Sample Category Title

Dollar Rallies Versus Yen on Inflation Prospects; European Stocks Rebound

Here are the latest developments in global markets:

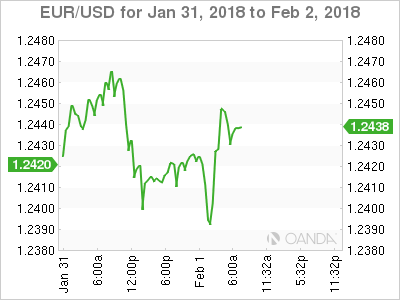

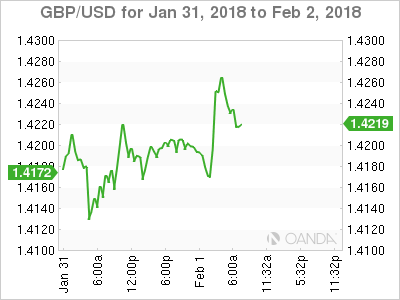

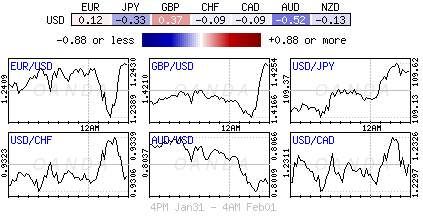

FOREX: Dollar/yen stretched towards a one-week high of 109.74 (+0.51%) during early European trading after the FOMC statement highlighted yesterday that the US inflation is expected to "move up this year". However, the dollar index inched down to 89.00, remaining near 3-year lows, on the face of a strengthening euro and pound. Euro/dollar crawled up to 1.2450 (+0.14%) amid prospects that the ECB will reduce monetary stimulus this year and pound/dollar was on track to post gains for the third consecutive day, surging to 1.4273 (+0.27%). On Tuesday, the BOE Governor, Mark Carney, acknowledged the strength of the economy and said that the focus was turning to inflation. Aussie/dollar dipped into further losses towards a one-week trough of 0.7992, harmed by worse-than-expected readings on Australian building approvals.

STOCKS: Encouraging earnings results helped European stocks to erase yesterday's losses on Thursday. The benchmark European STOXX 600 was up by 0.50% at 1000 GMT, underpinned by gains in the tech, utility and financial sectors, while the blue-chip Euro STOXX 50 increased by 0.40%, with energy shares leading the index's gains. The Italian FTSE MIB jumped by 1.0%, the French CAC 40 rose by 0.46% and the German DAX 30 moved up by 0.38%. The British FTSE 100 edged up by 0.06%.

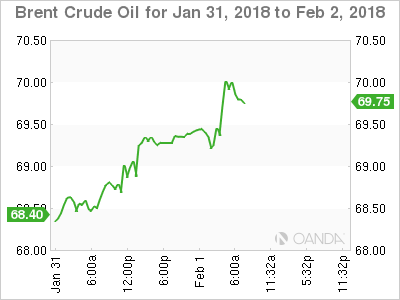

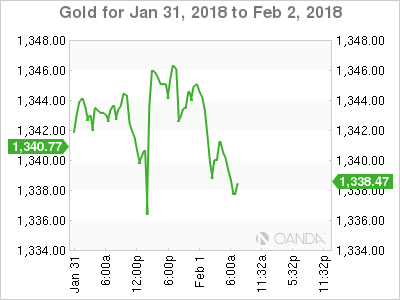

COMMODITIES: Oil prices rallied after a survey noted that OPEC's commitment to curb supply remains in place, despite increases in US production. WTI crude surged to an intraday high of $65.42/barrel (+0.96%) and Brent hit a top at $69.67/barrel (+ 1.06%). Gold slipped to a low of $1338/ounce (-0.50%).

Day ahead: US initial Jobless claims & ISM Manufacturing PMI eyed

For the remainder of the day, the calendar will feature US data, with attention turning mainly to initial jobless claims (1330 GMT) and ISM manufacturing PMI readings (1500 GMT).

