Sample Category Title

Sunset Market Commentary

Markets:

The global core bond sell-off accelerated today. German Bunds underperformed US Treasuries. The move was mainly technical in nature. US yields pierced through key resistance levels last week (2.42% for 5y and 2.64% for 10y), creating space for further gains. Good spending/income data and in-line-with consensus PCE inflation had no specific impact. An attempt to go through similar resistance in German yields failed last week, but today's attempt succeeds. The German 2y yield moves above -0.55%, the 5y yield above -0.05% (first time in positive territory since the end of 2015) and 10y yield above 0.62%. Last week's upbeat economic assessment by the ECB and subtle hint towards a mid-2019 rate hike still resonate cross markets. Dovish comments by ECB chief economist Praet couldn't change the tide. Intraday changes on the German yield curve range between +2.2 bps (2y) and +5.5 bps (10y). US yields add 1.6 bps (2y) to 3.5 bps (10y). 10y yield spread changes vs Germany are nearly unchanged with the periphery outperforming (-4 bps).

The dollar finally bottomed at the end of last week and this process continued today. There was little highly profile news to explain the move. The laws of gravity are again weighing more on USD/JPY than on USD/EUR. There was no one-on-one link between the USD's performance and interest rate differentials. Even so, we have the impression that the environment of higher yields (with US and EMU yields breaking beyond key levels) is becoming again a bit more supportive for the USD. Investors might also turn a bit more cautious on USD shorts going into Wednesday's Fed meeting. EUR/USD trades currently in the 1.2360 area. Soft comments from ECB Praet helped the euro correction. USD/JPY underperforms other USD cross rates. The pair doesn't succeed any further gains beyond Friday's late session 'spike'.

The recent sterling rally lost momentum at the end of last week. Investors grew less convinced that Brexit negotiations could go rather smoothly. There was plenty of noise on a flaring up of internal opposition against PM May within the Conservative Party. The House of Lords also sees some 'fundamental flaws' to the UK Brexit law. EUR/GBP rebounded north of 0.88 this morning, the move was reversed later, at least partially driven by the overall correction of the euro. EUR/GBP trades little changed in the 0.8775 area. The correction of cable continues. The pair trades in the high 1.40 area (compared to a top of 1.4345 last week).

European stock markets trade flat today. Main US indices opened on a weak footing with Nasdaq underperforming after Nikkei reported, without citing anyone, that Apple notified suppliers it decided to cut iPhone X's production target for January-March period to about 20m units due to slower-than-expected sales in year-end holiday shopping season in key markets such as Europe, the US and China.

News Headlines:

US consumer spending rose at a solid pace in December (0.4%) after an upwardly revised advance a month earlier (0.8%) as shoppers splurged during the holiday season. While incomes also rose (0.3%), the saving rate fell to a fresh 12-year low. The Federal Reserve's preferred inflation gauge -- tied to consumption -- rose 0.1% in December from the previous month and 1.7% from a year earlier. Excluding food and energy, so-called core prices climbed 0.2%, matching the survey median. The core was up 1.5% from December 2016.

The ECB will only stop pumping cash into the euro zone economy when it is confident that inflation is heading towards its target even without its extra help, the chief economist Praet said. He also added the ECB had not decided yet how to end the asset purchase programme, whether gradually or at once.

EURJPY: Declines On Bear Pressure

EURJPY - The pair now looks to weaken further after it saw a move lower during Monday trading session. On the downside, support comes in at the 134.00 level where a break if seen will aim at the 133.50 level. A cut through here will turn focus to the 133.00 level and possibly lower towards the 132.50 level. On the upside, resistance resides at the 135.00 level. Further out, we envisage a possible move towards the 135.50 level. Further out, resistance resides at the 136.00 level with a turn above here aiming at the 136.50 level. On the whole, EURJPY faces further weakness threats.

Copper – Repeated Recovery Rejections Keeps the Downside Vulnerable

Copper price is struggling to hold recovery as repeated upside rejection occurred today ($3.1975) after Friday' long-legged Doji signaled that weakness from last week's high at $3.2565 might be running out of steam. Long bullish candle that was left on Wednesday after the biggest one-day rally since 16 Oct, formed bullish outside day pattern which continues to underpin, along with rising and widening daily cloud, but upside attempts so far stay under cracked pivotal barrier at $3.2384 (Fibo 61.8% of $3.3200/$3.1065 downleg). The downside is expected to remain vulnerable while the latter stays intact, with risk of retesting Friday's low ($3.1840) and further retracement of $3.1065/$3.2565 upleg on break lower. Daily MA's are in mixed setup; RSI is neutral, while momentum studies remain negatively aligned and not showing clear near-term direction. Fresh bearish signal could be expected on firm break below Friday's low ($3.1840) while sustained lift above Fibo barrier at $3.2384 will be bullish signal.

