Sample Category Title

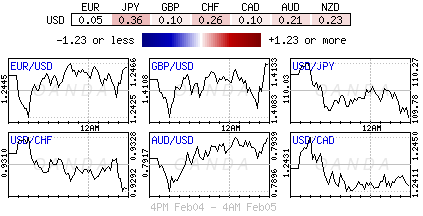

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4052; (P) 1.4165; (R1) 1.4229; More.....

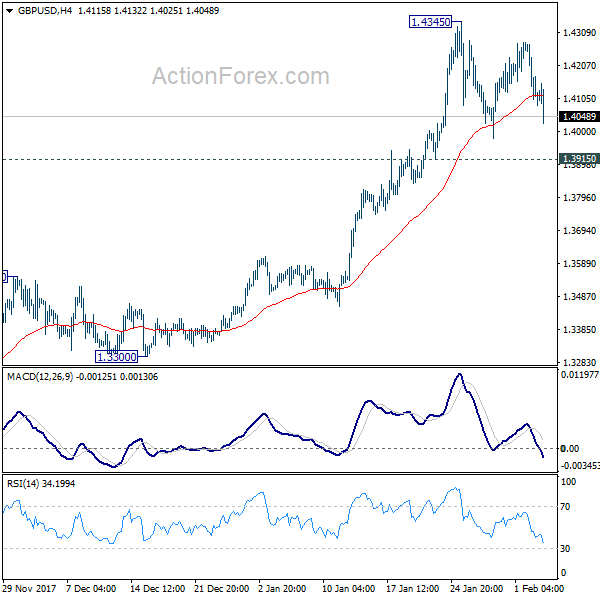

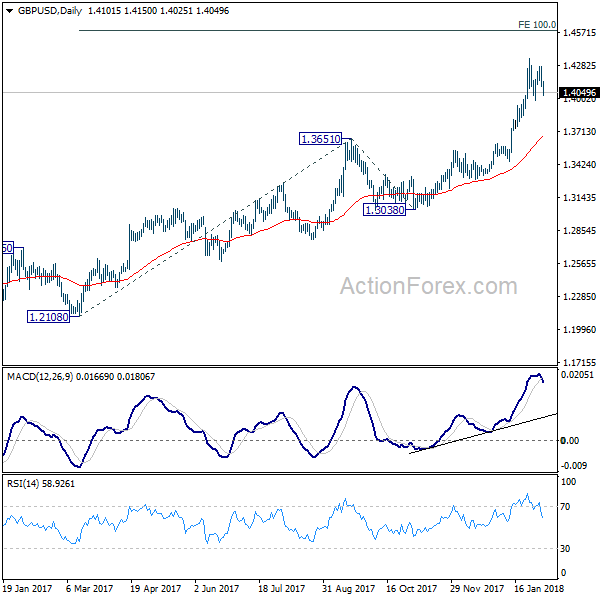

GBP/USD dips notably today but it's staying in established range below 1.4345. Intraday bias remains neutral for the moment. While further fall could be seen, downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Sterling Lower after PMI Services, Yen Stays Firm on Risk Aversion

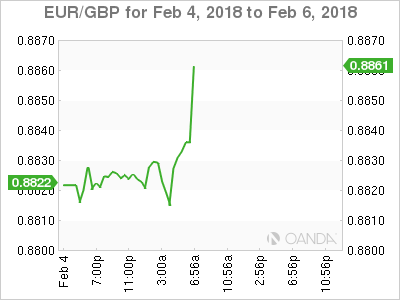

Sterling is trading broadly lower today as weighed down by weaker than expected services data. Concerns over UK's own internal split regarding Brexit ne got it ion is also weighing down on the Pound. Nonetheless, loss is so far limited. GBP/USD is holding above 1.4, EUR/GBP well below 0.9828, GBP/JPY also well above 151.95 support. The key to Sterling's trend will remain on the BoE Super Thursday. Yen is trading broadly higher today as global stock market rout continues but the Swiss Franc doesn't follow. And indeed, Aussie and Kiwi follow as the next strongest ones.

