Sample Category Title

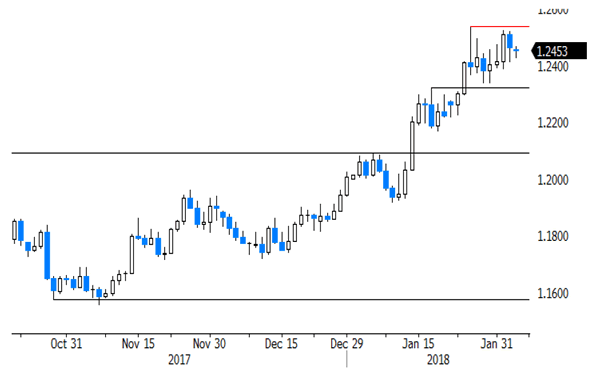

EUR/USD Analysis: Likely To Re-Test 1.25

EUR/USD lacked volatility on Friday morning, as it remained located relatively close to the 1.25 mark. This situation changed mid-session when solid US employment data strengthened the Greenback against major currencies, including the Euro. The pair was subsequently trading sideways, as the 55– and 100-hour SMAs bounded the Euro from both sides.

In terms of patterns, the rate breached a short-term trend-line mid-Friday and continued to trade in a new junior channel. This steep formation, however, should not hold any longer, as strong upside momentum is unlikely today.

The Euro is expected to find support near the 100– and 200-hour SMAs and the weekly PP circa 1.2435 and cap its gains around the 2015/17 high of 1.2540.

GBP/USD Analysis: Points To Limited Gains

Similarly to other major currencies which are trading against the US Dollar, downside risks were driving the Pound during the previous session. Thus, it was unable to re-test its 1,5-year high of 1.43.

The pair found support for at the 55-hour SMA for a brief period of time; however solid US fundamentals at 1330GMT resulted in a southern breakout of this moving average and eventually the longer-term SMAs, as well. In addition, the bottom boundary of the prevailing seven-week ascending channel also surrendered.

Technical indicators flash bullish signals. However, the expected appreciation is likely to be delayed or even stopped by the aforementioned SMAs in the 1.4170/1.4200 area.

In terms of support, the Pound is restricted by the monthly PP at 1.40.

USD/JPY Analysis: Flashes Mixed Signals

The US Dollar managed to continue its strong upside movement during the first part of Friday's trading session. Better-than-expected US employment data released at 1330GMT strengthened the Greenback by 40 pips within the first five minutes after the release, thus allowing it to test the 110.50 mark.

The pair's subsequent movement was a decline from this eight-day high towards the 55-hour SMA and the weekly PP at 109.70.

Technical indicators show mixed signals, thus the US Dollar is likely to remain stable in this session. In case the monthly PP does not hold, the upside target should be the weekly R1 at 111.00.

On the other hand, the daily low is expected to be the combined support of the 100– and 200-hour SMAs circa 109.30.

XAU/USD Analysis: Consolidates on Monday morning

Contrary to expectations, the yellow metal was driven by bearish momentum on Friday. Traders were still indecisive during the morning session; however, better-than-expected US employment data added some strength to the overall bearish sentiment thus pushing Gold down to the 1,330.00 mark where it had already found support by Monday morning.

This trading session marks a significant northern resistance which comes from the weekly and monthly PPs and the nearby-located 55-, 100– and 200-hour SMAs near 1,337.00 and 1,345.00, respectively.

Thus, the upside potential for this session could be 1,340.00, while the southern side is guarded by the weekly S1 at 1,323.60. Technical indicators suggest that Gold could spend the day closer to its resistance area.

GBP/USD: UK Construction PMI

The British Pound weakened against the Greenback 12 base points or 0.09% on the construction PMI report, though the pair was affected more from the US side after the country's job market data was released.

The UK construction sector almost began the contraction for the first time in five months in January, as Brexit uncertainties cased some dry up in new orders. The Markit/CIPS reported that Britain's construction PMI declined to 50.2 in January, following a 52.2 gain in the prior month. Firms anticipated business to enhance later this year, though the outlook is likely to depend on how the Brexit negotiations go, with the UK PM Theresa May aiming to reach the deal with the European Union that would exclude new barriers to investment and trade.