Res: 3.2132; 3.2384; 3.2565; 3.2696

Sup: 3.1932; 3.1840; 3.1638; 3.1419

US: Household Spending Capped 2017 off on a Strong Note

Personal income rose 0.4% in December, beating the consensus expectation for a 0.3% gain. Controlling for inflation and removing taxes, real disposable income rose 0.2% on the month, following a flat reading in November.

Personal spending ended 2017 on a strong note, up 0.4% in nominal terms. In real terms, spending was up 0.3%, following an even better (and upwardly revised) print of 0.8% in November (previously 0.6%).

By component, real spending on durable goods led the way, up 0.8%. Services were up 0.3%, while non-durable goods spending took a breather (effectively flat), following a 1.0% gain in November.

Prices rose 0.1% month-on-month in December, as energy prices pulled back (-1.2%). As a result, headline inflation edged down to 1.7% year-on-year (from 1.8%). Core prices firmed, rising 0.2% (m/m) in December, leaving core inflation unchanged at 1.5% year-on-year.

The personal saving rate edged down to 2.4% from a downwardly revised reading of 2.5% in November. The saving rate, while prone to revision, has only been lower in 2005, when it hit 1.9%

Key Implications

Personal spending ended 2017 on a strong note as the after effects of hurricanes helped to lift durable goods spending. While encouraging to see such a strong end to the year, spending growth has decelerated noticeably at the start of the calendar year over the past two years, part of the "residual seasonality" in real GDP growth in the quarter.

It remains to be seen whether this trend will continue in 2018, but there are mitigating factors that suggest it may not. Perhaps most important, after tax income growth will get a boost in the New Year. The cut in taxes should allow households to rebuild their saving buffer while maintaining a healthy pace of spending growth.

Inflation is still nothing to write home about, but the pickup in core price growth (up 1.9% annualized on average over the past three months) in December may give some comfort to the Federal Open Market Committee as it meets to set policy this week. The Fed is likely to remain on hold at this meeting, but a rate hike is likely coming in March at the first meeting Chaired by Jerome Powell.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.01; (P) 108.88; (R1) 109.49; More...

Intraday bias in USD/JPY is turned neutral with a temporary low in place at 108.27. Deeper fall is still expected as long as 110.18 support turned resistance holds. Break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

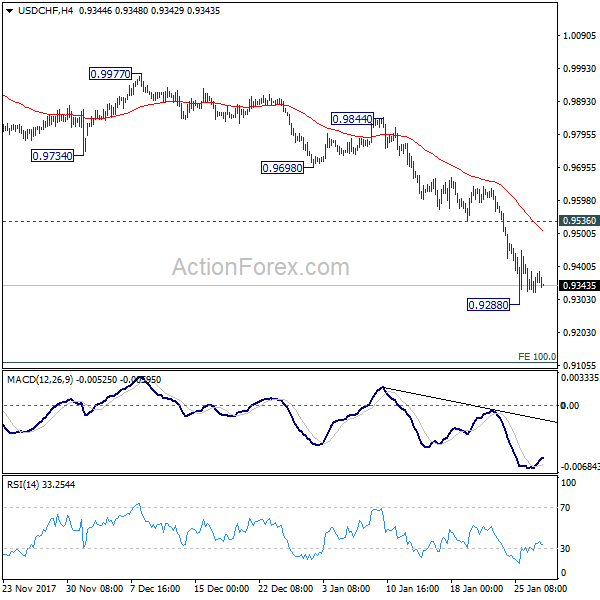

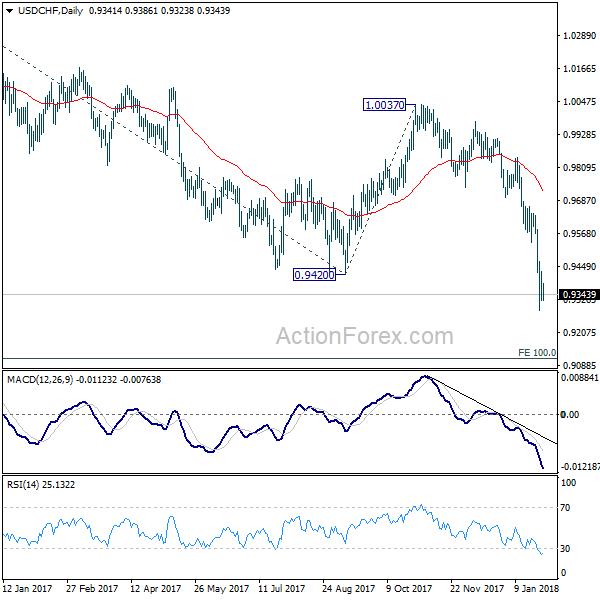

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9295; (P) 0.9360; (R1) 0.9397; More...

