Sample Category Title

Sell-Off Continues: You Can Hide But Can You Survive? | Tesco And Ryanair Under Focus

The biggest sell-off for the equity markets in nearly two years is here

A 10% correction could take place as this was long overdue

Dallas Fed President Robert Kaplan and New York Fed President William Dudley to speak

Prayers have been answered by the equities bears. The biggest sell-off for the equity markets in nearly two years is here as investors are reacting to surging global bond yields. Something which stood out last week for traders was that the sell-off was across all the 11 sectors in the S&P 500, something which we have not witnessed since 2016 (during the US election). Friday's equity markets rout is likely to extend as the futures of the US stock indices are indicating.

However, there isn't much to worry about because corporate profits are still rising and chances of US recession are remote. So this may only be a healthy pullback which the investors have been waiting for some time. A 10% correction could take place as this was long overdue. In other words, the long-term momentum for the equity markets is only easing off as these markets have been defying the Newton Law of Gravity.

Over in the US, after a strong US NFP data, in particular, the US wage growth number, has asserted more pressure on the Fed to adopt a policy which can address the rising bond yields. Dallas Fed President Robert Kaplan and New York Fed President William Dudley are going to provide more details about the Fed's monetary policy stance and the question among the investors would be if the pace of the interest rate hike would be gradual or if the Fed is going to adopt a more aggressive stance.

Investors are trying to make a sense of Janet Yellen's last interview with CBS during which she mentioned that valuations and real estate prices are overstretched. Does she mean that the stock market is a bubble? Perhaps, the upcoming Fed chairman Jerome Powell will have to address this question. Bond traders need to know if he is going to favour three or four interest rate hike this year.

TESCO

Traders are paying attention to Tesco's 2018 profit forecast of £1.58 for the year and the company's intentions are that it would reinstate dividend of 2 pence per share. The corporate is shaking its management once again, the CEO of the merging group, Booker, will be taking over the company's driving wheel. Charles Wilson, the current boss of Booker, is going to head the UK and Ireland operation for Tesco.

Insiders have a 0.01 percent stake. During the past six months, insiders have increased their holdings by 1.9 percent. The overall street consensus rating is equivalent to sell. During the month of January, Tesco's stock fell 3.6% while the peers dropped nearly by 2.9%.

RYANAIR

Another big surprise from Irish carrier, Ryanair announced a 750 million euro share buyback. The message is clear for investors, the company has strong books. It is going to stand at its position by assuring investors that it is determined to remain Europe's biggest low-cost airline. This is despite the fact that the staff cost would rise by 45 million euros this year as it has compensated its flight crews with higher wages. However, the potential threat remains for the airline as the pilot dispute is still not resolved. Nonetheless, the key ingredient which has helped the airline to fight higher fuel prices and higher wages is mainly due to the extra-dense Boeing 737.

Technical Outlook: USDJPY – Strong Signs Of Correction Stall

The pair holds in red in early Monday's trading and signaling increasing downside risk after last week's three-day recovery rally failed to clear key barriers at 109.26/32

Fibonacci resistances, 61.8% of 111.48/108.28 and 38.2% of 113.63/108.28) as the action was capped by falling 20SMA.

Daily RSI is moving lower after failing to regain 50 level and momentum turned south, holding in negative territory.

Overall picture is bearish and fresh negative signals are developing after recovery rally ran out of steam at key resistances, signaling that corrective phase might be over.

Key near-term points lay at 109.38 (falling 10SMA) and 109.21 (Friday's low) close below which is needed to confirm reversal and re-focus key support at 108.28 (26 Jan low).

Alternatively, fresh strength and close above 20SMA (110.26) will be bullish signal for extended correction.

Res: 110.26, 110.32, 110.72, 111.14

Sup: 109.75, 109.38, 109.21, 109.02

EUR/USD Ascending Trend Line Is Still Valid

The EUR/USD has recovered from the NFP lows it posted on Friday and at this point its trying to break W H1 that is an interim resistance. The EUR/USD is rejecting from the POC zone 1.1.2440-50 and if 1.2425 stays firm, we could see 1.2485, 1.2506 and eventually 1.2516. There are also multiple bullish patterns that suggest a possible upside continuation. ( Bullish SHS and W breakout) with an ascending trend line zig zag. However, if the price breaks below W L3 - 1.2400 we could see a drop to 1.2350.

