 2.68% versus 2.88% at their peak yesterday. The equity volatility index VIX more than doubled from around 17 to 37, higher than during the US election, Brexit and the Chinese slowdown in early 2016 – we have to go back to the flash crash on 24 August 2015 to find a higher VIX. The higher VIX leads to a big fall in short VIX products. Brent oil is now trading slightly below 67 dollars per barrel (versus slightly above 70 at its peak).

The question is whether the big risk sell-off reflects an economic slowdown. We do not think so. Economic optimism is high and both European PMIs and the US non-manufacturing ISM are at very high levels, suggesting economic growth is still strong. However, an increasing concern is whether the time of low inflation is over, not least after the stronger-than-expected wage growth numbers from the US on Friday. It is not unnatural for markets to take a break after a long period of big increases (and especially the equity markets have had a very strong start to 2018), as investors take home some profits. Long equities have been a crowded trade for some time with markets looking stretched and overbought. Despite the big falls, the S&P500 is still marginal above its 100-day moving average and still close to 30% higher than before Trump won the election. While the correction may not be over yet, we think it is short-lived.

Yesterday, Jerome Powell was sworn in as Fed chair. In the short term, he is going to stick to the current monetary policy by raising the Fed funds target range three times this year (the first one in March) but look out for the increasing discussions about shifting to a price level target instead of the current inflation target, see Flash Comment US: Powell is “Yellen in disguise” amid discussions about price-level targeting, 24 January.