Sample Category Title

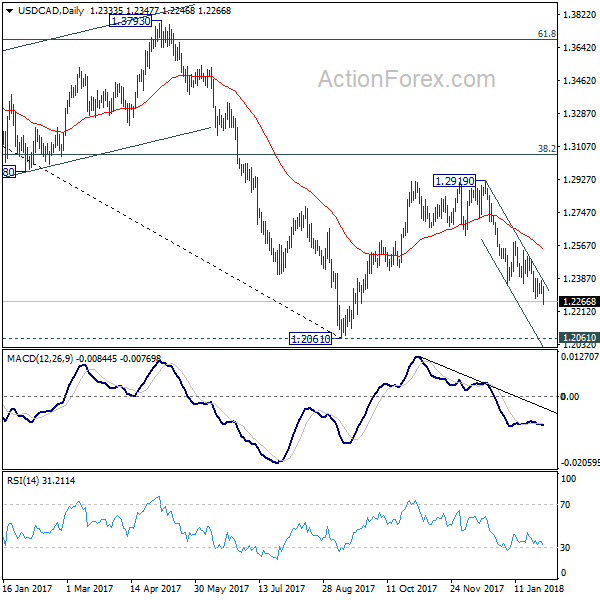

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2304; (P) 1.2341; (R1) 1.2375; More...

USD/CAD drops to as low as 1.2246 so far and break of 1.2281 indicates fall resumption. Intraday bias is turned back to the downside. Fall from 1.2919 should target a test on 1.2061 low. On the upside, however, break of 1.2390 resistance will indicate near term bottoming. That would be accompanied by bullish convergence condition in 4 hour MACD.

In the bigger picture, rebound from 1.2061 is likely completed completed at 1.2919, rejected by 55 week EMA and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

Dollar Weakens ahead of FOMC, Canadian Dollar Jumps after GDP

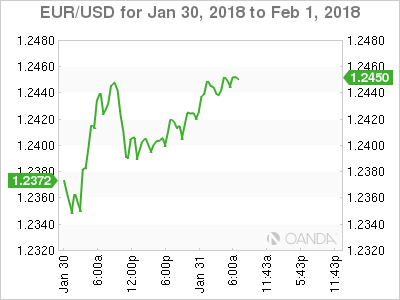

Dollar weakens broadly in early US session despite solid employment data. In particular, USD/CAD leads the way with Canadian GDP meeting forecasts. The greenback will look into Janet Yellen's last FOMC announcement today. But it's unlikely for Dollar to get any support from there. The key level to watch is 1.25 handle in EUR/USD. It's close to 1.2494/2516 cluster fibonacci level. A firm break there would likely prompt broad-based selloff in Dollar.

US ADP report showed 234k growth in private sector jobs in January, versus expectation of 183k. Employment cost index rose 0.6% in Q4, meeting consensus. From Canada, GDP grew 0.4% mom in November, meeting forecasts. IPPI dropped -0.1% mom in December while RMPI dropped -0.9% mom.

It is widely expected that no change would be made in Yellen's last FOMC meeting as Fed chair. The market focus is on the Fed's economic outlook and whether there are hints on the rate hike path. Notwithstanding the fact that inflation has remained soft, the robust employment market, with unemployment rate below the Fed's long-term target, should have anchored the Fed's confidence over the economic outlook. Fed could make an hawkish tweak in the statement the pave the rate for a March hike. Fed fund futures are already pricing in over 70% chance of that.

ECB Coeure: Not going to be too hasty on stimulus exit

ECB Executive Board member Benoit Coeure said today that the asset purchase program "of course will not last forever". But he emphasized that "there is also a very wide agreement in the Governing Council ... that we have to be patient and prudent because we are not yet where we want to be in terms of inflation." He added that "we are not going to be too hasty". Also, there were speculations that ECB could be soon ready to tweak its communications. But Coeure said that "we are having a discussion on having a discussion" only and "its meta monetary policy".

Release from Eurozone, CPI slowed to 1.3% yoy in January, down from 1.3% yoy and met expectation. CPI core rose to 1.0% yoy, up from 0.9% yoy, also met expectations. Eurozone unemployment rate was unchanged at 8.7% in December. Germany unemployment dropped -25k in January versus expectation of -20k. Germany retail sales dropped -1.9% mom in December, versus expectation of -0.4% yoy.