W H1 -. Weekly Camarilla Pivot (Interim resistance - Weak)

W H2 - Weekly Camarilla Pivot (Weekly resistance)

W H3 - Weekly Camarilla Pivot (Weekly resistance - main)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

W L4 - Weekly Camarilla Pivot (Interim support - Strong)

W L3 – Weekly Camarilla Pivot (Interim support - Main)

W L2 – Weekly Camarilla Pivot (Interim support)

W L1 - Weekly Camarilla Pivot (Interim support - Weak)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

EURO Gains Still Expected Above 1.2432 Level

The euro has moved marginally higher against the U.S dollar during the Asian trading session, as the U.S dollar index slips back from monthly price highsRe. The EURUSD is currently trading around the 1.2460 level, as buyers start to recover upside momentum following the pairs brief decline towards the 1.2420 level on Friday. Traders will now look to high-impacting economic data from the eurozone, as we see the release of Retail Sales, Economic Confidence and PMI Services numbers for January.

The EURUSD pair remains bullish while trading above the 1.2432 level, further upside towards 1.2470 and 1.2491 still seems possible.

If sellers can push the EURUSD pair below the 1.2432 level for a sustained period, we may see a decline back toward the 1.2400 and 1.2385 level.

USDJPY Still Bullish Above 109.77 Level

The U.S dollar is retracing lower against the Japanese yen currency in early Monday trading, with price-action finding strong support around the 109.77 level. The USDJPY pair hit 110.48 on Friday, following a better than expected 200,000 Non-farm payrolls job number and a solid increase in U.S monthly wage earnings. The pair has come under slight selling pressure, as the Japanese Nikkei225 Index suffers triple-digit intraday losses and the U.S dollar index gives background from Friday.

The USDJPY pair still retains a bullish bias while price-action trades above the 109.77 level. Further upside towards 110.18 and 110.48 seems likely.

Should sellers manage to push the USDJPY pair below the 109.77 level, we may see a correction back towards the 109.44 and 108.98 levels.

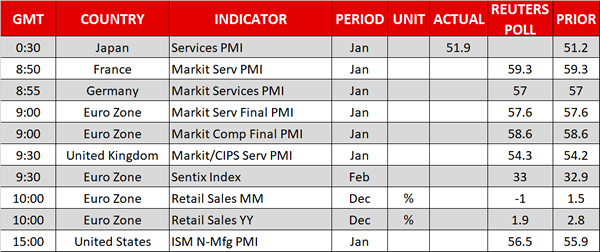

PMI Data Headlines Monday Session

The economic calendar will be flooded with PMI data on Monday, giving investors the latest glimpse into the Eurozone and US economies.

IHS Markit will release the final batch of Eurozone PMI figures beginning at 08:15 GMT with a report on Spain’s services industry. Later in the morning, Markit will release French, Germany and Eurozone Composite PMI. The Composite indicator tracks the performance of the manufacturing and services industries.

At 09:30 GMT, a report on the UK’s services industry will also make headlines.

Sentix is also scheduled to release its monthly investor confidence index for February. The comprehensive survey is based on consultations with 1,600 financial analysts and institutional investors.

The European Commission’s statistical agency will report on retail sales Monday. Receipts at retail stores are forecast to fall 1% in December following a 1.5% increase the month before. This translates into an annualized rate of 1.8%.

The US session will also feature headline PMI data, with Markit and the Institute for Supply Management reporting. The ISM’s report on US services activity is expected to show a PMI reading of 56.3, which is a slight uptick from the previous month.

Earlier in the session, Caixin China reported a stronger services PMI report for January that pointed to a strong uptrend in the world’s second largest economy. The Caixin services PMI strengthened to a reading of 54.7 from 43.9 in December on a scale of 1-100 where 20 represents the historic average.

