Sample Category Title

Dollar Vulnerable Ahead Of NFP Report, Bitcoin Tumbles

The battered Dollar weakened against its major peers this week, as investors closely evaluated the fundamental factors that are weighing heavily on the currency.

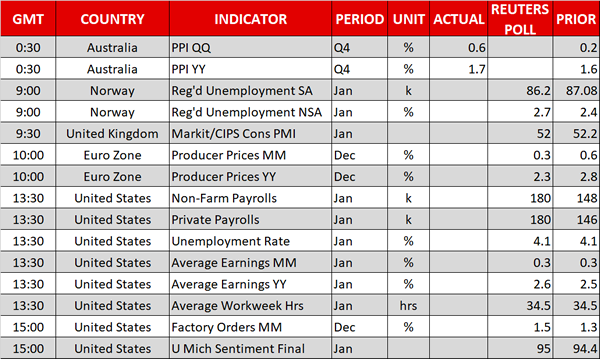

Friday's key event risk will be the US jobs report for January, which should offer fresh insight into the health of the US labor market. With the Federal Reserve expressing optimism over inflation rising this year and a brighter outlook for the economy, today's NFP report will be in sharp focus. Markets expect the US economy to have gained 180k jobs in January, with average earnings up by 0.3%, while the unemployment rate is expected to remain unchanged at 4.1%.

While every detail of the US jobs report is critical, there will be a strong focus on wage growth. Any signs of wage growth accelerating could stimulate expectations of rising inflation, ultimately lifting the prospects for further US interest rate increases this year. With the Dollar clearly in need of a lifeline, it will be interesting to see if January's US jobs report comes to the rescue. A scenario where the headline jobs number and wage growth both dish out upside surprisesmayoffer the Dollar some support.

Focusing on the technical picture, the Dollar Index remains firmly bearish on the daily charts. Technical lagging indicators, such as the 50 Simple Moving Average and MACD both go in line with the bearish bias. Repeated weakness below 89.00 may invite a further decline towards 88.50 and 88.00, respectively. Alternatively, a move back above 89.35 could spark an incline back to 89.60 and 90.00.

Commodity spotlight – Gold

Gold prices appreciated for the second straight session on Thursday, as a softening US Dollar stimulated investor appetite for the yellow metal.

Prices remain nearly unchanged during early trading on Friday, ahead of the heavily anticipated US jobs report scheduled forrelease this afternoon. Gold bulls could receive fresh inspiration to elevate prices higher towards $1360, if the NFP report disappoints. Alternatively, a solid US jobs report could trigger a technical correction which sends the metal back to $1340. From a technical standpoint, we remain bullish on Gold on the daily charts, as there have been consistently higher highs and higher lows. The new higher low around $1333 may create a foundation for Gold to test $1360 and higher.

Bitcoin struggles to fight back

It has certainly been a horribly bearish trading week for Bitcoin, thanks to heightened fears of a regulatory crackdown.

The growing confusion revolving around the Indian government's view on cryptocurrencies sparked uncertainty on Thursday, consequently exposing Bitcoin to downside risks. With US regulators closely scrutinizing one of the world's largest digital exchanges and Facebook Inc banning adverts that promote cryptocurrencies, Bitcoin is in trouble. Price action suggests that bears are clearly in control, with further losses on the cards as jitters over regulation erode investor appetite further. From a technical standpoint, Bitcoin is firmly bearish on the daily charts. The breakdown below $9000 may encourage a further decline towards $8400 and $8000, respectively.

Dollar Retreats Despite Rising Yields, US Jobs Report In The Spotlight

Here are the latest developments in global markets:

FOREX: The dollar index was practically unchanged on Friday ahead of the US employment data, after it previously posted notable losses on Thursday. The yen tumbled against its major peers, weighed on by the BoJ's regular bond-buying operations, which pushed Japanese bond yields lower.

STOCKS: Japanese markets retreated despite the overnight tumble in the yen. The Nikkei fell 0.9%, while the Topix pulled back 0.3%. In Hong Kong, the Hang Seng was in the green, though not by much. In Europe, futures tracking the Euro STOXX 50 were in negative territory. Finally, in the US, the major indices were mixed yesterday. The Dow Jones closed marginally higher, though the S&P 500 and the Nasdaq Composite both finished lower. The recent underperformance of US equities is being attributed to the continued surge in US Treasury yields. As yields rise, bonds begin to offer a higher and “safer” return for investors, thereby curbing demand for stocks. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently in negative territory.