EUR/USD: US Non-Farm Employment Change

The Greenback strengthened against the European single currency, as Friday's report revealed that hiring in the US accelerated. The EUR/USD exchange rate lost 31 base points or 0.25% to the 1.2460 mark.

The job growth in the US increased in January, while wages surged further, recording the strongest annual growth in more than eight years, fuelling expectations that consumer inflation would push higher in 2018, as the job market reaches full employment. The Labour Department stated that non-farm payrolls rose 200K positions last month. Meanwhile, the jobless rate rmained at the lowest level in 17 years of 4.1%. Strong data underscored robust growth momentum, encouraging the Fed to be more agressive in hiking interest rates in 2018.

EURUSD Fails To Extend Strong Gains, Indicators Signal For Retracement

EURUSD posted a strong positive January while this month started with downside pressure. The US dollar strength drove the pair lower on Friday and failed to hit again the three-year high of 1.2540. The short-term technical indicators are flat and point to more weakness in the market.

Having a look on the daily timeframe, the Relative Strength Index (RSI) dropped slightly lower of the 70-overbought level at 68, suggesting that the latest upswing may be running out of steam and that the risk of a near-term correction is high. Additionally, the MACD oscillator is holding near its trigger line and is ready to create a bearish crossover in the positive territory, indicating further losses.

Should prices reverse lower, immediate support could come near the 1.2280 price level, which is the 20-day simple moving average at the time of writing. Below that, the 1.2160 barrier is another major support, while a drop below this area could take the price closer to 1.2080, which overlaps with the 23.6% Fibonacci retracement level of the up-leg from 1.0560 to 1.2540. Moreover, near 1.2080 the 50-day SMA is holding and is pointing to the upside. So, the aforementioned barrier is acting as a strong obstacle for the bears.

On the flip side, there is immediate resistance at 1.2540, while above it, the next major resistance to watch is 1.2570 taken from the high of December 2014.

Currencies: Dollar Holds Indecisive Pattern Despite Higher Yields And Rising Volatility

Sunrise Market Commentary

- Rates: Higher yields contaminate other markets

The global core bond sell-off continued last Friday following strong US payrolls and average hourly earnings. Higher rates contaminated stock markets with a huge correction in main US indices (-2%/-2.5%). Sentiment remains bearish in both bonds and stocks this morning. The US- and German 10-yr yields are heading at high-speed towards the psychological levels of 3% and 1%. - Currencies: Dollar holds indecisive pattern despite higher yields and rising volatility

On Friday, the dollar gained only modest ground after a strong US payrolls report. The sharp rise in US yields and the spike in global volatility provides no clear guidance for the dollar. The services PMI's/ISM are probably only of second tier importance today. Will the euro stay strong if the risk-off correction continues?

The Sunrise Headlines

- US stock markets suffered a huge correction last Friday as the surge in yields starts to bite. Main indices lost around 2% to 2.5%. Asian bourses lose more than 1% this morning with Japan underperforming (-2%).

- Democrats have sounded the alarm of a potential constitutional crisis in Washington, warning that President Trump may use the release of a top-secret memo as grounds to fire his deputy attorney-general.

- China's services sector got off to a flying start in 2018, expanding at its fastest pace in almost six years as new orders surged and companies rushed to hire more staff. The Caixin Services PMI rose from 53.9 to 54.7.

- Outgoing Fed chair Yellen said US stocks and commercial real estate prices are elevated but stopped short of saying those markets are in a bubble.

- SF Fed Williams said US central bank's decision on whether to hike by three times or four in 2018 will be driven by the data, and that both possibilities are “still reasonable at this point to think about as options.”

- UK PM May has ruled out staying in the EU's customs union after Brexit, a government official said, adding it isn't government policy to stay in "a" customs union either.

- Today's eco calendar contains the EMU and UK services PMI's and US (ISM). EMU retail sales will also be released. ECB President Draghi speaks in European Parliament.