In the week ending January 26, analysts expect that 238,000 people applied for unemployment benefits for the first time compared to 233,000 seen in the preceding week, reflecting a strong labor market as long as the measure continues to remain below the threshold of 300,000 that is linked to a strong jobs market.

The Institute for Supply Management (ISM) will release stats on manufacturing activity for the month of January. The index is expected to inch down by 0.9 points to 58.8, though, any print above 50 would indicate that the manufacturing industry is generally expanding.

Other releases that might draw some attention out of the US are Q4 2017 preliminary data on labor costs and productivity (1330 GMT), Markit's final reading on January manufacturing PMI (1445 GMT), December construction spending figures (1500 GMT) and January's total vehicle sales (2030 GMT).

On the equities front, corporate giants Alibaba, Amazon, Apple and Google parent Alphabet will be among companies releasing quarterly earnings reports on Thursday.

Canadian Dollar Unchanged, Investors Await NFP, Wage Growth Reports

The Canadian dollar has recorded small gains in the Thursday session. Currently, the pair is trading at 1.2318, up 0.02% on the day. On the release front, there are no major Canadian events. Over in the US, there are two key events. Unemployment claims are expected to rise to 237 thousand, and the markets are forecasting that ISM Manufacturing PMI will slow to 58.7 points. On Friday, the focus will be on US job reports, with the release of wage growth, nonfarm payrolls and the unemployment rate.

Will NAFTA survive past March? Negotiators are working against a self-imposed deadline to wrap up talks by March, with limited progress. The latest round of negotiations over NAFTA ended in Montreal last week, and there were no breakthroughs. Still, the sides continue to talk, and a Merrill Lynch has lowered the odds of the United States leaving the pact to 25 percent. The US has demanded far-reaching concessions from Canada and Mexico, such as shifting more auto production to the US. Canada and Mexico are strongly opposed to the US demands, but both economies would take a sharp hit if NAFTA is terminated. At the same time, many US businesses don't want to blow up NAFTA and are pressuring President Trump to remain in the trade pact. The next round of negotiations is scheduled for late February in Mexico.

The Federal Reserve held the course on interest rate policy on Wednesday, as expected. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What was more noteworthy was that the Fed predicted that inflation would rise to the Fed's 2 percent target this year. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to "remain somewhat below 2 percent." Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three, or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

Dollar Depressed Despite Hawkish Fed, Gold Dips

It's remarkable how the Dollar remains depressed and unloved, despite the Federal Reserve expressing optimism over increased inflationary pressures as the year moves on.

Although the U.S. Federal Reserve left rates unchanged as expected in January, the relatively upbeat appraisal of the economy and rising inflation expectations offered a hawkish touch. The fact that the Dollar remains pressured following the hawkish Fed meeting, continues to suggest that other key fundamental drivers are impacting the currency. As Janet Yellen prepares to pass the baton of leadership to Jerome Powell, there are widespread discussions over how this will impact the Dollar, current monetary policy and the U.S. economy.

While it may be too early to predict how the FOMC under Powell's leadership could impact the U.S. economy it obviously breeds uncertainty, resulting in a weaker Dollar. It must be kept in mind that there are many new Fed governors on board as well, and the new Fed Chair is a lawyer by practice, not an economist. Although the central bank may avoid obstacles further down the road by following the status quo, there could be some issues if the U.S. economy experiences unexpected shocks.

Other themes that continue to punish the Dollar revolve around political uncertainty in Washington and concerns over the United States' stance on global trade. With the prospects of other major central banks gradually tightening monetary policy also adding to the mix and denting buying sentiment, further losses could be on the cards for the U.S. Dollar.

Taking a look at the technical picture, the Dollar Index remains heavily bearish on the daily charts. There have been consistently lower lows and lower highs, while the MACD trades to the downside. Sustained weakness below the 89.00 level may encourage a decline towards 88.50 and 88.00, respectively.

Currency spotlight - GBPUSD

Sterling edged lower during Thursday's trading session, after weaker-than-expected data from Britain's manufacturing sector weighed on sentiment. The U.K's manufacturing sector activity fell in January to 55.3, from 56.2 in December. This disappointing report is likely to instill bears with fresh inspiration to attack the British Pound.