A temporary low is in place at 0.9288 and intraday bias is turned neutral for consolidation. But after all, near term outlook remains bearish as long as 0.9536 support turned resistance holds. Break of 0.9288 will resume the larger down trend and target next key fibonacci level at 0.9115.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

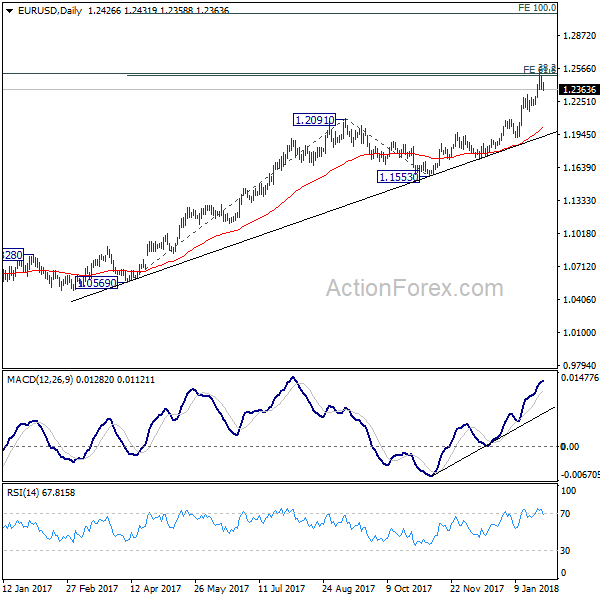

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2366; (P) 1.2430 (R1) 1.2491; More....

Intraday bias in EUR/USD remains neutral at this point but further rally is expected as long as 1.2222 support holds. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

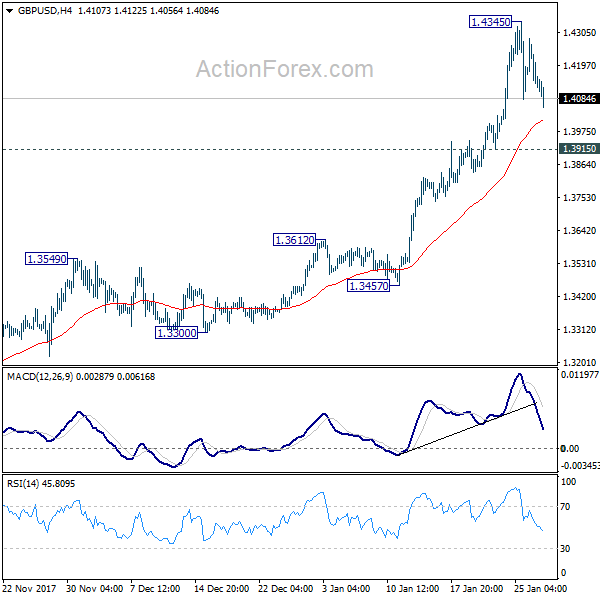

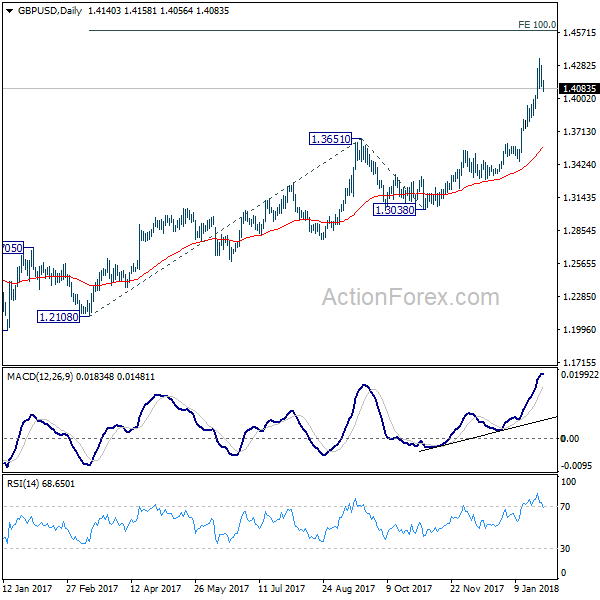

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4079; (P) 1.4180; (R1) 1.4256; More.....