Currencies: Dollar Holds Indecisive Pattern Despite Higher Yields And Rising Volatility

Dollar shows no clear trend despite global risk-off

Friday's US payrolls were strong, including good wage growth. The report caused a further rise in US yields. USD/JPY spiked north of 110 and stayed there even as US equities sold off sharply. The BOJ's commitment to keep an easy policy and the rise in core (US and EMU) yields prevented a yen rebound. The pair closed the session at 110.17. The dollar gained modest ground against the euro. EUR/USD finished the day at 1.2463.

Asian equities are under pressure overnight after Friday's sell-off in the US. Japan underperforms. The losses on Chinese equity markets remain modest. Even so, the US 10-y yield is setting a new cycle high north of 2.85%. The dollar is a place of relative calm give the global volatility. EUR/USD hovers in the mid 1.24 area. The yen gains a few ticks. USD/JPY is drifting back below 110. Before Parliament, BOJ's Kuroda said that quantitative easing is highly needed to reach 2% inflation. The rise of core bond yields and the verbal offensive of the BOJ currently prevent the yen from taking up its safe haven role.

Today, EMU January services PMI, EMU retail sales and the US nonmanufacturing ISM are interesting. The US ISM is expected to improve from 55.9 to 56.5. Markets will especially look for clues on inflation. In this respect, (too much) good news might be bad for bonds and for risky assets. For now, the sharp rise in core yields and the up-tick in volatility provided no clear guidance for the dollar. We tend to believe that a protracted period of risk aversion should be modestly negative for the euro, or at least prevent a further rise. Admittedly, the jury is still out on this issue. We still look out for a technical sign. Technical picture: the dollar decline slowed of late, but no meaningful rebound occurred, especially not against the euro. EUR/USD 1.2537/98 remains the first topside resistance. A break would signal more trouble for USD short term. EUR/USD 1.2323/35 is a minor support A break below 1.2165 would call off the ST downside alert (for the dollar).

Sterling declined further on Friday. Ongoing Brexit noise and a global risk-off context weighed on the UK currency. EUR/GBP rebounded above 0.88. Today's UK services PMI is expected little changed at 54.1. The Brexit debate in the conservative Party suggests that Brexit hardliners are gaining momentum. This might weigh on sterling even as investors look out for this week's BoE meeting.

EUR/USD: USD going nowhere despite strong payrolls

Market Update – Asian Session: Equities Across The Region Lower Tracking US Friday Session

Headlines/Economic Data

General Trend: Energy, Real Estate and Materials companies underperform

(US) US 10-year Treasury yield higher by 2bps, after rising over 5bps on Friday’s session; yield at 2.86% vs 2.88% for Australia 10-year yield

Australia 10 year yield rises over 9bps amid gain in Treasury yields and weaker bid to cover at bond auction

Taiwan sells 10-year bonds at lower bid to cover, despite rise in yield

Broad dollar strength, rising 1% against the KRW

Japan

Nikkei 225 opened -1.5%; closed -2.6%

TOPIX Real Estate Index -3%, Electric Appliances -2.2%, Iron & Steel -2%, Securities -2%

Mitsubishi UFJ [8306.JP] Declines over 3%: Reported flat 9-month pretax profits

Softbank [9984.JP]: -2%: Expected to report earnings on Wed, Feb 7th

Toyota [7203.JP] -1.5%: Expected to report earnings on Tuesday Feb 6th

Fast Retailing [9983]: Declines over 3%: Jan domestic SSS -2.4% y/y

Honda [7267.JP] Gains over 1.5% after raising FY outlook

(JP) PM Abe backed candidate Taketoyo Toguchi said to defeat incumbent Susumi Inamine in the Nago mayoral elections – Japanese Press

(JP) Japan PM Abe expected to ask the US and South Korea o conduct a planned joint military drill after the Pyeongchang Winter Olympics without scaling it down so as to keep pressuring North Korea to give up its nuclear and missile development – Nikkei

(JP) Japan cryptocurrency exchange Coincheck, has not been successful tracking stolen funds, were transferred to anonymous e-wallets; not sure when they will resume withdrawals – Nikkei

