Sample Category Title

Japanese Manufacturing Sector Growth Revised Higher In January

For the 24 hours to 23:00 GMT, the USD rose 0.3% against the JPY and closed at 109.22.

In the Asian session, at GMT0400, the pair is trading at 109.34, with the USD trading 0.11% higher against the JPY from yesterday’s close.

Data released overnight showed that Japan’s final Nikkei manufacturing PMI climbed to a level of 54.8 in January, higher than a rise to a level of 54.4 indicated in the preliminary print and remaining at a nearly 4-year high level. In the prior month, the PMI had recorded a level of 54.0.

The pair is expected to find support at 108.81, and a fall through could take it to the next support level of 108.28. The pair is expected to find its first resistance at 109.66, and a rise through could take it to the next resistance level of 109.98.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss ZEW Economic Expectations Index Eased In January

For the 24 hours to 23:00 GMT, the USD declined 0.33% against the CHF and closed at 0.9316.

On the economic front, Switzerland’s ZEW economic expectations index dropped to a level of 34.5 in January, after recording a level of 52.0 in the previous month. Also, the nation’s UBS consumption indicator fell to a level of 1.69 in December, compared to a revised reading of 1.73 in the previous month.

In the Asian session, at GMT0400, the pair is trading at 0.9315, with the USD trading slightly lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9287, and a fall through could take it to the next support level of 0.9259. The pair is expected to find its first resistance at 0.9345, and a rise through could take it to the next resistance level of 0.9375.

Moving ahead, market participants would closely monitor Switzerland’s SECO consumer confidence index and the SVME-PMI, both for January along with the nation’s real retail sales for December, set to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Canada’s Economy Accelerates At Its Quickest Pace In 6 Months In November

For the 24 hours to 23:00 GMT, the USD declined 0.15% against the CAD and closed at 1.2308.

The Canadian Dollar jumped against the USD, following strong Canadian GDP figures.

Data showed that Canada's gross domestic product (GDP) climbed 0.4% on a monthly basis in November, meeting market expectations and rising by the most since May 2017. The GDP had registered a flat reading in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2308, with the USD trading flat against the CAD from yesterday's close.

The pair is expected to find support at 1.2262, and a fall through could take it to the next support level of 1.2215. The pair is expected to find its first resistance at 1.2344, and a rise through could take it to the next resistance level of 1.2379.

Ahead in the day, all eyes will be on Canada's RBC manufacturing PMI for January.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Market Update – Asian Session: Markets Mixed After Fed Holds Rates

Headlines/Economic Data

General Trend:

Fairly quiet Asian trading session for the FX majors post FOMC statement

Markets looking ahead to Apple’s earnings release on Thursday

Japan

Nikkei 225 opened +0.8%; closed +1.7%

TOPIX Iron & Steel Index gains over 2%, Securities higher by more than 1.5%

Mega-banks gain after reporting 9-month results and affirming outlooks: Sumitomo Mitsui higher by over 3%, Mizuho Financial gains more than 2%

Fujifilm [4901.JP]: Gains over 12% after confirming merger with Xerox

Fujitsu [6702.JP]: Declines over 9% as 9-month Op profit declined y/y

Nippon Steel [5401.JP]: Reports 9M Net ¥156.1B v ¥59.4B y/y; Op ¥138.0B v ¥62.2B y/y; Rev ¥4.16T v ¥3.33T y/y; Raises guidance for FY17/18 Net ¥180B v ¥170B prior

(JP) Japan Jan Final Manufacturing PMI: 54.8 v 54.4 prelim (highest since Feb 2014)

(JP) Japan MoF sells ¥2.3T v ¥2.3T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.088% v 0.078% prior; bid to cover 4.58x v 3.74x prior

Korea

Kospi opened +0.5%

Celltrion [068270.KR]: Declines over 2% after receiving US FDA warning letter

(KR) SOUTH KOREA JAN CPI M/M: 0.4% V 0.7%E; Y/Y: 1.0% V 1.3%E, CPI Core Y/Y: 1.1% v 1.5%e

(KR) SOUTH KOREA JAN TRADE BALANCE: $3.72B V $4.0BE

(KR) South Korea Major department stores have put a large number of delivery workers on standby for the Lunar New Year holiday, expecting stronger sales after adjustments to an anti-corruption law - Korean press

China/Hong Kong

Hang Seng opened +0.2%, Shanghai Composite -0.1%

Hang Seng Services Index -1.2%, Consumer Goods -0.8%

ZTE Corp [0763.HK]: Has dropped over 9% after announcing planned share sale

Lenovo, 992.HK Reports Q3 Net loss $288.8M v profit $125Me; Rev $12.9B v $12.5Be

(HK) Macau Jan Gaming Rev MOP26.3B, +36.4% v 27%e (largest gain since 2014)