Also from Europe, Swiss UBS consumption indicator rose 0.2 to 1.69 in December. UK Gfk consumer confidence rose to -9 in January. BRC shop price index dropped -0.5% yoy in January.

Australia CPI picked up but missed expectations

Australia CPI accelerated to 1.9% yoy in Q4, up fro Q3's 1.8 yoy. However, this came in weaker than expectations of 2.0% yoy. On RBA's other inflation measures, the trimmed mean CPI stayed unchanged at 1.8%, missing consensus of 1.9%. The weighted median CPI rose to 2.0% from 1.9% in the third quarter. This exceeded expectations of 1.9%. The set of inflation data gives no pressure for RBA to hike any time soon. And indeed, recent rally in Aussie's exchange rate could give some downward pressure to inflation in near term ahead. And, there is still a lack of evidence of pick up in wage growth.

China manufacturing PMI slipped to 51.3

From China, official manufacturing PMI slipped -0.3 point to 51.3 in January, comparing to consensus of 51.5. Non-manufacturing PMI added 0.3 point to 55.3, beating expectations of 55. Note the government's PMI estimates cover large corporations while the one compiled by Caixin/ Markit covers medium to small firms. Traders should interpret China's economic data with caution as the accuracy is under question. HSBC complained about the country's lack of transparency and withdrew from being the partner of Markit in compilation of China's PMI data in 2015. Meanwhile, several provincial and local governments including Inner Mongolia and Tianjin have admitted exaggerating the economic data earlier this month.

BoJ Iwata: Some distance to 2% inflation

BoJ Deputy Governor Kikuo Iwata said today that the "powerful" monetary easing should be maintained. He noted "the economy is expanding moderately but prices remain weak." And, "there's some distance to 2 percent inflation." And he called for "government steps, as well as appropriate monetary policy, are necessary to achieve price stability with sustained economic growth." BoJ released summary of opinions from the January meeting. One member said that recent surge in market expectation of stimulus exit would be "undesirable".

Released from Japan, consumer confidence was unchanged at 44.7 in January. Housing starts dropped -2.1% yoy in December. Industrial production rose 2.7% mom in December.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2304; (P) 1.2341; (R1) 1.2375; More...

USD/CAD drops to as low as 1.2246 so far and break of 1.2281 indicates fall resumption. Intraday bias is turned back to the downside. Fall from 1.2919 should target a test on 1.2061 low. On the upside, however, break of 1.2390 resistance will indicate near term bottoming. That would be accompanied by bullish convergence condition in 4 hour MACD.

In the bigger picture, rebound from 1.2061 is likely completed completed at 1.2919, rejected by 55 week EMA and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Dec P | 2.70% | 1.50% | 0.50% | |

| 00:01 | GBP | GfK Consumer Confidence Jan | -9 | -13 | -13 | |

| 00:01 | GBP | BRC Shop Price Index Y/Y Jan | -0.50% | -0.40% | -0.60% | |

| 00:30 | AUD | CPI Q/Q Q4 | 0.60% | 0.70% | 0.60% | |

| 00:30 | AUD | CPI Y/Y Q4 | 1.90% | 2.00% | 1.80% | |

| 00:30 | AUD | CPI RBA Trimmed Mean Q/Q Q4 | 0.40% | 0.50% | 0.40% | |

| 00:30 | AUD | CPI RBA Trimmed Mean Y/Y Q4 | 1.80% | 1.90% | 1.80% | |

| 00:30 | AUD | CPI RBA Weighted Median Q/Q Q4 | 0.40% | 0.50% | 0.30% | |

| 00:30 | AUD | CPI RBA Weighted Median Y/Y Q4 | 2.00% | 1.90% | 1.90% | |

| 01:00 | CNY | Manufacturing PMI Jan | 51.3 | 51.5 | 51.6 | |

| 01:00 | CNY | Non-manufacturing PMI Jan | 55.3 | 55 | 55 | |

| 05:00 | JPY | Consumer Confidence Jan | 44.7 | 44.9 | 44.7 | |

| 05:00 | JPY | Housing Starts Y/Y Dec | -2.10% | 1.10% | -0.40% | |

| 07:00 | EUR | German Retail Sales M/M Dec | -1.90% | -0.40% | 2.30% | |

| 07:00 | CHF | UBS Consumption Indicator Dec | 1.69 | 1.67 | 1.73 | |

| 08:55 | EUR | German Unemployment Change Jan | -25K | -20K | -29K | |

| 08:55 | EUR | German Unemployment Claims Rate Jan | 5.40% | 5.40% | 5.50% | |

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 8.70% | 8.70% | 8.70% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan A | 1.00% | 1.00% | 0.90% | |

