Sample Category Title

Daily Wave Analysis: EUR/USD Builds Triangle Pattern In Wave 4 Correction

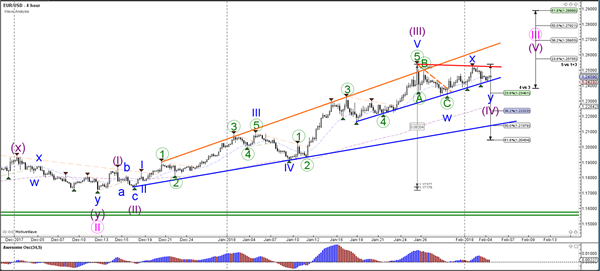

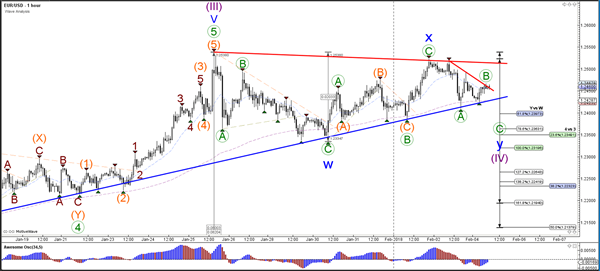

Currency pair EUR/USD

The EUR/USD failed to break above the previous top (red), which means that price could now be building a larger WXY (blue) correction. A break below the support trend line (blue) could indicate a deeper correction at the Fibonacci levels of wave 4 (purple), unless price breaks below the 50%. A break above the resistance (red) could indicate an uptrend continuation within wave 5 (purple).

The EUR/USD is probably building a bearish ABC (green) correction within wave 4 (purple) unless price manages to break above the resistance (red) trend lines. A bullish break could start a continuation of the uptrend.

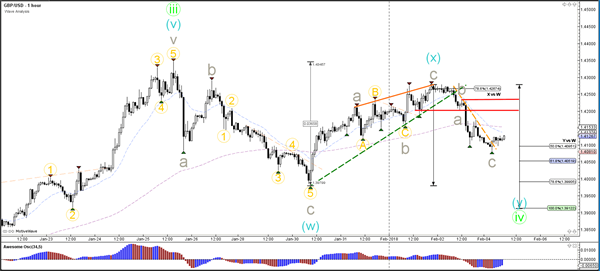

Currency pair GBP/USD

The GBP/USD is building a triangle pattern which is marked by support (green) and resistance (red). A bullish breakout could indicate an uptrend continuation.

The GBP/USD completed a bullish ABC (grey) rather than a 123 when price broke below the support trend line (dotted green). Whether the bearish ABC (grey) has been completed remains to be seen and depends if price is able to break above resistance (red).

Currency pair USD/JPY

The USD/JPY broke above thelarger resistance trend line (red) and is most likely building a bullish wave 3 (purple).

The USD/JPYis in a bullish channel. The current bearish retracement is testing the Fibonacci support levels of wave 4 (blue) which could be bouncing spots for a continuation higher towards the Fib targets.

Asian Stock Indices Down 1-2%

Market movers today

The main focus starting this week is whether the sharp sell-off in both bond markets and equity markets continues on the back of the 'inflation scare' flaring up in markets.

On the global agenda today, ECB's Weidman speaks in Fran kfurt at 10.00CET. The final Euro PMI service indices with more country details are released at 10.00CET followed by Euro area retail sales at 11.00CET.

US ISM non-manufacturing at 16.00CET will give more insights into the strength of the US service sector.

Rest of the week Fed speeches and Bank of England meeting are the key things to watch. The Fed speeches will be particularly interesting following the job report Friday showing higher wage growth.

In Scandi , attention today turns to Norwegian housing prices at 11.00CET. Rest of the week Norwegian inflation and GDP numbers and Swedish industrial orders/ production and household consumption are the main economic figures in focus.

Selected market news

Service PMIs released for China and Japan overnight both came out stronger than expected showing healthy expansion in service sector activity in both economies. Despite these news and the overall strong global economic backdrop equity markets continued to sell off overnight with major Asian stock indices down 1-2% and futures in Europe and US down as well.

Overnight , Japan's prime minister Abe supported continuation of easing by Bank of Japan by saying that he st ill expects dynamic quantitative easing and that the economy has not completely escaped deflation yet . Bank of Japan governor Kuroda was out saying that there is no change to approach in quantitative easing.

