Sample Category Title

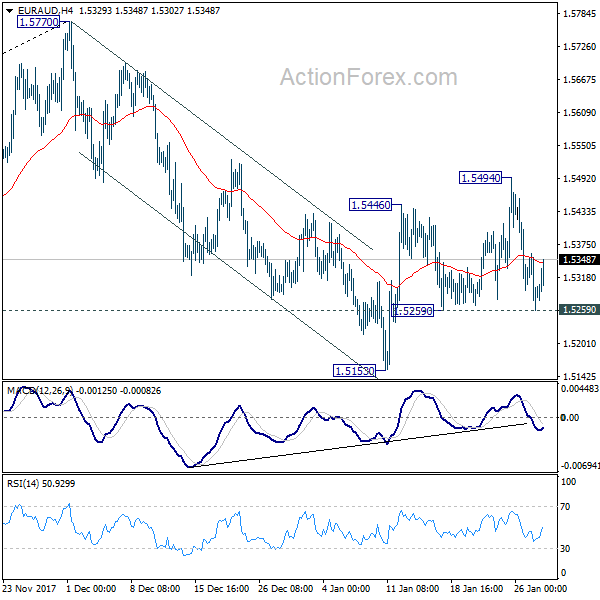

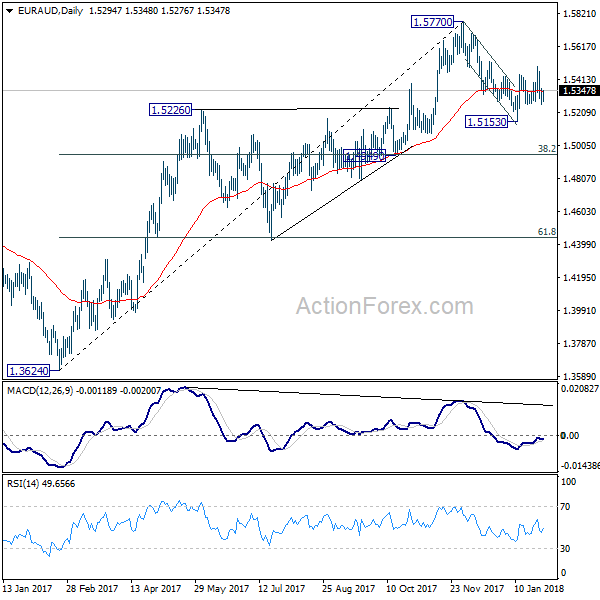

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5249; (P) 1.5303; (R1) 1.5348; More....

Intraday bias in EUR/AUD remains neutral at this point. Current development argues that fall from 1.5770 is not completed yet. On the downside, below 1.5259 will turn intraday bias to the downside for 1.5153. Break will target 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950).

In the bigger picture, price actions from 1.5770 so far suggests that it's corrective in nature. That is, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

