Sample Category Title

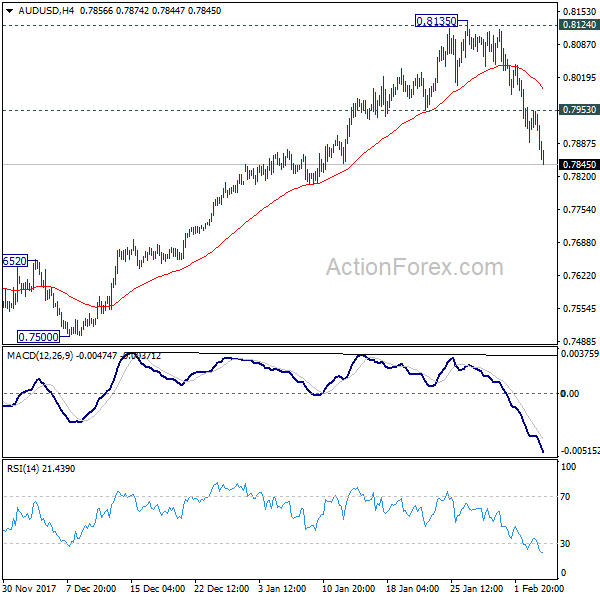

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7850; (P) 0.7901; (R1) 0.7929; More...

AUD/USD's fall from 0.8135 continues to as low as 0.7847 so far today and touches 55 day EMA (now at 0.7854). Intraday bias remains on the downside. Sustained trading below 55 day EMA will argue that rise from 0.7500 has totally completed and will pave the way to retest this support level. On the upside, above 0.7953 minor resistance will turn intraday bias neutral first. But recovery will likely be limited below 0.8135 resistance at first attempt.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

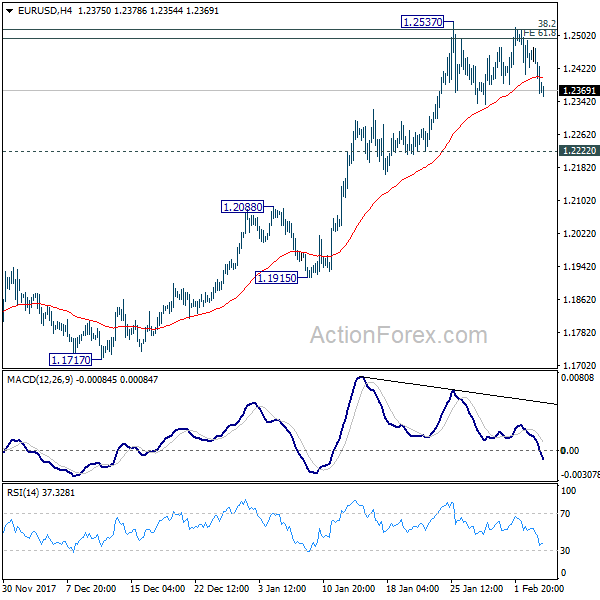

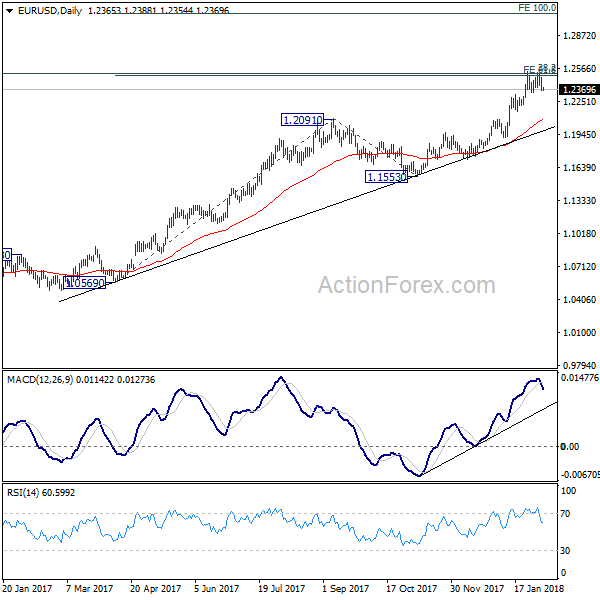

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2327; (P) 1.2401 (R1) 1.2439; More....

