Sample Category Title

EURJPY Runs Sharply Higher; Bulls Took the Lead

EURJPY has reversed back up again after finding support at the 134.10 barrier during yesterday's trading session. The pair has been developing higher along its current trend line since August 18. Additionally, over the last hours, prices broke above the 135.00 handle and are trading above the short-term moving averages.

The pair is recording a sharp upside movement and the short-term momentum indicators are pointing to a bullish bias. The Relative Strength index (RSI) entered the positive territory and is strengthening its momentum, whilst the MACD oscillator is moving higher in the bearish area above its trigger line.

On the upside, if prices continue the bullish rally, there is scope to test the 136.30 resistance level. Clearing this key level could see additional gains towards the 136.60 obstacle, taken from the high on January 05.

If prices reverse lower, immediate support should come at 23.6% Fibonacci retracement level at 134.40 with the low of 127.45 and the high of 136.60. Below that, the 134.10 is another major support around 134.10, which is holding slightly above the ascending trend line.

Sunset Market Commentary

Markets

Global core bond trading slowed to a trickle today ahead of tonight's FOMC meeting. Both the Bund and the US Note future eke out some gains with end-of-month extension buying playing a minor role. EMU CPI remains low at 1.3% Y/Y for the headline and 1% Y/Y for the core reading, but didn't affect intraday trading dynamics. Strong German and US labour market data couldn't do the trick neither. The US yield curve flattens with yield changes ranging between +0.4 bps (2-yr) and -2.9 bps (30-yr). The German yield curve bull flattens with yields 0.5 bps (2-yr) to 6 bps (30-yr) lower. The significant outperformance of the 30-yr yield is partly technically related following the failed attempt to break above the 2017 top (1.38%). 10-yr yield spread changes versus Germany are barely changed with Greece underperforming (+7 bps). We expect the Fed to leave policy rates unchanged tonight (even though the market implied probability of a hike is 20%), but upgrade its assessment of the economy and inflation thereby paving the way for a March hike. Given market positioning, this could trigger a steepening of the US curve, with room for a short term correction lower in yields at the front end. The US Treasury's announcement (quarterly refunding) that it will halt attempts to extend the maturity of its debt also argues in favour of some steepening as supply will be more directed to the front-and of the curve.

EUR/USD continued trading with a positive bias today. Dollar caution ahead of the Fed policy decision was probably at play. At the same time, the euro remained will bid even as EMU eco data were mixed, at best. EMU (un)employment data confirmed an ongoing improvement in labour market conditions. On the other hand, German retail sales printed soft and EMU inflation (headline 1.3% in January from 1.4%) drifted further away from the 2% ECB target. On the other side of the Atlantic, ADP private job growth was very strong (234 k). The report was completely ignored in EUR/USD trading. The pair trades currently at 1.2450. USD/JPY gained a few ticks an is nearing the 109 barrier. The focus now turns to the Fed statement. An unchanged decision is expected, but the Fed might upgrade its assessment on growth and inflation. Will the Fed's assessment by strong enough to put a floor for the dollar?

Sterling opened strong this morning. Political noise from the UK government continued to linger. However, the UK currency was supported by decent data overnight and, more importantly, by modestly hawkish comments from BoE governor Carney. Yesterday, he indicated that the BoE could give some more weight to inflation in its assessment further out this year. EUR/GBP traded in the 0.8760 area at the start of European dealings. However, gradually some sterling selling kicked in. A big EUR/GBP buying order and end-of month position adjustments were rumoured to be behind the move. Euro strength was a secondary factor, too. EUR/GBP trades in the 0.88 area. USD weakness kept cable in the 1.4150/1.42 area.

News Headlines

EMU Inflation slowed at the start of the year, highlighting the hurdles faced by the ECB as it attempts to foster price growth in a region still beleaguered in places by high unemployment. CPI rose 1.3% Y/Y in January, above 1.2% Y/Y consensus, but down from 1.4% Y/Y. Core CPI picked up from 0.9% Y/Y to 1% Y/Y. The EMU unemployment rate stabilized at 8.7%, matching the lowest level since January 2009. German unemployment extended its decline as companies stepped up hiring to meet buoyant demand. The German jobless rate dropped to a record low of 5.4% in January. The number of people out of work plunged by 25,000 to 2.415 mn (vs -17,000 forecast).