UK PMIs cast doubts on any imminent BoE hike

UK PMI services dropped to 53.0 in January, down from 54.2 and missed expectation of 54.1. Markit noted that, along with other PMI figures, the gauges indicated sharp slow down in economic growth in the UK. And, "the January slowdown pushes the all-sector PMI into dovish territory." Chief business economist Chris Williamson added that "with the survey also indicating weaker upward price pressures, the data therefore cast doubts on any imminent rise in interest rates." Released last week, PMI manufacturing dropped to from 56.2 to 55.3. More seriously, PMI construction dropped from 52.2. to 50.2.

BoE on Thursday will be the major focus for the week with quarterly Inflation Report featured. There are increasing speculations that BoE would pull ahead the next rate hike. In a Bloomberg survey, 13 out of 32 economists predicted the next hike coming as soon as in May. Another 5 predicted it to happen in August. The economic projections to be published in the Inflation Report will be a key to such market expectations. But the determining factor would be the outcome of the Brexit transition agreement with EU.

EU Barnier: Please respect rules of the Union

EU chief Brexit negotiation Michel Barnier is meeting UK Theresa May and Brexit Secretary David Davis for the first time since December today. Since last week, the debate on whether UK should remain within a customs union with the EU heated up, causing serious split inside Conservatives. Barnier said the EU "knew the line of the government". He emphasized "we have to respect the red lines of the British government, but they have to respect the rules of the Union".

ECB: Impact of US tax reform "highly uncertain and complex

ECB said in a short article today that the tax report in the US will provide a "significant fiscal stimulus" to growth in the U.S. and would be "positive in the short term." However, the impacts on the Eurozone are "highly uncertain and complex" including tax base erosion. It noted that "Lower U.S. corporate tax rates raise the tax attractiveness of the United States relative to other countries." And, "prior to the reform, the U.S. corporate tax rate stood above the rates of all large euro area countries, while, after the reform, it is close to the lower end of rates in those countries."

Eurozone Sentix showed first cloud in the blue sky

Eurozone Sentix investor confidence dropped to 31.9 in February, down from 32.9 and missed expectation of 33.2. Sentix said in the release that "the recovery process in the Eurozone is... continuing, although the first clouds are appearing in the blue economic sky". It added that "negotiations on forming another grand coalition aren't going down well with investors". And the figure was "a vote of no confidence in a grand coalition" in Germany. Also from Eurozone, Services PMI was revised up to 58.0 in January. Retail sales dropped -1.1% mom in December.

Germany coalition talk enters extra time

In Germany, Chancellor Merkel's CDU/CSU and the Social Democrats couldn't conclude the coalition negotiations in time to meet the self-imposed deadline of Sunday. The talks will enter into extra time today. On the positive side, agreements were made on housing and digital economy. But, it's believed that two key issues remain on the table, including SPD's demand to tighten up rules for businesses to grant temporary contracts, and aligning doctors pay between private and public health care.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4052; (P) 1.4165; (R1) 1.4229; More.....

GBP/USD dips notably today but it's staying in established range below 1.4345. Intraday bias remains neutral for the moment. While further fall could be seen, downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | CBA Australia PMI Services Jan | 53.8 | 55.1 | ||

| 0:00 | AUD | TD Securities Inflation M/M Jan | 0.30% | 0.10% | ||

| 1:45 | CNY | Caixin China PMI Services Jan | 54.7 | 53.5 | 53.9 | |

| 8:45 | EUR | Italy Services PMI Jan | 57.7 | 55.9 | 55.4 | |

| 8:50 | EUR | France Services PMI Jan F | 59.2 | 59.3 | 59.3 | |

| 8:55 | EUR | Germany Services PMI Jan F | 57.3 | 57 | 57 | |

| 9:00 | EUR | Eurozone Services PMI Jan F | 58 | 57.6 | 57.6 | |

| 9:30 | GBP | Services PMI Jan | 53 | 54.1 | 54.2 | |

| 9:30 | EUR | Eurozone Sentix Investor Confidence Feb | 31.9 | 33.2 | 32.9 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -1.10% | -1.00% | 1.50% | 2.00% |

| 14:45 | USD | US Services PMI Jan F | 53.3 | 53.3 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Jan | 56.6 | 55.9 |

