Sample Category Title

Market Morning Briefing: Pound Has Moved Up Beyond Immediate Resistance Near 1.42 On The 3 Day Candles

STOCKS

Dow (26186.71, +0.14%) is held well by support near 26000. While above 25700-26000 region, the index may attempt to move higher towards 26500 in the near term.

Dax (13003.90, -1.41%) came off sharply to test 13000 on the downside. This is an important level for the near to medium term. If the support at 13000 holds, the index could move back to levels near 13300 or higher; else a fall below 13000 could easily take it down towards 12800-12700 in the medium term.

Nikkei (23181.34, -1.30%) is almost trapped in the 23000-23600 region and is unable to decide which direction to take. A possible test of support near 22800 is possible before it bounces back towards 23400-23600 levels. Overall range-bound movement is likely to be seen in the near term.

Shanghai (3440.49, -0.19%) has been coming off sharply and could test levels near 3350 which is a medium term support coming from May’17. While 3350 holds, a bounce back towards 3400-3450 is possible in the longer term. Near term looks bearish.

Yesterday the Indian stock indices saw some volatility as the Bugdet statement was laid out, but surprisingly recovered almost the whole of the dip by the end of the session. It is most likely that Nifty (11016.90, -0.10%) and Sensex (35906.66, -0.16%) have already made a near term top and that the corrective dip could begin any time sooner. While below the recent highs, we may expect a dip next week or at least some sessions of sideways consolidation. Near term targets for Nifty and Sensex are 10800 and 35500 respectively, considering a test of these levels were almost seen yesterday.

COMMODITIES

Brent (69.79) and WTI (66.04) have risen. Although we were looking at a rise in Brent and a small dip in WTI, both have risen sharply from levels seen yesterday. While immediate support near 68 holds on Brent, it may target 71-72 in the near term. WTI on the other hand is respecting support near 64 and while that holds, it could move up towards 67 to make fresh highs within the current rally.

Gold (1347.85) has moved up as expected and could be headed towards 1350-1360 while above 1340 support. Watch price action near 1350-1360 to get an indication on further course of direction.

Copper (3.21) has moved up to test immediate resistance near 3.225. While that holds, a dip back towards 3.1750 is possible; else a rise above 3.225, if seen and sustains, could lead to a rise towards 3.25-3.26 in the near term.

FOREX

Dollar Index (88.757) has dropped below 89 and is now testing support on the daily line charts near 88.6-88.7. There is similar support near 88.8-88.9 on the weekly line chart. There are good chances for this support zone of 88.6-88.9 to hold. We still await for the correlation between Dollar strength and high US yields to resurface in the days to come.

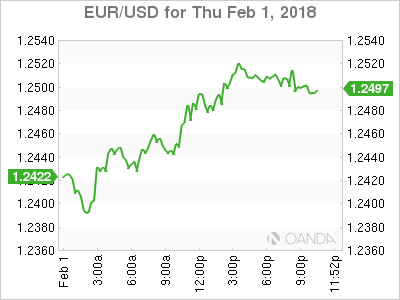

Contrary to our expectations, Euro (1.2495) has moved up afresh instead of dipping. It reached a high of 1.2516 today and is currently trading just below 1.25. Resistance is seen between current levels and 1.26 on the Weekly Line chart. This is a crucial resistance level and we will have to wait and watch if a dip from here towards 1.23 (support on weekly candles) happens in the days ahead.

The Euro-Rupee quotes higher at 80.02 and could head further up to 82 also, suggesting Euro strength and Rupee weakness might both sustain for a while.

Dollar-Yen (109.64) is strengthening as the Bank of Japan has reacted aggressively to the recent rise in Japanese yields (see Interest Rates below) by increasing its bond purchases. With the Japanese govt and Central Bank not seeming to favour Yen strength, it will be interesting to see if an increasing yield spread between US and Japanese bonds (in favour of US bonds) will strengthen Dollar Yen in the coming days. For now, Dollar Yen is at resistance near 109.7 on the daily candles and if this resistance holds, there could be a slight dip towards 109 in the current session.