Following the US jobs report on Friday a number of Federal Reserve officials made comments about monetary policy. Kashkari stood out the most as he hinted that the high wage growth number if a sign that wage pressures were building could warrant more hikes this year and thus struck a more hawkish tone on monetary policy than usual. Kaplan and Williams made hawkish and dovish comments respectively.

The Iranian oil minister Zanganeh said this weekend that Iran can increase oil product ion swiftly if OPEC decides to end production cuts following the planned June review of the production cut deal. On Friday, the US oilrig count rose further to 765 indicating future rise in US production. The price on Brent crude has dropped below USD68/bbl level overnight partly owing to the posit ive supply fundamentals and partly to the above mentioned weak sen iment in equity markets.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 155.07; (P) 155.83; (R1) 156.27; More...

Intraday bias in GBP/JPY is neutral for the moment. But after all, the cross is supported well by the rising 55 day EMA. And there is no sign of reversal yet. Near term outlook will remain bullish as long as 151.95 support holds. Break of 156.59 will extend recent rally to 100% projection of 139.29 to 152.82 from 146.96 at 160.49.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

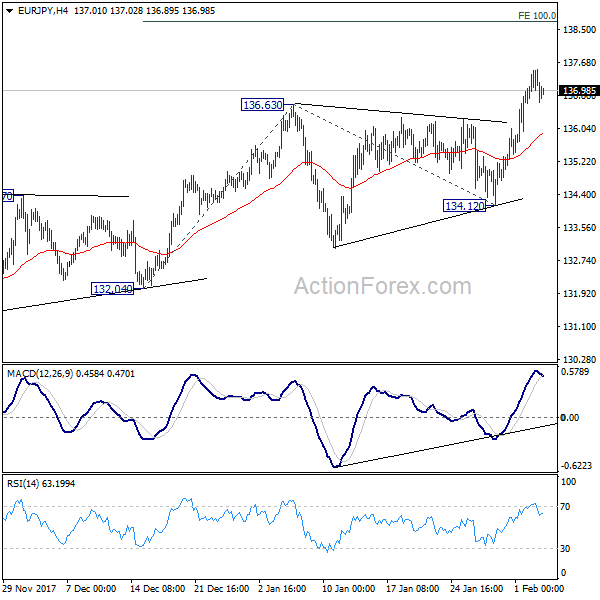

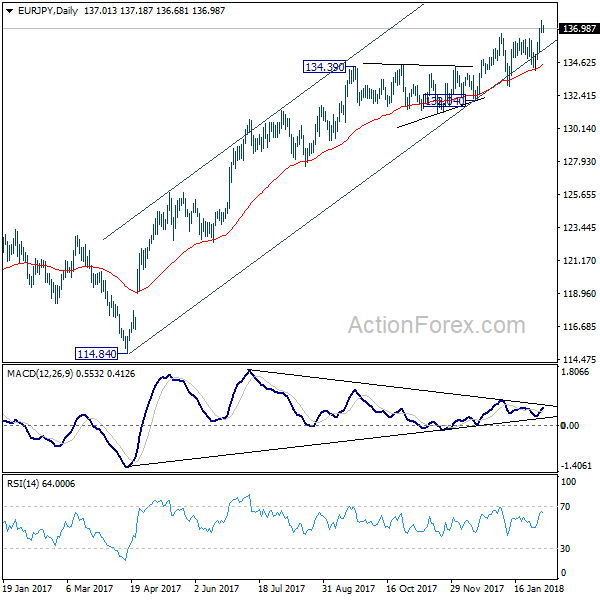

EUR/JPY Daily Outlook

Daily Pivots: (S1) 136.73; (P) 137.11; (R1) 137.57; More....