European Stocks Join the Rout; RBA Policy Decision Next

Here are the latest developments in global markets:

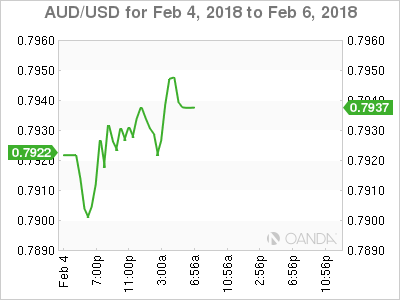

FOREX: The dollar index was little changed on Monday, last trading near the 89.10 level. Sterling/dollar was down more than 0.2%, pressured by the softer-than-anticipated UK services PMI for January. Dollar/yen fell nearly 0.3%, as the broader risk-off sentiment in equity markets strengthened the yen, which is typically regarded as a safe haven. Elsewhere, the aussie was 0.2% higher against the greenback ahead of the RBA's policy decision, due at 0330 GMT on Tuesday.

STOCKS: European markets were a sea of red on Monday. The blue-chip Euro STOXX 50 was down by 0.9%, while the pan-European STOXX 600 fell 1.1%. In Germany, the DAX was 0.8% lower, while in France, the losses of the CAC 40 exceeded 1.0%. In the UK, the FTSE 100 edged lower by 1.2%. The rout in stocks appears to be in full swing at the moment, as the acceleration in US wages has spooked markets that higher inflation is on the way, causing US bond yields to surge. As yields move higher, bonds finally produce adequate returns to keep investors interested, potentially leading them to reduce their exposure to equities.

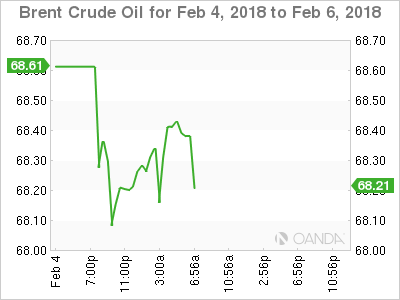

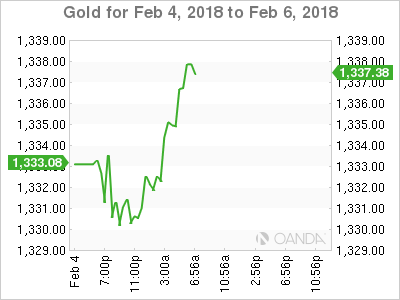

COMMODITIES: WTI crude oil traded 0.4% lower in the day, last seen near $65.00 per barrel after previously touching $64.62. Brent was down 0.9%, trading around $68 per barrel, with its intraday low being $67.69. In precious metals, gold advanced more than 0.3%, currently hovering near $1337 per ounce, perhaps buoyed by the risk-aversion prevailing in equity markets.

Day ahead: US data and Draghi's speech in focus ahead of RBA decision

In terms of economic data, the only major release left on the agenda is the US ISM non-manufacturing PMI, which is due at 1500 GMT. Expectations are for the print to reach 56.5 in January, from 56.0 previously. Coming on top of recent encouraging US data, an increase in the non-manufacturing index would be one more factor supporting the case for the Fed to deliver three (or more) rates hikes this year, and could thereby help the dollar to recover somewhat further.

As for public appearances, Jerome Powell is due to be sworn in to the position of Fed chair at 1400 GMT, taking over from outgoing chair Janet Yellen. Even though Powell is widely perceived as someone who will continue the Fed's current gradual approach to removing monetary accommodation, it is worth noting that markets have now started to contemplate the possibility of faster-than-signaled hikes in the future, amid signs that inflation might pick up soon.

