Sample Category Title

Spotlight On US Data Continues

Attention will remain on US economic data in the latter half of the week, with Thursday’s reports focused on jobs and manufacturing.

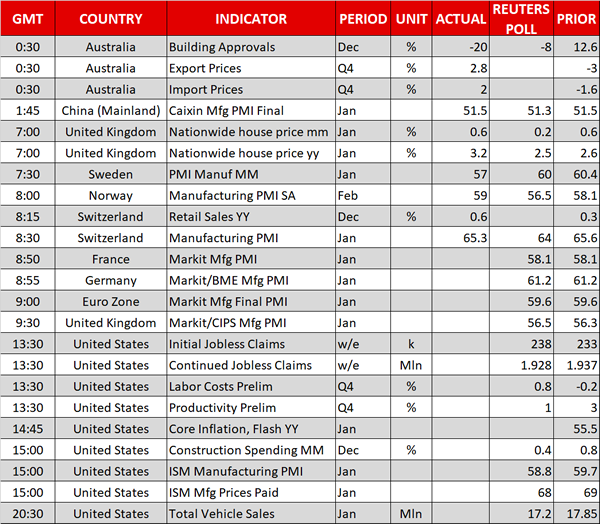

Investors can expect a somewhat active European session on Thursday, with IHS Markit reporting on manufacturing PMI for the UK, Germany, France, Italy, Greece and the broader euro area. The Eurozone manufacturing PMI is forecast to hold steady at 59.6 on a scale of 1-100 where 50 separates expansion from contraction.

The start of US trading will feature the weekly initial jobless claims report courtesy of the Department of Labor. The number of Americans filing for first-time unemployment benefits is forecast to rise by 5,000 to a seasonally adjusted 238,000. On Wednesday, payrolls processor ADP said US private sector employers added 234,000 workers last month, a figure that was well above forecasts.

Later in the morning, IHS Markit and the Institute for Supply Management (ISM) will each report on US manufacturing PMI. The ISM report, which is more closely followed by the financial market, is forecast to show a half point drop to 58.8.

Finally, the Department of Commerce will report on construction spending at 15:00 GMT. The December report is forecast to show expansion of 0.4%.

Earlier in the day, Caixin China reported a slightly better than expected reading of manufacturing PMI for the world’s second largest economy. The manufacturing purchasing managers’ index came in at 51.5 in January, unchanged from the previous month.

The report indicated: “The manufacturing industry had a good start to 2018. Going forward, we should keep a close eye on the stability of the demand side.”

EUR/USD

Europe’s common currency has been rangebound all week long, as the prolonged dollar slide finally found a short-term bottom. The EUR/USD exchange rate was last seen trading at 1.2419 for a gain of 0.1%. The pair peaked at 1.2475 on Wednesday before reversing back down to the low 1.2400 range. EUR/USD faces immediate resistance at 1.2470, followed by 1.2500. On the downside, immediate support is located at 1.2390, followed by 1.2355.

GBP/USD

Pound sterling is holding steady against the dollar, with cable trading around 1.4200. The pair was kept in check by an assertive US Federal Reserve, which indicated on Wednesday that interest rates may soon rise in response to faster inflation. The GBP/USD exchange rate faces near term support at 1.4120, the intraday low, with resistance up ahead at 1.4232.

USD/CAD

The USD/CAD continues to hold steady above 1.2300 following a series of protracted drops in previous weeks. The pair remains highly sensitive to economic data and monetary policy, with the Canadian dollar gaining more competitive advantage thanks to a robust domestic economy. The US nonfarm payrolls report on Friday could be the pair’s next major trading catalyst.