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3045 v 6.3339 PRIOR

(CN) China PBoC: Skips OMO (6th straight session) v skipped prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3045 v 6.3339 PRIOR

(CN) CHINA JAN CAIXIN MANUFACTURING PMI: 51.5 V 51.5 PRIOR

(CN) China Commerce Ministry (MOFCOM): Reiterates hopes US does not politicize trade issues, still views US as 'partner' in trade

(CN) China 2017 gold consumption 1,089 tonnes, +9.4% y/y; production 426.1 tonnes, -6.0% y/y-

Australia/New Zealand

ASX 200 opened +0.5%; closed %

ASX 200 Consumer Discretionary Index +1.4%, Financials +1.1% Resources +1.1%, Energy +1.2%, Utilities +0.9%

(AU) Australia Treasurer Morrison: To tighten rules for key energy infrastructure and farmland M&A

(AU) AUSTRALIA DEC BUILDING APPROVALS M/M: -20.0% V -7.6%E; Y/Y: -5.5% V 11.5%E

(AU) AUSTRALIA Q4 EXPORT PRICE INDEX Q/Q: 2.8% V 2.0%E; IMPORT PRICE INDEX Q/Q: 2.0% V 1.5%E

Other Asia

(TW) Taiwan names current Deputy Gov Yang Chin-Long as new Central Bank Gov [**Note: Current Gov Perng has been Gov of the central bank since Feb 1998]

(ID) Indonesia Jan CPI m/m: 0.6% v 0.7%e; y/y: 3.3% v 3.3%e; Core y/y: 2.7% v 2.8%e (core CPI at multi-year low)

North America

US equity markets ended mostly higher: Dow +0.3%, S&P500 +0.1%, Nasdaq +0.1%, Russell 2000 -0.5%

S&P500 Real Estate sector +2.1%, Utilities +1.1%

PayPal [PYPL] declines over 11% in the afterhours: eBay said that Adyen will become its primary payments processing partner, replacing PayPal (timing uncertain)

eBay [EBAY]: Gains more than 8% in afterhours: Q4 $0.59 v $0.59e, Rev $2.60B v $2.61Be; Guides Q1 $0.52-0.54 v $0.51e; Rev $2.57-2.61B v $2.39Be

AT&T [T]: Higher by over 2.5% in the afterhours: Reports Q4 $0.78 adj v $0.66e, Rev $42B v $41.2Be; Guides initial FY18 $3.50 v $3.08e,

US Steel [X]: Gains over 2% in the afterhours: Reports Q4 $0.76 v $0.68e, Rev $3.13B v $3.07Be; Guides initial FY18 ~$3.88 v $3.28e

(US) FOMC HOLDS TARGET RATE RANGE AT 1.25-1.50% (AS EXPECTED); Vote was unanimous; Inflation to rise this year, stabilize around 2% in medium term

(US) Former Fed Chair Greenspan: We have stock market and bond market bubbles - TV interview

(US) DOE CRUDE: +6.8M V +2ME

Looking Ahead: Apple due to report quarterly results after the US equity close on Thursday; US Jan ISM Manufacturing PMI due for release

Europe

(UK) China Commerce Ministry: To sign £9B worth of deals with the UK when PMc May visits China

(EU) EU said to be considering a tax blacklist on UK post Brexit

(EU) ECB’s Coeure (France): Currency war is always a losing proposition - press interview

(EU) European Banking Authority (EBA) released macroeconomic scenarios related to 2018 EU-wide stress test; The adverse scenario encompasses a wide range of macroeconomic risks that could be associated with Brexit.

(IT) Forza Italia party denies reports about Berlusconi's ill health; A report earlier this week said Berlusconi, age 81, was ordered by his doctor to stop campaigning and rest for at least 48 hours.

Levels as of 01:00ET

Nikkei225 +1.7%, Hang Seng -0.3%; Shanghai Composite -1.1%; ASX200 +0.9%, Kospi +0.3%

Equity Futures: S&P500 +0.3%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.3%

EUR 1.2429-1.2406; JPY 109.41-109.09; AUD 0.8063-0.8035;NZD 0.7381-0.7352

Apr Gold +0.4% at $1,347/oz; Mar Crude Oil +0.3% at $64.89/brl; Mar Copper +0.1% at $3.20/lb

Elliott Wave View: SPX Correction In Progress

SPX Short Term Elliott Wave view suggests that the rally to 2872.15 ended Primary wave ((3)). Down from there, Primary wave ((4)) pullback is unfolding as a double three Elliott Wave structurewhere Intermediate wave (W) ended at 2818.27 and Intermediate wave (X) ended at 2839.26. Intermediate wave (Y) is in progress and while near term bounces stay below 2872.15, expect the Index to extend lower towards 2774.3 – 2786.8 area to end Primary wave ((4)) before Index resumes the rally or at least bounce in 3 waves. We don’t like selling the Index and expect buyers to appear from the above area for a 3 waves bounce at minimum.

