Sample Category Title

Technical Outlook: EURUSD Stands At The Back Foot Ahead Of EU Data

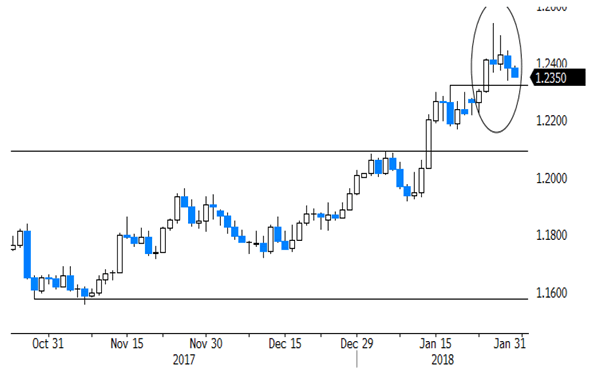

The Euro remains in red on Tuesday and probes again through cracked daily Tenkan-sen (1.2351), looking for retest of Monday’s spike low at 1.2336 and attack at rising 10SMA at 1.2316.

Studies on lower timeframes are in negative setup and point to the downside. Also, daily RSI reversed from overbought zone and supports scenario.

Violation of stops below 1.2300 would trigger fresh weakness, but extended dips should hold above rising 20SMA (1.2193) to keep overall bulls intact for renewed attempts through 1.25 barrier.

Release of EU Q4 GDP and German inflation data are key events for the Euro today.

The bloc’s economic growth remains steady and is expected rise by 2.7% Y/Y in the fourth quarter from 2.6% in Q3.

Solid GDP data today (at/above forecast) would inflate the Euro and reduce current downside risk.

On the other side, inflation in Germany is expected to dip in January (-0.5% f/c vs 0.6% previous month).

The performance of US dollar is closely watched as the greenback holds in near-term recovery mode off fresh three-year lows and after being shaken by conflicting comments from top US officials last week in economic forum in Davos.

President Trump’s State of the Union speech due in early hours on Wednesday and the outcome of Fed two day policy meeting will be closely watched for fresh signals.

Res: 1.2388, 1.2432, 1.2493, 1.2537

Sup: 1.2316, 1.2300, 1.2253, 1.2193

Ugly Sell Off Picture Spook Investors | Gold Down While Dollar Up

Global bond sell off intensifies, dollar index off its low

ECB’s governing council increase hawkish talks, bullish long term outlook for euro

French GDP growth better than expectation (0.6% vs 0.5%)

Bitcoin still consolidating below 11K

Shock and horror are flashing on traders' dashboard as they start the day. Thanks to the US where we witnessed the worst bond sell off for 2018. Rising bond yield is a ticking time bomb. Expectations around higher inflation, stimulated by Trump’s tax incentive, need to be factored in. The markets have decided to wake up to this idea now because firms will be increasing wages and bonuses. Nonetheless, the bond sell-off spooked investors and it shifted their focus to VIX which surged yesterday. It is up by 25% so far this year.

Looking at the European markets and US futures, we do believe that the (bond sell-off) spill-over would continue. It appears that the chief anxiety amid investors is about rising US bond yields, a film which we have seen before. Better than expected French GDP q/q number (act 0.6%, est 0.5%) failed to offset this pessimism. Yesterday, the US 20 year bond yield jumped to it’s highest level since April 2014 and the 2-year bond yield accelerated to a level not seen since September 2008. The timing of this is important, because the Fed rate meeting is also due this week and there is a stronger probability that we may get a revision for the US economy in order to factor in the spillover effects of tax benefits.

The dollar index is the ultimate beneficiary of this as traders are staring at a true risk-off situation. The yellow metal typically jumps when volatility index explodes. The adverse risk sentiment weighing on traders, however, there is no evidence of a shift in the move towards a safe haven. The textbook trade isn’t behaving the way it does. Perhaps, this is because of the dollar strength, some investors could consider this pullback as an opportunity and they are not worried about the overall health of the economy.