Optimistic Fed Message Does Little For The Dollar, Major Economies’ Manufacturing PMI Data Due

Here are the latest developments in global markets:

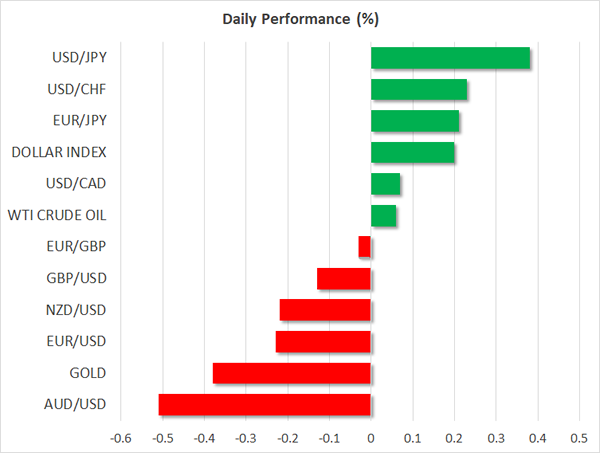

FOREX: The dollar index traded 0.2% higher on Thursday, recovering some of its recent losses, buoyed by the Fed's slightly more hawkish tone on the US economic outlook upon completion of its two-day meeting on monetary policy.

STOCKS: Japanese markets skyrocketed, with the Nikkei 225 moving 1.7% higher and the Topix surging by 1.8%, both indices regaining some of the ground they lost in recent days. In Hong Kong, the Hang Seng was down by 0.4%, while in Europe, futures tracking the Euro STOXX 50 are 0.6% higher. Turning to the US, the S&P 500, Dow Jones and Nasdaq Composite all finished higher yesterday, albeit not by much. The Dow gained the most out of the three, advancing by less than 0.3%. The relatively muted performance of these indices is being attributed to the surge in US Treasury yields, with the 10-year benchmark briefly topping 2.75% overnight, its highest level since April 2014.

COMMODITIES: Gold was nearly 0.4% lower, last trading near $1340 per ounce, as the modest rebound in the greenback weighed on the dollar-denominated precious metal. Oil prices were little changed, with both WTI and Brent crude rising by less than 0.1%. Interestingly enough, both oil benchmarks finished the day higher yesterday, even despite the weekly EIA inventory data showing a much higher build in stockpiles than what was anticipated

Major movers: FOMC upgrades inflation outlook, paves the way for March hike

The Fed kept its policy unchanged yesterday via a unanimous vote, as was widely anticipated. The statement accompanying the decision had a more optimistic tone compared to previously, upgrading the Committee's assessment of inflation. Inflation is now anticipated “to move up this year” and to stabilize around 2%, from previously being expected to remain somewhat below 2%. Policymakers also appeared upbeat on the broader economy, noting that gains in employment, household spending, and business investment have been solid.

The dollar spiked up on the news, but quickly gave back all of its winnings to trade virtually unchanged in the following hours, before assuming a direction during the Asian trading session Thursday and moving a little higher. The relatively indecisive price action in the USD, at least initially, may reflect the fact that many investors already anticipated a slightly more hawkish bias by the Committee, given the economy's solid performance. Markets have fully priced in a March rate increase, while another two quarter-point hikes by the end of the year are almost fully factored in, according to the Fed funds futures.

The greenback gained the most against the aussie, which suffered a little overnight after Australia's building approvals for December came in significantly lower than projected.

Day ahead: Major economies on the receiving end of PMI data; US jobless claims also on the horizon

The eurozone will see the final release of Markit's manufacturing PMI for the month of January at 0900 GMT. The reading is expected to be confirmed at 59.6, reflecting a decrease from December's 60.6, though still pointing to robust sectoral growth by comfortably exceeding the 50 mark that separates expansion from contraction. Germany and France, the eurozone's two largest economies, will see the release of their manufacturing PMI figures for the first month of the year a few minutes earlier (at 0855 GMT and 0850 GMT respectively).

The UK will also be on the receiving end of manufacturing PMI data. The January Markit/CIPS manufacturing PMI will be made public at 0930 GMT. The measure is anticipated to tick slightly higher relative to December, remaining well above 50. Unlike the eurozone that sees the release of a flash estimate as well, the UK only receives a single release; this may render sterling more “susceptible” to greater market movement upon release of the data and in case of a surprise.

Over in the US, of most interest are likely to be data on weekly initial and continued jobless claims due at 1330 GMT, as well as the ISM's January manufacturing PMI scheduled for release at 1500 GMT. First-time jobless claims applicants are expected to have increased during the week ending January 27, though not by much and to still remain well below the 300k threshold that's associated with a healthy labor market. The ISM's survey on manufacturing activity is projected to reflect a reduction compared to December, though at 58.8 – should expectations materialize – it would still constitute a robust number.