SPX 1 Hour Elliott Wave Chart

GBP/JPY Daily Outlook

Daily Pivots: (S1) 153.89; (P) 154.61; (R1) 155.68; More...

Intraday bias in GBP/JPY remains neutral at this point. For the moment, 156.07 is seen as a short term top. Hence, risk remains mildly on the downside for another another fall. Also, break of 151.95 will now be an early sign of reversal and will bring deeper decline back to 149.96 key support level. Nonetheless, above 156.07 will resume larger up trend to 167.78 fibonacci level.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

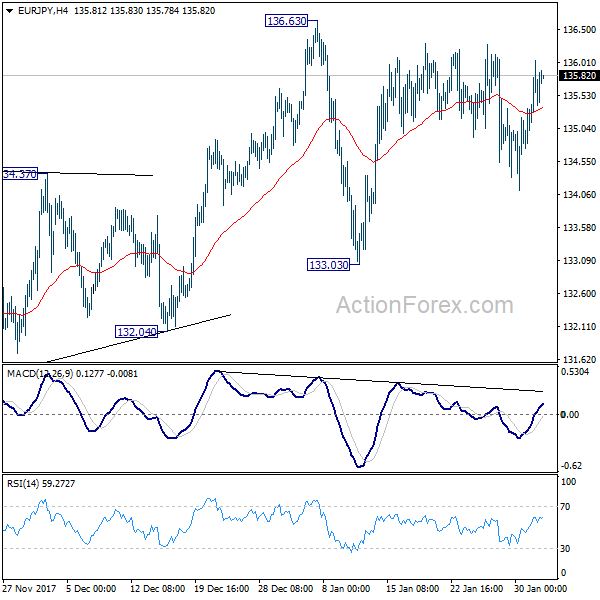

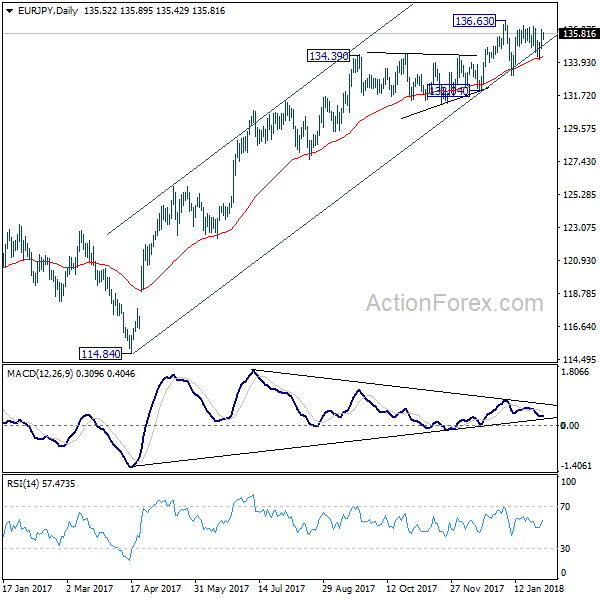

EUR/JPY Daily Outlook

Daily Pivots: (S1) 134.89; (P) 135.46; (R1) 136.11; More....

EUR/JPY is still staying in consolidation below 136.63 and intraday bias remains neutral. Near term outlook remains bullish as 133.03 support is intact. On the upside, break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