COMMODITIES: Oil was one of the biggest movers on Friday, with WTI and Brent crude surging 0.5% and 0.4% respectively. Today, oil traders are likely to focus on the Baker Hughes US oil rig count, in order to gauge whether US producers have continued to increase their output in the face of elevated prices. Meanwhile, gold prices were little changed, with the precious metal last trading near $1348 per ounce.

Major movers: Dollar softens ahead of employment data

The greenback tumbled once more during the European trading session on Thursday, with no clear catalyst behind the move. Interestingly enough, the dollar retreated even despite a spectacular surge in US Treasury yields, something that usually supports the currency. The 10-year yield rose to a fresh high - it's highest since April 2014 - last trading near 2.79%, while 30-year yields broke above the 3% milestone, last trading around 3.03%. The biggest gainers from the tumble in the US currency were the euro and sterling.

Today, dollar-traders will turn their eyes to the US employment report for January. Since the US economy is already considered to be near full employment conditions, investors are likely to focus more on wage growth as opposed to jobs added, as they try to gauge whether inflationary pressures are beginning to intensify.

Despite the softer tone in the greenback, dollar/yen actually rose 0.2% on Friday, underpinned by the BoJ's bond-buying operations. The Bank stepped into the market and offered to buy “unlimited” amounts of bonds in order to curb Japanese yields from rising. Such actions are typical under the Bank's QQE with yield-curve control framework. The BoJ has committed to keeping 10-year yields near 0%, so every time yields approach 0.1%, it steps into the market to push them back down.

Elsewhere, the antipodean currencies retreated, with both aussie/dollar and kiwi/dollar declining nearly 0.4%

Day ahead: US NFP report dominates attention; UK releases construction PMI; eurozone producer prices due

The UK will see the release of the Markit/CIPS construction PMI for the month of January at 0930 GMT. The measure is projected to decline for the second straight month, but at 52.0 - should expectations materialize - it would remain in growth territory (above 50). Yesterday's manufacturing PMI for the same month surprised to the downside, leading to sterling weakness. The respective PMI figure for the much more important for the UK economy services sector will be released next week (Monday).

Eurozone data on December producer prices will be made public at 1000 GMT. Prices are expected to reflect a slowdown on both a monthly and an annual basis.

Without a doubt the highlight of the day - and the release having the capacity to spur sharp movements in dollar pairs - will be the US nonfarm payrolls report for the month of January due at 1330 GMT. The number of positions added to the economy is anticipated to have bounced up after some weakness in December on the back of poor weather conditions; forecasters project the addition of 180k jobs versus 148k in December. The unemployment rate is expected to remain at the 17-year low of 4.1%, but yet again investors' focus is likely to turn on wage growth. Average hourly earnings are expected to grow at a monthly rate of 0.3%, the same as in December, while on an annual basis they're projected to expand by 2.6% - this compares to 2.5% in December. Growth in wages has the potential to alter the outlook for inflation and thus affect the Federal Reserve's tightening cycle.

Later in the day (at 1500 GMT), the US will see the release of data pertaining to December's factory orders, as well as the University of Michigan's final reading on consumer sentiment for the month of January.

In energy markets, the US Baker Hughes oil rig count is due at 1800 GMT.

Policymakers making appearances include ECB executive board member Benoit Coeure who will be speaking at the conference titled “Deepening of EMU” at 1000 GMT, and Fed Bank of Dallas President Robert Kaplan - a non-voting FOMC member in 2018 - who will be participating in a Q&A session before the Teacher Retirement System of Texas Annual Conference at 1830 GMT. Fed Bank of San Francisco President John Williams - a voting FOMC member in 2018 - will be talking about the US economy before the Financial Women of San Francisco at 2030 GMT.

Energy companies Chevron and Exxon Mobil and pharma firm Merck & Co. are among firms releasing quarterly results on Friday. All three will be releasing their reports before the US market open.