GBP/USD's retreat from 1.4345 extends lower today but outlook remains unchanged. Intraday bias stays neutral and further rise is still expected with 1.3915 support intact. On the upside, break of 1.435 will extend the up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Dollar Recovery Continues, Sterling Weighed Down by Political Uncertainties

Dollar's recovery continues in early US session and is gathering some extra momentum against Sterling and Euro. But still, there is no clear indication of near term trend reversal yet. Meanwhile, Sterling is under broad based selling pressure. Profit taking after recent strong rally is one of the reasons. Additionally, the pound is weighed down by re-emerging political uncertainties in the UK. Elsewhere in the FX markets, Euro is following as the second weakest one. Kiwi and Aussie are also soft.

Release from US today, personal income rose 0.4% in December versus expectation of 0.3%. Personal spending rose 0.4%, in line with consensus. Headline PCE slowed to 1.7% yoy. Core CPI was unchanged at 1.5% yoy. Released earlier, German import price index rose 0.3% mom in December.

Sterling broadly lower on political uncertainties

Sterling tumbles broadly today on re-emergence of political uncertainties. It's reported that Prime Minister Theresa May could face another leadership challenge after the House of Lords Constitution Committee criticize3d that May's Brexit legislation had "fundamental flaws". The committee chairwoman Baroness Taylor said that "we acknowledge the scale, challenge and unprecedented nature of the task of converting existing EU law into UK law, but as it stands this bill is constitutionally unacceptable." And, there is additional complexity because "in many areas the final shape of that law will depend on the outcome of the UK's negotiations with the EU". The committee added that the method proposed to create a new category of "retained EU law" will cause "problematic uncertainties and ambiguities."

Additionally, regarding the transition deal is set to insist that UK must apply EU laws as if it were a member state during the transition period. And such compliance is expected to be unconditional. On the other hand, the UK is clearly uncomfortable with the demand. Brexit secretary David Davis hinted that he would demand the power to object. As Davis said, "means to remedy issues" are needed if laws were "deemed to run contrary to our interests". But some EU officials see the UK's position on it being counter productive, in particular as Prime Minister Theresa May is targeting to complete a transition deal in March, as businesses requested.

ECB Praet: Some distance from meeting ending QE

ECB chief economist Peter Praet sounded cautious as he pushed back the idea of ending the asset purchase program. He said that ECB is still "some distance" away from meeting the three measurements on the the program. And the three criteria are:

- Firstly, "headline inflation will have to be on course to reach levels below, but close to, 2 percent by the end point of a meaningful medium-term horizon."

- Secondly, "the Governing Council wants to be sure that the expectation of an upward adjustment in inflation has a sufficiently high probability of being realized and is being met on a sustainable basis."

- Thirdly, "if the inflation outlook is overly dependent on monetary support, the upward adjustment cannot be considered sustained. So we want to verify that the path would be maintained even in less supportive monetary policy conditions."

Praet emphasized that "the transition toward a normalization will begin once we have established that there is a sustained adjustment in the path of inflation." However, "despite the strong cyclical momentum, domestic price pressures remain subdued, as do measures of underlying inflation."

ECB Governing Council member Klass Knot delivered some hawkish comments over the weekend. He said "there is no reason whatsoever to continue" the EUR 30b a month asset purchase program after it ends in September. He added "we don't have to communicate yet that it will be over after September, but I think that's where we're headed." Meanwhile, interest rates would stay low in the coming years. Knot noted that "Interest is mainly low because there are more people that want to save, than that want to invest. This will change as the economy grows, but that will take time."

FOMC to highlight a busy week

The highlight of the coming week is the FOMC meeting. This is also the last time for outgoing Fed Chair Janet Yellen to preside the meeting. While it has been widely expected that no change would be made in the monetary policy, the market focus is on the Fed's economic outlook and whether there are hints on the rate hike path. Notwithstanding the fact that inflation has remained soft, the robust employment market, with unemployment rate below the Fed's long-term target, should have anchored the Fed's confidence over the economic outlook. We do expect the Fed to address the issue recent USD weakness. On the monetary policy outlook, the market continued to price in over 70% of a rate hike in March.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4079; (P) 1.4180; (R1) 1.4256; More.....