EUR/USD still staying in consolidation below 1.2537 and intraday bias remains neutral. As long as 1.2222 support holds, further rise is in favor. Sustained break of 1.2494/2516 will target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

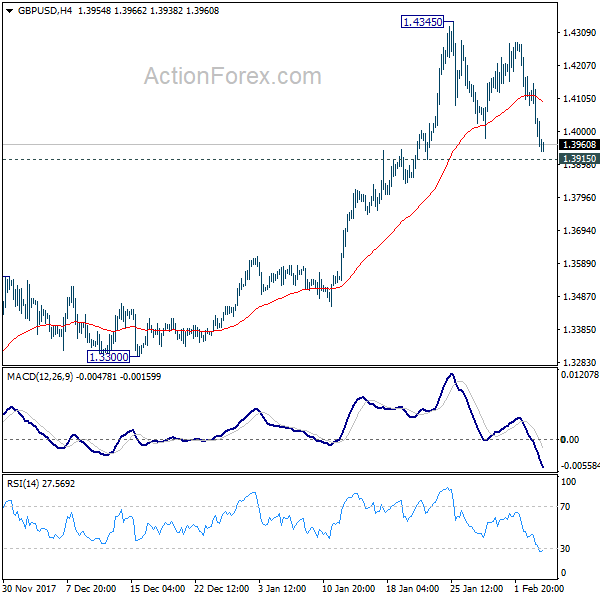

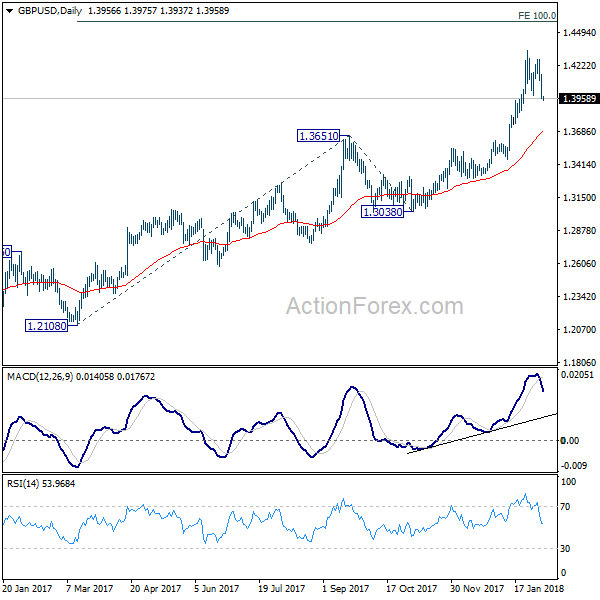

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3890; (P) 1.4020; (R1) 1.4088; More.....

GBP/USD's corrective pattern from 1.4345 is extending and intraday bias stays neutral. For the moment, we'd still expect downside to be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