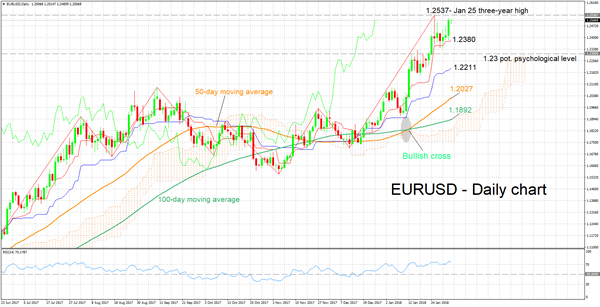

Technical Analysis: EURUSD trades near highest since late 2014; RSI overbought

EURUSD is trading not far below its highest since December 2014 of 1.2537 hit on January 25. Technical indicators are projecting a bullish picture in the short-term: the Tenkan- and Kijun-sen lines are positively aligned and the RSI is well into bullish territory (above 50) and continues rising. The fact that the RSI has crossed above the 70 overbought level though, could be a sign that a short-term pullback in not to be ruled out.

A disappointing US jobs report - especially on the wage growth front - is likely to see the pair rising. In this case, last week's three-year high of 1.2537 might act as immediate resistance. An upside break, which is not that unlikely in this scenario given that price action is currently taking place close to the aforementioned high, would shift focus to the area around 1.26 as another barrier to the upside; 1.26 being a potential psychological level.

On the downside and in case of a strong NFP report, EURUSD could find support around the current level of the Tenkan-sen at 1.2380. The area around this point also encapsulates 1.24, this being another mark that may be of psychological significance.

US NFP Data To Set The Trading Tone | Cryptos Still Suffering

Gold up ahead of US NFP data

Cryptocurrencies still under pressure

Dollar index could move higher

Oil markets looking more balanced

GOLD

Gold has bounced back up today and any losses posted during Thursday's sessions are wiped off. However, caution is the word which everyone is focused on today ahead of the mother of all data - the US NFP number. The stronger than expected average hourly earning would confirm that the US labour market is picking up further strength and this could make the dollar stronger. Usually, the relationship between the US dollar and gold is negative however, this relationship does become out of a whack sometimes. A strong US NFP today would provide more confidence for the Fed to increase the interest rate coming in March which may not be as positive for the gold price. Improving consumer sentiment and wage growth would pave the way for higher inflation forecast which would be a combat by the central banks by tighter monetary policy, as US equities further suffer as US Treasury prices take further blows

FOREX

The USD ISM Manufacturing data coming in at levels better than expected, and the FED’s hawkish tone were not enough to contain the dollar bears today with the DXY sliding down to 88.6. The dollar’s overnight rally proved short-lived with US 30-year Treasury yields rising above 3%, providing fuel for the Euro to break above $1.25 and cable to increase 0.6%. However, recent data suggests that Investors are gambling on reduced equity volatility in the days ahead, suggesting that the equity market bull run may come to a halt, reducing the dollar sell-off

Cryptocurrency

The announcement from India’s finance minister that cryptocurrency was not legal tender in the country worsened the crypto market correction with the overall crypto market cap plummeting below $500 billion. Bitcoin dips below $9000. We think that the price could be moving towards the 200-day moving and that would be the real test for the market. Bitcoin below 10K tells you only message which is the upward momentum has died out and the odds are that we would continue to consolidate or grind lower.

Oil

Biggest economies of the world are doing well and this supports the demand for oil. Simply put, there is a lot of optimism in the market as the oil market increasingly look more balanced in terms of supply and demand. If the situation continues to improve at this pace, we could see the oil equation improving much quicker than OPEC’s anticipation further. The dollar drop was enough to stimulate another bullish rally for oil with Brent up over 1%, but still remaining shy of last week’s 3-year high.