Intraday bias in EUR/JPY remains mildly on the upside for 100% projection of 132.04 to 136.63 from 134.12 at 138.71 first. On the downside, break of 134.12 support is needed to indicate near term reversal. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

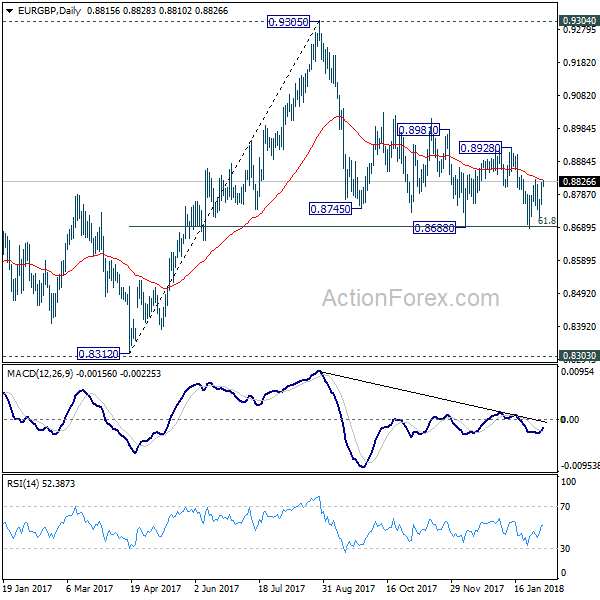

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8775; (P) 0.8799; (R1) 0.8843; More...

Intraday bias in EUR/GBP remains neutral as range trading continues inside 0.8686/8928 . And, near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

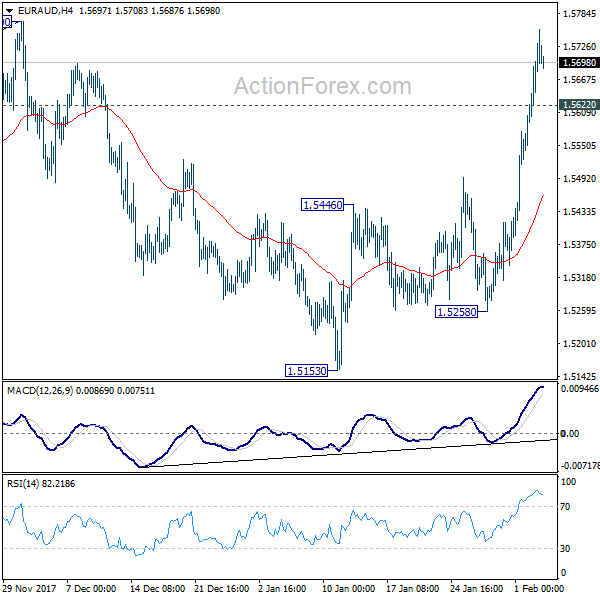

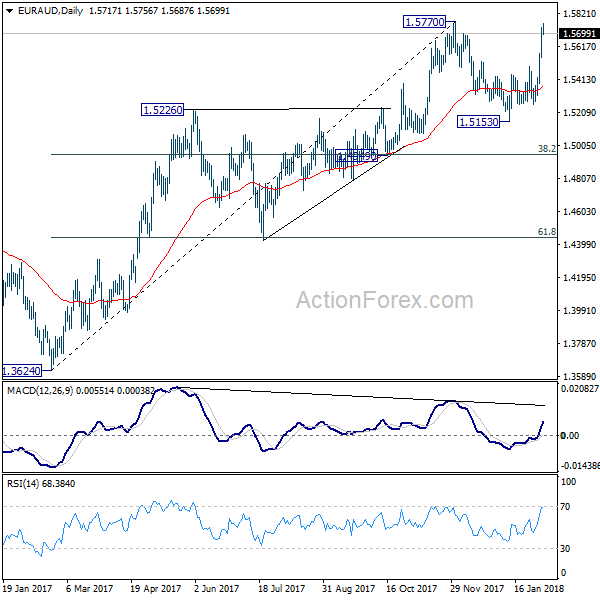

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5600; (P) 1.5665; (R1) 1.5778; More....

Intraday bias in EUR/AUD remains on the upside for 1.5770 resistance. Based on current strong upside momentum, the cross might be resuming medium term rise from 1.3264. Decisive break there will confirm this bullish case and target 1.6587 key long term resistance. On the downside, below 1.5622 minor support will dampen this bullish case and turn intraday bias neutral first.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1570; (P) 1.1596; (R1) 1.1621; More...

Intraday bias in EUR/CHR remains neutral for consolidation above 1.1540. Upside of recovery should be limited by 1.1684 minor resistance to bring fall resumption. As noted before, the decline from 1.1832 is correcting medium term rise from 1.0629. Below 1.1540 will target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.)

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Australia’s Services Sector Activity Quickened In January

For the 24 hours to 23:00 GMT, the AUD declined 0.92% against the USD and closed at 0.7930 on Friday.