Euro-Yen (137.06) has moved up well past 136 as Dollar-Yen (109.64) has remained stable at relatively elevated levels. However, there is crucial Resistance coming up near 138 on the Euro-Yen, which can hold, especially as Dollar-Yen has some chances of starting to fall afresh. Note that Yen-Rupee (0.5846) also looks potentially bullish.

Pound (1.4270) has moved up beyond immediate resistance near 1.42 on the 3 day candles. It should find resistance at 1.43-1.44 (1.43 is seen as next resistance level on the 3 day line chart and 1.44 is seen as next resistance level on the weekly candles).

Dollar-Rupee (64.02) – Expected roadmap for the next few days... (A) see 64.1075 tomorrow (B) then we might see a dip to 63.90-80 (C) after that we may see a fresh rise to 64.15-17. Where the market will go from 64.17 will have to be seen.

INTEREST RATES

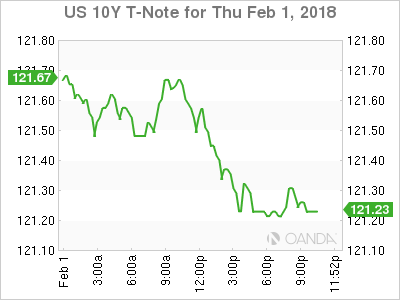

US bonds sell off seem to be continuing globally as confidence in the US economy increases and inflation expectations remain strong. Yesterday’s statement by the FOMC confirming that inflation expectations are indeed on an uptrend, is lending support to the present sell off. Parallely, positive growth and inflation sentiments in the Euro zone countries is leading to a rise in German bond yields as well. Japan on the other hand seems to be panicking with a rise in 10 year yield beyond 0.1% (happened yesterday) and is trying its best to keep the yield below 0.1% and nearer to the targeted 0%.

US 10 Yr (2.7915%), 30 Yr (3.0299%), 5 Yr (2.5745%) & 2 Yr (2.1690%) – On Wednesday, the shorter term yields had risen significantly with the rise in longer term yields being less. Yesterday, the opposite happened with both 10 Yr and 30 Yr yields rising almost 8 basis points, lending some relief to the yield curve flattening which happened yesterday. We repeat that 5 Yr and 2 Yr are very near to long term resistance levels near 2.5-2.6% and 2.2% respectively (these resistances are shown on long term charts in our January Treasury report – available on request). Both these resistances are seen on trend lines which join resistance levels over the last 30 years – thereby making us believe that the short term yields shouldn’t rise much further.

Yield spreads have come back near respective support levels as the recent hovering around support levels continues. US 10 Yr-5Yr (0.217%) is above 0.2% (seen as support on short term charts) and US 30 Yr – 10 Yr (0.2384%) is almost touching 0.24% (seen as support on long term charts).

Japanese 10 Year Yield (0.088%) is back below 0.1% after the Bank of Japan increased its bond purchases in response to the rise in yields. We could see the Bank of Japan now making sure that the yield stays below resistance near 0.088%-0.9% on the short term charts.

German 10 Year yield (0.721%) is rising fast and could target 0.9% on the upside in coming weeks (this high was last seen in June-July 2015).

AUDUSD – Sells Off, Remains Vulnerable

AUDUSD - The pair looks to weaken further after selling off during Thursday trading session. On the downside, support resides at the 0.7950 level where a breach will aim at the 0.7900 level. Below that level will set the stage for a run at the 0.7850 level with a cut through here targeting further downside pressure towards the 0.7800 level. On the upside, resistance lies at the 0.8050 level. A cut through here will turn attention to the 0.8100 level and then the 0.8150 level where a violation will set the stage for a retarget of the 0.8200 level. On the whole, AUDUSD faces further bear threats.