Focusing on the technical outlook, the GBPUSD continues to find support in the form of Dollar weakness on the daily charts. A decisive breakout and daily close above 1.4230 could encourage an incline higher towards 1.4300. Alternatively, a failure of prices to keep above the 1.4230 may inspire a move back towards 1.4110 and 1.4000.

Commodity spotlight - Gold

Gold found itself under noticeable selling pressure on Thursday, with prices dipping below $1340 after the Federal Reserve hinted of more rate hikes taking place this year.

While further losses could be witnessed in the short term, a vulnerable U.S. Dollar is likely to cushion the yellow metal's downside. Gold remains bullish on the daily charts and is poised to venture higher, if the NFP report, that is due for release on Friday, fails to meet market expectations. From a technical perspective, Gold remains in the process of creating a new higher low. Sustained weakness below $1335 may invite a decline back towards $1324.15. Alternatively, an intraday breakout above $1340 may open a path towards $1360.

DAX Trading Sideways as German, Eurozone Manufacturing Reports Within Expectations

The DAX is showing little movement in the Thursday session. Currently, the index is trading at 13,194.00, up 0.03% on the day. On the release front, market estimates for German and Eurozone Final Manufacturing PMIs were on the money. The German release came in at 61.1, just shy of the estimate of 61.2 points. The eurozone indicator dipped to 59.6, matching the estimate. On Friday, the eurozone releases PPI and the US will publish nonfarm payrolls.

As expected, the Federal Reserve held the course on interest rate policy at its January meeting. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What was more noteworthy was that the Fed predicted that inflation would rise to the Fed's 2 percent target this year. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to "remain somewhat below 2 percent." Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

With eurozone inflation well under the ECB target of 2 percent, the ECB has some breathing room regarding its stimulus program (QE), which is scheduled to terminate in September. A stronger eurozone economy has raised speculation that the ECB could wind up QE and shift to normative policy, and perhaps even raise interest rates. However, ECB members have been cautious, trying to keep in check any market enthusiasm about a major change in policy. Last week, ECB President Mario Draghi went as far as saying that QE could be extended or increased if necessary.

USDJPY Intraday Bullish Above 109.44 Level

The U.S dollar has recovered upside momentum against the Japanese yen, after the Federal Reserve struck a bullish tone towards U.S inflation at Wednesday's policy meeting. The USDJPY pair has now broken above key daily resistance, with price-action currently trading at the highs of the week, around the 109.70 zone. Going forward, the upcoming release of the ISM Manufacturing data and tomorrow's January Non-Farm Payrolls job report, should dictate the next directional move in the pair.

Bullish momentum is gathering in the USDJPY while price trades above the 109.44 level, further upside towards 110.18 and 110.58 seems possible.

Should sellers push the USDJPY pair below the 109.44 level, we may see a correction back towards the 108.98 and 108.58 levels.

GBPUSD Further Bullish Above 1.4234 Level

The British pound remains increasingly volatile against the U.S dollar, with price action moving in a one-hundred pip range during the European session. On the first trading day of February, the pair saw strong monthly in-flows moving on the UK market open, moving price-action to an intraday high of 1.4274. The GBPUSD pair has now corrected back towards the pivotal 1.4230 region, following a weaker than expected January Manufacturing PMI from the United Kingdom economy.

The GBPUSD pair retains a strong bullish bias while trading above the 1.4232 level, further upside towards 1.4280 and 1.4350 cannot be ruled out.

Should the GBPUSD pair start to trade below the 1.4232 level, we may see a swift price correction back towards the 1.4200 handle.

Dollar Support Lukewarm Despite Fed’s ‘Hawkish-Hold’

Thursday February 1: Five things the markets are talking about

Global equities have kicked off the new month mostly in the 'black' as capital market participants have decided that the outlook for growth and corporate earnings remains strong enough to suppress concerns about the back up in sovereign yields.