At 1600 GMT, all eyes will turn to France, where ECB President Mario Draghi will address the European Parliament Plenary in Strasbourg. Several ECB officials have recently suggested that QE should begin to be unwound after September and it will be interesting to see whether Draghi echoes such remarks, especially after the Eurozone's core CPI rate unexpectedly ticked up in January. The euro will also be sensitive to any remarks regarding the exchange rate.

As for central bank meetings, the Reserve Bank of Australia (RBA) will announce its rate decision during the Asian trading session Tuesday, at 0330 GMT. Policymakers are widely anticipated to keep interest rates unchanged and as such, attention will turn to the phrasing of the accompanying statement. The Bank is not expected to signal any major policy shift, especially following the disappointing CPI prints for the fourth quarter. Still, it could well toughen its language around the AUD, which has rallied notably in recent months, threatening to act as a drag on economic growth and inflation. Any hints that the RBA is becoming uncomfortable with the AUD's strength are likely to act against the currency.

CAC Slides on US Inflation Concerns

The CAC index is down sharply in the Monday session. Currently, the index is at 5293.90, down 1.32% since the Friday close. On the release front, Eurozone and French Services PMIs improved in January, and both readings beat their estimates. Eurozone retail sales declined 1.1%, matching the forecast. Later in the day, ECB President Mario Draghi testifies on the ECB's Annual Report for 2016 before the European Parliament. On Tuesday, the Eurozone releases Retail PMI and France publishes the government budget deficit.

It's been a rough start for the CAC on Monday, as European markets are lower to start off the week. An excellent nonfarm payrolls report in the US has raised concerns of inflation, which the Fed could counter with a series of rate hikes. This in turn would make the dollar more attractive for investors, at the expense of the stock markets.

The CAC had a rough week, losing 3.0% last week. On Friday, Deutsche Bank shares dropped more than 5%, sending European stock markets into red territory, and the DAX is at its lowest level since September 26. The picture for Deutsche Bank is not a pretty one, as the stock price is at its lowest level since November, and the bank posted its third straight annual loss in 2017. A decline in investment bank revenue and the US tax reform bill contributed to a weak fourth quarter for Deutsche Bank shares.

With the eurozone economy continuing to perform well, there has been speculation that the ECB could wind up its asset-purchase program (QE) in September and shift to a normative policy, and perhaps raise interest rates. However, Mario Draghi and other ECB members have taken pains to reiterate that the Bank is in no rush to end QE. Last week, executive board member Benoit Coeure joined the chorus, saying that although QE "will not last forever" policymakers were in agreement "that we have to be patient and prudent because we are not yet where we want to be in terms of inflation". Investors would be well advised to keep a close eye on eurozone and German inflation numbers, as asset purchases could be extended beyond September if inflation remains well below the ECB target of around 2.0%.

US Futures Add to Friday’s Losses

US futures are trading back in the red again on Monday, adding to substantial declines seen on Friday when higher interest rate and inflation expectations weighed heavily on stocks.

We've seen a sharp increase in US bond yields over the last week after the Federal Reserve released a more hawkish than expected statement – alongside its monetary policy decision – and the jobs data reported a significant increase in earnings. Markets now have three rate hikes this year more than 50% priced in and some people are even anticipating a fourth, which is unusually ahead of current Fed forecasts.

While Friday's declines were larger than we've become accustomed to and the biggest drop in the Dow since June 2016, I don't think it yet signals that a large correction is underway. Small corrections are normal in markets, even if we haven't experienced them as often in recent years. Asian and European markets have suffered significant losses this morning in response to the US declines on Friday but we'll have to see over the coming days whether this will trigger more downside.

Bitcoin Testing $7,600 Lows Again

Bitcoin on other hand is struggling yet again at the start of the week and is trading back below $8,000 at the time of writing. Cryptocurrencies have seriously fallen out of favour since the middle of December and constant negative news flow and speculation of increased regulation has exacerbated the move lower, much in the same way that the constant flow of positive news stories aided the explosion higher.