While the strength in the dollar has pushed the euro lower, however, traders are going to keep a close eye on the Eurozone’s economic growth reading which may show some signs of losing steam. The expectations are for 0.6% while the previous reading was at 0.7%. Nonetheless, despite the reading of 0.6%, investors still have an optimistic picture to look at especially when they look through the lens of economic growth which has some significant meaning. We do think that the ECB’s monetary policy would anchor in the coming months because they won’t have to worry about German coalition, which is taking forever and also Italian elections would not present anything serious which they need to worry about. This would help the German bond yields to rise, and make the days of negative yield look like they never appeared.

US Dollar Rebounds As Stocks Sell Off, Flash Eurozone GDP On Tap

Here are the latest developments in global markets:

FOREX: The US dollar continued to stage a recovery during Tuesday’sAsian session against most majors with the exception of the yen. The latter currency was bid as it performed its traditional role of safe-haven. The dollar index was around 1% higher from its 3-year low hit on Thursday. Rising bond yields were said to bolster the greenback.

STOCKS: Stocks were correcting following their stellar run of the previous weeks. The Dow closed two-thirds of a percent lower on Mondayand futures were signaling a negative open for Tuesday as well. The Nikkei closed down 1.4% today and other Asian indices were also under pressure. A selloff in Apple shares on Monday and the rise in bond yields were cited as the main reasons for the pullback.

COMMODITIES: Gold fell at the same time as the US dollar recovered and yields rose. Gold fell to a 1 ½-week low of $1333 per ounce. The bounce in the dollar also pushed crude oil lower, with the US benchmark falling below $65 to $64.85. Fears about rising US production also seem to be holding back further gains by crude oil for now.

Major movers: Yen does best after stock sell-off; dollar off lows

The Japanese yen managed to strengthen during Tuesday’s trading as it attracted some safe-haven related flows. The yen’s gains were more pronounced versus the pound and to a lesser extent against the euro, whereas the Japanese currency managed to post small gains versus the greenback as the dollar recovered on the back of higher Treasury yields. In terms of Japanese data, except for retail sales, employment and household spending numbers came in on the disappointing side.

10-year US Treasury yields climbed near their highest in four years at 2.72%, as long-term interest rates in the US have risen on the back of expected Fed rate hikes, fiscal deficits and strong growth prospects for the world’s largest economy. Interestingly, German 10-year Bund yields have also risen to around 2 ½ -year highs by touching 0.70% on Monday as the ECB is increasingly expected to wind down its QE program in the coming months.

The aussie was one of the biggest losers versus the greenback – perhaps because of risk aversion and because the Australian currency was one of the best performers of 2018 and therefore would need to correct the most. The pound was in a similar position following previous strong performance as pound/dollar broke below 1.40 on the back of dollar strength and worries that UK’s Brexit-related woes would return because of unstable politics.

Finally, oil was down by around 1% but it remained close to three-year high levels.

Day ahead: Eurozone GDP, German inflation and US consumer confidence on the agenda

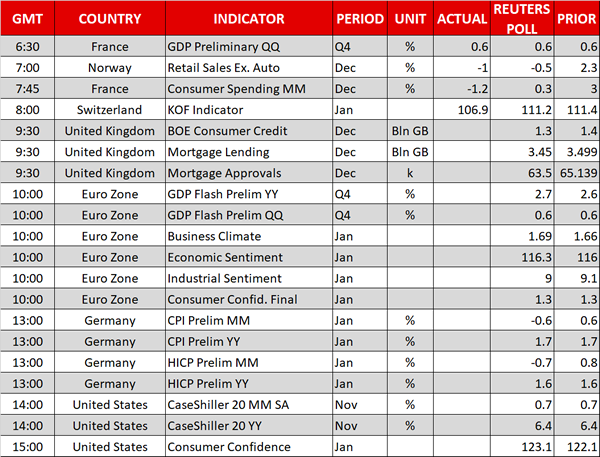

UK data on consumer credit and mortgage lending & approvals will be made public at 0930 GMT.