USD Struggles Ahead Of Jobs Report

US expected to add 184,000 jobs in January

The US dollar fell against a basket of currencies on Thursday. The greenback has failed to gain traction in 2018 and is awaiting the first US jobs report of the year looking for a shot in the arm. The U.S. non farm payrolls (NFP) will be published on Friday, February 2 at 8:30 am EST. Economists are expecting the US to add 184,000 positions and keep the unemployment rate at 4.1 percent. Last month’s report came in lower than expected but the saving grace for the USD was that hourly wages grew 0.3 percent as expected. There are similar gains forecasted for January wages with a special emphasis on inflationary data as the Fed ponders what to do with stagnant wages despite a strong job component.

- European manufacturing gathered steam in January

- Unemployment claims fell last week in evidence of strong US labour market

- Higher growth expectations outside of US putting pressure on dollar

Dollar Lower Despite Support from Central Bank

The EUR/USD gained 0.82 percent on Thursday. The single currency is trading at 1.2515 a day after the U.S. Federal Reserve kept rates unchanged and ahead of the release of the January’s U.S. non farm payrolls (NFP) report. Strong manufacturing data out of Europe continued to make the case for accelerated growth. The European Central Bank (ECB) did not make any changes to its QE program or interest rate in January, but with higher growth and inflation expectations are rising that its bond buying program could end this year with a possible rate hike.

US economic growth continues to soldier on, with the U.S. Federal Reserve forecasted to lift interest rates 3 to 4 times in 2018. Strong fundamentals and a supportive central bank should have the USD higher versus the euro, but political uncertainty going into the midterms has impaired the dollar. Employment has been the pillar of the economic recovery, but at near full employment there is little that even a monster jobs report can do to boost the dollar. The ADP private payrolls report released on Wednesday saw 234,000 jobs added in January, and while there is no perfect correlation between the ADP and the NFP, after the disappointing jobs report in December an improvement is anticipated which could help the USD finish the week higher versus other currencies.

The USD has fallen 3.25 despite so far this year and comments from the Fed that inflation is expected to rise helped only a little. The FedWatch tool by the CME is showing a 83.1 percent probability of a rate hike in March after the release of the FOMC January statement. Growth and interest rate rises have all been priced in, but for some investors the threat of higher political uncertainty during the midterms is a cause for concern.

Next week will offer the USD less opportunities to shine as the main indicator release will be the non manufacturing PMI related by the ISM. Services have slowed down since reaching a reading of 60.1 in October with the forecast for the January figures to be around 55.9.

US bond prices have fallen as a result of higher growth and inflation expectations this year and yields are higher seeking to attract investors that have been tempted by fixed income alternatives overseas.

The USD has been on the back foot against major currencies for most of 2018. The rally that followed the victory of Donald Trump in the November 2016 elections was driven by tax reform and infrastructure promises. The 12 month period before the promise and the reality proved to be too much for a market that was expecting a quicker turn around and the greenback depreciated in 2017. This year follows a similar trend with the euro hitting three year highs and even the pound recovering to pre-Brexit levels thanks to a softer dollar.

Market events to watch this week:

Friday, February 2

4:30am GBP Construction PMI

Gold Ticks Lower, Investors Eye Nonfarm Payrolls

Gold has posted small losses in the Thursday session. In North American trade, the spot price for an ounce of gold is $1343.22, down 0.14% on the day. On the release front, employment data was positive, as unemployment claims dropped to 230 thousand, below the forecast of 237 thousand. ISM Manufacturing PMI slowed to 59.1, but still beat the estimate of 58.7 points. ISM Manufacturing PMI slowed to 59.1, but still beat the estimate of 58.7 points. On Friday, the spotlight will be on employment numbers, with the release of wage growth, nonfarm payrolls and the unemployment rate. As well, the US releases UoM Consumer Sentiment.