Hiring in the US private sector continued to outperform expectations in January, underscoring the strength of the labour market. Non-farm private sector employers added 234,000 jobs this month, according to a report from payroll processor ADP. The figure easily topped expectations for 185,000 jobs and marks the fourth straight month of 200k+ gains. The Chicago PMI declined from 67.8 to 65.7, beating consensus (64) and remaining near the highs

Auto Production Helped the Canadian Economy Come Back to Life in November

The Canadian economy jumped ahead in November, with output rising 0.4% month-on-month as the manufacturing and resource sectors came back to life following earlier setbacks. 17 of the 20 major industries saw output gains, the broadest base of expansion since April 2017.

The goods producing side of the economy led the way, up 0.8% month-on-month. With production resuming at several major auto plants following earlier shutdowns, manufacturing jumped 1.8%. This was the largest monthly gain in three years, supported by a 14.3% increase in motor vehicle manufacturing. Resource extraction also gained, up 0.5%. The increase was largely due to the oil and gas sector as production continued to improve following earlier maintenance activities at several facilities.

The service industries remained steady performers, recording a 20th straight monthly expansion. Aggregate services output rose 0.3%, helped by solid retail and wholesale trade figures (up 0.6% and 0.5% respectively).

Key Implications

When it comes to economic growth, what goes down usually pops back up, with the November GDP figures the perfect example. Earlier setbacks in key sectors, including retooling at key auto production facilities and disruptions in the oil sector have since been resolved. The result was a solid headline gain of 0.4%.

Equally important to the strength of growth was its breadth. The Canadian economy fired on all cylinders in November: production resumptions led the way, but nearly all major sectors reported gains on the month, an encouraging sign.

Just as one should 'look through' one-off shocks such as maintenance shutdowns, the pop in activity that occurs as production comes back online should also be discounted. That said, as shown by this month's breadth of growth, the underlying trend for the Canadian economy remains a positive one: economic growth of around 2.4% (annualized) looks likely for the fourth quarter of 2017, confirming the spate of positive economic indicators that have so far characterized the end of last year.

The Bank of Canada will undoubtedly be encouraged by today's report, not least as it confirms their most recent economic growth tracking. Confirmation does not mean a change in view however, and today's report does little to change the notion that the balance of economic fundamentals vs risks suggests July is the most likely timing for the next rate increase.

Canadian GDP Bounced Back in November

Highlights:

- Canadian GDP rose 0.4% in November - bouncing back after the weaker-than-expected flat reading in October.

- Growth in the mining and manufacturing sectors benefited from the end of earlier transitory shutdowns but gains were also widespread, if more modest, outside of those sectors.

- The November GDP gain is consistent with the economy growing at a 1.9% pace (annualized) in Q4 - down from the outsized mid-2016 to mid-2017 pace but still above most estimates of the economy's long-run run rate.

Our Take:

GDP rose 0.4% in November after a surprisingly weak flat reading in October. Nonconventional oil extraction bounced back 3.7% to reverse a 3.4% decline in October that was reportedly the result of transitory maintenance shutdowns. A 1.8% surge in manufacturing output also reflected a retracement of earlier weakness as shutdowns of some motor vehicle and chemical production in earlier months ended. Increases outside of those two components were generally more modest but widespread. Statistics Canada noted 17 of 20 industries posted increases in November. Yes, uncertainties remain about the outcome of NAFTA renegotiations and that could have significant implications in particular for the manufacturing sector that accounted for a big chunk of November's GDP growth. Looking through monthly volatility, though, the GDP numbers add to the evidence that the Canadian economy as a whole continues to grow at a modestly 'above-potential' pace even as it increasingly looks to be operating at or beyond its long-run capacity. With inflation still remaining well-behaved, the Bank of Canada can continue be cautious about raising interest rates, particularly in light of elevated household debt levels. Absent a downside surprise on near-term growth or an unexpectedly 'bad' outcome from NAFTA negotiations, though, we expect the central bank will continue to ease off on the accelerator in terms of monetary policy and look for gradual interest rate hikes to continue this year.