Technical Outlook: EURUSD Holds Firm Tone And Trading Around 1.25 Handle Ahead Of US Jobs Data

The Euro remains firm in early Friday's trading and trading around 1.25 handle which was broken on Thursday's rally. Manufacturing data from the Eurozone showed solid results on Thursday, signaling that growth of bloc's economy is on firm path, which could further fuel expectations that the ECB is on track for tightening monetary policy. Near-term technical outlook improved as the pair broke above triangular consolidation and shifted focus higher. Thursday's long bullish candle underpins for eventual break through barriers at 1.2517/37 (Fibo 38.2% of 1.6039/1.0340, 2008/2017 fall/25 Jan peak, the highest since Dec 2014) and extension towards next target at 1.2597 (Fibo 61.8% of larger 1.3992/1.0340 descend). Close above 1.2517/37 will generate strong bullish signal for continuation of larger uptrend from 1.0340 (2017 low). Asian low at 1.2486 marks initial support with more significant 1.2400 support, provided by rising 10SMA and 4-hr cloud top. US jobs data are in focus today and expected to provide fresh signals for the greenback, as hawkish Fed on Wednesday inflated the currency but positive signals from the central bank need further confirmation which could be expected on solid numbers from the US labor sector. US Non-Farm payrolls are forecasted to rise 184K in Jan, compared to previous month's 148K, while other key parameters, average earnings and unemployment rate are expected to stay unchanged at 0.3% and 4.1% respectively.

Res: 1.2537, 1.2567, 1.2597, 1.2630

Sup: 1.2486, 1.2453, 1.2428, 1.2400

Currencies: Dollar Struggles Despite Sharp Rise In US Yields

Sunrise Market Commentary

- Rates: Inflation (expectations) on the rise

Market-based inflation expectations resumed their march higher and so did US yields. The curve significantly bear steepened. Today's eco calendar contains the US labour market report. The bar for average hourly earnings is rather low. Beating it could resume current trends while a disappointment could trigger some short covering ahead of the weekend. - Currencies: Dollar struggles despite sharp rise in US yields

Yesterday, the dollar hardly profited from a new up-leg in US yields. EUR/USD even holds near its multi-year peak. The yen declined slightly this morning as the BOJ stepped up its easing efforts. Later today, focus for USD trading turns to the US payrolls. In the current environment, there is no guarantee that strong payrolls will trigger a sustained USD rebound

The Sunrise Headlines

- US stock markets ended nearly unchanged, outperforming Europe yesterday. The Nasdaq slightly underperformed (-0.35%) ahead of big US tech earnings. Asian risk sentiment is negative overnight with Korea underperforming.

- The BOJ offered to buy an unlimited amount of bonds at a fixed rate for the first time since July, backing up its repeated stance that actions by its peers and global yields wouldn't dictate its policy.

- Stronger iPhone prices and hints that Apple could return more than half of its $285 bn in cash to shareholders eased concerns among investors, even as the company gave a disappointing revenue outlook for the current quarter.

- Google parent Alphabet confounded WS with news of a big jump in costs in the final quarter of last year, along with fresh evidence of increasing pressure on profit margins as it becomes more dependent on mobile advertising.

- The White House will likely give Congress approval to make public a secret Republican memo alleging FBI bias against President Trump in its Russia probe, an official said, as tensions over the disputed document gripped Washington.

- The EU will hold out the prospect of membership to western Balkan countries (6) by 2025 as it seeks to breathe new life into enlargement, strengthen controls on migration, and counter Russian influence in the volatile region.

- Today's eco calendar contains US payrolls, the unemployment rate and average hourly earnings. Fed Kaplan, Fed Williams and ECB Coeuré are scheduled to speak.

Currencies: Dollar Struggles Despite Sharp Rise In US Yields

Dollar struggles despite sharp rise in US yields

Wednesday's positive Fed guidance didn't help the dollar much. EUR/USD returned temporary to ST support below 1.24, but the test was rejected. The US manufacturing ISM was strong. The US bond sell-off resumed after the report, but the dollar hardly profited. USD/JPY held up fairly well despite rising nervousness on the equity markets. The rise in USD yields didn't stop the EUR/USD rebound. The pair returned north of 1.25, but a break of the EUR/USD 1.2537 top didn't occur.

Overnight, Asian equities are mostly trading in the red. Mixed results from US tech giants and the bond sell-off are weighing. The BOJ offered to buy an unlimited amount of 10-yr bonds at a fixed rate (0.11%) signaling a disconnect from the trend to global policy/interest rate normalization. The yen declined slightly. USD/JPY trades at 109.75 and EUR/JPY north of 137. The euro is holding strong across the board. EUR/USD hovers near the 1.25 big figure.