At 1000 GMT, the eurozone will see the release of numerous surveys gauging business and consumer sentiment, including the final reading of consumer confidence for the month of January released by the European Commission’s Directorate General for Economic and Financial Affairs. Consumer confidence is expected to be confirmed at 1.3, its highest since 2000.

Eurozone Q4 2017 flash GDP figures will also be released at 1000 GMT and are expected to attract investor interest, with a surprise potentially leading to positioning on euro pairs. Quarter-on-quarter, growth is expected to stand at 0.6%, the same as in the preceding two quarters which is considered a solid rate of expansion, while on an annualized basis, it is anticipated to come in at 2.7%, this being a multi-year high.

One day before the eurozone’s preliminary estimate of January CPI goes public, Germany, the eurozone’s – and Europe’s largest economy – will see the release of its respective inflation figures for the month of January at 1300 GMT.

Out of the US, the CaseShiller indices gauging house prices for the month of November are due at 1400 GMT, while the Conference Board’s consumer confidence index for January will be released at 1500 GMT – the relevant index is expected to rise, albeit not by much, after declining in December. It should also be mentioned that the Federal Reserve will commence its two-day meeting on monetary policy later on Tuesday, with a policy decision due on Wednesday; this will be Janet Yellen’s last meeting as Fed chief with Jerome Powell subsequently taking over. Some analysts are anticipating a “hawkish hold” of rates at current levels, with a signaling for a hike during the March meeting.

Bank of England Governor Mark Carney will be speaking before the House of Lords Economic Affairs Committee at 1530 GMT.

API data on US crude oil stocks will be made public at 2135 GMT.

The earnings season remains under way with pharma giant Pfizer being among companies releasing quarterly earnings on Tuesday.

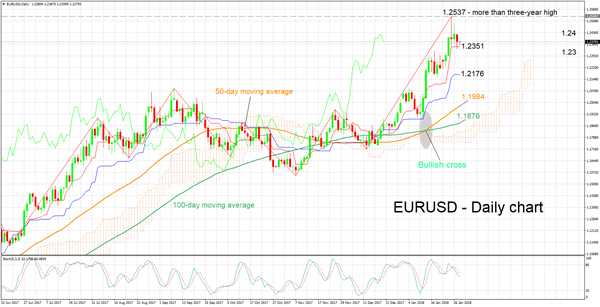

Technical Analysis: EURUSD weakening positive momentum

EURUSD has declined from 1.2537, the highest since late 2014 hit on Thursday, presently falling below the 1.24 handle. The positively aligned Tenkan- and Kijun-sen lines continue to project a bullish picture in the short-term. However, the two lines have started moving sideways, this potentially being an indication of weakening positive momentum. The stochastics are also giving a bearish signal in the very short-term as the %K line has crossed below the slow %D line and both lines are moving lower.

Should eurozone data due during morning European trading hours surprise to the upside, the positive momentum might be refueled with the area around last week’s more than three-year high of 1.2537 – including the 1.25 mark – coming into view as potential resistance. Before that, the range around the 1.24 handle might act as a psychological barrier to price advancing.

A disappointment on the data front on the other hand, is likely to exert selling pressure on the pair. The area around the Tenkan-sen at 1.2351 could offer support in this case, with steeper declines shifting the focus to the 1.23 level – a point of potential psychological significance – for additional support. Notice that the price is at the moment not far above the current level of the Tenkan-sen.

Currencies: Risk Off Correction To Become Dominant Factor For FX Short-Term?

Sunrise Market Commentary

- Rates: German yields clear important technical resistance

The core bond sell-off accelerated yesterday. German yields copied last week's move by US yields, breaking above key resistance levels. The sell-off might slow if the overnight risk-off correction on stock/commodity markets persists. However, German inflation data, president Trump's state of the union and the Fed meeting are all able to start a new selling bout. - Currencies: Risk off correction to become dominant factor for FX short-term?

Yesterday, the dollar extended the bottoming out process that started end last week. Overnight risk sentiment turned further risk-off. The yen was already well bid of late and might further profit. We keep a close eye at EUR/JPY. A further rise of the yen/decline of EUR/JPY might prevent further euro gains even in case of good EMU eco data.