USDCAD – Loonie Hits New Over 4-mth High on Weaker Greenback and Solid Canadian Data

The USDCAD pair fell to new over four-month low on Wednesday at 1.2248 as loonie benefited from weaker greenback after President Trump's speech, with positive impact on upbeat US ADP jobs data (234K in Jan vs 186K f/c).

Canadian dollar received additional support from Canada's solid data on Wednesday as GDP came in line with expectations in Nov (0.4%) but above 0.0% previous month while Industrial Product Price Index (IPPI) and Raw Materials Price Index (RMPI) showed better than expected results in December (IPPI -0.1% vs -0.2% f/c) and (RMPI -0.9% vs -2.2% f/c).

Fresh weakness comes after brief consolidation phase which was capped by falling 10SMA and today's dip cracked support at 1.2263 (Fibo 76.4% of larger 1.2061/1.2920 ascend) which marks the only significant obstacle on the way to key med-term support and target at 1.2061 (08 Sep low).

Close below 1.2263 is needed for fresh bearish signal for continuation of downtrend from 1.2920 (19 Dec high).

The outcome of Fed's two-day monetary policy meeting which ends today is in focus as investors are looking for more clues about US central bank's next steps.

Falling 10SMA marks solid resistance (currently at 1.2378) which is expected to limit upticks and keep immediate bears intact.

Stronger recovery above falling 20SMA (1.2419) would sideline immediate downside risk.

Res: 1.2348; 1.2378; 1.2419; 1.2488

Sup: 1.2263; 1.2248; 1.2195; 1.2118

Dollar Slips ahead of Fed Meeting, Bitcoin Wobbles

Market players who were expecting fireworks from President Donald Trump's first State of the Union address, were left empty-handed following the Dollar's fairly muted response. Although Trump stuck to script and adopted a more conciliatory tone, the address failed to offer fresh insight into the $1.5 trillion infrastructure spending plan.

The Dollar found itself under noticeable selling pressure on Wednesday, ahead of the Federal Reserve decision later today, which is widely expected to conclude with monetary policy unchanged. It is already considered a foregone conclusion that US interest rates will be left unchanged in January, so attention will largely be directed towards the press conference by Yellen. Today's FOMC could have a nostalgic note, considering that this will be Janet Yellen's last Fed meeting as Chair. The Dollar could be offered a lifeline if policymakers adopt a hawkish stance and reinforce markets' expectations of three rate hikes in 2018.

From a technical standpoint, the Dollar Index is under pressure on the daily charts. Sustained weakness below 89.00 could invite a decline towards 88.50, and 88.00.

Carney comes to the rescue

Sterling bulls received a shot in the arm on Tuesday thanks to Mark Carney's upbeat tone on the UK economy. With the Bank of England now turning its focus towards bringing down inflation, speculations may heighten over the central bank raising interest rates faster than expected. Although the Pound could continue to benefit from renewed rate expectations, the upside could be capped by Brexit concerns and political developments at home. From a technical standpoint, the GBPUSD remains bullish on the daily charts thanks to ongoing Dollar weakness. If the upside momentum holds, prices could challenge 1.4230 and 1.4300, respectively. Alternatively, an intraday breakdown below 1.4110 may trigger a decline towards 1.4000 and 1.3850, respectively.

Commodity spotlight - WTI Crude

WTI Crude found itself under intense selling pressure on Tuesday after industry reports illustrated an unexpected build in US crude inventories.