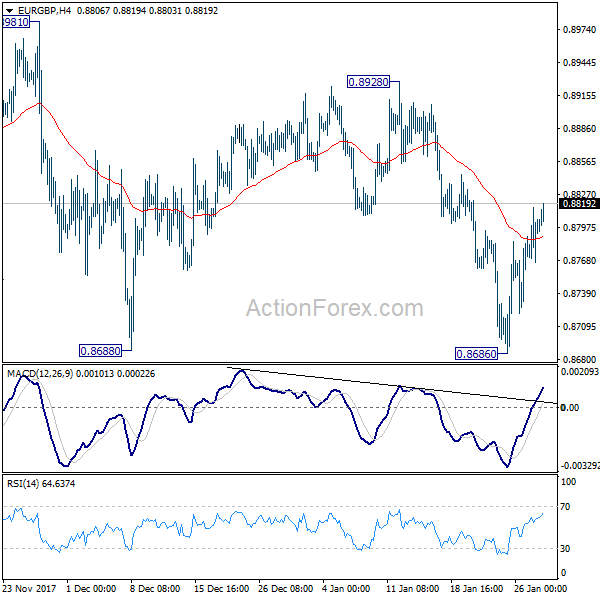

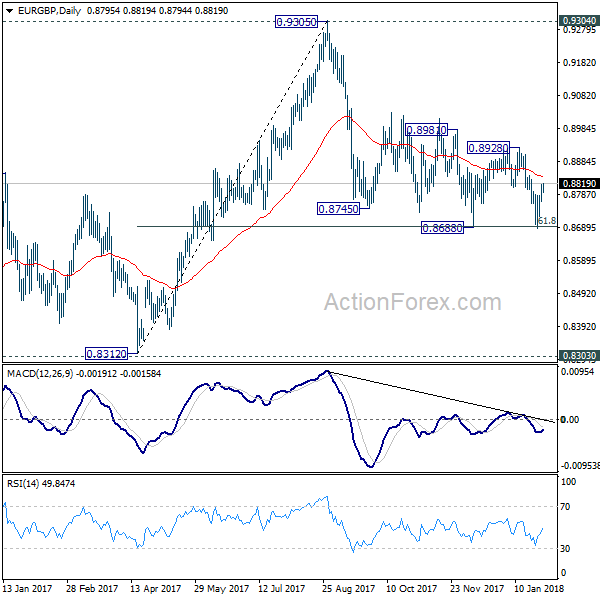

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8769; (P) 0.8793; (R1) 0.8819; More...

Rebound from 0.8686 is still in progress and further rise could be seen. But after all, near term outlook stays bearish as long as 0.8928 resistance holds and another fall is expected. Firm break of 0.8686 support will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

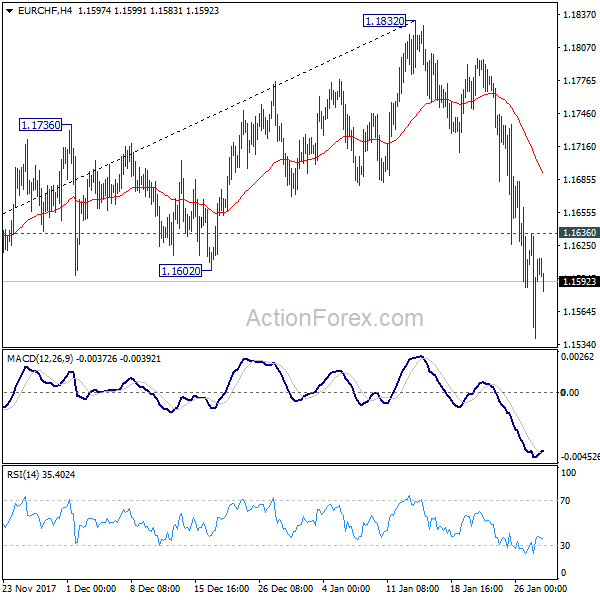

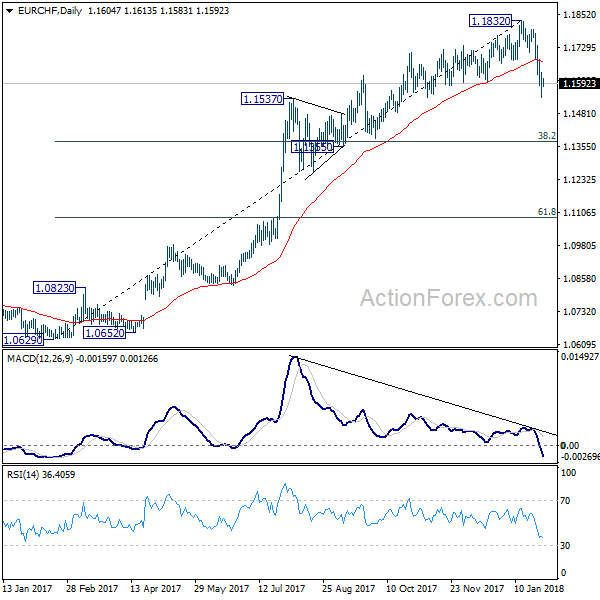

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1552; (P) 1.1595; (R1) 1.1649; More...