As expected, the Federal Reserve held the course on interest rate policy at its January meeting on Wednesday. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What was more noteworthy was that the Fed predicted that inflation would rise to the Fed’s 2 percent target this year. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to “remain somewhat below 2 percent.” Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

Gold posted gains last week, taking advantage of a USD sell-off. However, the dollar has steadied this week, and gold prices are slightly lower. Since the start of the year, gold is up 2.2%, joining the major currencies which have posted gains against the greenback in 2018. This has been somewhat of a surprise, as the robust US economy has supported risk appetite, yet gold has not lost its luster early in 2018. Last week, gold climbed to $1366, its highest level since August 2016.

British Pound Shrugs Off Soft Manufacturing Report, Construction PMI Next

The British pound has posted gains in the Thursday session. In North American trade, GBP/USD is trading at 1.4247, up 0.41% on the day. On the release front, British Manufacturing Production slowed to 55.3, shy of the estimate of 56.5 points. In the US, employment data was strong, as unemployment claims dropped to 230 thousand, below the forecast of 237 thousand. ISM Manufacturing PMI slowed to 59.1, but still beat the estimate of 58.7 points. ISM Manufacturing PMI slowed to 59.1, but still beat the estimate of 58.7 points. On Friday, the spotlight will be on employment numbers, with the release of wage growth, nonfarm payrolls and the unemployment rate. As well, the US releases UoM Consumer Sentiment.

Britain’s economy is expected to worsen after it departs the European Union, but any worries over the economy are not hurting the British pound, which has enjoyed a strong January. The currency has jumped 5.2% gain in January, as the USD selloff saw the dollar’s rivals post strong gains. Last week, the pound pushed above 1.43, its highest level since June 2016. On the political front, Theresa May is facing strong domestic criticism over her handling of Brexit, and there has even been talk of a no-confidence vote in parliament. For their part, the Europeans are still smarting from Britain’s decision to leave the club, and are not in a giving mood, with barely a year for the sides to reach a trade deal before the Brexit deadline in March 2019.

In the latest Brexit development, the EU has drafted guidelines regarding a transition period after Brexit until December 2020. The European proposal calls for Britain to abide by EU rules, including freedom of movement, during the transition period which would last until 2020. However, on Wednesday, Prime Minister May said that EU citizens arriving in the UK during the transition period would be subject to stricter rules than those living in the UK before Brexit takes effect in March 2019. A strong EU reaction was not late in coming, with Guy Verhofstadt, the European parliament’s Brexit coordinator, stating that the EU would not accept two sets of rights for EU citizens.

There were no major surprises from the Federal Reserve policy meeting, the final one under Janet Yellen’s watch. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What caught investor’s attention was that the Fed forecast that inflation would rise this year to the Fed’s target of 2 percent. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to “remain somewhat below 2 percent.” Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

Yen Subdued, Markets Await US Nonfarm Payrolls

The Japanese yen is trading sideways in the Thursday session and continues to have a quiet week. In North American trade, USD/JPY is trading at 109.28, up 0.08% on the day. On the release front, Japanese Final Manufacturing PMI improved to 54.8, above the estimate of 54.4 points. In the US, key indicators were mixed. Unemployment claims dipped to 230 thousand, below the forecast of 237 thousand. ISM Manufacturing PMI slowed to 59.1, but still beat the estimate of 58.7 points. On Friday, the spotlight will be on employment numbers, with the release of wage growth, nonfarm payrolls and the unemployment rate. As well, the US will release UoM Consumer Sentiment.

There were no major surprises from the Federal Reserve policy meeting, the final one under Janet Yellen’s watch. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What caught investor’s attention was that the Fed forecast that inflation would rise this year to the Fed’s target of 2 percent. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to “remain somewhat below 2 percent.” Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

The Bank of Japan has continually said that it has no plans to end its massive stimulus program, but may have sent its most direct message (warning?) on Wednesday. The Bank increased its purchases of 3-5 year government bonds (JGB), while at the same time senior members were on the offensive. BoJ Governor Haruhiko Kuroda and Deputy Governor Kikuo Iwata said that the Bank would maintain “powerful” easing as long as inflation was well of the BoJ target of 2 percent. Iwata stressed that the BoJ had no plans to change its yield target levels “for the time being”. Under current yield curve policy, short-term interest rates are at -0.10% and 10-year government bonds are at 0.0%. The Japanese economy has heated up, raising speculation that the Bank could taper its stimulus program and even raise interest rates. However, the BoJ appears determined to hold the course until inflation moves higher.