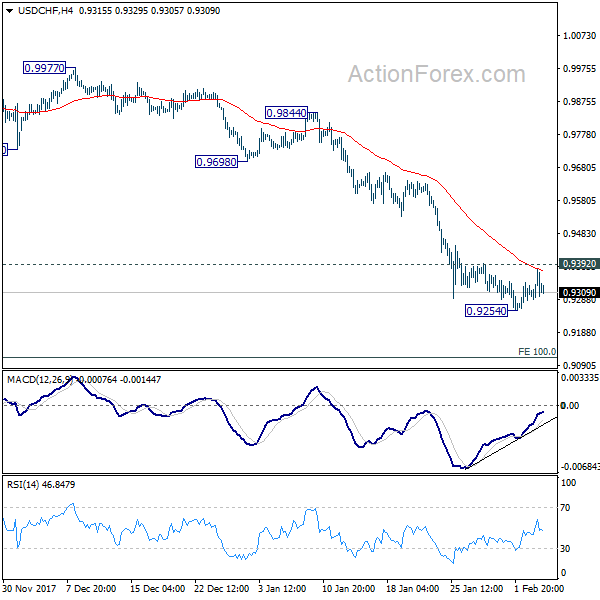

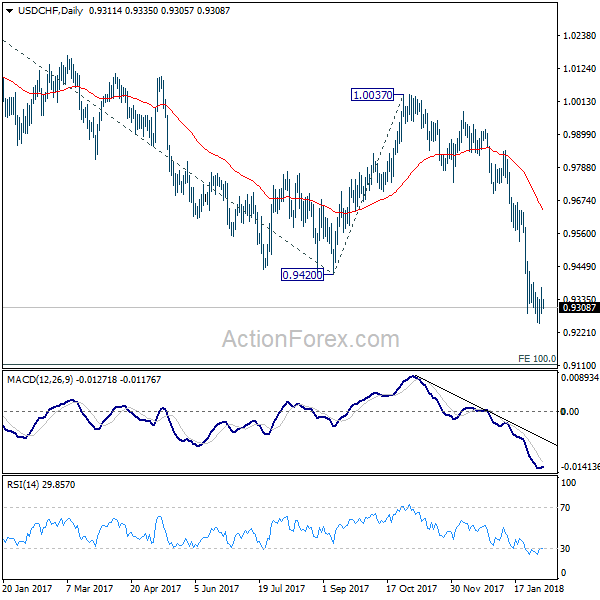

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9259; (P) 0.9298; (R1) 0.9345; More...

Intraday bias in USD/CHF continues to stay neutral first. But with 0.9392 minor resistance intact, deeper fall is expected. Below 0.9254 will extend recent fall from 1.0037 to next fibonacci projection level at 0.9115. On the upside, break of 0.9392 minor resistance, however, will indicate short term bottoming on bullish convergence condition in 4 hour MACD. That will bring stronger rebound back to 0.9420 support turned resistance and above.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.65; (P) 109.46; (R1) 109.94; More...

USD/JPY's sharp decline and break of 109.22 minor support indicates that rebound from 108.27 has completed at 110.47. More importantly, larger fall from 114.73 is still in progress. Intraday bias is flipped back to the downside for 108.27 first. Break will now likely resume the medium term correction from 118.65. That will send USD/JPY through 107.31 to 106.48 fibonacci level.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Stock Market Crash Intensified With DOW Scored Biggest Single Day Point Drop, Yen Firm

Selloff of global stock markets intensified further as DOW scored the largest single day point drop in history overnight. DOW declined -1175.21 points or -4.6% to 24345.75, comparing to 26616 record high made just six trading days ago. S&P 500 closed down -113.19 pts or -4.1% at 2648.94. NASDAQ lost -273.42 pts or -3.78% to 6967.53. 10 year yield hit new 4 year high at 2.862, before closing down -0.60 at 2.794. In Asian markets, Nikkei follows by dropping more than -5.2% at the time of writing. Hong Kong HSI is down -4.3%. In the currency markets, Yen is trading as the strongest major currency for the week, followed by Dollar and then Swiss Franc. Sterling is the biggest loser, followed by Canadian and then Aussie Dollar.

Just released, RBA left interest rate unchanged at 1.50% as widely expected. Aussie has practically no reaction to the release. Also from Australia, retail sales dropped -0.5% mom in December, trade balance indicated AUD -1.36b deficit in December.

DOW in larger correction towards 22351

Technically, DOW powered through key near term cluster support level at 24708.42 cluster support (38.2% retracement of 21731.12 to 26616.71 at 24750.41), as well as 55 day EMA. The development suggests that correction from 26616.71 is at at least one larger degree.

Fall from 26616.71 is probably correction the up trend from 2016 low at 15450.56. If that's the case, DOW could head to 38.2% retracement of 15450.56 to 26616.71 at 22351.24, which is close to 55 week EMA (now at 22569.93). That's the point where DOW would realistically get some solid support to form a base.

ECB Draghi: New headwinds have arisen from Euro volatility

ECB President Mario Draghi pledged to the European Parliament yesterday that the central bank will monitor exchange rate movement and the impact on inflation closely. He said that "while our confidence that inflation will converge towards our aim of below, but close to, 2 percent has strengthened, we cannot yet declare victory on this front." And, "new headwinds have arisen from the recent volatility in the exchange rate, whose implications for the medium-term outlook for price stability require close monitoring."

On the economy, Draghi sounded upbeat. He noted "the euro area economy is expanding robustly, with stronger growth rates than previously expected and significantly above potential." And, "these developments bode well for economic growth, as expansions tend to be stronger and more resilient when growth is broad-based."