No change in EUR/CHF's outlook. Decline from 1.1832 is still in progress. It's seen as correcting medium term rise from 1.0629. Deeper fall would be seen to 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) On the upside, above 1.1636 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1832 resistance holds.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Daily Wave Analysis: EUR/USD, GBP/USD Break Below Shallow 23.6% Fibonacci

Currency pair EUR/USD

The EUR/USD continued with building a bearish retracement as part of a potential wave 4 (purple). Price has slightly broken below 23.6% Fibonacci level of wave 4 vs 3, which could still act as a support level. But a full bearish breakout could indicate that deeper Fibs like the 38.2% and 50% might act as targets if price does break.The Fib levels could be potential bouncing zones too.

The EUR/USD is building a bearish channel which could be part of a corrective ABC (blue) pattern. A break above the resistance (red) could mark the continuation of the uptrend whereas a bearish break could see price continue with the bearish channel.

Currency pair GBP/USD

The GBP/USD has broken below the support trend line (dotted blue), which could be an expansion of a bearish retracement within potential wave 4 (green). A break below the 50% Fib pf wave 4 vs 3 makes a wave 4 unlikely. The continuation of the uptrend seems likely if price is able to break above the resistance trend line (red).

The GBP/USD broke below the support trend line (dotted blue) and could be ready to challenge deeper Fibonacci level such as the 38.2%. A break above the resistance trend lines (red) could indicate an uptrend continuation.

Currency pair USD/JPY

The USD/JPY remains in a downtrend but price is close to a strong support zone (green line) from the daily chart.

The USD/JPY is in a triangle chart pattern. A bullish break above the pattern could indicate the end of the downtrend whereas a break below the support zone (horizontal green) could indicate a continuation of the downtrend.

Market Update – Asian Session: Dollar Remains At Multi-Year Lows, Bond Yield Higher With Equities Cautious Ahead Of FOMC

Headlines/Economic Data

General Trend: Asian equities trade generally lower following negative leads out of the US

Energy shares underperform vs outperformance seen on Monday

Japan Dec Jobless Rate rises for the first time since May 2017; job-to-applicant ratio highest since Jan 1974

US Treasury Futures extend losses during Asian session

PBoC sets yuan weaker for first time in 8 sessions

Japan

Nikkei 225 opened -0.3%; closed -1.4%

TOPIX Securities Index -1.2%, Electric Appliances -1.7%

Hitachi Metals [5486.JP]: Declines over 5% (9-month profits declined y/y)

Fuji Electric [6504.JP]: Trades lower by over 1% (affirmed FY net profit forecast)

Hitachi Construction [6305.JP]: Gains over 7% (Raised FY18 guidance)

Canon Electronics [7739.JP]: Gains over 9% (FY profit rose by ~38%)

(JP) Japan's Topix passes 1,900 for the first time since 1991

(JP) Japan Dec Overall Household Spending Y/Y: -0.1% v 1.5%e

(JP) JAPAN DEC JOBLESS RATE: 2.8% V 2.7%E; JOB-TO-APPLICANT RATIO: 1.59 (highest since Jan 1974) V 1.57E

(JP) Japan PM Abe Adviser Hamada: Yen could 'firm' in short-term on factors such as US currency policy

(JP) Japan Econ Min Motegi: Will closely watch FX rates as they have impact on Japan economy

(JP) Japan Fin Min Aso: Coincheck event is very regrettable; if needed authorities will search crypto exchanges

(JP) JAPAN DEC RETAIL SALES M/M: +0.9% V -0.2%E; RETAIL TRADE Y/Y: 3.9% V 2.2%E

JSR, 4185.JP Reports 9M Net ¥27.7B v ¥22.3B y/y; Op ¥37.2B, 44.5% y/y; +14.4%

(JP) Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.10% (prior 0.10%) 2-yr JGBs; avg yield -0.130% v -0.136% prior; bid to cover 5.02x v 4.32x prior