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Jan | 1.30% | 1.30% | 1.40% | |

| 13:15 | USD | ADP Employment Change Jan | 234K | 183K | 250K | 242K |

| 13:30 | USD | Employment Cost Index Q4 | 0.60% | 0.60% | 0.70% | |

| 13:30 | CAD | GDP M/M Nov | 0.40% | 0.40% | 0.00% | |

| 13:30 | CAD | Industrial Product Price M/M Dec | -0.10% | 0.00% | 1.40% | |

| 13:30 | CAD | Raw Materials Price Index M/M Dec | -0.90% | -2.50% | 5.50% | |

| 14:45 | USD | Chicago PMI Jan | 64 | 67.6 | ||

| 15:00 | USD | Pending Home Sales M/M Dec | 0.50% | 0.20% | ||

| 15:30 | USD | Crude Oil Inventories | 0.1M | -1.1M | ||

| 19:00 | USD | FOMC Rate Decision | 1.50% | 1.50% |

Fed Statement Eyed In Yellen’s Final Meeting

US Markets Bounce Back From Tuesday's Month-End Sell-Off

US equity markets are seen opening a little higher on Wednesday, reversing part of Tuesday's declines ahead of the first Federal Reserve interest rate announcement of the year.

US stocks came under pressure on Tuesday but with month end fast approaching and indices having recorded around 7% gains this month, as of last week's close, it's likely that much of this was driven by some rebalancing, rather than being a sign that investors are less bullish. It will be interesting to see how markets trade in the coming days but I don't expect this to be the start of a broader decline.

As is the case for much of the week, there's plenty for investors to focus on today. Donald Trump's first State of the Union address offered little for markets to get excited about, with the President instead taking to opportunity to showcase the triumphs of his first year in charge. This is broadly in line with expectations heading into the event itself and so investors now move on to the next of the week's key events.

Fed Statement Key in the Absence of Press Conference

The Fed monetary policy meeting will be the first of the new year and the last under the leadership of Janet Yellen, who will be replaced as Chair by Jerome Powell. Bearing that – and the fact that the central bank raised interest rates at the last meeting in December – in mind, we're not expecting any changes today, but we may get some insight into whether the new tax reforms have altered the views of policy makers.

Of course, in the absence of a press conference with the Fed Chair, we'll have to rely on the accompanying statement to provide fresh insight, at least until the minutes are released in a few weeks. A slight change in the statement can get quite a reaction in the markets though so traders as ever will be looking for any signs that future rate hikes are under-priced, given the recent changes.

ADP Number and Earnings Also in Focus

Ahead of the central bank announcement, we'll get some employment data from ADP which comes ahead of Friday's jobs report. The ADP is seen as being indicative of the official Non-Farm Payrolls figure but in reality that is often not the case. Still, traders will be looking for signs that market expectations for January are way off the mark and so it always has the potential to move things in the markets.

There's also a lot of companies reporting fourth quarter earnings today – including 34 from the S&P 500 and two from the Dow – which will be of interest to investors and could have an impact on overall market sentiment. Once again though, with it being the final trading day of the month, equity markets may not move entirely rationally today.

Canadian Dollar Improves, GDP Next

The Canadian dollar has posted slight losses in the Wednesday session. Currently, the pair is trading at 1.2281, down 0.45% on the day. On the release front, Canada releases GDP for December, which is expected to climb to 0.4%. Canada will also release an important inflation indicator, the Raw Materials Price Index. The markets are braced for a sharp drop of 2.2%. In the US, the markets will get a good look at employment numbers, starting with ADP Nonfarm Employment Change. The indicator is expected to slow to 186 thousand. The Federal Reserve will release a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%. On Thursday, the US publishes unemployment claims and the ISM Manufacturing PMI.