UK delay of immigration paper criticized

In UK, the government decided to delay the paper regarding post Brexit immigration system and that triggered much criticisms from the business sector. The Deputy Director general of the Confederation of British Industry Josh Hardie said business would be "hugely frustrated" by the postponement. He said that "firms need time to plan for change" and, "It is perfectly possible to be clear on people's rights to work in the UK, for the transition period at least." And he urged the government to "commit now that people's rights to work won't change over the first two years from our date of departure from the EU."

Looking ahead

Germany will release factory orders and Eurozone will release retail PMI in European session. US will release trade balance later in the day. Canada will release trade balance and Ivey PMI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.65; (P) 109.46; (R1) 109.94; More...

USD/JPY's sharp decline and break of 109.22 minor support indicates that rebound from 108.27 has completed at 110.47. More importantly, larger fall from 114.73 is still in progress. Intraday bias is flipped back to the downside for 108.27 first. Break will now likely resume the medium term correction from 118.65. That will send USD/JPY through 107.31 to 106.48 fibonacci level.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:01 | GBP | BRC Sales Monitor Y/Y Jan | 0.60% | 0.70% | 0.60% | |

| 0:30 | AUD | Trade Balance Dec | -1.36B | 0.25B | -0.63B | 0.04B |

| 0:30 | AUD | Retail Sales M/M Dec | -0.50% | -0.20% | 1.20% | 1.30% |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 7:00 | EUR | German Factory Orders M/M Dec | 0.70% | -0.40% | ||

| 9:10 | EUR | Eurozone Retail PMI Jan | 53 | |||

| 13:30 | CAD | International Merchandise Trade (CAD) Dec | -2.3B | -2.5B | ||

| 13:30 | USD | Trade Balance Dec | -52.1B | -50.5B | ||

| 15:00 | CAD | Ivey PMI Jan | 60.4 |

Volatility Explodes (and Imploded)

As insane as the market moves were during regular trading hours on Monday, some extraordinary things happened in volatility products late. The yen was the top performer while the pound lagged. The RBA decision is due up next. The Premium video on today's wild market swings (biggest intraday point decline in the history of the Dow) will be posted later tonight. Stay tuned.

Betting against volatility is one of the infamous trades of all-time. It's so lucrative, so perfect that it pays over and over again – until it doesn't. Betting against volatility was the trade that took down the famed hedge fund Long Term Capital Management and resulted in a Fed-led bailout in 1998.

Now, it's an even bigger trade. In a recent poll from BAML, fund managers cited short-volatility as the most-crowded trade. The VIX fell below 9 in early January.

As Ashraf warned last week, volatility has spiked. The VIX closed at 37 on Monday as it doubled. But that's just where the story begins. Something happened in after-hours trade to the ETF VXX. It closed at 99 after opening at 115. It's designed to trade inverse from longer-dated VIX futures. It was a sharp, painful fall but it was orderly. In after hours trading, it fell to 28.

No one is quite sure what happened. There are some provisions for a liquidation in the ETF but it's not clear if the provisions were met. A similar move happened in SVXY, which is a similar ETF.

It's possible that some kind of fund liquidation and margin call event is underway but it could also be a liquidation that feeds back into volatility on Tuesday. If it's liquidated, then volatility is going to continue to spike Tuesday and it could get much uglier from here as funds are wiped out in the same way LTCM was.

If so, the yen is particularly attractive until the dust settles.

In the bigger picture, the RBA decision is at 0330 GMT. If they were to make a hawkish shift, it would come at a terrible time for equity markets and sentiment in general.

Not the Best Time to Raise RBA Rates

The Reserve Bank of Australia will meet for its first interest rate decision for 2018 on Tuesday but a rate hike will be probably off the table. Although the economy recorded solid growth and consumer and business surveys improved since December's policy meeting, household spending remained a risk, while an appreciating currency signals that this is likely not the right moment to tighten monetary policy, at least this time.

In the third quarter of 2017 private business and public investments enhanced the strength of the Australian economy, sending GDP growth to 2.8% on a yearly basis from 1.8% seen in the preceding quarter. The labor market also showed some improvement, with the number of employees rising strongly by almost 97,000 between November and December and the wage growth inching up to 2.2% y/y. However, this is not enough evidence to convince policymakers that a rate hike is appropriate as inflation continues to hold below the RBA's range target of 2-3.0% at 1.9%, missing repeatedly analysts' projections. Besides that, increased borrowing costs will squeeze consumption even further at times when homeowners are struggling to meet their debt obligations. According to recent estimates by Digital Finance Analytics, more than 924,000 or 30.0% of the households are under mortgage stress.