(JP) Japan 10-yr JGB yield trades above 0.09% (highest since July)

Looking Ahead: Japan Dec Prelim Industrial Production due on Wednesday, along with comments from BoJ official Iwata

Korea

Kospi opened -0.3%

Chipmakers trade broadly lower: Hynix and Samsung Electronics decline over 2%

(KR) South Korea customs data shows washing machine exports have nearly halved over the past 5-yrs; with more declines likely from new US safeguard measures -

Korean press

(KR) According to Korea Financial Investment Association, the Korea stock market has seen the number of participants pass 25M for the first time - Korean press

(KR) South Korea Feb Business Manufacturing Survey: 77 v 82 prior; Non-Manufacturing Survey: 78 v 78 prior

Samsung, LG open new logistics facilities in US over safeguard measures - Korean press

(KR) South Korea Dec Department Store Sales y/y: 3.2% v 8.5% prior; Discount Store Sales y/y: 2.2% v 0.0% prior

(KR) North Korea armed forces have reportedly scaled back their winter military exercises due to shortages of fuel and food - press

Looking Ahead: South Korea Dec Industrial production due for release on Wed

China/Hong Kong

Hang Seng opened -0.7%, Shanghai Composite -0.3%

Hang Seng Materials Index -2.6%, Energy -2.5%, Info Tech -1.5%, Financials -1.4%, Property/Construction -0.9%

Wynn Macau, 1128.HK Forms special committee following recent sexual misconduct allegations related to Steve Wynn; -5.5% (declined 6.5% Monday)

(CN) Some China banks said to have been ordered to curb overnight lending - Chinese press

(CN) China Premier Li: China will properly manage the timing, pace and intensity of macroeconomic controls to achieve higher quality growth – CD

(CN) PBoC: Skips OMO (4th straight session) v skipped prior; Net drain CNY240B v CNY140B drain prior

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3312 V 6.3267 PRIOR (1st weaker setting in 8 sessions)

(CN) China targeting to meet crude steel capacity cut target early

(CN) China province of Shanxi (2nd largest coal producer) has asked coal miners to shorten or eliminate Spring Festival holiday - press

Looking Ahead: China Jan Official Manufacturing and Non-Manufacturing PMIs due on Wed

Australia/New Zealand

ASX 200 opened -0.1%; closed -0.9%

ASX 200 Energy Index -1.3%, Resources -1.4%, Utilities -1%, Financials -0.6%

(NZ) NEW ZEALAND DEC TRADE BALANCE (NZD): +640M V -125ME; YTD -2.84B V -3.44BE

Fortescue, FMG.AU Reports Q2 ore mined 47.5 Mt v 50.1 Mt y/y; ore shipped 40.5 Mt v 42.2 Mt y/y

Village Roadshow, VRL.AU Reports H1 substantially lower y/y

Looking Ahead: Australia Q4 CPI due for release on Wed

(AU) Wholesale energy prices more than doubled in last 12 months in Victoria and S. Australia - AMEO data

(NZ) S&P affirms New Zealand sovereign rating at AA; outlook stable

Other Asia

(PH) Philippines Central Bank Gov Espenilla: Peso is broadly stable over medium term

(TH) Thailand Central Bank: GDP may grow 4% in 2018; interest rate to remain accomodative to help economy

North America

US equity markets ended broadly lower: Dow -0.7%, S&P500 -0.7%, Nasdaq -0.5%, Russell 2000 -0.6%

S&P500 Energy Sector -1.5%, Utilities -1.3%, Real Estate -1.2%

Maxim Integrated Products [MXIM]: Declines over 8% in the afterhours, as Japan’s Renesas denied media report related to $20B merger.