New Month, Same Story For USD

The US dollar finished on the lows in the first trading day of February despite strong manufacturing data and a jump in Treasury yields. The euro was the top performer while the Australian dollar lagged; Bitcoin was battered. Australian PPI is up next. 7 out of the 8 existing Premium trades are currently in the green. We will lock in gains in some of these trades ahead of Friday's US jobs report.

Hopes that rising yields will give the US dollar a sustained lift are evaporating. The US 10-year yield jumped 7 bps to 2.78% but USD/JPY slipped to 109.30 from a high of 109.75. The euro is a handful of pips below the cycle high after a fresh push above 1.25.

The dollar got some good news on the data from with the ISM manufacturing index at 59.1 compared to 58.6 expected. Construction spending also beat at +0.7% versus +0.4% expected. On the flipside, auto sales were soft and so was productivity.

One thing we were watching closely was how the US dollar would perform after the turn of the calendar. There were plenty of reasons to think that end-of-the-month flows were at work and that's increasingly looking realistic. Even more disconcerting for USD bulls is that intraday swings in equity indices have little impact on USD.

Looking ahead, data will be the main focus of Australian dollar traders with the 0030 GMT PPI release. There is no consensus estimate but the prior was +0.2% q/q. Given that CPI was already reported, the effect is likely to be muted. One thing to note on AUD/USD is that the pair has risen in February in 14 of the past 16 years. This is easily the best month on the calendar for AUD.

US: Manufacturing Activity Remains Strong at the Start of 2018

The Institute for Supply Management (ISM) index of manufacturing for January printed at 59.1, largely unchanged from a downward revised 59.3 recorded in December, and ahead of market expectations of a slightly more pronounced decline to 58.8. This marks the 17th straight month that the index has been in expansionary territory.

The underlying details of the report were mixed, with the headline index benefiting largely from strong advances in inventories (+3.8 to 52.3) and supplier deliveries (+1.9 to 59.1). Employment (-3.9 to 54.2), new orders (-2.0 to 65.4), and production (-0.7 to 64.5) all fell back in January, coming off of cycle highs at the end of 2017.

Prices paid recorded a healthy gain of 4.4 points to 72.7, a new cycle high.

The spread between new orders and inventories – a good leading indicator of activity – narrowed to 13.1 (-5.8 points) in January after reaching a cycle-high of 18.9 in December. Overall this indicator remains consistent with manufacturing activity continuing to expand through the first quarter of 2018.

Key Implications

The stellar performance of the U.S. manufacturing sector continues into the New Year, with no clear end in sight. Healthy demand for U.S. manufactured goods should persist especially as savings from tax cuts arespent, and as long as healthy global demand persists. Better insight on the health of the U.S. economy at the start of 2018 will be gleaned from January car sales out later today, and tomorrow's payrolls report.

NZDUSD Holds in Narrow Range; Maintains Weak Bias in Near Term

NZDUSD has been trading within a consolidation area with upper boundary the 0.7420 resistance level and lower boundary the 0.7285 support barrier. The narrow range has been holding since January 24 where the price reached a five-month high of 0.7436, though it ended the day in the red and the bullish phase weakened.

In the 4-hour chart, short-term indicators are signaling a bearish movement. The Relative Strength Index (RSI) is flattening near the 50 level, while the MACD oscillator is weakening in the positive territory. Also, the latter oscillator recorded a bearish crossover with its trigger line, indicating further losses.