Other releases that might draw some attention out of the US are Q4 2017 preliminary data on labor costs and productivity (1330 GMT), Markit's final reading on January manufacturing PMI (1445 GMT), December construction spending figures (1500 GMT) and January's total vehicle sales (2030 GMT).

ECB executive board member and chief economist Peter Praet will be giving a speech at the luncheon conference of Cercle de Lorraine at 1115 GMT.

On the equities front, corporate giants Alibaba, Amazon, Apple and Google parent Alphabet will be among companies releasing quarterly earnings reports on Thursday.

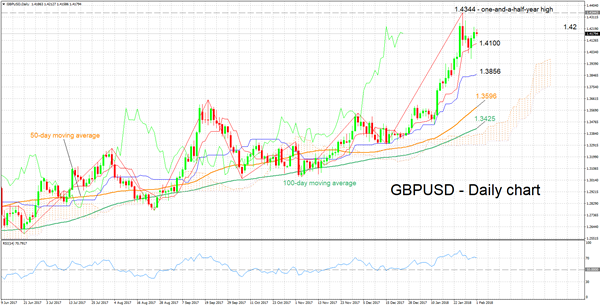

Technical Analysis: GBPUSD bullish bias could be under threat as RSI halts advance

GBPUSD is trading roughly 150 pips below the one-and-a-half-year high of 1.4344 hit on January 25. The Tenkan-sen line remains above the Kijun-sen line and the RSI indicator is in bullish territory above 50. The aforementioned are supporting the view for a bullish short-term bias. Notice though that the RSI has halted its advance after rising well above the 70 overbought level last week. This could be an indication of changing dynamics in the short-term.

A stronger manufacturing PMI out of the UK during early European trading hours – or weaker releases out of the US later on Thursday – could see the pair gaining ground. The area around the 1.42 handle – a level of potential psychological significance – might be acting as immediate resistance at the moment. An upside breakup would turn the focus to the range around last week's one-and-a-half-year high of 1.4344 as an additional barrier to stronger bullish movement.

Weaker UK data, or equivalently more robust figures out of the US, on the other hand, might see the pair heading lower. In this case, the area around the current level of the Tenkan-sen at 1.41, which coincides with a point of potential psychological importance, might offer support

Yellen Makes A Hawkish Exit | Manufacturing PMI Data Under Lights

US March rate hike on table

ADP sets a strong tone for US NFP

Euro could cross 1.25

They are calling it hawkish exit for Janet Yellen (current Fed president) but we are saying it job well done. Janet Yellen, the Federal Reserve chairwomen, made pretty much clear in her last meeting that the economy warrants more rate hikes. Therefore, the first decision by the upcoming Fed chairperson would be increase the interest rate. Trump administration's tax incentive plan has strengthened the inflation equation and this allows the Fed to move the interest rate to a more normal level.

The ADP number released yesterday has set a strong tone for the upcoming US NFP. The private sector is thriving once again by employing higher number of job candidates and this sets the tone that the US NFP should show a positive outcome. Investors would be looking closely towards the average hourly earning number; this will set the tone for traders. The FOMC upgraded the inflation forecast last night and if the US NFP data support the Fed's view, we could see the dollar index strengthening further.

Investors around the globe have taken the Fed's message as a sign of confidence. The massive sell-off in the equity markets was the opportunity if the current trend continues from here. The S&P 500 finished the month on a higher note, marking the 15th month in a row.

The Euro hass lost some steam today mainly because of the stronger dollar, however, we do think that it is likely that it will touch the level of 1.25 soon. Manufacturing PMI data from the four biggest economies of the Eurozone would confirm the economic health of these countries. Spain, Italy, France and Germany are expected to show a strong picture of their manufacturing sectors and the forecasts are 55.7, 57.7, 58.1 and 61.2 respectively.

The European banks could come under pressure when the EU releases its stress test results. To date, these would be the toughest test which European banks will face as this includes the Brexit scenario. Some of the strong assumptions include the eurozone's GDP dropping 8.3% short of the ECB's recent forecast, housing sector experiencing massive drop of 27.7% and unemployment surging by 3.3%.