U.S Treasuries have resumed their slide, while the 'mighty' U.S dollar trades steady against G10 currency pairs.

Yesterday, as expected, the Fed held the overnight interest rate target range steady between +1.25 – 1.50% in a unanimous vote (9-0). In their accompanying statement, policy makers noted that the U.S labor market had continued to strengthen and they dropped the language on expecting inflation to remain below +2% in near-term. In fact, the statement made few changes from December and affirmed a solid outlook for U.S. growth. It offered little sign that officials' thinking about the economy has changed materially.

Note: Next up is tomorrow's U.S non-farm payroll report (NFP), where U.S employers are supposed to have added more jobs in January than a month earlier (+180k vs. +148k).

1. Stocks get the green light

In Japan, the Nikkei share average rallied overnight, rebounding from a six-day losing streak and pushed most sectors into positive territory, as a weaker yen and upbeat corporate earnings drove the benchmark index higher. The Nikkei rose +1.7%, while the broader Topix jumped +1.8%.

Down-under, Australian shares rose overnight, supported by strong gains in mining stocks and financials. The S&P/ASX 200 index climbed +0.9%. In S. Korea, the Kospi index dropped -0.05%.

In Hong Kong, shares weaken as energy and finance stocks fall. At close of trade, the Hang Seng index was down -0.75%, while the Hang Seng China Enterprises index fell -0.94%.

In China, equities were also under pressure, as investors dumped firms, which are expected to report weaker 2017 earnings, and took profits ahead of the upcoming long Lunar New Year holidays. At the close, the Shanghai Composite index was down -0.99% losing ground for the fourth consecutive session. The blue-chip CSI300 index was down -0.71%.

Note: Data overnight showed that growth in China's manufacturing sector remained solid last month, beating market expectations, as new business led factories to raise output at the start of 2018.

In Europe, regional indices trade higher across the board and in tandem with U.S futures, as corporate earnings support the move higher.

U.S stocks are set to open in the 'black' (+0.2%).

Indices: Stoxx600 +0.4% at 397.1, FTSE +0.1% at 7540, DAX +0.4% at 13237, CAC-40 +0.5% at 5507, IBEX-35 +0.5% at 10507, FTSE MIB +0.9% at 23717, SMI +0.4% at 9376, S&P 500 Futures +0.2%

2. Oil rises as OPEC compliance trump's U.S output, gold lower

Oil is better bid after a survey showed OPEC's commitment to its supply cuts remains in place, even as U.S production topped +10m bpd for the first time in 48-years.

Brent crude futures are up +49c at +$69.38 a barrel, while WTI crude for March delivery rose +45c to +$65.18 a barrel.

Note: Brent crude rallied +3.3% in January – it was the strongest start to a New Year for five-years.

The week's EIA report showed the biggest increase in crude oil stocks in 11-months, a rise of +6.8m barrels.

For crude bears, they now have to gage how much U.S production will increase as prices rise.

Ahead of the U.S open, gold prices are under pressure after the Fed left interest rates unchanged, but hinted at hikes later this year. The market would also prefer to take his cues from tomorrow's U.S payrolls report. Spot gold is down -0.4% at +$1,339.71 per ounce. Yesterday, it touched +$1,332.30 an ounce, its lowest print since Jan. 23.

3. Sovereign yields continue to back up

Yesterday's FOMC meeting was the last attended by Chair Janet Yellen before she turns over the reins to her successor, Fed Governor Jerome Powell.

Governor Powell will begin his term as chairman on Saturday, and is scheduled to be sworn-in as chairman of the Fed board of governors on Monday.

With the Fed's three hike 'dot-plot,' the odds for a rate increase at the March 20-21 meeting remains at around +78%.

However, yesterday's FOMC statement hinted that officials might favour more than three-rate increases this year because it offered slightly more conviction that inflation would move higher in 2018.

The yield on U.S 10-year Treasuries has backed up +3 bps to +2.73%, the highest in almost four-years. In Germany, the 10-year Bund yield has climbed +2 bps to +0.72%, the highest in more than two-years, while the U.K's 10-year Gilt yield has advanced to +1.525%, its highest yield in 21-months.