The Sunrise Headlines

- US stock markets corrected 0.5% to 0.7% lower yesterday. The sell-off accelerates in Asia this morning with also commodity markets and mainly base metals under pressure.

- ECB policy makers are sticking to the assumption that their bond-buying program will be wound down over about three months rather than brought to a sudden halt, according to euro-area officials familiar with the matter.

- The EU has passed Brexit transition guidelines making clear the UK will have to abide by all the bloc's laws but have no say in the decision-making process during a two-year transition period.

- Polish central bank governor Glapinski said that he would not be surprised if interest rates, presently at 1.5%, were raised in the first half of 2019 or if they stay unchanged as inflation is benign despite fast economic growth.

- UK consumer confidence recorded its highest M/M increase in a year in January (108.2 from 107.1 vs 109.8 in January last year), according to a YouGov survey. Respondents reported a rosier outlook for household finances.

- A congressional panel voted to make public a classified Republican-authored memo that alleges surveillance abuses against an associate of President Donald Trump dating back to the 2016 campaign.

- Today's eco calendar contains EMU Q4 GDP, EC economic confidence, German inflation, US S&P housing data and UK consumer confidence. Italy holds a BTP auction and ECB Mersch & BoE Carney are scheduled to speak

Currencies: Risk Off Correction To Become Dominant Factor For FX Short-Term?

Risk-off supportive for USD (ex USD/JPY?)

The dollar decline slowed at the end of last week and that continued yesterday. Core yields extended their break higher, but interest rate differentials were no good explanation for the USD price swings. EUR/USD drifted south in the 1.23 big figure. Remarkably, the move stalled after headlines that the ECB could consider a small tapering at the end of its APP. EUR/USD closed the session at 1.2383. The upside momentum in USD/JPY was far less strong. The pair tried to regain 109, but the move lacked momentum. USD/JPY finished at 108.96.

Asian equities join yesterday evening's US correction. The risk-off move also weighs on commodities. The impact on the dollar is mixed. EUR/USD is losing a few ticks (1.2350). USD/JPY struggles not to return lower in the 108 area.

EMU data will be at least be as important for FX trading as US ones today. EMU Q4 growth is expected at 0.6% Q/Q and 2.7% Y/Y. German inflation is forecast to decline 0.7% M/M to stay unchanged at 1.6% Y/Y. We keep a close eye on the German inflation data. US consumer confidence is expect to rise from 122.1 to 123. Last but not least, risk sentiment might also return as a driver for FX trading. The EMU eco data will be strong. However, interest rate differentials weren't really a good guide for FX trading of late. So, we don't expect a resumption of the euro rally, even not on good EMU data. A risk-off correction could inspire further yen buying. USD/JPY looked already vulnerable of late and this might persist ST. Question is what it will mean for EUR/JPY and for EUR/USD. The jury is still out, but in a daily perspective, a further decline of USD/JPY and EUR/JPY might also cap the topside in EUR/USD and even cause some more downside pressure short-term. Later this week, the focus might turn to the Fed, the State of the Union and the US data.

Sterling showed some intraday gyrations yesterday. Sentiment clearly was more fragile than last week. EUR/GBP hovered in the high 0.87/low 0.88 area. EU ministers gave EU's Barnier a mandate for the next phase of the Brexit negotiations. At the same time, the division in the UK conservative party is flaring up again. Today, UK credit data will be published and BoE's Carney will testify before Parliament. Brexit headlines and a risk-off sentiment might continue to weigh on sterling. EUR/GBP can continue its rebound in the 0.8790/0.9033 trading range.

EUR/USD: correction continues

Rise In Global Bond Yields To Test Equity Investors’ Confidence

After enjoying the best kickoff in more than three decades, the S&P 500 posted its biggest decline since 17 August 2017. All ten sectors traded in red territory suggesting that we didn't see any rotation, but the selloff was broad-based led by Energy, Utilities, and Telecom sectors.