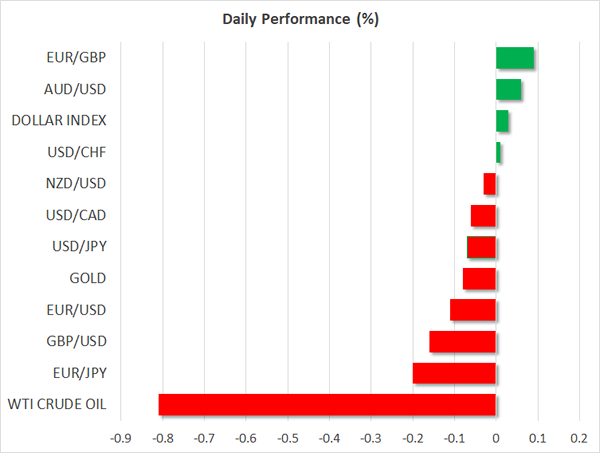

In the currency markets, the US dollar was off to a soft start Monday, as it fell slightly against a basket of world peers. The dollar index is down more than 3% since the start of 2018 and is currently trading near three-year lows.

EUR/USD

The euro was little changed at the start of Monday trading. The pair consolidated at the end of last week following the release of better than expected US jobs data. However, the report failed to generate a sustained rally for the greenback. As such, the EUR/USD continues to trade around 1.2460. The pair face immediate resistance at the psychological 1.2500 level. On the downside, support is located at 1.2435.

GBP/USD

Pound sterling has fallen sharply from Friday highs of 1.4265 US, where it was testing 20-month highs. Cable is now trading in the low 1.41 range. Despite the recent slide, the pair remains in a firm uptrend that could see prices barrel higher in the near term.

USD/CAD

The USD/CAD rallied on Friday to retake the 1.2400 handle. At the start of Monday’s Asian session, the pair had successfully maintained that level. However, the short term outlook continues to favour the Canadian dollar, which is benefiting from a stronger economy and rising interest rates.

Technical Outlook: GBPUSD – Risk Of Further Easing While 10SMA Caps, Friday’s Long Red Candle Weighs

Cable is consolidating on Monday after suffering heavy losses on Friday as the greenback rallied on upbeat US jobs data.

Friday's close in red and below 10SMA was a signal that the pair may extend lower after renewed upside attempts stalled at 1.4277 on Thu/Fri.

Broken 10SMA (1.4143) marks initial resistance and so far caps today's action, maintaining downside risk while the price remains below.

Extended bears would look for renewed attack at strong support at 1.40 zone (Fibo 38.2% of 1.3457/1.4344, 11/25 Jan upleg) and 30 Jan correction low at 1.3979.

The notion is supported by south-moving daily RSI / slow stochastic and Friday's long bearish candle weighing on near-term action.

Lift and close above 10SMA would sideline immediate downside risk and shift near-term focus higher.

Res: 1.4143, 1.4156, 1.4202, 1.4232

Sup: 1.4081, 1.4050, 1.4000, 1.3979

Technical Outlook: EURUSD – Bullish Bias While Above 10SMA, But Risk Of Deeper Pullback Exists

The Euro is trading within narrow range in early Monday, but still above rising 10SMA (currently at 1.2413) which tracks the ascend and marks initial support.

Friday's close in red after repeated rejection above 1.25 barrier and weekly close in long-legged Doji after six straight weeks of rally, could be seen as initial signs that bulls are running out of steam.

Overbought daily / weekly studies also warn of extended consolidation / deeper correction as dollar remains steady after receiving fresh boost from solid US jobs data which add on expectations of US rate hike in coming months.

Firm break below ascending 10SMA is needed to generate bearish signal and open way for further easing towards next pivotal support at 1.2300 (Fibo 38.2% of 1.1915/1.2537, 09/25 Jan upleg).

Extended consolidation with bullish bias remaining in play cold be expected while 10SMA holds.

Bullish scenario needs sustained break above 1.2537 (25 Jan peak) to signal bullish continuation and expose target at 1.2597 (Fibo 61.8% of 1.3992/1.0340 descend).

Res: 1.2466, 1.2490, 1.2522, 1.2537

Sup: 1.2424, 1.2413, 1.2334, 1.2300

Markets Adjusting To New Reality

When markets are priced for perfection, a slight shift in sentiment causes much damage. This is what we saw last week, after U.S. jobs report showed wage growth accelerated at its quickest pace since mid-2009. It seems the Fed will be faced with a new challenge after Janet Yellen’s departure, and investors are adjusting fast to the new reality.