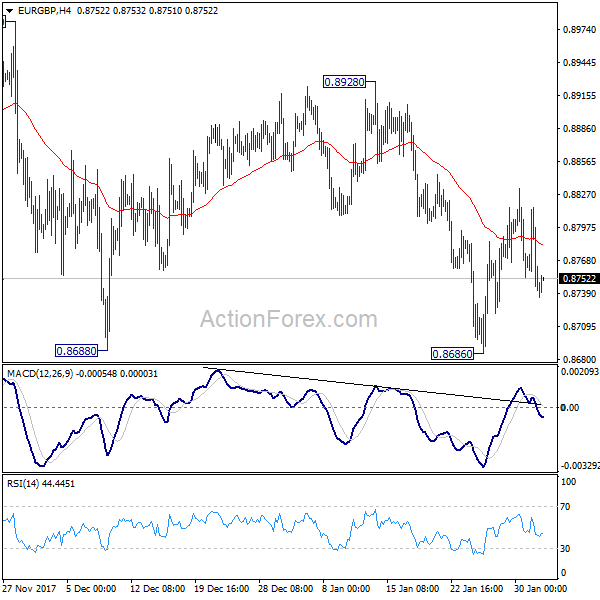

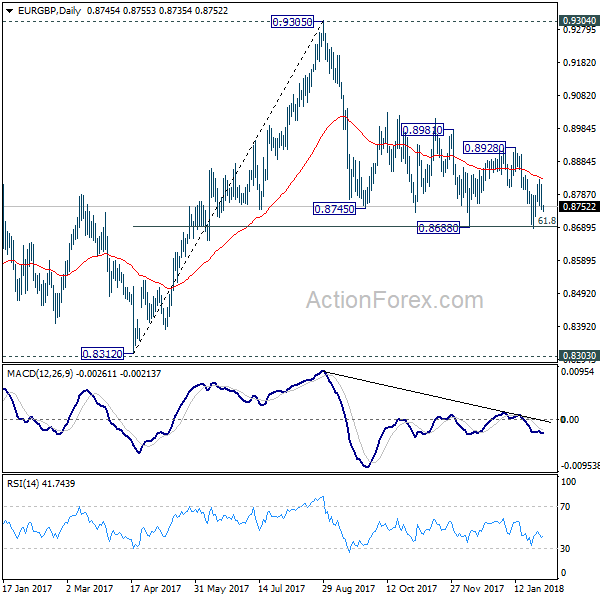

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8719; (P) 0.8767; (R1) 0.8794; More...

EUR/GBP continues to gyrate in range of 0.8686/8928 and intraday bias remains neutral. Outlook stays bearish with 0.8928 resistance intact. That is, fall from 0.9305 is expected to resume later. Break of 0.8686 will also have 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. In that case, deeper decline would be seen to retest 0.8303/8312 support zone.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

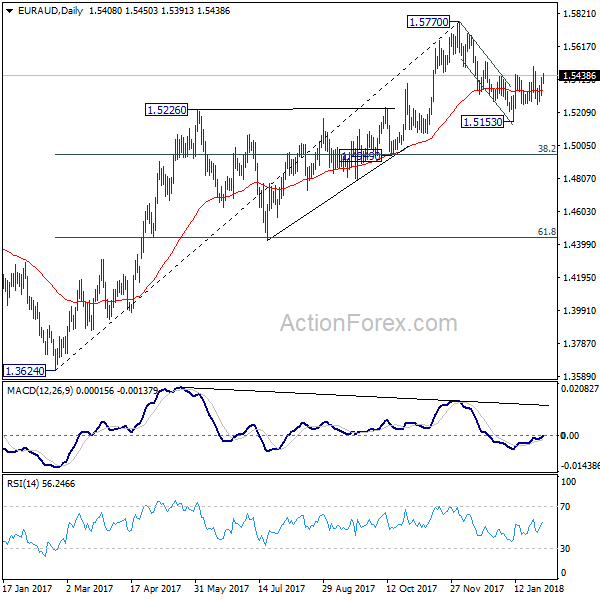

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5338; (P) 1.5381; (R1) 1.5449; More....

EUR/AUD is staying in range of 1.5259/5494 and intraday bias remains neutral. Fall from 1.5770 is likely not finished yet. Below 1.5259 should send EUR/AUD through 1.5153 low to 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950). On the upside, break of 1.5494 will extend the rebound form 1.5153. But we don't expect a break of 1.5770 in first attempt.

In the bigger picture, price actions from 1.5770 so far suggests that it's corrective in nature. That is, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

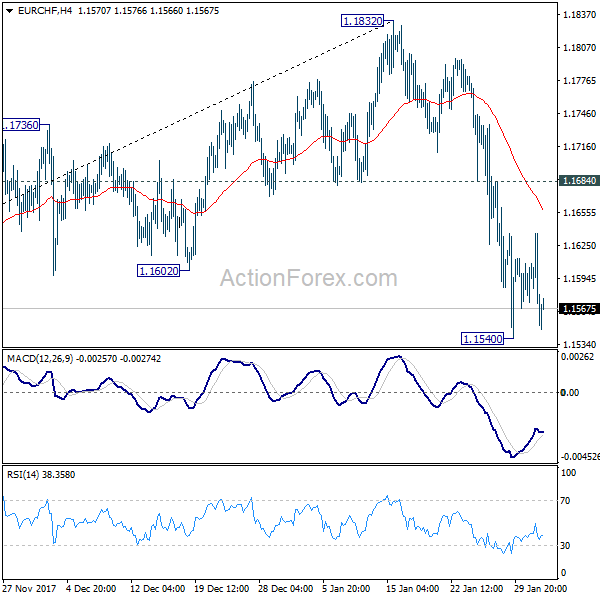

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1527; (P) 1.1582; (R1) 1.1613; More...

Intraday bias in EUR/CHF stays neutral for consolidation above 1.1540 temporary low. In case of another recovery, upside should be limited by 1.1684 resistance to bring fall resumption. As noted before, the decline from 1.1832 is correcting medium term rise from 1.0629. Below 1.1540 will target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.)

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.