MetLife [MET]: Declines over 6% in the afterhours: Reports prelim Q4 $0.61-0.66 v $1.10e; discovered material weakness in internal control over financial reporting; to see $135-165M FY17 net income impact; to increase reserves by $525-575M; to postpone earnings

Thomson Reuters [TRI] Confirms Advanced Discussions with Blackstone Regarding Financial & Risk (F&R) Business; no terms disclosed yet

Callidus Software [CALD]: To be acquired by SAP for $36.00/shr for $2.4B (~10% premium to closing price)

(US) FBI Deputy Director McCabe reportedly plans to step down effective today, sooner than expected - NBC News

(US) Treasury Sec Mnuchin comments before Tuesday's Senate Banking Committee Testimony: Reiterates Treasury can fund government into Feb

(US) Treasury quarterly financing estimates: to borrow $441B in Jan-Mar quarter (v $512B prior projection); Treasury to borrow $176B in Apr-Jun quarter; Treasury borrowed $282B in Oct-Dec quarter v $275B estimate

Looking Ahead: Weekly US API Crude Oil Inventories due for release

Corporate earnings are expected from companies including AK Steel, AMD, Aetna, Corning, Electronic Arts, Harley-Davidson, Juniper, McDonald’s, Pfizer, Robert Half

Europe

(EU) Reportedly ECB officials are assuming the QE program will wind down over about 3 months (rather than suddenly halting the program); Even the hawkish members of the council are said to support a short taper period rather than a sudden halt to QE ; There has still not been a decision made on QE after the nominal end date in Sept - press

(UK) EU Chief Brexit Negotiator Barnier: EU institutions and govts are united in Brexit talks; Brexit transition to take 21 months

(UK) PM May spokesperson: "there remains some distance" between the UK and EU on more than one issue over the UK's transition deal - Sky News

(UK) Unreleased UK Brexit analysis: UK would be worse off outside the EU under every scenario modeled - Buzzfeed

(UK) Moody's: UK corporate credit quality to remain stable in 2018 despite Brexit uncertainty

(DE) Germany govt to raise 2018 GDP forecast to 2.4% from 1.9% prior - press

Luxottica [LUX.IT]: Reports Q4 Rev €2.09B v €2.07Be

Telecom Italia [TIT.IT]: CEO expected to announce plan for network spin off proposal on Monday

Looking Ahead: Euro Zone Q4 prelim GDP and Germany Jan Prelim CPI due for release

Levels as of 01:00ET

Nikkei225 -1.4%, Hang Seng -1.0%; Shanghai Composite -0.6%; ASX200 -0.9%, Kospi -1.1%

Equity Futures: S&P500 -0.5%; Nasdaq100 -0.7%, Dax -0.7%; FTSE100 -0.5%

EUR 1.2388-1.2361; JPY 109.20-108.66; AUD 0.8100-0.8066;NZD 0.7338-0.7314

Feb Gold -0.4% at $1,334/oz; Mar Crude Oil -1.0% at $64.88/brl; Mar Copper -0.9% at $3.17/lb

Elliott Wave View: DXY In Double Correction

DXY Dollar Index Short Term Elliott Wave view suggests that decline to 88.44 ended Intermediate wave (3). Up from there, Intermediate wave (4) bounce is unfolding as a double three Elliott Wave structure where Minor wave W ended at 89.58 and Minor wave X ended at 88.723. Minor wave Y is in progress with Minute wave ((w)) ended at 89.619 and while Minute wave ((x)) pullback stays above 88.723, Index should extend higher in Minute wave ((y)) of Y towards 89.88 – 90.59 area. The rally should also complete Intermediate wave (4) and Index should then resume the decline lower or at least pullback in 3 waves. We don’t like buying the proposed bounce and expect sellers to appear in the above area for at least a 3 waves pullback.

DXY 1 Hour Elliott Wave Chart

Australia’s NAB Business Confidence Index Hit 5-Month High In December

For the 24 hours to 23:00 GMT, the AUD rose 0.06% against the USD and closed at 0.8093.