Global above-trend synchronized growth, enthusiasm over the Trump administration’s fiscal policies, and strong earnings growth have been the key ingredients that fueled the equities rally throughout 2017. Moreover, while inflation remained absent, investors had more reasons to take risks given the low borrowing costs companies were enjoying. Now with inflation indicators heading north, the Federal Reserve is expected to move more aggressively than previously thought.

The era of cheap money is ending, and for markets who got addicted to it, it’s undoubtedly bad news. Today, 10-year U.S. Treasury yields are trading at a four-year high of 2.87%, an 18% increase from where they started the year. This suggests, Jay Powell, the new Fed Chair will be facing the opposite challenge of Ms. Yellen, during his tenure. If inflation runs faster than previously estimated, the Fed will need to speed up the pace of hiking rates from three to possibly four or five in 2018. The consequences might be severe on equity markets which enjoyed the second-longest bull run ever.

Equity bulls may argue that despite the spike in bond yields, they are still considered much lower than where they stood back in 2007 when 10-year treasury yields peaked at 5.33%. This is entirely true, but also in 2007, the S&P Cyclically Adjusted PE Ratio peaked at 27 compared to 33 currently. Although the earning season looks magnificent, forward PE ratio stands above 18 times, which is significantly higher than both the five and ten-year averages. The markets overstretched valuations may no longer be justified when interest rates surprise to the upside.

The only way to justify high valuations going forward, is to see economic and earnings growth resuming their uptrend, despite facing higher borrowing costs. Will President Trump’s fiscal policies make the magic? That is what should equity bulls bet on.

It’s important to see how investors react when Wall Street opens today, as it may determine whether the selloff will attract buyers, or it suggests a start of a more significant correction; however, future indices aren’t showing signs of optimism as of now.

The dollar is also likely to attract some attention after being dumped throughout 2017, particularly against emerging market currencies, if the selloff in equities resumes.

Equities Collapse, Dollar Recovers After Payrolls

Here are the latest developments in global markets:

FOREX: The dollar index traded virtually unchanged on Monday, after recovering somewhat on Friday on the back of robust US employment data.

STOCKS: US equity indices collapsed on Friday. The Dow Jones led the plunge, closing lower by 2.5%, while the S&P 500 fell 2.1%. The Nasdaq composite was down by 2%. These gigantic corrections came after the US jobs data for January showed wages accelerating notably, spurring speculation that US interest rates may rise faster than previously anticipated and triggering a surge in US bond yields. As yields rise, bonds begin to offer a better and “safer” return, thereby curbing demand for stocks. This negative sentiment rolled over into Asian trading on Monday, with Japan’s Nikkei 225 and Topix indices being down 2.5% and 2.2% respectively. In Europe, futures tracking the Euro STOXX 50 are currently in negative territory.

COMMODITIES: Oil prices dipped on Monday, with WTI and Brent crude both falling 0.8%, extending the losses they posted on Friday. A stronger US dollar and the broader risk-off market sentiment are being cited as the catalysts for the selloff. The increase in the US Baker Hughes oil rig count on Friday probably didn’t do oil prices any favors either, as it confirmed that US production continues to rise. In precious metals, gold is marginally lower. The dollar-denominated metal tumbled on Friday too, as the greenback recovered.

Major movers: Yields rise on inflation woes, dollar regains ground after jobs data

The dollar regained some lost ground on Friday, following the stronger-than-anticipated US employment report for January. Nonfarm payrolls came at 200k, beating the forecast of 180k, while last month’s print was also revised higher. The unemployment rate held steady as anticipated, though the surprise came from average hourly earnings, which accelerated by much more than expected to reach 2.9% in yearly terms.

The pick-up in wages is monumental for the Fed. Accelerating wages are broadly considered to be a precursor to an acceleration in inflation, as higher wages feed into more spending and therefore higher prices. Considering that inflation has long been the missing piece of the puzzle in an otherwise robust US economy, this development increases the likelihood that the FOMC may deliver three 25bps rate hikes this year, and even opens up the possibility for a fourth. Indeed, markets have now almost fully priced in three hikes in 2018, according to the Fed fund futures.

Now as for the dollar, although it did regain some poise after the US data, it did not advance as much as one would have expected given the strength of the prints. The currency once again seemed unable to draw support from the bond market, where the yields on 10-year US Treasuries surged by 7bps on the day, last trading near 2.86%. The relatively subdued recovery in the greenback is yet another confirmation of just how negative the sentiment surrounding the currency is right now.