In much the same way that picking the high on the way up proved to be extremely difficult, it's tough to establish a realistic low for bitcoin and others. It would appear cryptos can't rely on the speculators to drive prices higher again as its likely they've been severely burned over the last couple of months and may be reluctant to jump back in.

BoE "Super Thursday" Eyed This Week

This week will be a little quieter than the one just gone, although there are a few central bank meetings that traders will be keen on. The Bank of England meeting stands out, with it being accompanied by the quarterly inflation report and press conference with Governor Mark Carney. The central bank raised interest rates last year and many people expect another in 2018. With the economic outlook so uncertain though and inflation probably having peaked, I question whether another rate hike is as nailed on as some would suggest.

DAX Drops to 17-Week Low, Eurozone Retail Sales Slide

The DAX remains under pressure, and has started the week with strong losses. In the Monday session, the index is trading at 12,659.00 down 0.98% since the Friday close. On the release front, Eurozone and German Services PMIs improved in January. Both readings beat their estimates. Eurozone retail sales declined 1.1%, matching the forecast. Later in the day, ECB President Mario Draghi testifies on the ECB's Annual Report for 2016 before the European Parliament. On Tuesday, Germany releases Factory Orders.

It was a dismal week for the DAX, which slipped 4.3% last week. On Friday, Deutsche Bank shares dropped more than 5%, sending European stock markets into red territory, and the DAX is at its lowest level since September 26. The picture for Deutsche Bank is not a pretty one, as the stock price is at its lowest level since November, and the bank posted its third straight annual loss in 2017. A decline in investment bank revenue and the US tax reform bill contributed to a weak fourth quarter for Deutsche Bank shares.

With the eurozone economy continuing to perform well, there has been speculation that the ECB could wind up its asset-purchase program (QE) in September and shift to a normative policy, and perhaps raise interest rates. However, Mario Draghi and other ECB members have taken pains to reiterate that the Bank is in no rush to end QE. Last week, executive board member Benoit Coeure joined the chorus, saying that although QE "will not last forever" policymakers were in agreement "that we have to be patient and prudent because we are not yet where we want to be in terms of inflation". Investors would be well advised to keep a close eye on eurozone and German inflation numbers, as asset purchases could be extended beyond September if inflation remains well below the ECB target of around 2.0%.

EURUSD Buyers In Control Ahead Of Draghi

The euro remains largely unchanged against the U.S dollar, following the release of mixed macroeconomic data during the European trading session. Eurozone Services and Composite PMI’s beat expectations, while Retail Sales and Investor Confidence data declined. Financial markets now await European Central Bank President Mario Draghi, who is due to testify before the European Parliament later this afternoon. Mario Draghi’s testimony should create volatility in the EURUSD, and we are likely to see a clear break of the current 1.2432 to 1.2470 trading range.

EURUSD buyers retain control of the pair while price-action trades above the 1.2432 level, further upside towards 1.2491 and 1.2538 remain possible.

Should intraday sellers clearly breach the 1.2432 level, the EURUSD pair may decline towards the 1.2400 and 1.2385 levels.

GBPUSD Intraday Bearish Below 1.4151 Level

The British pound continues to drift lower against the U.S dollar, as traders remains cautious amidst UK political wrangling and fresh round of Brexit talks between UK and the EU negotiators. The GBPUSD pair is now trading around the 1.4100 mark, after suffering heavy trading losses on Friday following a solid U.S Non-farm payrolls report. Early today the UK services PMI for January fell to a sixteen-month low, further enhancing the bearish intraday sentiment around sterling.

The GBPUSD pair is bearish while trading below the 1.4151 level, further downside towards 1.4080 and 1.4036 cannot be ruled out.

Should the GBPUSD pair start to trade below the 1.4151 level, we may see a price correction back towards the 1.4189 level.