The factors which supported the rally over the past couple of months are still in play. Global synchronized growth, enthusiasm over the Trump administration's tax cuts, and strong earnings growth. According to Factset, more than 76% of S&P 500 companies have reported positive EPS surprises and 81% have reported positive sales surprises. These figures represent a record high in terms of U.S. companies beating sales estimates.

Given this optimistic view, many investors may consider buying the dips. This strategy has been profitable during the stock market uptrend, so why not buy the dips now?

Few will disagree that valuations are overstretched, however, due to low global interest rates, equities have remained attractive during the past couple of years.

Now with U.S. 10-year Treasury bond yields trading above 2.7%, and breaking above a three-decade downtrend, the uptrend in equity markets will be under a new test. Not only U.S. interest rates are on the rise, but German 5-year bund yields moved into positive territory for the first time since December 2015 and Japan's 10-year yields are trading at a 7-month high.

The rise in global bond yields isn't necessarily a bad thing; it reflects the strength of the economic recovery. However, the pace of the rise in yields may create significant headwinds for equities in the days to come, especially if U.S. 10-year yields break above 3%, a very critical physiological level in my opinion. A simple question that may come to investors mind, is “why would I remain in equities when two-year U.S. treasury bills can provide the same divided yield return of the S&P 500 at 2.12”?.

The CBOE's volatility index VIX edged up 25% on Monday, the highest close since August last year, suggesting that investors are demanding put options to protect their portfolios from potential downside risks. This combination of higher bond yields and the VIX increase, are catalysts for a further correction in the days to come, so keep a close eye on these two indicators.

EUR Fixed Income Markets Continued To Be Under Pressure

Market movers today

In the euro area, market focus will be on GDP figures for Q4 17 today. Growth was strong in the first three quarters of 2017, with the latest print for Q3 at 0.7% q/q.

Both survey and activity indicators have pointed towards continued strong growth and hence we look for another solid reading of Q4 GDP growth of 0.6% q/q. As it is the first release, we will not yet receive much detail on the growth drivers though. Note that France and Spain will also release preliminary Q4 17 GDP data today.

Also in the euro area, German inflation figures are published, ahead of the euro area HICP data tomorrow. Markets are likely to look out for any signs that core inflation is picking up, as visible inflationary pressure in t he euro area's biggest economy remains largely absent .

The ECB's Yves Mersch will also speak in Frankfurt and markets will watch out for further insights into the cont rasting views within the Governing Council at the moment .

In the US, today's key event will be Donald Trump's State of the Union speech. We will look out for hints on infrastructure spending and protectionist trade policy measures.

In the Scandi markets, Danish business confidence data and Norwegian retail sales for December are due to be released.

Selected market news

The EUR fixed income markets continued to be under pressure yesterday with the entire yield curve moving higher. However, the sell-off did diminish somewhat late last night as an ‘ECB sources story' surfaced stating that the ECB's QE will end with a short taper rather than a sudden stop. According to the story, even the more hawkish GC members endorse a gradual slowdown of QE after September.

Japanese figures out this morning on the labour market giving mixed signals. The unemployment rate increased from 2.7% in November, the lowest level since 1994, to 2.8% in December, whereas the jobs-to-applicants ratio increased further, now standing at 159 jobs for every 100 applicants – the highest since 1972. The tightness of the labour market is of historic proportions and still no pickup in core inflation. Coming spring wage negotiations will be key here.

Regarding the US debt limit suspension, the US Treasury Secretary Steven Mnuchin said that he can extend the suspension period in to February be fore the government's borrowing capacity is exhausted, i .e. beyond the end of January deadline he had given previously. Yesterday, the US Treasury published new cash balance estimates with its estimate at the end of Q1 18 revised down to USD210bn from USD300bn (October est imate). However, the US Treasury expects the cash balance to be USD360bn at the end of Q2 18, which would lead to a tightening of USD liquidity.