(JP) Japan Jan PMI Composite: 52.8 v 52.2 prior; PMI Services: 51.9 v 51.1 prior

(JP) Japan PM Abe: 2% inflation is a global standard, market environment has greatly changed due to 2% target - Parliament

(JP) BoJ Iwata: Companies raising prices has not progressed 'far'

(JP) Bank of Japan (BOJ) Gov Kuroda: No change in approach to QE; maintaining 2% inflation target is very important - Parliament

Korea

Kospi opened -1.5%

Continued weakness in chip sector: Samsung Electronics and Hynix drop further after Friday’s over 2% declines

Samsung: 005930.KR South Korea Appeals Court: Samsung's support of equestrian sport constitutes bribery in the Jay Lee case

(KR) South Korea Dec Current Account Balance: $4.1B v $7.4B prior; Balance of Goods (BOP): $8.2B v $11.5B prior

(KR) North Korea military parade on Thursday is not targeted at the Olympics

(KR) Bank of Korea (BOK) sells KRW720B in 6-month bonds at 1.62%

(KR) According to Statistics Korea, 2017 online shopping in South Korea reached KRW78T, +19.2% y/y - Korean press

(KR) North Korea official: North Korea's nuclear capabilities will deter Trump from 'showing off on the Korean peninsula' - UK press

(KR) South Korea sells KRW1.65T in 3-yr Govt bonds: avg yield 2.275%

China/Hong Kong

Hang Seng opened -2.7%, Shanghai Composite -1.5%

Hang Seng Energy Index -3%, Information Tech -2.7%, Materials -2.1%, Consumer Goods -2%, Financials -2%

(CN) Yuan (CNY) ‘internationalization’ may accelerate in 2018 – China Economic Info Daily

(CN) Chinese Academy of Social Sciences (CASS): China is likely to leave its benchmark interest rate unchanged in the near future amid reasonable inflation rises and a stable yuan, even with the higher likelihood of US Fed interest rate rise next month - China Daily

(CN) China Ministry of Commerce (MOFCOM): to launch anti-dumping investigation into US sorghum imports

(CN) China urges the US to drop its "Cold War mentality" earnestly assume its special disarmament responsibilities, correctly understand China's strategic intentions and objectively view China's national defense and military build-up

(CN) China PBoC: Skips OMO (8th straight session) v skipped prior; Net drain CNY40B v CNY90B prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3019 v 6.2885 PRIOR

(CN) CHINA JAN PMI SERVICES: 54.7 V 53.5E (highest since May 2012); PMI COMPOSITE: 53.7 V 53.0 PRIOR

(CN) China securities regulator CSRC said to ask brokerage firms to help 'avert sharp stock crashes' - US financial press

Australia/New Zealand

ASX 200 opened -1.4%; closed -1.6%

ASX 200 Resources Index -2.5%, Energy -2.2%, Telecom -1.6%, Financials -1.4%, REIT -1.3%

(AU) Australia Jan CBA PMI Composite: 54.2 v 55.5 prior; PMI Services: 53.8 v 55.1 prior

AWE.AU Board recommends bid from Mitsui at A$0.95/share

WES.AU Guides H1 non-cash impairment for UK and Ireland Bunnings unit of A$795M resulting in underlying pretax loss A$165M; targeting H1 EBITDA of A$33M

(AU) Australia AOFM buy backs A$400M in bonds due March and Oct 2019; combined bid to cover 2.95x

(AU) Australia Jan Melbourne Institute Inflation M/M: 0.3% v 0.1% prior; Y/Y: 2.0% v 2.3% prior

(AU) Australia sells A$400M v A$400M indicated in April 2033 bonds, avg yield 3.0717%, bid to cover 1.87x

(AU) Australia Jan ANZ Job Advertisements M/M: +6.2% v -2.3% prior

(NZ) New Zealand Treasury: Sees annual inflation at ~1.0% in Q1; inflation to gradually pick up in 2018 and 2019