The latest round of negotiations over NAFTA ended in Montreal last week, and there were no breakthroughs. Still, the sides continue to talk, and a Merrill Lynch has lowered the odds of the US leaving the pact to 25 percent. The US has demanded far-reaching concessions from Canada and Mexico, such as shifting more auto production to the US. Canada and Mexico are strongly opposed to the US demands, but both economies would take a sharp hit if NAFTA is terminated. At the same time, many US businesses don't want to blow up NAFTA and are pressuring President Trump to remain in the trade pact. The next round of negotiations is scheduled for late February in Mexico.

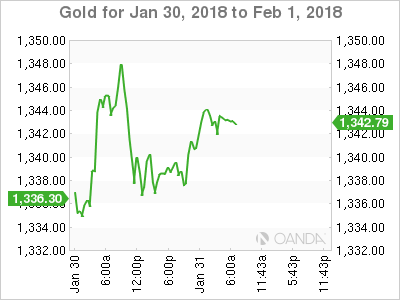

All eyes are on the Federal Reserve, which will make a rate announcement on Wednesday, the final one under Janet Yellen's watch. The tone of the rate statement could affect investor sentiment and have an impact on gold prices. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.

Dollar Pressured ahead of Fed Rate Decision; European Stocks Rebound

Here are the latest developments in global markets:

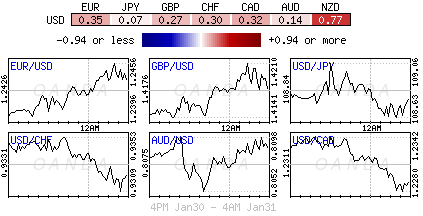

FOREX: Kiwi/dollar remained the biggest winner in early European trading, approaching fresh one-week highs at 0.7400 (+0.94%), while aussie/dollar reached an intra-day high at 0.8109. Dollar/yen inched up to 108.76 but was unable to recover earlier losses despite the BOJ increasing its medium-term Japanese government bonds. Trump's State of Union speech also failed to feed dollar bulls, giving few details on US policies. The dollar index was moving sideways around three-year lows at 88.90 (-0.29%). Euro/dollar changed hands at 1.2450 (+0.40%), showing little reaction to Eurozone's core CPI inflation which came in better than expected. Pound/dollar erased today's gains, falling back to 1.4144. Yesterday, comments by the BOE Governor Mark Carney signaled that the BOE could raise rates faster than previously thought to mitigate inflation. Dollar/loonie retreated to a two-week low of 1.2271 (-0.38) ahead of the Canadian GDP growth figures.

STOCKS: European stocks recovered after holding onto losses the last two days as investors remained optimistic on European markets amid a strong start in the new year. The benchmark European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.06% at 1100 GMT. The German DAX 30 improved by 0.17%, the French CAC 40 gained 0.24% and the British FTSE 100 was steady.

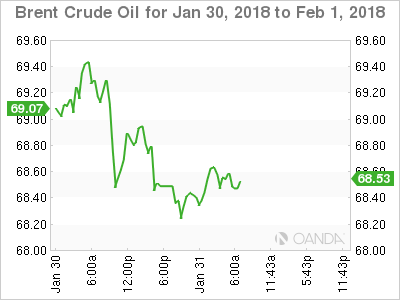

COMMODITIES: Oil prices were on the backfoot for the third day but were on track to post gains for the fifth month in a row. The market weakened as recent stats showed that US rig counts increased amid rising oil prices, threatening to disturb the OPEC-led supply cuts. WTI crude oil retreated by 0.54% to $64.15 per barrel and Brent fell by 0.64% to $68.58 per barrel. Gold was last seen at $1343.30 per ounce, gaining 0.35% in the day.

Day ahead: Fed policy meeting concludes; Canadian GDP growth in focus

US and Canadian data will dominate the economic calendar in the remaining of the day, while the outcome of the Fed's two-day policy meeting will be closely scrutinized by investors.

Fed policymakers are anticipated to announce their decision on interest rates and provide a monetary policy statement today at 1900 GMT, with markets widely expecting the central bank to keep its fund rates unchanged and probably hint that more stimulus reduction is on the way during the year. Note that this is the last meeting for Janet Yellen who was the head of the Fed for the last four years, as Jerome Powell has been officially appointed to take over in February.