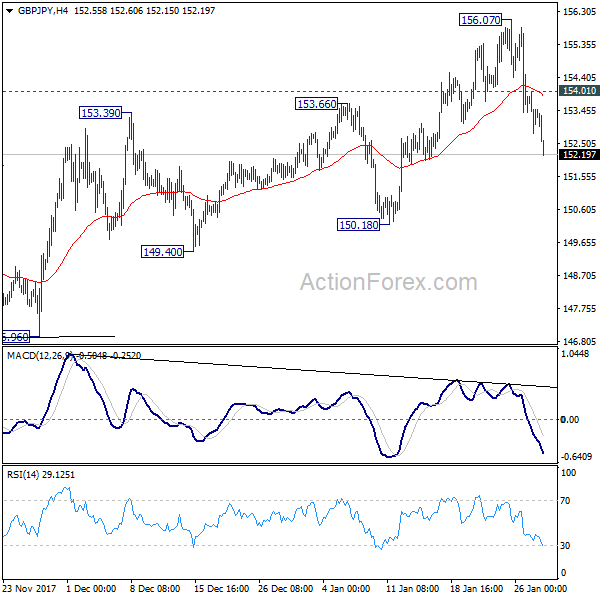

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.77; (P) 153.39; (R1) 153.97; More...

GBP/JPY's fall from 156.07 is still in progress and intraday bias remains on the downside for 150.18 support. As 156.07 is seen as a short term top. Break of 15018 will target 149.96 key support level. On the upside, above 154.01 minor resistance will turn intraday bias neutral first. But risk will now stay on the downside as long as 156.07 resistance holds.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

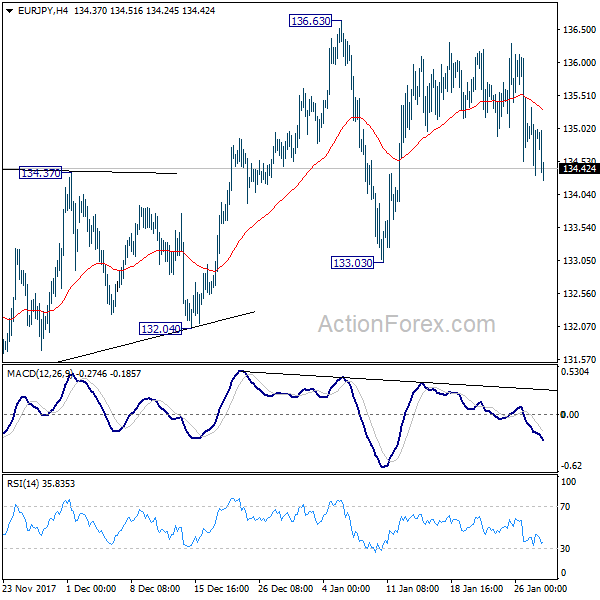

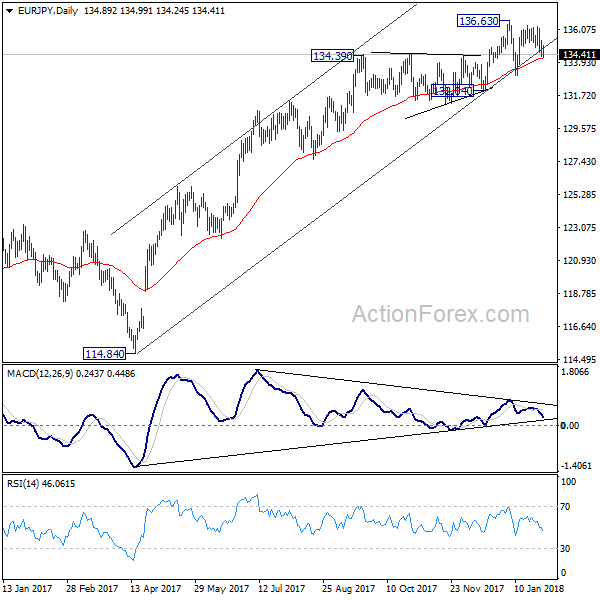

EUR/JPY Daily Outlook

Daily Pivots: (S1) 134.37; (P) 134.85; (R1) 135.39; More....