Other Asia

(ID) Indonesia Q4 GDP Q/Q: -1.7% v -1.7%e; Y/Y: 5.2% v 5.1%e; 2017 GDP Y/Y: 5.1% v 5.1%e

(MY) Malaysia Central Bank (BNM) Gov: Not on a tightening trend, monetary policy is still accommodative

(TW) Taiwan Central Bank sells NT$25B in 10-yr bonds at 1.069% v 0.981% prior (1.02-1.05%e); bid to cover 1.73x v 2.20x prior

North America

On Monday’s session, S&P500 Futures trade lower by more than 0.7% in Asia

(US) Outgoing Fed Chair Yellen: Asset valuations are generally elevated, but don't want to call what we are seeing a bubble - PBS interview (from Feb 3rd)

(US) Fed's Williams (moderate, voter): need to continue raising interest rates; hikes will keep the economy on track and avoid overheating (from Feb 2nd)

(US) Fed's Kaplan (moderate, non-voter): Has more conviction in three rate hikes than six months ago; - There's a chance I'm wrong and we may consider more than three hikes; Jobs report today [Friday] was consistent with his thinking (from Feb 2nd)

(US) Larry Lindsey said to withdraw from being considered for the Fed Vice Chairman position – US financial media

(US) White House econ adviser Cohn: White House would like to make individual side of tax reform permanent; We have had a mild backup in Treasury yields ; Stocks are seeing a few days of consolidation after a long rally; Expects strong Q1 GDP in the US; Strong dollar is always in the best interest of the US - Fox Business interview (From Feb 2nd)

QCOM Broadcom said to raise bid for Qualcomm to $80-82/shr (vs $70/share currently), ~$120B; will also include higher breakup fees - financial press

Looking Ahead: US Jan ISM Non-Manufacturing PMI due for release on Monday

Europe

(DE) Germany suspends coalition talks, will resume Monday 09:00GMT, failing to meet self imposed Sunday deadline; disputes over healthcare and labor policy remain

(FR) ECB's Villeroy (France): whether we end QE program in Sept or taper somewhat more gradually is not a deep existential question; We will keep an eye on impact of exchange rate evolution and be prepared to reassess if necessary (from Feb 2nd)

(UK) UK Official: PM May has ruled out staying in customs union - press [Note: PM May advisers were said to consider a customs union deal covering trade in goods with the EU after Brexit, said a press report from Feb 1st. The possible plan would take effect after the 2-year Brexit transition period.]

Fiat Chrysler: US regulators reportedly to seek major fines and recall as part of Fiat diesel motor settlement - press

GKN [GKN.UK]: Onex in talks with GKN on aerospace unit - Uk press

Carillion [CLLN.UK]: Greybull Capital will be among bidders interested in acquiring parts of Carillion that might be ringfenced following its liquidation - FT

Looking Ahead: UK Jan Services PMI due for release

Levels as of 01:00ET

Nikkei225 -2.6%, Hang Seng -1.3%; Shanghai Composite +0.5%; ASX200 -1.6%, Kospi -1.1%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.1%, Dax -0.4%; FTSE100 -0.4%

EUR 1.2466-1.2424; JPY 110.29-109.79; AUD 0.7939-0.7890;NZD 0.7309-0.7278

Apr Gold -0.2% at $1,334/oz; Mar Crude Oil -0.8% at $64.91/brl; Mar Copper +0.4% at $3.19/lb

The Rout In Equities Continues

Equities are once again down this morning after a hard sell-off last week, in stark contrast to the recent run higher. The NFP report had little impact on stocks but affected the USD, sending GBPUSD lower from 1.42157 to test the 1.41000 support area.

Fed Chair Janet Yellen was out with comments over the weekend as she departs her role on the FOMC. She said that US stocks and commercial real estate prices were high. Price-earnings ratios are near the high end of their historical ranges. Commercial real estate prices are now quite high relative to rents. It is a source of some concern that asset valuations are so high.

In other news, Major Credit Card Lenders are prohibiting the use of Credit Cards for use in funding Cryptocurrency transactions.