USDJPY Posts Some Gains, Re-Enters Into Symmetrical Triangle

USDJPY surged above the 109.50 price level during today’s European session and is trying to enter again into the symmetrical triangle that has been holding since June 2015 in the medium-term timeframe. The short-term technicals are bullish and point to more strength in the market.

From the technical point of view, in the daily timeframe, the RSI indicator rebounded from the oversold area and is currently sloping to the upside, indicating further gains. The stochastic oscillator is moving higher approaching the positive territory.

In case of further bullish movement, the next level to have in mind is the 110.10 resistance level. Rising above this area could shift the focus to the upside towards the 111.50 barrier. As a side note, the price needs to surpass the mid-level of the Bollinger band, which stands near the 110.50 price level, to hit the aforementioned barrier. Breaking 111.50 could see a re-test of the descending trend line.

However, the expectation is a touch of the 110.10 resistance level and then create a bearish movement. Downside moves below 108.20 and the lower band of the Bollinger band could help the price to create a resumption of the downtrend and put in place a lower low at 107.20. From there, USDJPY would be on the path to slip even lower at 105.50.

Overall, the bigger picture remains bearish and the selling pressure is still very strong.

Technical Outlook: EURUSD – No Stronger Impact From Hawkish Fed For Now, Rising 10SMA Continues To Maintain Bullish Bias

The Euro stands at the back foot and probes below 1.224 handle after overnight's action was capped at 1.2428.

The single currency eased on Wednesday following repeated upside rejection (1.2375) and sentiment was soured by more hawkish Fed.

The US central bank left interest rates unchanged at its policy meeting which ended on Wednesday but highlighted the confidence in the economic growth and inflation, rising hopes for more rate hikes this year.

However, fresh boost to the dollar did not show stronger impact on the single currency as the pair holds above ascending 10SMA which currently lies at 1.2361 and marks first pivot.

Near-term price action is holding in narrowing range in triangular consolidation after initial attempt through 1.25 barrier failed to sustain gains.

Increased downside risk could be expected on break below 10SMA which would risk test of next pivot at 1.2300 (Fibo 38.2% of 1.1915/1.2537 upleg) and generate stronger reversal signal on break lower.

Daily RSI is holding in sideways mode at the border of overbought area while momentum is falling and could support negative scenario.

On the other side, daily MA's are in full bullish setup and bias is expected to remain with bulls while rising 10SMA contains dips.

The Fed's decision needs further signals for confirmation and traders eye a batch of data from the US today and key event – US Non-Farm Payrolls on Friday, to get more clues whether the Fed's signals would lead towards expected scenario or the central bank is just giving a breather to dollar's broader bears.

Res: 1.2474, 1.2493, 1.2537, 1.2597

Sup: 1.2385, 1.2361, 1.2335, 1.2300

Forex Analysis: PMI Readings From Around The World Out Today

The markets went to test nearby support and resistance after the Fed's Monetary Policy Statement was released yesterday. The Interest Rate was left unchanged and only small parts of the text were altered. The statement added that the expectations would 'warrant FURTHER gradual increases in the federal funds rate' (adding the word 'further'). They also dropped a line saying 'inflation will remain below 2% in near term'. It is expected that there will be three tightening moves in 2018, with the March meeting a ‘live' meeting in terms of a hike. EURUSD tested resistance at 1.24378 and support at 1.23866 and has stayed in this range since. GBPUSD tested support at 1.41508 and resistance around 1.42107 and has largely maintained that range since. Gold found support at 1332.50 and tested a high of 1344.40, later getting to a high of 1347.50.

US EIA Crude Oil Stocks Change (Jan 26) showed a surprise build of 6.776M against an expected 0.126M, from a previous reading of -1.071M.

French Consumer Price Index (EU norm) (YoY) (Jan) was released coming in at 1.5% against an expected 1.1%, from 1.2% previously.

German Unemployment Change (Jan) was -25K v an expected -17K, from -29K previously, which was revised down to 30K. Unemployment Rate s.a. (Jan) was 5.4% v an expected 5.5%, against 5.5% prior. EURUSD moved higher from 1.24323 to a high of 1.24596 after this data release.