A stronger Australian dollar could also refrain policymakers from delivering higher interest rates. However, this seems not to be a reason to blame Australian policies but instead external factors including the strengthening US dollar and improved global conditions. Over the last two months, the dollar's weakness helped aussie/dollar to rally by 6.5% despite shrinking US-Australian bond yields spreads. Moreover, commodities exported from Australia such as iron, copper, and gold also saw significant gains from a tumbling greenback during this period providing substantial support to the aussie. Last but not least, economic growth in China added further impetus to the aussie rally as Australia's biggest export partner grew faster than anticipated, beating government's targets for 2017.

Therefore, considering the above, the RBA is more likely to leave rates at a record low of 1.5% for the sixteenth consecutive month, giving no boost to aussie/dollar unless the central bank alters its currency language in the rate decision statement following the anouncment at 0330 GMT. In case the RBA echoes its worries about the exchange rate, aussie/dollar could slip back to the 0.78 key-level and in the worst scenario break below the 200-day moving average to retest the 0.77 handle. On the other hand, hawkish messages could erase Friday's losses and drive the pair up to 0.80 with scope to reach the three-year high of 0.8135. Prior the rate announcement, retail sales and trade data out of Australia might have the potential to shake the market. A speech by the RBA Governor, Philip Lowe, at the A50 Australian Economic Forum on Thursday and the monetary statement due on Friday will be next in focus.

Dow Suffers Biggest Ever One Day Points Loss

US stock markets bounced back following the flash crash on Monday but the Dow still ended the session down 4.6%, having suffered the largest one day points loss ever. The Dow shedded more than 1,500 points at one stage, a large chunk of which occurred in a very short period of time.

Naturally there is a lot of questions being asked about the role of automated trading in the collapse and I'm sure the discussion will happen over the coming days but the important thing is that markets have recovered from the initial shock, while at the same time losing a considerable amount in the process.

With this being the second consecutive session in which we've had heavy selling, traders are looking for reasons for the decline and whether further downside is to come. Higher yields on the expectation that interest rates will rise faster than expected has been blamed until now and could be responsible for what will hopefully prove to be a brief and healthy correction.

Still, this is unlikely to be what Jerome Powell was hoping when he started his tenure as Fed Chair and already people are asking questions about whether investors were getting ahead of themselves in expecting three or more rate hikes this year. Once the dust settles we'll surely have a much better idea of whether higher rate expectations are truly to blame for these suddenly shaky markets and a storming return for volatility.

Gold Shrugs as US Services PMI Beats Expectations

Gold has posted small gains in the Monday session. In North American trade, the spot price for an ounce of gold is $1335.14, up 0.15% on the day. On the release front, the ISM Non-Manufacturing PMI climbed to 59.9, above the forecast of 56.5 points. This points to strong expansion in the services sector and marked a 3-month high. On Tuesday, the US releases JOLTS Job Openings.

On Friday, US employment numbers were strong, propelling the dollar to broad gains, including against gold, which dropped 1.2%. Nonfarm payrolls jumped to 200 thousand, beating the estimate of 181 thousand. Wage growth remained steady at 0.3%, edging above the estimate of 0.2%. Will the strong numbers lead to additional interest rate hikes? Minneapolis Fed President Neel Kaskkari said on Friday that the Fed might need to be more aggressive if wages continued to move higher. The Fed is planning to raise rates three times in 2018, but some economists are forecasting four hikes.

The Janet Yellen era is over at the Federal Reserve. On the weekend, Jerome Powell took over as chair, replacing Yellen. On Friday, Yellen waxed optimistic about the economy, saying that strong growth, a red-hot labor market and increased wage growth would require the Fed to gradually raise interest rates. Powell is expected to continue to Yellen's policies, so the markets are not expecting any dramatic shifts. However, the massive US tax cut will have a strong impact on the US economy, and the markets will be looking to the Fed for guidance. If the Fed sounds optimistic about the tax reform package, the US dollar could move higher.