LME Copper prices declined 0.02% or $1.5/MT to $7062.0/MT. Aluminium prices rose 0.6% or $13.5/MT to $2251.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.8085, with the AUD trading 0.1% lower against the USD from yesterday's close.

Overnight data showed that Australia's NAB business confidence index advanced to a level of 11.0 in December, surging to its highest level since July 2017, suggesting that the economic outlook remains bright for the business sector. In the prior month, the index had recorded a revised level of 7.0. Moreover, the nation's NAB business conditions index remained unchanged at a level of 13.0 in December.

The pair is expected to find support at 0.8067, and a fall through could take it to the next support level of 0.805. The pair is expected to find its first resistance at 0.8104, and a rise through could take it to the next resistance level of 0.8124.

Going ahead, traders would look forward to Australia's consumer price index for 4Q, scheduled to release overnight.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average

Euro Trading A Tad Lower, Ahead Of The Euro-Zone’s GDP Data

For the 24 hours to 23:00 GMT, the EUR declined 0.12% against the USD and closed at 1.2384.

On the economic front, Germany's import price index rose 1.1% YoY in December, in line with market expectations and compared to an advance of 2.7% in the prior month.

Macroeconomic data showed that personal spending in the US grew 0.4% on a monthly basis in December, meeting market estimates and after recording a revised gain of 0.8% in the previous month. Moreover, the nation's personal income climbed more-than-anticipated by 0.4% on a monthly basis in December, while markets were expecting for an increase of 0.3%. Personal income had registered a rise of 0.3% in the prior month.

Other data revealed that the Dallas Fed manufacturing business index registered an unexpected rise to a level of 33.4 in January, notching a more than 12-year high level and confounding market expectations for a drop to a level of 25.4. In the previous month, the index had registered a level of 29.7.

In the Asian session, at GMT0400, the pair is trading at 1.2378, with the EUR trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.2334, and a fall through could take it to the next support level of 1.2289. The pair is expected to find its first resistance at 1.2426, and a rise through could take it to the next resistance level of 1.2473.

Trading trend in the Euro today is expected to be determined by the release of the Euro-zone's flash 4Q GDP numbers as well as Germany's consumer price inflation data for January, both scheduled to release in a few hours. Additionally, the US consumer confidence index for January, due to release later in the day, would garner significant amount of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Pound Trading On A Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.33% against the USD and closed at 1.4075, as reports about political divisions on Brexit sparked uncertainty over whether the UK Prime Minister, Theresa May would be able to clinch a divorce deal with the European Union.

In the Asian session, at GMT0400, the pair is trading at 1.4056, with the GBP trading 0.13% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.4005, and a fall through could take it to the next support level of 1.3955. The pair is expected to find its first resistance at 1.4127, and a rise through could take it to the next resistance level of 1.4199.

Going ahead, investors would focus on UK’s net consumer credit and mortgage approvals data, both for December, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japan’s Jobless Rate Unexpectedly Ticked Up In December

For the 24 hours to 23:00 GMT, the USD rose 0.08% against the JPY and closed at 108.95.

In the Asian session, at GMT0400, the pair is trading at 108.83, with the USD trading 0.11% lower against the JPY from yesterday's close.

Overnight data indicated that Japan's unemployment rate unexpectedly rose to 2.8% in December, defying market expectations for a steady rate of 2.7%.

On the other hand, the nation's seasonally adjusted retail trade surprisingly climbed 0.9% on a monthly basis in December, against market anticipation for a fall of 0.4%. Retail trade had risen by a revised 1.8% in the previous month. Also, the nation's large retailers' sales jumped 1.1% in December, beating market estimates for a gain of 0.5% and compared to an increase of 1.4% in the preceding month.

The pair is expected to find support at 108.57, and a fall through could take it to the next support level of 108.32. The pair is expected to find its first resistance at 109.14, and a rise through could take it to the next resistance level of 109.46.

Going forward, the Bank of Japan's (BoJ) summary of opinions report from its January meeting as well as Japan's flash industrial production data for December, set to release overnight, would be on investors' radar.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.