In terms of data out of the US, the ADP Research Institute will give an early indication on national employment ahead of the government's comprehensive nonfarm payrolls due on Friday. The report which tracks employment changes only in the private sector is expected to show that 185,000 workers joined the labor market in January compared to 250,000 seen in December, hinting that Friday's nonfarm payrolls might also come lower. The report is expected to be released at 1315 GMT. Chicago PMIs for the month of January, and December's pending home sales will be also available at 1445 GMT and 1500 GMT respectively.

Canada will see the release of GDP growth readings and producer prices at 1315 GMT. Analysts forecast that the Canadian economy will expand by 0.4% m/m in November after posting no growth in October. This would be the highest growth print recorded since May. On the other hand, producer prices might show some weakness in December, declining by 0.1% after posting the biggest rate of expansion since March 2015.

In energy markets, investors will be looking forward to the EIA weekly report on the US oil inventories for the week ending January 26 (1530 GMT). Crude oil inventories are said to rise by 0.126 million barrels following ten weeks of consecutive losses. Gasoline stocks are projected to increase by a smaller amount of 1.809 billion barrels and distillate stocks to decrease by 1.454 million barrels.

In equity markets, AT&T, Boeing, Facebook, and Microsoft will be among companies releasing quarterly earnings on Wednesday.

USDJPY Selling Still Expected 108.98

The USDJPY pair remains intraday bearish while trading below the 108.98 level, further declines towards 108.25 and 107.32 seems possible.

Should the USDJPY pair start to gather bullish momentum above the 108.98 level, we may see buyers move price-action towards the 109.52 and 110.18 levels.

GBPUSD Sellers Look Towards 1.4130 Pivot

The British pound has turned sharply lower against the greenback during the European trading session, after earlier hitting 1.4214, following a dramatic rebuttal from EU officials. The GBPUSD pair has fallen back towards the 1.4130 level after European Union officials handling Brexit rejected a proposal from the United Kingdom on financial services. Moving into the U.S session, downside pressure on the pair is gathering, as overall risk-on sentiment towards the British pound is starting to wane.

The GBPUSD pair is likely to encounter a deeper sell-off below the 1.4130 level, with downside support layered at 1.4082 and 1.4024.

Should the GBPUSD pair maintain price-action above the 1.4130 level, we may see further upside towards 1.4214 and 1.4284.

EURUSD: Strengthens, Eyes At 1.2493 Zone

EURUSD: The pair was seen heading higher during early Wednesday trading session today. While it holds on to that strength, more bull pressure is likely in the days ahead. On the upside, resistance comes in at 1.2500 level with a cut through here opening the door for more upside towards the 1.2550 level. Further up, resistance lies at the 1.2600 level where a break will expose the 1.2650 level. Conversely, support lies at the 1.2400 level where a violation will aim at the 1.2350 level. A break of here will aim at the 1.2300 level. Below here will open the door for more weakness towards the 1.2250. All in all, EURUSD faces further price upside pressure.

European Stock Markets Up Slightly as Eurozone Inflation Report as Expected

The DAX and CAC indices have posted slight gains in the Tuesday session. The DAX is trading at 13,217.50, up 0.15% since the close on Tuesday. The CAC is following a similar trend, trading at 5484.90, for a 0.20% gain since the Tuesday close. The Eurozone CPI Flash Estimate ticked lower to 1.3%, its lowest level since July 2017. However, investors focused on the fact that the reading matched the forecast.

German releases continue to be sluggish this week. Retail Sales slipped 1.9%, well short of the estimate of -0.3%. It was the sharpest decline since June 2015. Preliminary CPI declined 0.7%, the weakest reading since January 2016. There was some good news, as unemployment claims dropped by 25 thousand, beating the estimate of 16 thousand. Eurozone numbers for fourth quarter 2016 remain solid, the unemployment rate has been steadily dropping, and remained at 8.7% in December, matching the forecast. On Tuesday, Preliminary Flash GDP for the fourth quarter remained unchanged at 0.6%, matching the forecast.