Eurozone Unemployment Rate (Dec) was as expected, unchanged at 8.7%. Consumer Price Index – Core (YoY) (Jan) was as expected at 1.0%, from 1.1% prior. Consumer Price Index (YoY) (Jan) was also as expected at 1.3, from 1.4% previously. EURUSD sold off from its high at 1.24596 to 1.24391 before rebounding higher again.

US ADP Employment Change (Jan) was 234K v an expected 185K, from 250K previously, which was revised down to 242K. Employment Cost Index (Q4) was as expected at 0.6%, from 0.7% previously. USDJPY moved up from 108.843 to 108.981 following this data release.

US Chicago Purchasing Managers' Index (Jan) was 65.7 v an expected 64.1, from a prior read of 67.8, which was revised up from 67.6.

Pending Home Sales (YoY) (Dec) was -1.8% v an expected -0.2%, from a prior reading of 0.6%. Pending Home Sales (MoM) (Dec) was 0.5% v an expected 0.4%, from a prior reading of 0.2%, which was revised up to 0.3%. GBPUSD tested support at 1.41644 before moving higher to 1.42320.

Chinese Caixin Manufacturing PMI (Jan) was 51.5 v an expected 51.3, from 51.7 previously, which was revised down to 51.5. This shows an improvement at a modest pace.

EURUSD is down -0.13% overnight, trading around 1.23971.

USDJPY is up 0.32% in early session trading at around 109.531.

GBPUSD is down -0.16% to trade around 1.41660.

USDCAD is up 0.05%, trading around 1.23187.

Gold is down -0.21% in early morning trading at around $1,341.80.

WTI is unchanged this morning, trading around $64.68.

Major data releases for today:

At 08:15 GMT, Swiss Real Retail Sales (YoY) (Dec) will be released with an expected 1.5% from -0.2% previously.

At 08:55 GMT, German Markit Manufacturing PMI (Jan) is expected to be unchanged at 61.2. EUR crosses could be affected by this data.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (Jan) is expected to be unchanged at 59.6. EUR pairs may be moved by this release.

At 09:30 GMT, UK Markit Manufacturing PMI (Jan) is expected to be 56.5 from 56.3 previously. GBP pairs may be moved by this release.

At 13:30 GMT, US Continuing Jobless Claims (Jan 19) is expected to be 1.928M from 1.937M previously. Initial Jobless Claims (Jan 26) is expected to come in at 238K from 233K previously. Nonfarm Productivity (Q4) is expected to be in at 1% from 3% previously. Unit Labour Costs (Q4) is expected to be 0.8% from -0.2% prior. USD crosses could see an increase in volatility from this data release.

At 14:30 GMT, Canadian Markit Manufacturing PMI (Jan) is expected to be 54.8 from 54.7 previously. CAD crosses could be moved by this release.

At 14:45 GMT, US Markit Manufacturing PMI (Jan) is expected to be 54.9 from 55.5 previously. USD pairs may be moved by this release.

At 15:00 GMT, US ISM Prices Paid (Jan) is due out with a consensus of 68.0 expected. The previous reading was 69.0. ISM Manufacturing PMI (Jan) is also out at this time, with an expectation for a number of 58.8 v 59.7 prior, which was revised down to 59.3. And finally, Construction Spending (MoM) (Dec) is expected at 0.4% from the previous reading of 0.8%. USD crosses could be impacted by the volume of data releases at this time and turbulent price action can result.

At 19:00 GMT, New Zealand Building Permits s.a. (MoM) (Dec) will be released, with a previous reading of 10.8%. NZD crosses may experience volatility during this time.

Currencies: USD Little Changed Post Fed

Sunrise Market Commentary

- Rates: Fed more confident in economy and inflation

The Fed kept its policy rate unchanged, but sounded more upbeat on growth and on inflation. The outlook warrants further gradual rate increases. The market reaction was rather modest. Core bond momentum remains bearish, but the sell-off could slow ahead of tomorrow's payrolls. - Currencies: USD little changed post Fed

The dollar traded in the defensive yesterday ahead of the Fed meeting. The USD gained marginally ground as the Fed slightly upgraded its assessment on inflation and growth. However, no technically relevant levels have been regained yet. The markets are cautiously giving a higher probability to four rate hikes this year. Will this finally help the dollar?