The fact that WTI sharply tumbled following the industry report continues to highlight how oil still remains sensitive to oversupply fears. While optimism over OPEC's production cuts rebalancing markets has inspired bulls, bears remain supported by concerns over US Crude production reaching new records. Oil prices could witness steep losses if US crude production hits the 10 million barrel per day mark. Focusing on the technical picture, WTI Crude bulls remain in control above the $63.00 higher low on the daily charts with the next level of interest at $65. A breakdown below $63 could trigger a decline back to $62.20.

Bitcoin shivers on crackdown fears

Bitcoin was in trouble on Tuesday with prices dipping below $10,000 after US regulators moved to crackdown on one of the world's largest digital currency exchanges. The selling pressure on Bitcoin was fueled by reports of Facebook Inc. banning adverts promoting cryptocurrencies. If cryptocurrencies continue to fall under the intense magnifying glass of regulators, this could weigh on demand and result in further downside. From a technical standpoint, Bitcoin remains heavily bearish with prices struggling to keep above $10,000. Sustained weakness below this level could encourage a further decline towards $9000, $8400 and $8000, respectively.

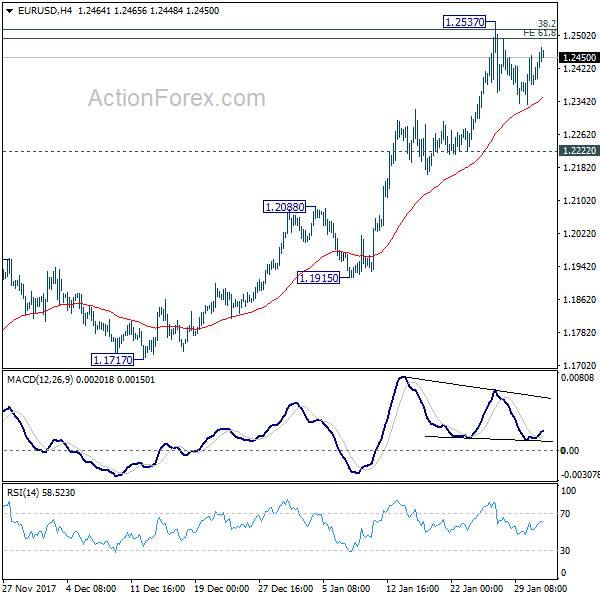

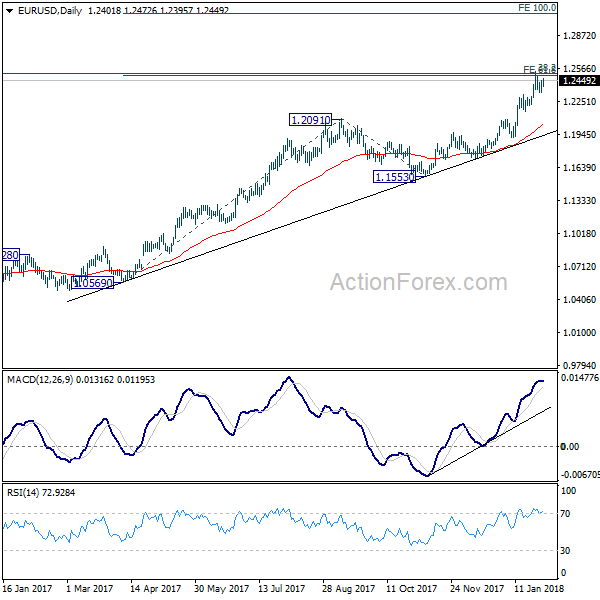

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2335; (P) 1.2383 (R1) 1.2431; More....