With eurozone inflation well under the ECB target of 2 percent, the ECB has some breathing room regarding its stimulus program (QE), which is scheduled to terminate in September. A stronger eurozone economy has raised speculation that the ECB could wind up QE and shift to normative policy, and perhaps even raise interest rates. However, ECB members have been cautious, trying to keep in check any market enthusiasm about a major change in policy. Last week, ECB President Mario Draghi went as far as saying that QE could be extended or increased if necessary.

Fed Could Signal Changes To Outlook

Wednesday January 31: Five things the markets are talking about

Month-end USD sales and event risk of today''s Fed''s interest rate decision (2 pm EDT) have seen a dramatic pick-up in realized volatility that''s given implied vols another boost this week.

Ahead of the U.S open, Euro stocks have stemmed the bleeding; Asian bourses were mixed, even as the EUR (€1.2454) and JPY (¥108.69) both climbed.

The U.S dollar has found little support from President Trumps first State of the Union address last night as his speech offered few clues on U.S policy.

At today''s FOMC meeting, officials are likely to keep interest rates steady, but they could provide clues on whether their 2018 outlook has changed amid a steadily expanding economy.

Up to now, many investors have doubted the Fed''s dot plot; initially for good reason as central-banker predictions on the pace of rate hikes were not as aggressive as Fed officials predicted. However, that was last years thinking.

In the past month, the market has gotten on board with the prospect that the Fed just might follow up last year''s three-rate hikes with three more in 2018.

Fed-fund futures now show a +36% probability that three +25 bps increases are to happen in 2018, versus +25% a month ago. Meanwhile, for just one hike it''s slumped to +10% from +23% and for two hikes dropped to +29% from +36%.

Conversely, bets have surged that three may be 'too conservative''; the probability of four rate increases is at +19%, versus +8.7% a month ago.

1. Stocks rebound, on pace for monthly gains

Global stocks and bonds mostly rebounded overnight, keeping major indexes on track for solid monthly gains.

Ahead of the U.S open, investors have been analysing President Trump''s first State of the Union address, a slew of corporate earnings and Janet Yellen''s final meeting as leader of the Federal Reserve.

In Japan, the Nikkei fell for a sixth consecutive session overnight, with most sectors in negative territory. The Nikkei was down -0.8%. The index is still up +1.5% this year, it has fallen -4.5% from the 26-year peak hit a week ago. The broader Topix has declined -1.2%.

Down-under, Aussie shares shrugged off lower oil prices and rising bond yields to end the overnight session higher as real estate stocks strengthened. The S&P/ASX 200 index gained +0.3%. In S. Korea, the Kospi climbed +0.2%.

In Hong Kong, stocks reversed earlier losses to end higher overnight, posting its best month in nearly three-years, helped by gains for financial and services firms. At close of trade, the Hang Seng index was up +0.86%, while the Hang Seng China Enterprises index rose +1.29%.

In China, stocks ended the session mixed, with the blue-chip index recouping earlier losses to close higher, aided by a bounce in real estate and consumer firms. At the close, the Shanghai Composite index was down -0.19%, while the blue-chip CSI300 index was up +0.48%.

In Europe, regional indices are trading mostly higher, rebounding from yesterday''s steep declines on the back of upbeat earnings and a small retreat in bond yields.

U.S stocks are set to open in the 'black'' (+0.3%).

Indices: Stoxx600 +0.1% at 396.6, FTSE +0.1% at 7592, DAX +0.3% at 13235, CAC-40 +0.2% at 5483 , IBEX-35 +0.2% at 10452, FTSE MIB flat at 23874 , SMI flat at 9433, S&P 500 Futures +0.3%

2. Oil drops for a third day, gold prices higher

Oil prices are under pressure for a third consecutive day, but remain on track for its biggest gain in January in five-years, and this in spite of data that shows that U.S stocks rose more than expected last week.

Brent is down -49c at +$68.43 a barrel, after touching a two-week intraday low earlier overnight. U.S West Texas Intermediate (WTI) futures are down -39c at +$64.11.

Yesterday, U.S crude fell -1.6% to close at +$64.50 a barrel, far outpacing a -0.6% drop in the price of Brent.

Note: Prices of WTI and Brent are still on track for a fifth month of gains and Brent is set for its largest percentage increase in the month of January since 2013, with a rise of +2.7%.

Providing price pressures are U.S producers increasing their rig count – energy companies added 12 oil rigs last week, the biggest weekly increase in 11 months.