Today, the focus is on the US Payrolls. Net job growth is expected at 180.000. The unemployment rate is expected unchanged at 4.1% and AHE at 0.2% M/M and 2.6% Y/Y (from 2.5%). A good report might solidify the recent uptrend in US yields. Of late that didn't help USD even if it widened interest rate differentials. The disconnect of the dollar from interest rate trends and eco data won't last forever, but for now the established trends are strong. Short-term, even a strong payrolls report is no guarantee for a USD rebound. We look out whether the rise in yields triggers a rise in volatility of risky assets even if the dollar apparently hasn't that much of a safe haven role to play. So, we need a technical sign (or new market theme) before concluding that the sharp repositioning ran its course. That sign is currently not available. Technical picture: the dollar decline slowed end of last week, but no meaningful rebound occurred, especially not against the euro. EUR/USD 1.2537/98 is the first topside resistance. A break would signal more trouble for the USD short term. EUR/USD 1.2323/35 is a minor support A break below 1.2165 would call off the ST downside alert (for the dollar).

Yesterday, a dip in EUR/GBP was reversed after a disappointing UK manufacturing ISM. The intraday rebound of EUR/USD also reinforced the intraday rise of EUR/GBP. Today, The UK construction PMI is expected little changed at 52.0. We expect sterling to stay in the 0.8690/0.8833 consolidation pattern.

EUR/USD near multi-year top going into US payrolls report

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5440; (P) 1.5507; (R1) 1.5623; More....

EUR/AUD surges to as high as 1.5622 as rebound from 1.5153 resumed. Intraday bias is back on the upside for 1.5770 resistance. At this point, we'd be cautious on strong resistance from there to limit upside and bring another decline. Below 1.5494 resistance turned support will turn intraday bias back to the upside. Nonetheless, sustained break of 1.5770 will confirm resumption of larger up trend from 136.24.

In the bigger picture, price actions from 1.5770 so far suggests that it's corrective in nature. That is, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

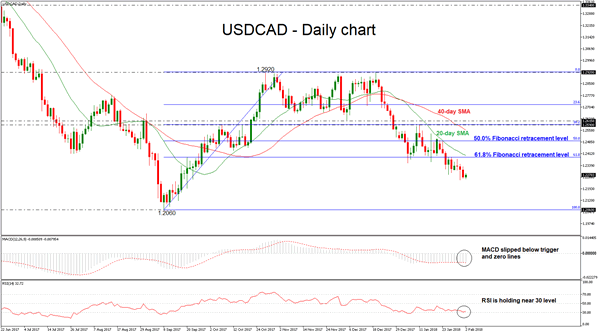

USDCAD Remains Under Pressure, Maintains Short-Term Bearish Bias

USDCAD has been developing lower over the last weekly sessions, after the strong pullback on the 1.2920 resistance level on December 19. The price broke several obstacles to the downside and ended Thursday’s session below the 1.2300 handle. Also, the short-term technical indicators are bearish and are pointing more weakness in the market.

In the daily timeframe, the RSI indicator stands in the negative territory and is flattening near the 30 level, whilst the MACD oscillator is strengthening its bearish movement as it created a downside crossover with its trigger line. In addition, the 20 and 40 simple moving averages are following the price fall.

If price remains below the 61.8% Fibonacci retracement level at 1.2390 of the up-leg from 1.2060 to 1.2920, it could open the way for the 1.2060 level, which is acting as a major support barrier, taken from the low on September 2017.

On the flip side, upside moves are likely to find resistance at 61.8% Fibonacci mark. Rising above this area, could help the pair to touch the 50.0% Fibonacci level of 1.2490. It is worth mentioning that prices need to go through the 20-day SMA before creating a significant bullish movement.