4. Dollar support remains lukewarm

The USD has ebbed and flowed in the overnight session on market belief that yesterday's Fed 'hawkish hold' has very much been priced-in.

EUR/USD (€1.2433) is back above the psychological €1.24 handle as Euro manufacturing PMI's this morning support the region's recovery story.

Note: Beats: France, Swiss, Norway, Czech; misses: Germany, U.K, Spain, Sweden, Poland and in-line: Euro-Zone and Russia.

The single unit is also getting some passive support that eurozone inflation data may have bottomed.

GBP is higher by +0.5% at £1.4245, atop of its strongest level in 19-months, supported by the markets optimism on Brexit talks. Some fixed income dealers are bringing forward their forecast for the next Bank of England (BoE) rate hike to May. It's conditional on a Brexit transitional agreement next month.

USD/JPY (¥109.73) trades at its overnight highs, underpinned by the Fed's 'hawkish-hold' statement. The pair seems to be locked in a ¥107-110 range.

And following a horrid January for crypto currencies, Bitcoin (BTC) has again edged lower, trading below the psychological $10,000, down-6% at $9,605.

5. U.K manufacturing growth slows

Data this morning revealed an unexpected drop in January U.K manufacturing PMI to a seven-month low of 55.3, down from 56.2 in December and below the market consensus for 56.5.

Digging deeper, Markit (which compiles the survey) said that the reading remained “well above its long-run average of 51.7” and still showed a strengthening in new export order inflows.

Today's report also revealed a sharp rise in inflationary pressures, with purchase prices rising at the fastest rate in 11-months.

Dollar Struggles Despite Fed Optimism

- Eurozone Manufacturers Still Extremely Bullish Despite Stronger Euro;

- UK PMI Slips But Sterling Continues Push Higher;

- US Data Eyed as Optimistic Fed Fails to Lift the Greenback;

- Bitcoin Below $10,000 and Looking Vulnerable.

Eurozone Manufacturers Still Extremely Bullish Despite Stronger Euro

It's been a positive start to trading on the first day of the month, with markets in Europe trading well in the green and US futures ticking a little higher as well.

It's been a busy morning of economic releases and broadly speaking, the data is very positive for the eurozone economy. The region carried some strong momentum into the new year and the latest manufacturing PMIs suggest confidence in the recovery is showing no signs of faltering. The survey for the region as a whole remained at 59.6, slightly shy of last month's high of 60.1 while still signalling a strong growth outlook for the sector.

The weak euro has played a big role in the strong performance of the sector which has led many to speculate about whether its resurgence over the last year will hinder output going forward. The survey's we're seeing suggest manufacturers are not particularly concerned at this stage and are continuing to see strong demand, despite the 20% increase in the value of the euro over the dollar over the last year. The rise against the pound has been far more modest though.

UK PMI Slips But Sterling Continues Push Higher

The UK data has been less encouraging as of late and the manufacturing PMI for January was no different, slipping to 55.3 from 56.2 in December. The sector has actually benefited in the post-Brexit world, with the sterling depreciation driving more demand for UK manufactured goods. Unfortunately, it still remains a very small part of the UK economy and the boost seems to be wearing off.

That said, a weaker PMI number this morning did little to shake the pound which is heading back to last week's highs against the dollar. Cable now finds itself back it pre-Brexit territory, although much of this can be attributed to the greenbacks decline over the last year. The pair found some resistance around 1.4350 but there's clearly still some bullish appetite there. A break through here could see the pair testing 1.45, which isn't a million miles from the 2016 highs.

US Data Eyed as Optimistic Fed Fails to Lift the Greenback

The dollar is continuing to have a rough time, even a more optimistic sounding Fed did little to lift the greenback which continues to languish around three year lows. Yields on near-term US debt have risen in the aftermath of the Fed statement, with a rate hike in March now almost entirely priced in and a further two this year around 65% priced in. This would typically be positive for the dollar any gains were short-lived.