Elsewhere, dollar/loonie skyrocketed on Friday. Besides the strong US jobs figures, the surge was fueled by some comments from Canadian Prime Minister Justin Trudeau, who said that his country is willing to walk away from NAFTA. His remarks follow media reports in recent weeks that Canadian officials anticipate the US to pull out of NAFTA soon, and underscore that these negotiations have yet to bear fruit. A potential breakdown in these talks would probably weigh notably on the loonie, as well as the Mexican peso.

Day ahead: US, UK & Eurozone PMIs in focus; Powell takes over as new Fed chair

Out of the Eurozone, final PMI readings for the month of January will be released at 0900 GMT, while figures on the Sentix index and retail sales will follow at 0930 GMT and 1000 GMT respectively.

According to forecasts, the Eurozone composite Markit PMI is expected to stand at record highs in January as was initially estimated, rising by 0.5 points to 58.6. However, the euro might show little reaction to these data – unless the index surprises to the upside or downside – as flash estimates tend to be more important for the currency.

On the other hand, the block’s retail sales are said to slow down in December, with analysts anticipating the measure to decline by 1.0% on a monthly basis, driving the yearly gauge lower to 1.9% growth from 2.8% seen in November.

The Sentix index which tracks the six-month economic outlook is projected to inch up by 0.1 points to +33 in February, underlying investor’s strong confidence in the region. The index is fluctuating among the highest scores seen since August 2007.

In the UK, January’s CIPS/Markit PMI for the service industry is expected to come at 54.3 in January, slightly above the previous mark of 54.2. Considering that the services sector accounts for the vast majority of UK GDP, market participants will likely keep a close eye on this print as they try to gauge the economy’s momentum ahead of the Bank of England meeting on Thursday.

Meanwhile in the US, market watchers will be waiting for the ISM non-manufacturing PMI due at 1500 GMT. Following encouraging manufacturing PMI records last week which remained close to the strongest prints seen since 2004 despite a pullback in January, the non-manufacturing PMI is projected to improve to 56.5 in the aforementioned month, compared to 56.0 in December.

Regarding today’s public appearances, Jerome Powell, Janet Yellen’s successor, will be sworn into the position of the next Fed chair at 1400 GMT. Projections are for Powel to follow Yellen’s footsteps by tightening monetary policy even further this year. Later on, the ECB chief, Mario Draghi, will comment on the draft resolution of the European Parliament concerning the 2016 annual ECB report in the European Parliament Plenary in Strasbourg, France at 1600 GMT.

In stock markets, earnings releases will remain in the spotlight.

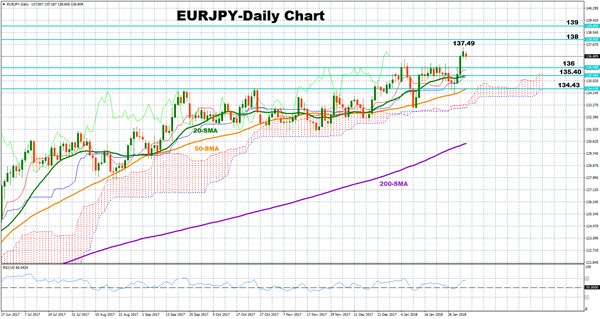

Technical analysis – EURJPY holds at 2 ½ -year highs; maintains bullish bias

EURJPY managed to break above the 137 key-level on Friday, stretching towards a fresh 2 ½ -year high of 137.49. Today, the pair returned to the 136 area but it continues to hold a bullish bias.

Prices remain above the Ichimoku cloud and the moving average lines, which are positively sloped, supporting that the market might maintain its positive trend both in the short and the medium-term. The RSI is also in bullish territory above 50 but has no specific direction, signaling that the pair might consolidate for a while before it resumes its uptrend. The Ichimoku indicators also support this view, with the Tenkan-sen and the Kijun sen being flat.

If the market extends to the downside, immediate support could come from the 136 psychological level, which was a frequently congested area since the beginning of the year. Then the 20-day simple moving average line (SMA) at 135.40 could come into view, while a substantial close below this level could increase bearish actions towards the 50-day SMA at 134.43.

To the upside, the previous top at 137.49 is expected to provide resistance, opening the way towards the 138 and 139 handles.