The Sunrise Headlines

- US stock markets ended close to opening levels with another round of solid corporate earning putting investors back in the buying mood following a 2-day sell-off. Most Asian stock markets eke out gains with China underperforming.

- The Fed kept its policy rate unchanged at 1%-1.25%. The policy statement signalled greater confidence in officials' upbeat economic outlook. It also offered slightly more conviction that inflation would move higher in 2018.

- China's manufacturing sector sustained growth at multi-month highs in January, according to the Caixin PMI (51.5), as factories continued to raise output to meet new orders, suggesting resilience in the Chinese economy.

- US oil production surged above 10 million barrels a day for the first time in more than four decades, another marker of a profound shift in global crude markets.

- EU Brexit negotiators have set out a tough line on financial services, ruling out an ambitious trade deal for the lucrative sector and arguing that Europe would benefit from a smaller City of London, according to confidential discussions.

- Carles Puigdemont has said in a leaked private message to an ally that his drive to create a new independent Catalan republic was over and that the Spanish government had won.

- Today's eco calendar contains manufacturing surveys in EMU (final PMI), UK (PMI) and US (ISM). Weekly jobless claims will also be released. The CNB is expected to hike rates and ECB Praet is scheduled to speak

Currencies: USD Little Changed Post Fed

Dollar little changed post-Fed

The dollar initially remained under pressure in the run-up to the Fed policy statement yesterday. The EMU inflation was soft at 1.3% Y/Y, but didn't hurt the euro. The dollar didn't profit from very strong ADP job growth. The dollar finally found a better bid in the last hours before the Fed decision. The Fed as expected left its policy unchanged. Yellen and co grow more confident on the economic expansion. They also see signs of a gradual rise in inflation/inflation expectations that warrants further gradual policy tightening. The market reaction was very limited. After some hesitation, the dollar gained a few more ticks. EUR/USD finished the session at 1.2424. USD/JPY closed at 109.19.

Asian equities mostly trade in positive territory overnight with Japan outperforming and China underperforming. USD/JPY extends most gains north of 109. EUR/USD hovers in the low 1.24 area. The Aussie dollar is drifting away from the recent top. Yesterday's soft inflation data and weak housing data today are weighing on the currency.

The eco calendar contains the final EMU manufacturing PMI and the US manufacturing ISM. The headline PMI is expected to ease from 59.3 to 58.6, more or less in line with evidence from regional indicators. The price index is expect to stay at a very high level (68.8). Aside from the data, markets will ponder the consequences from yesterday's Fed assessment. The debate on 3 or 4 rate hikes this year continues. Chances on four hikes are gradually rising. Question is whether this will be enough to finally put a floor for the dollar.

The dollar developed a very tepid bottoming out process since the end of last week, but didn't regain any technically relevant level yet. For now, some further consolidation might be on the cards going into the payrolls. EUR/USD 1.2537/98 is the first topside resistance. EUR/USD 1.2323/35 is a minor support short-term. A break below 1.2165 would call off the ST downside alert (for the dollar).

Sterling made some intraday swings yesterday probably mostly driven by end of month positioning. Today, the UK Manufacturing PMI is expected to improve slightly from 56.3 to 56.5. A positive surprise might be slightly supportive for sterling. However, political noise both on the relations between the UK and the EU and on the internal discord with May's party will probably dominate the headlines. For now we expect EUR/GBP to hold the 0.8690/0.8928 range.

EUR/USD: no big reaction post-Fed. Topside run a bit exhausted?

Australia’s Manufacturing Sector Advanced In January, Building Approvals Slumped In December

For the 24 hours to 23:00 GMT, the AUD declined 0.12% against the USD and closed at 0.8058.

LME Copper prices rose 0.7% or $51.5/MT to $7100.5/MT. Aluminium prices declined 0.2% or $4.5/MT to $2224.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.8051, with the AUD trading 0.09% lower against the USD from yesterday's close.