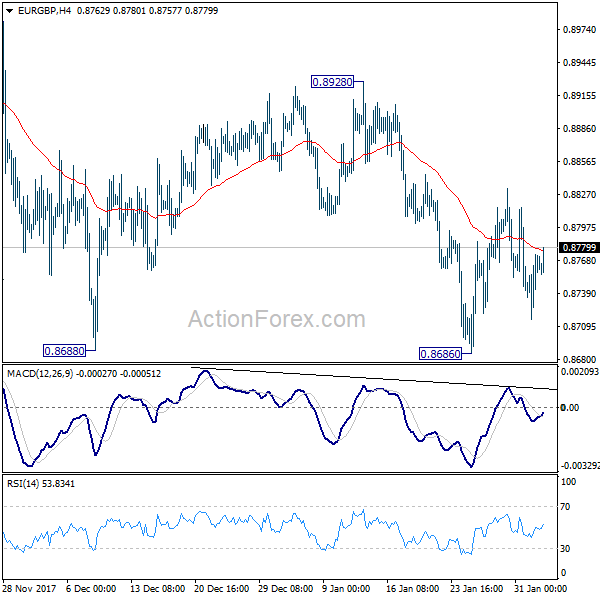

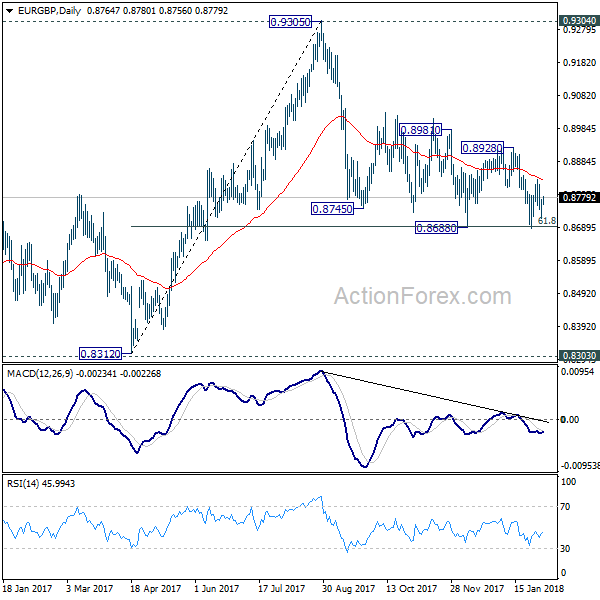

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8729; (P) 0.8752; (R1) 0.8788; More...

EUR/GBP continues to gyrate in range of 0.8686/8928 and intraday bias remains neutral. Outlook stays bearish with 0.8928 resistance intact. That is, fall from 0.9305 is expected to resume later. Break of 0.8686 will also have 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. In that case, deeper decline would be seen to retest 0.8303/8312 support zone.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

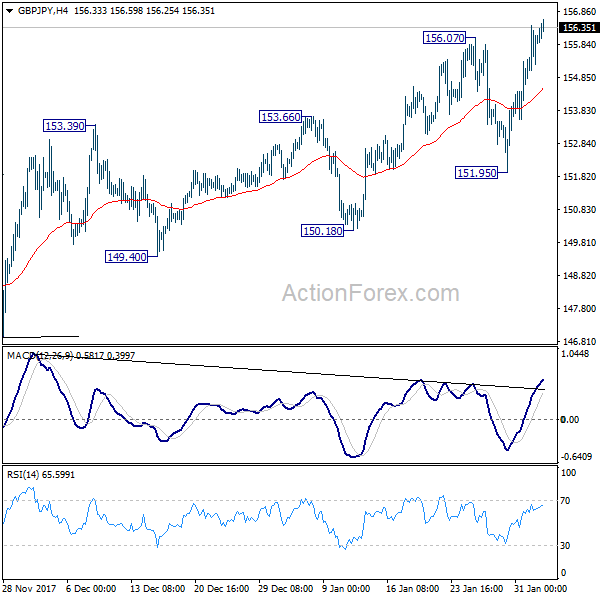

GBP/JPY Daily Outlook

Daily Pivots: (S1) 155.12; (P) 155.77; (R1) 156.69; More...

GBP/JPY rises to as high as 156.59 so far. Break of 156.07 indicates larger up trend resumption. Intraday bias is turned back to the upside. Current rally would target 100% projection of 139.29 to 152.82 from 146.96 at 160.49 next. On the downside, break of 151.95 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

Forex Analysis: US Nonfarm Payrolls Today

Today is Non-farm Payrolls day in the US. This data release is generally one of the most important of the month, being a leading indicator of consumer spending and economic health, made public shortly after it is calculated. It charts the change in the number of employed during the previous month. Also released at the same time will be the Unemployment Rate, which has dropped below the 2007 low during H1 2017. The continued fall has put further pressure on the Fed to normalise Interest Rates. Markets also focus on Average Hourly Earnings which is an indicator of labour inflation. Faster wage growth can lead to an increase in the pace of Fed hikes. There have been minimum wage increases in a number of states which could boost earning for January.