Equities Slump Deepens, Dollar Steady

Monday February 5: Five things the markets are talking about

Global stocks have extended their biggest decline in two-years overnight while the 'big' dollar steadies outright against G10 currency pairs. Sovereign treasury yields continue to creep higher, while crude oil prices again come under pressure as U.S explorers raised the number of rigs drilling for crude to the most since August.

This week is again dominated by monetary policy decision with four central banks meetings in the coming sessions – today, the Reserve Bank of Australia (RBA), Wednesday, the Reserve Bank of New Zealand (RBNZ) and the Reserve Bank of India (RBI) and its 'super' Thursday for the Bank of England (BoE) as it also publishes its quarterly inflation report.

Other data releases will focus on December industrial production (IP) and January composite PMI's. China will release January data for its merchandise trade balance and its consumer and producer price indexes. North of the U.S border, Canada will close out the week reporting its January labor force survey. It's December international trade balance is reported on Tuesday.

1. Stocks see red

In Japan, the Nikkei share average fell sharply on overnight as fear that U.S inflation may be finally gathering pace pound global equities. The Nikkei tumbled -2.5%, its biggest one-day drop since Nov 9, 2016, when President Trump won the U.S election. The broader Topix slumped -2.2%.

Down-under, Aussie shares fell overnight, dragged down by financial and materials. The S&P/ASX 200 index slid -1.6% ahead of Wednesday's Reserve Bank of Australia (RBA) rate decision.

In Hong Kong, stocks ended lower on overnight, but recouped much of their earlier losses sparked by Friday's slide on Wall Street. The Hang Seng index slumped -1.09%, while the Hang Seng China Enterprises index fell -0.43%.

In China, stocks bucked the region's tumble as the Shanghai Composite index ended the session up +0.73%, while the blue-chip CSI300 Index also reversed its earlier losses, closing up +0.1%.

In Europe, regional indices are trading lower across the board, but off the session lows as markets have faded a large part of the earlier move lower, on the back of a slight pullback in Euro Bond yields as well as a bounce in U.S futures.

U.S stocks are expected to open little changed.

Indices: Stoxx600 -1.0% at 384.1, FTSE -1.0% at 7366, DAX -0.5% at 12715, CAC-40 -0.9% at 5317 , IBEX-35 -0.6% at 10145, FTSE MIB -0.7% at 23048 , SMI -1.0% at 9132, S&P 500 Futures flat

2. Oil trades atop one-month lows, gold prices higher

Oil prices are under pressure for a second consecutive session overnight, as rising U.S output and a weaker physical market added to the pressure from a widespread decline across equities and commodities.

Brent crude futures are down -36c at +$68.22 a barrel, while U.S West Texas Intermediate (WTI) crude has fallen -13c to +$65.32.

Oil is caught up in the markets general risk-off move, not helped the strength of the U.S dollar in the past two trading sessions.

Adding to the pressure on oil, which hit its highest price in nearly three-years in January, has been evidence of rising U.S crude production, which could threaten OPES's efforts to support prices.

Data from the U.S government last week showed that output climbed above +10m bpd in November for the first time in nearly fifty-years, as shale drillers expanded operations.

Ahead of the U.S open, gold prices have inched higher as declining equities lend support to the yellow metal even though robust U.S. jobs data potentially increased the chances of more interest rate hikes this year. Spot gold is up +0.1% at +$1,334.23 per ounce, after declining -1.2% on Friday in its biggest one-day fall since early December.

3. Sovereign yields continue to back up

Investors on both sides of the Atlantic are dumping government debt, but for different reasons. In the U.S, investors see more inflation coming; while in the eurozone, they see stronger economic growth.

On Friday, the 10-year Treasury yield closed at +2.852%, the highest yield in two-years, compared with +2.410% at the start of the year. German 10-year sovereign Bunds have edged up to +0.701% from 0.430% over the same period.

Note: Inflation-linked Treasuries' (TIP's) show that almost two-thirds of the U.S bond selloff that started at the beginning of December is explained by inflation expectations.