A report from the API Tuesday shows that U.S crude stocks rose by +3.2m barrels last week. Expect dealers to take their cue from today''s U.S DoE report (10:30 am EDT) – the report is expected to show an increase in inventories for the first time in 11-weeks.

Ahead of the U.S open, gold prices have rebounded a tad as the U.S dollar resumes its downtrend. Spot gold is up +0.4% to +$1,342.80 per ounce.

Note: Many believe that gold bullion remains vulnerable to weakness ahead of the Lunar New Year. On Tuesday, the 'yellow'' metal touched its lowest since Jan. 23 at +$1,334.10 an ounce.

3. Sovereign yields remain elevated

U.S government bonds continue to gyrate near this weeks low prices prints, pushing sovereign yields stateside a tad higher towards their four-year high yield print.

U.S yields, in particular, have hit fresh four-year high yields this month as investors have bet on a pickup in growth and inflation following the passage of the U.S corporate tax cuts.

The great debate – the rise in U.S sovereign yields has certainly raised a number of concerns about the durability of the stock rally, while others have said that U.S corporate earnings growth looks solid enough to support further stock gains.

The Fed is expected to send an upbeat message in its statement later today as market based inflation expectations and the growth outlook have improved since the last meeting. The Fed''s 'dot plot'' forecasts three rate increases for 2018.

The odd''s for a Fed hike in March – the first meeting this year that has a press conference and fresh projections outlook, is around +70%.

The yield on U.S 10-year Treasuries fell -2 bps to +2.70%. In Germany, the 10-year Bund yield has declined -1 bps to +0.67%, the first retreat in a week, while in the U.K, the 10-year Gilt yield declined -1 bps to +1.46% and the biggest fall in a fortnight.

Note: In Japan, the Bank of Japan (BoJ) increased its purchases in 3-5 year JGB''s by +¥30B to +¥33B – the first increase in six-months.

4. Dollar on the defense

The once 'mighty'' USD remains on the back foot outright vs. G10 currency pairs and is poised to close out its worst monthly performance in 24-months.

The EUR/USD is slowly edging back towards the psychological €1.25 handle as dealers discount some disappointing Euro inflation data (see below), while believing (pricing-in) that the ECB would tighten policy aggressively down the road. The techies see €1.25 as key resistance in the short-term.

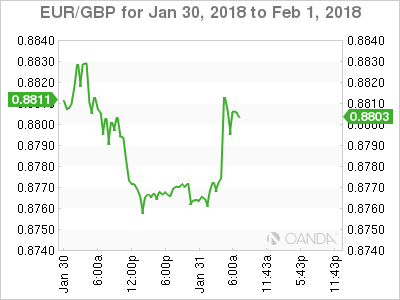

The GBP (£1.4138) trades atop of its overnight lows, mostly weighed down by report the E.U Commission officials had rejected the City of London''s proposal to strike a post-Brexit free trade deal on financial services.

USD/JPY (¥108.82) remains little changed ahead of the U.S open.

Elsewhere, South Africa''s rand (ZAR $11.8285) has gained +1% – its strongest rate outright in almost three-years.

5. Eurozone inflation continues to lag, despite robust economic growth

Despite some stellar job numbers and stronger domestic growth in Europe, data this morning once again highlights a missing ingredient in the eurozone''s expansion – an acceleration in the rate at which consumer prices are rising.

The E.U said prices were +1.3% higher in January than a year earlier, the lowest rate of annual inflation since July 2017 and well short of the ECB''s target, which is just below +2%.

Some of that decline had been expected by the ECB, since energy prices jumped at the turn into 2017, and those sharp rises have not been repeated this year.

Note: But not all of the weakness in inflation is down to energy prices. According to Eurostat, services prices rose at an annual rate of +1.2%, unchanged for four straight months. Overall, the core rate of inflation edged up to +1.0% from +0.9%.

The ECB continues to expect that inflation will eventually rise, driven in large part by a rise in wages as unemployment falls and as skilled workers become scarce.

Other data this morning showed that eurozone employment continues to run strong. In Germany, Europe''s powerhouse, January unemployment rate has hit fresh its post-unification low of +5.4%, while the eurozone matches its December 2008 lows of +8.7%.