Swiss Real Retail Sales (YoY) (Dec) was 0.6% v an expected 1.5%, from -0.2% previously, which was revised up to 0.3%. USDCHF sold off from 0.92320 to a low of 0.93031 after this data was released.

German Markit Manufacturing PMI (Jan) was 61.1 v an expected 61.2, from 61.2 previously. Eurozone Markit Manufacturing PMI (Jan) was as expected, unchanged at 59.6. EURUSD moved higher from 1.24274 to 1.24493 following this release.

UK Markit Manufacturing PMI (Jan) was 55.3 v an expected 56.5, from 56.3 previously, which was revised down to 56.2. GBPUSD moved lower from 1.42631 to a low of 1.42018.

US Continuing Jobless Claims (Jan 19) was 1.953M v an expected 1.928M, from 1.937M previously, which was revised up to 1.940M. Initial Jobless Claims (Jan 26) was 230K v an expected 238K, from 233K previously, which was revised down to 231K. Nonfarm Productivity (Q4) was -0.1% v an expected 1%, from 3% previously, which was revised down to 2.7%. Unit Labour Costs (Q4) were 2.0% v an expected 0.8%, from -0.2% prior, which was revised up to -0.1%. USDJPY moved lower from 109.590 to 109.274 from this data release.

Canadian Markit Manufacturing PMI (Jan) was released at 55.9 v an expected 54.8, from 54.7 previously. USDCAD sold off from 1.23218 to 1.22677, moved by this release.

US Markit Manufacturing PMI (Jan) was 55.5 v an expected 54.9, from 55.5 previously.

US ISM Prices Paid (Jan) was 72.7 against a consensus of 68.0. The previous reading was 69.0. ISM Manufacturing PMI (Jan) was also out at this time, coming in at 59.1 v an expected 58.8, from 59.7 prior, which was revised down to 59.3. And finally, Construction Spending (MoM) (Dec) was 0.7% against an expected 0.4%, from the previous reading of 0.8%, which was revised down to 0.6%. EURUSD moved higher from support at 1.24314 to a high of 1.24975.

New Zealand Building Permits s.a. (MoM) (Dec) were -9.6% form 10.8% previously, which was revised down to 9.6%.

EURUSD is down -0.15% overnight, trading around 1.24894.

USDJPY is up 0.38% in early session trading at around 109.801.

GBPUSD is down -0.04% to trade around 1.42544.

USDCAD is up 0.20%, trading around 1.22894.

Gold is down -0.10% in early morning trading at around $1,347.05.

WTI is up 0.12% this morning, trading around $65.95.

Major data releases for today:

At 09:30 GMT, UK PMI Construction (Jan) is expected to be 52.0 from 52.2 previously. GBP pairs may be moved by this release.

At 10:00 GMT, Eurozone Producer Price Index (YoY) (Dec) is expected to be 2.3% from a previous reading of 2.8%. EUR currency pairs may be moved by this data point.

At 13:15 GMT, US Non-Farm Payrolls (Jan) is expected at 180K v a prior 148K. This measures the change in the number of employed people in January. The Unemployment Rate (Jan) is expected unchanged at 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during December. Average Hourly Earnings (YoY) (Jan) is expected to be 2.6% form 2.5% previously. Average Weekly Hours (Jan) is expected to be unchanged at 34. Labor Force Participation Rate (Jan) is expected to be 62.8% from a prior reading of 62.7%. USD crosses could experience volatility around these data releases.

At 15:00 GMT, US Factory Orders (MoM) (Dec) is expected to be 1.5% from 1.3% previously. USD pairs may be moved by this release.

At 18.00 GMT, Baker Hughes US Oil Rig Counts will be released, with a headline number from last week of 759. The expected number this week is 758. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

At 19:30 GMT, FOMC Member Williams will speak about the US economic outlook at the Financial Women of San Francisco luncheon. A questions and answers session will follow.