EUR/USD is still bounded in consolidation from 1.2537 and intraday bias remains neutral. As long as 1.2222 support holds, near term outlook remains bullish. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

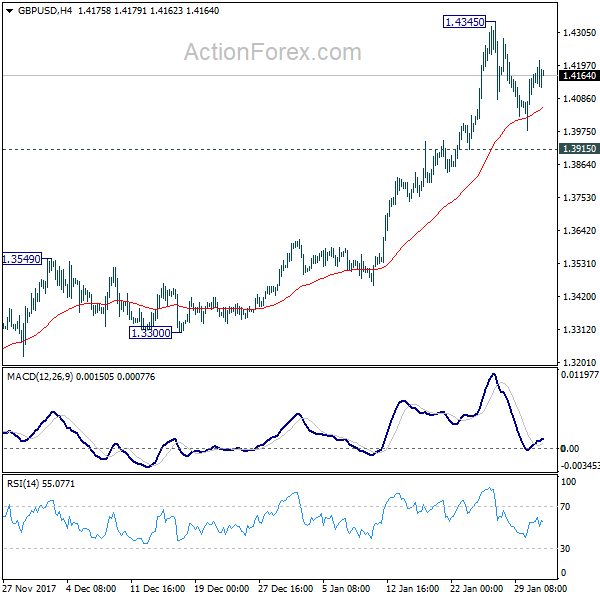

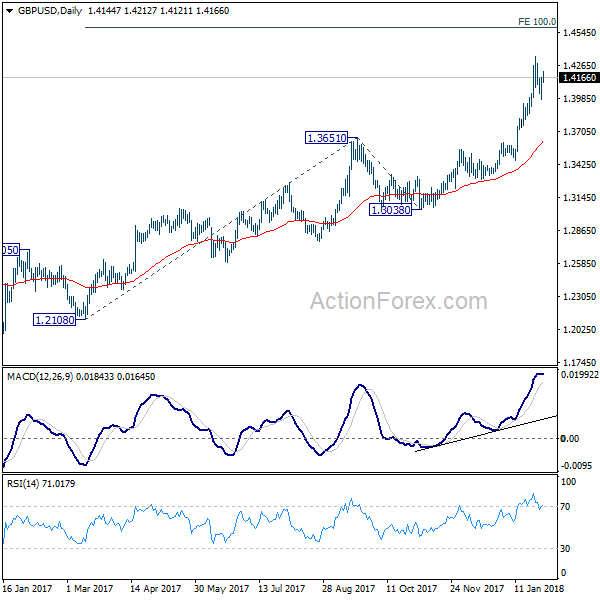

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4029; (P) 1.4098; (R1) 1.4216; More.....

GBP/USD is staying in consolidation below 1.4345 and intraday bias remains neutral first. More corrective trading could be seen. But downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

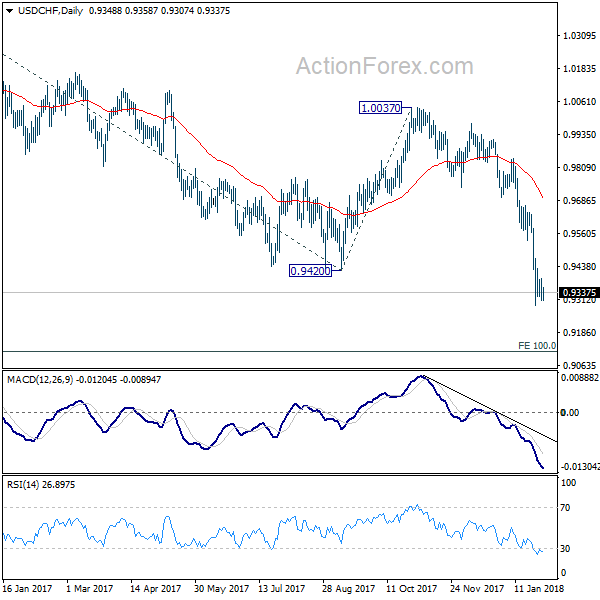

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9301; (P) 0.9347; (R1) 0.9384; More...

Intraday bias in USD/CHF remains neutral as consolidation from 0.9288 temporary low is in progress. With 0.9536 resistance intact, outlook stays bearish and deeper fall is expected. Break of 0.9288 will resume the larger down trend and target next key fibonacci level at 0.9115.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.39; (P) 108.79; (R1) 109.18; More...

USD/JPY is still bounded in consolidation from 108.27 temporary low. Intraday bias remains neutral at this point. As long as 110.18 resistance holds, deeper decline is expected. On the downside, break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).