Overnight data revealed that Australia's AiG performance of manufacturing index registered a rise to a level of 58.7 in January, after recording a reading of 56.2 in the prior month. On the contrary, the nation's seasonally adjusted building approvals plummeted 20.0% on a monthly basis in December, higher than market expectations for a drop of 7.6%. Building approvals had risen 11.7% in the previous month.

Elsewhere in China, Australia's largest trading partner, the Caixin/Markit manufacturing PMI index remained steady at a level of 51.5 in January, meeting market expectations.

The pair is expected to find support at 0.8018, and a fall through could take it to the next support level of 0.7986. The pair is expected to find its first resistance at 0.8100, and a rise through could take it to the next resistance level of 0.8150.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Growth Cooled To A 6-Month Low Level In January

For the 24 hours to 23:00 GMT, the EUR declined slightly against the USD and closed at 1.2417.

Macroeconomic data showed that the Euro-zone's flash consumer price index (CPI) rose 1.3% on an annual basis in January, meeting market expectations, recording its weakest growth rate since July 2017, thus stoking fears that stubbornly low inflation might continue to bother policymakers in 2018. The CPI had recorded a gain of 1.4% in the prior month. Nevertheless, the region's unemployment rate remained steady at a 9-year low of 8.7% in December, meeting market expectations.

Separately, Germany's seasonally adjusted unemployment rate eased to a fresh record low of 5.4% in January, in line with market expectations, pointing to continuous tightening in the domestic labour market. Unemployment rate had posted a reading of 5.5% in the prior month. On the contrary, the nation's retail sales retreated more-than-anticipated by 1.9% on a monthly basis in December, compared to a revised increase of 1.8% in the prior month, while markets were anticipating retail sales to ease 0.4%.

The US Dollar initially gained ground against its major peers, after the Federal Reserve (Fed), at its January monetary policy meeting, provided an upbeat view on inflation, spurring speculation that the central bank will pick up the pace of interest-rate hikes this year.

The Federal Open Market Committee (FOMC), in a widely expected move, voted unanimously to leave the benchmark interest rates unchanged in a range of 1.25% to 1.50%. In a statement post-meeting, the central bank stated that it expects sluggishly low inflation to finally pick-up this year and to stabilise around its 2.0% goal. Further, the central bank hinted at further gradual monetary policy tightening, as the world's largest economy is growing at a robust pace and the labour market continues to improve.

On the macro front, ADP's private sector employment in the US climbed by 234.0K in January, exceeding market expectations for an advance of 185.0K, thus underscoring strength of the labour market. The private sector employment had recorded a revised increase of 242.0K in the previous month. Moreover, the nation's pending home sales grew 0.5% on a monthly basis in December, meeting market expectations and rising for the third straight month. In the previous month, pending home sales had climbed by a revised 0.3%.

On the other hand, the nation's Chicago Fed PMI fell less-than-estimated to a level of 65.7 in January, compared to market expectations for a drop to a level of 64.0. The PMI had recorded a revised level of 67.8 in the previous month. Additionally, the nation's MBA mortgage applications declined 2.6% in the week ended 26 January. In the previous week, mortgage applications had climbed 4.5%.

In the Asian session, at GMT0400, the pair is trading at 1.2424, with the EUR trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2382, and a fall through could take it to the next support level of 1.2341. The pair is expected to find its first resistance at 1.2470, and a rise through could take it to the next resistance level of 1.2517.

Looking forward, traders would keep a close watch on the release of final Markit manufacturing PMI for January across the Euro-zone, scheduled in a few hours. Additionally, the US initial jobless claims, followed by the ISM manufacturing and the final Markit manufacturing PMIs for January, as well as construction spending data for December, would keep investors on their toes.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Pound Trading A Tad Lower, Ahead Of Britain’s Manufacturing PMI Data

For the 24 hours to 23:00 GMT, the GBP rose 0.27% against the USD and closed at 1.4199.

In the Asian session, at GMT0400, the pair is trading at 1.4197, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.4135, and a fall through could take it to the next support level of 1.4073. The pair is expected to find its first resistance at 1.4246, and a rise through could take it to the next resistance level of 1.4295.

Moving ahead, traders would focus on UK's Markit manufacturing PMI for January, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.