There's plenty more data still to come today, with two manufacturing PMIs from the US as well as unit labour costs, non-farm productivity and jobless claims. Earnings season remains a key focus for investors and some big names are due to report after the close on Thursday, including Amazon, Apple and Alphabet.

Bitcoin Below $10,000 and Looking Vulnerable

Bitcoin is coming under pressure once again today and is trading back below $10,000, a level that has proven difficult to hold below. It's currently trading down more than 5% on the day though and should we close below here, it could be yet another bearish signal for the cryptocurrency which is already more than 50% below its peak.

After Fed, Dollar Seeks Additional Reprieve From NFP Report, Higher Wage Growth Eyed

Even as US data continues to point to an upside risk to growth this year, the dollar has had a terrible start to 2018, falling by around 3.5% against a basket of currencies. A convincing sign that labour shortages are finally starting to push up wages could be the catalyst investors need to price in the possibility of three or more rate hikes by the Fed in 2018. Friday’s nonfarms payrolls report (due at 13:30 GMT) might go some way in achieving this.

The US economy is expected to add 180k jobs in January, after a modest slowdown in December to 148k jobs. The average monthly pace of job creation was down in 2017 compared to 2016 and has been steadily slowing since 2015 as the labour market approaches full employment. However, with the unemployment rate at a 17-year low of 4.1%, investors are more likely to start worrying about the risk of an overheating economy, if the economy continues to generate more than 100k jobs a month, than to cheer the upbeat numbers.

So far though, there has been little indication of this as wages have remained subdued. Average hourly earnings did tick higher in December to 2.5% year-on-year and are expected to edge further up in January to 2.6%. A bigger-than-expected increase would boost the outlook for wage growth. But without a sustained rise towards 3% and above, the Fed is not seen to be adjusting its rate hike path, at least not without a rise in underlying inflation from other sources

With the dollar now finding itself back below the key 110 level versus the yen, a strong jobs report on Friday may not be enough to lift the pair to a more comfortable range above the 110 handle. Investors have become so focused on what other central banks such as the European Central Bank and the Bank of Japan may do next, they may have taken their eyes off the ball as to what the Fed will do in 2018.

However, a positive report should nevertheless help the greenback move back towards recent resistance just below 109.80 yen. A successful break of this level could set the path towards the past congested areas around 110.15 and 110.75, before challenging the psychological 111 level. In the event of a disappointing set of numbers, a re-test of last week’s 4½-month low of 108.27 is possible. A breach below that level would open the way towards last September’s 10-month low of 107.31.

Euro Edges Higher, German And Eurozone Manufacturing PMIs Meet Estimates

The euro continues to have a quiet week. Currently, the pair is trading at 1.2443, up 0.15% on the day. On the release front, market estimates for German and Eurozone Final Manufacturing PMIs were on the money. The German release came in at 61.1, just shy of the estimate of 61.2 points. The eurozone indicator dipped to 59.6, matching the estimate. In the US, there are two key events. Unemployment claims are expected to rise to 237 thousand, and the markets are expecting ISM Manufacturing PMI to slow to 58.7 points. On Friday, the eurozone releases PPI. In the US, the focus will be on employment reports, with the release of wage growth, nonfarm payrolls and the unemployment rate.

The Federal Reserve held the course on interest rate policy on Wednesday, as expected. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What was more noteworthy was that the Fed predicted that inflation would rise to the Fed’s 2 percent target this year. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to “remain somewhat below 2 percent.” Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three, or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

Inflation levels in the eurozone pointed upwards in 2017, but softened in January. Eurozone CPI Flash Estimate came in at 1.3%, as inflation remains well below the ECB target of around 2 percent. Lower inflation gives the ECB some breathing room regarding its stimulus program (QE), which is scheduled to terminate in September. A stronger eurozone economy has raised speculation that the ECB could wind up QE and shift to normative policy, and perhaps even raise interest rates. However, ECB policymakers have been cautious, trying to keep in check any market enthusiasm about a major change in policy. Last week, ECB President Mario Draghi went as far as saying that QE could be extended or increased if necessary.