Elsewhere, the RBA looks set to continue lagging the trend toward higher interest rates globally. It's first policy meeting this year on Tuesday will likely see the RBA's official cash rate steady at +1.5%, with interest in whether its guidance will be more upbeat reflecting a stronger job market.

Aussie policy makers continue to face the problem of weak wages growth, soft inflation reads and an elevated AUD (A$0.7934). Forecasts for the first interest rate hike have been pushed back lately.

4. Dollar under constant pressure

The U.S. dollar remains relatively contained after rebounding at the end of last week, when a strong non-farm payroll (NFP) suggested the currency's weakness might have gone too far, too fast.

The EUR/USD (€1.2426) has managed to eek out a small gain overnight as optimism continued to flow about a grand coalition in Germany – political parties have said to seek a grand coalition by tomorrow (Feb 6th).

GBP/USD (£1.4102) is little changed despite the Jan. U.K PMI Services reading missed expectations (see below).

USD/JPY 's strong correlation with U.S interest yields seems to have broken down as the pair tested ¥109.80 in the session overnight despite the BoJ's rhetoric that it would continue advocating an easy monetary policy.

Bitcoin (BTC) is down -6.7% at $7,637.

5. U.K services expansion slides to 16-month low, Europe expands

In the U.K, services PMI fell to 53, from 54.2 in December, below the expected consensus for an increase to 54.5. This morning's data is now following weaker-than-expected manufacturing and construction PMI data last week.

Note: This January slowdown pushes the all-sector PMI into 'dovish' territory as far as the Bank of England (BoE) monetary policy is concerned. The BoE announces its latest interest rate decision and inflation report on Thursday.

Elsewhere, the composite PMI for the eurozone in January was revised up to 58.8 from 58.6, hitting its highest level in a dozen years and further proof that the eurozone economy started this year on a very strong footing.

At a national level, Italy stood out, recording its highest reading in a dozen years, as businesses hired at the fastest pace in 17-years.

Note: The ECB will be encouraged to expect acceleration in wages growth that would help it meet its inflation target in the coming years.

Euro Yawns As German, Eurozone Services PMIs Improve

The euro is trading sideways on Monday, after an uneventful week. Currently, the pair is trading at 1.2463, up 0.06% on the day. On the release front, Eurozone and German Services PMIs improved in January. Both readings beat their estimates. Eurozone retail sales declined 1.1%, matching the forecast. Later in the day, ECB President Mario Draghi testifies on the ECB’s Annual Report for 2016 before the European Parliament. In the US, the sole event on the calendar is ISM Non-Manufacturing PMI. The indicator is expected to rise to 56.5 points. On Tuesday, Germany releases Factory Orders and the US publishes JOLTS Job Openings.

With the eurozone economy continuing to perform well, there has been speculation that the ECB could wind up its asset-purchase program (QE) in September and shift to a normative policy, and perhaps raise interest rates. However, Mario Draghi and other ECB members have taken pains to reiterate that the Bank is in no rush to end QE. On Wednesday, executive board member Benoit Coeure joined the chorus, saying that although QE “will not last forever” policymakers were in agreement “that we have to be patient and prudent because we are not yet where we want to be in terms of inflation”. Investors would be well advised to keep a close eye on eurozone and German inflation numbers, as asset purchases could be extended beyond September if inflation remains well below the ECB target of around 2.0%.

There was a changing of the guard at the Federal Reserve on the weekend, as Jerome Powell took over as chair, replacing Janet Yellen. On Friday, Yellen waxed optimistic about the economy, saying that strong growth, a red-hot labor market and increased wage growth would require the Fed to gradually raise interest rates. Powell is expected to continue to Yellen’s policies, so the markets are not expecting any dramatic shifts. However, the massive US tax cut will have a strong impact on the US economy, and the markets will be looking to the Fed for guidance. If the Fed sounds optimistic about the tax reform package, the US dollar could move higher.