If prices extend the downward pressure, immediate support could come at the 0.7300 strong psychological level. Below that, the price could hit 0.7285, which is near the 23.6% Fibonacci retracement level of the last big upward movement with the low of 0.6780 and high of 0.7436. As a side note, the price needs to go through the 20 and 40 simple moving averages that stand near the current market price of 0.7350.

In the event of an upside reversal, the upper boundary of the Bollinger Band at 0.7400 could act as a resistance barrier. A jump above the aforementioned obstacle could shift the short-term outlook to bullish as it could take the pair towards the 0.7436 barrier.

Sunset Market Commentary

Markets:

Yesterday evening's Fed meeting had no lasting impact on today's trading session. The Fed kept its policy rates unchanged while upgrading its economic and inflation assessment and strengthening the tightening bias in its forward guidance. Core bond sentiment remained bearish with modest losses during European dealings. The Bund and US Note future bottomed when stock market sentiment soured. The German Dax lost short-term support and currently records a 1.5% loss. Second tier eco data and dovish comments by Praet were ignored. The German yield curve steepens on a daily basis with yield changes varying between -1.3 bps (2-yr) and +1.2 bps (30-yr). US yield increases range between +0.4 bps (2-yr) and +1.9 bps (10-yr). 10-yr yield spread changes versus Germany are narrowly mixed with the periphery outperforming (-2 bps to -4 bps).

The dollar also couldn't find a clear trend despite yesterday's 'positive' guidance from the Fed's policy statement. EUR/USD again revisited a short-term intermediate support just below 1.24, but the test was rejected, triggering a new intraday euro upleg. The further rise in core yields early this morning initially supported USD/JPY. However, this move slowed as bond yields eased later due to profit taking on European equity markets. Eco data were second tier. US jobless claims remain low, indicating an ongoing positive momentum on the US labour market. However, the report was ignored. Investors are looking forward to tomorrow's US payrolls, with the focus on wage growth. USD/JPY is changing hands in the mid 109 area, off the intraday top around 109.75. EUR/USD (1.2440) is holding relatively strong, but the short-term consolidation range (1.2337/1.2598 ) remains in place.

Sterling held a positive momentum this morning despite several negative headlines on the EU-UK Brexit talks and on political tensions within the UK government because of PM's May's Brexit approach. EUR/GBP drifted further south in the 0.87 big figure. Mid-morning, the UK manufacturing PMI declined more than expected from 56.2 to 55.3 (56.5 was expected). This is still a decent level, but the decline indicates that the UK production sector will contribute less to overall growth than what was hoped for. Especially domestic demand disappointed. The report also suggests that there is no need for the BoE to rush to further rate hikes short term, downplaying recent comments from BoE's Carney earlier this week. EUR/GBP rebounded and currently trades in the 0.8760 area. Overall euro strength supported the rebound. Cable (1.4200 area) trades off the intraday highs, but losses are limited as the dollar continues trading soft across the board.

News Headlines:

The Czech National Bank as expected increased its policy rate by 25 bps from 0.50% to 0.75%. The central bank raised its 2018 GDP growth forecast from 3.4% to 3.6% and expects 3.2% growth in 2019. The Q1 2019 inflation forecast was lowered from 2% to 1.9%. The CNB forecasts an average koruna rate of EUR/CZK 24.9 in 2018 and EUR/CZK 24.5 in 2019. The forecasts imply one more rate hike in 2018. Our in-house expectations is two additional hikes this year.

The final January EMU manufacturing PMI was confirmed at 59.6. The UK manufacturing PMI disappointed and slipped to 55.3 from 56.2 (vs 56.5 expected). New orders fell to 56 from 56.9, but that remains a decent level. The US manufacturing ISM stabilized near December levels (59.1 from 59.3) while consensus expected a bigger setback. The prices paid component surged to an incredible 72.7. New orders declined to 65.4, which remains very high.

Inflation in the euro zone is still weak so the ECB needs to keep in place its stimulus measures, ECB Chief Economist Praet said, repeating the bank's long-standing guidance