LME Copper prices rose 0.6% or $39.0/MT to $7066.0/MT. Aluminium prices rose 0.5% or $10.0/MT to $2228.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7926, with the AUD trading a tad lower against the USD from Friday's close.

Overnight data indicated that Australia's AiG performance of services index climbed to a level of 54.9 in January, compared to a level of 52.0 in the previous month, thus adding further evidence of a strengthening economy.

Elsewhere in China, Australia's largest trading partner, the Caixin/Markit services PMI unexpectedly advanced to a level of 54.7 in January, confounding market expectations for a drop to a level of 53.5 and marking the sharpest increase since May 2012. In the prior month, the PMI had registered a reading of 53.9.

The pair is expected to find support at 0.7873, and a fall through could take it to the next support level of 0.782. The pair is expected to find its first resistance at 0.7997, and a rise through could take it to the next resistance level of 0.8068.

Going forward, Australia's trade balance and retail sales data, both for December, slated to release overnight, would be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Producer Prices Rose At Its Weakest Pace Since July 2017 In December

For the 24 hours to 23:00 GMT, the EUR declined 0.33% against the USD and closed at 1.2494 on Friday.

On the economic front, the Euro-zone's producer price index (PPI) climbed 2.2% on an annual basis in December, rising at its slowest pace in 5 months. The PPI had advanced 2.8% in the previous month, while markets were expecting for a gain of 2.3%.

The US Dollar gained ground against a basket of major currencies on Friday, propelled by better-than-expected US jobs report.

Data showed that non-farm payrolls in the US increased more-than-estimated by 200.0K in January, compared to market anticipations for an advance of 180.0K. Non-farm payrolls had recorded a revised gain of 160.0K in the prior month. Further, the nation's average hourly earnings of all employees grew 0.3% on a monthly basis in January, beating market expectations for a rise of 0.2%, thus boosting hopes that inflation will push higher as tighter labour market is finally fuelling wage growth. In the previous month, average hourly earnings of all employees had recorded a revised rise of 0.4%. Moreover, the nation's unemployment rate remained unchanged at a 17-year low rate of 4.1% in January, meeting market expectations.

Other data revealed that the US final Reuters/Michigan consumer sentiment index registered a drop to a level of 95.7 in January, less than a flash print indicating a fall to a level of 94.4. The index had registered a level of 95.9 in the prior month. On the contrary, the nation's factory orders climbed more-than-expected by 1.7% on a monthly basis in December, after recording a revised similar rise in the prior month and compared to market expectations for a rise of 1.5%. Meanwhile, the nation's final durable goods orders rose less than initially estimated by 2.8% in December, while the preliminary figures had indicated a gain of 2.9%. Durable goods orders had registered a revised increase of 1.7% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2456, with the EUR trading slightly higher against the USD from Friday's close.

The pair is expected to find support at 1.2405, and a fall through could take it to the next support level of 1.2353. The pair is expected to find its first resistance at 1.2513, and a rise through could take it to the next resistance level of 1.2569.

Moving ahead, investors would keep a close watch on the final Markit services PMIs for January, scheduled to release across the Euro-zone in a few hours. Additionally, the Euro-zone's Sentix investor confidence index for February as well as retail sales for December, will also be eyed by traders. Later in the day, the US ISM non-manufacturing and the final Markit manufacturing PMIs for January, will attract a lot of market attention.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving average

UK’s Construction Sector Growth Dipped To A 4-Month Low Level In January

For the 24 hours to 23:00 GMT, the GBP declined 0.93% against the USD and closed at 1.4123 on Friday, after UK's construction PMI showed a poor performance in January.

Data revealed that activity in UK's construction sector slumped to a 4-month low level in January, after the Markit construction PMI sharply eased to a level of 50.2, as uncertainty surrounding Brexit led to a sharp slow-down in new orders. Markets were expecting the PMI to drop to a level of 52.0, after recording a level of 52.2 in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.4115, with the GBP trading 0.06% lower against the USD from Friday's close.

The pair is expected to find support at 1.4041, and a fall through could take it to the next support level of 1.3967. The pair is expected to find its first resistance at 1.4231, and a rise through could take it to the next resistance level of 1.4347.

Trading trend in the Pound today is expected to be determined by the release of UK's Markit services PMI for January, set to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.