UK PMI Construction (Jan) was 50.2 v an expected 52.0, from 52.2 previously. GBPUSD gapped down from 1.42257 to 1.42194 at the time of this release and then sold off to 1.42018.

Eurozone Producer Price Index (YoY) (Dec) was 2.2% v an expected 2.3%, from a previous reading of 2.8%. EURUSD sold off from 1.24863 to 1.24752 by this data point.

US Non-Farm Payrolls (Jan) was 200K, higher than the expected 180K, from a prior 148K, which was revised up to 160K. This measures the change in the number of employed people in January. The Unemployment Rate (Jan) was as expected, unchanged at 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during January. Average Hourly Earnings (YoY) (Jan) was 2.9% v an expected 2.6%, from 2.5% previously. Average Weekly Hours (Jan) was 34.3 v an expected 34.5, from a previous 34.5. Labor Force Participation Rate (Jan) was 62.7% v an expected 62.8%, from a prior reading of 62.7%. EURUSD sold off from 1.24921 to 1.24090 following these data releases. Gold moved lower from 1345.70 to 1327.00.

US Factory Orders (MoM) (Dec) was 1.7% v an expected 1.5%, from 1.3% previously, which was revised up to 1.7%. USDJPY sold from 110.418 to 110.315 before recovering to 110.476.

Baker Hughes US Oil Rig Counts was released, with a headline number coming in at 765 against last week’s number of 759. The expected number this week was 758. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

FOMC Member Williams spoke about the US economic outlook at the Financial Women of San Francisco luncheon. His main remark was that the Fed needed to continue on its path of raising rates. He said in his comments that he is optimistic about the economy, which is performing better than expected but is not shifting gears. He still believes the Phillips curve holds true. He said he expects growth this year to pick up by 2% and for inflation to pick up this year and next.

EURUSD is unchanged overnight, trading around 1.24530.

USDJPY is down -0.12% in early session trading at around 110.019.

GBPUSD is down -0.09% to trade around 1.41063.

USDCAD is unchanged overnight, trading around 1.24184.

Gold is down -0.10% in early morning trading at around $1,331.09.

WTI is down -0.32% this morning, trading around $64.63.

Major data releases for today:

At 08.15 GMT, Spanish Markit Services PMI (Jan) is expected to be 55.4 from a prior reading of 54.6.

At 08:55 GMT, German Markit PMI Composite (Jan) is expected to be unchanged at 58.8. Markit Services PMI (Jan) is also expected unchanged at 57. EUR currency pairs and the German 30 Index may see a sudden change in price due to this data release.

At 09:00 GMT, Eurozone Markit PMI Composite (Jan) is expected unchanged at 58.6. Markit Services PMI (Jan) is also expected unchanged at 57.6. EUR currency pairs may be moved by this data point.

At 09.30 GMT, UK Markit Services PMI (Jan) is expected to be 54.3 from a prior reading of 54.2.

At 14:45 GMT, US Markit Services PMI (Jan) is expected unchanged at 53.3. Markit PMI Composite (Jan) is expected to be 53.9 from a previous reading of 53.8. USD crosses could experience volatility around these data releases.

At 15:00 GMT, US ISM Non-Manufacturing PMI (Jan) is expected to be 56.3 from 56.0, which was revised up from 55.9 previously. USD pairs may be moved by this release.

At 16:00 GMT, ECB President Draghi will testify on the ECB’s Annual Report for 2016 before the European Parliament in Strasbourg.

Major releases for this week:

On Tuesday at 00:30 GMT, The Royal Bank of Australia will release its Interest Rate Decision and Rate Statement.

On Wednesday at 08:00 GMT, the ECB will release its Non-monetary policy’s meeting minutes.

On Wednesday at 20:00 GMT, the Royal Bank of New Zealand will release its Monetary Policy Statement, Rate Statement and the Interest Rate Decision. At 21:00, a speech by Deputy Governor Grant Spencer will be followed by a press conference.

On Thursday at 12:00 GMT, the Bank of England will release its Interest Rate Decision and Monetary Policy Statement, MPC Official Bank Rate Vote results and its Inflation Report