GBP/USD's retreat from 1.4345 extends lower today but outlook remains unchanged. Intraday bias stays neutral and further rise is still expected with 1.3915 support intact. On the upside, break of 1.435 will extend the up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | German Import Price Index M/M Dec | 0.30% | 0.20% | 0.80% | |

| 13:30 | USD | Personal Income Dec | 0.40% | 0.30% | 0.30% | |

| 13:30 | USD | Personal Spending Dec | 0.40% | 0.40% | 0.60% | 0.80% |

| 13:30 | USD | PCE Deflator Y/Y Dec | 1.70% | 1.70% | 1.80% | |

| 13:30 | USD | PCE Core M/M Dec | 0.20% | 0.20% | 0.10% | |

| 13:30 | USD | PCE Core Y/Y Dec | 1.50% | 1.50% | 1.50% |

Pound Slips as Brexit Talks Resume; Dollar Waits for PCE Inflation

Here are the latest developments in global markets:

FOREX: The dollar consolidated gains earned early in the day on the back of rising US bond yields which jumped to peaks last seen in 2014. The dollar index was trading at 89.60 (+0.22%) and dollar/yen was steady at 108.70 (+0.05%). Euro/dollar eased to 1.2397 (-0.19%) as German bonds yields continued to rise for the fourth day reaching two-year highs after the Dutch central bank said on Sunday that the ECB should be clear on its plans to end the asset purchase program in September. Pound/dollar was the worst performer, correcting lower to 1.4070 (-0.70%) in the first day of the new Brexit phase where EU foreign ministers will discuss terms regarding transition period. Although the EU leaders showed their thumbs to move Brexit talks to the next stage, some believe that the UK is not ready to complete the divorce.

STOCKS: European stocks were in the red except the British FTSE 100. The pan-European STOXX 600 was down by 0.23% at 1100 GMT unable to gain from upbeat AMS earnings results. The Austrian chipmaker AMS saw its shares surging by 17.60% after its revenues doubled in 2017 and its iPhone component supplier upgraded its growth forecasts more than expected. The blue-chip Euro STOXX 50 retreated by 0.30% weighed by losses in healthcare and consumer cyclicals. The German DAX 30 lost 0.19%, the Spanish IBEX 35 decreased by 0.32% and the French CAC 40 edged down by 0.04%. On the other hand, the UK's FTSE 100 increased by 0.20%.

COMMODITIES: Oil prices were on the backfoot as the US oil production seemed to offset OPEC-led supply cuts. WTI crude was last down by 0.50% on the day at $65.80 per barrel and Brent was weaker by 0.88% at $69.90. Gold moved up by 0.20% to $1346.40 per ounce.

Day ahead: US PCE inflation eyed; Japanese employment data due in Asian session

The dollar will remain in the spotlight during the European afternoon on Monday as inflation data and figures on consumption out of the US are expected to bring fresh volatility to the currency.

The core PCE index which excludes volatile items - the Fed's most preferred inflation measure - is expected to remain steady at 1.5% y/y in December at 1330 GMT, finishing 2017 below the Fed's target of 2.0%, while on a monthly basis, the gauge is anticipated to inch up from 0.1% to 0.2%. However, personal consumption and personal spending figures released at the same time might gather greater attention as any surprise to the upside would signal higher inflationary pressures for 2018. According to forecasts, personal income is said to grow at November's pace of 0.3% m/m, whereas personal spending is projected to slow down to 0.4% m/m from 0.6% seen in the previous month.

Later in the day, the Asian session will see the release of the Japanese household spending and employment data at 2330 GMT. While the employment stats are forecasted not to deviate much from previous prints in December, with the unemployment rate standing flat at a multi-decade low of 2.7% and the jobs to application ratio edging up to a fresh 44-year high of 1.57, household spending is seen declining on a monthly basis. Particularly the gauge might have fallen by 0.6% m/m after it surged by 2.1% in November, posting the biggest expansion since March. On an annual basis, the measure is expected to ease to 1.6%.

A few minutes later, December's Japanese retail sales might come softer at 1.8% m/m at 2350 GMT.

Beyond the above releases, the economic calendar is relatively light today with New Zealand's trade data for December gaining some interest. Those are scheduled for release at 2145 GMT.

Brexit developments will also be in focus as negotiations on transition period resume today, while discussions on other issues including trade will be in preparation.

In equity markets, corporate earnings releases will continue to keep investors busy.