Intraday bias in EUR/JPY remains neutral but outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

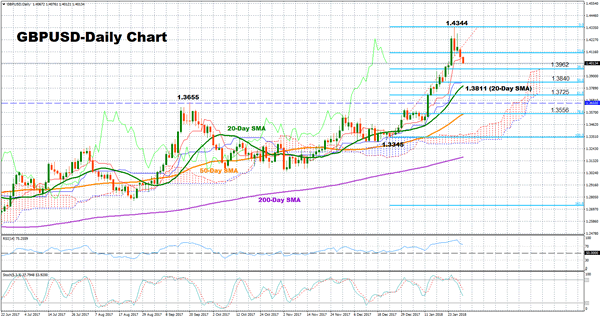

GBPUSD Loses Steam But Outlook Still Bullish

GBPUSD stalled its recent rally after touching its highest level since June 2016 but continues to trade in bullish environment as it maintains a positive trend and technical indicators signal that the market might retain this bullish phase in the medium-term.

The market crawled well above the simple moving average lines (SMA) which are currently positively aligned and show no sign of reversing direction, while the Tenkan-sen is positively sloped above the Kijun-sen. However, downside corrections in the near term cannot be ruled out yet as the RSI continues to fluctuate above 70, hinting that the market might be overbought. Stochastics are also moving downwards after reaching overbought territory above 80.

Immediate support is now at the 38.2% Fibonacci of 1.3962 of the upleg from 1.3345 to 1.4344. A stronger barrier, though, would be found at the 20-day moving average of 1.3811, which if violated would confirm that another leg down is underway with scope to reach next support at 1.3556.

On the flip side, if prices improve, resistance could come from the 1.41 handle. Further increases could also shift focus to the 1.42 psychological level and the previous top at 1.4344.

Turning to medium-term picture, the outlook is positive as long as prices remain above the September’s high of 1.3655

Forex Analysis: US State Of The Union Tonight

President Donald Trump will deliver his first State of the Union Address at 21:00 EST (02:00 GMT Wednesday 31st January) tonight from Capitol Hill. Any reference made to the economy, trade or the U.S. dollar could result in volatility in markets. The consensus deems it likely that the speech will have a direct impact on the dollar, as it includes a budget message and an economic report of the nation.

US Personal Consumption Expenditures – Price Index (YoY) (Dec) was 1.7% v an expected 1.9%, from 1.8% previously. Core Personal Consumption Expenditures – Price Index (MoM) (Dec) came in at 0.2%, from 0.1% previously. Personal Consumption Expenditures – Price Index (MoM) (Dec) was 0.1% v an expected 0.0%, from 0.2% previously. Personal Income (MoM) (Dec) was 0.4% v an expected 0.3%, from 0.3% previously. Personal Spending (Dec) was as expected at 0.4%, from 0.6% previously, which was revised up to 0.8%. Core Personal Consumption Expenditures – Price Index (YoY) (Dec) was as expected, remaining unchanged at 1.5%. USDCAD moved higher from 1.23331 to 1.23453 as a result of this data.

US Dallas Fed Manufacturing Business Index (Jan) was 33.4 against an expected number of 14.6, from 29.7 previously. EURUSD traded down from 1.23739 to a low of 1.23367 following the data release.

New Zealand Trade Balance (MoM) (Dec) numbers were released at $640M against an expected $-125M. The prior number was $-1,193M but was revised down to $-1,233M. Imports (Dec) were $4.91B from $5.82B previously, which was revised up to $5.84B. Trade Balance (YoY) (Dec) was $-2.840B from $-3.444B previously, which was revised down to $-3.480B. Exports (Dec) were $5.55B from $4.63B previously, which was revised down to $4.61B. NZDUSD moved higher from 0.73242 to 0.73357.

Japanese Job/Applications Ratio (Dec) was 1.59 v an expected 1.57, from 1.56 previously. Unemployment Rate (Dec) was 2.8% v an expected 2.7%, from 2.7% previously. Overall Household Spending (YoY) (Dec) was -0.1% against an expected 1.7%, from 1.7% prior. Large Retailer’s Sales (Dec) was 1.1% against an expected -0.6%, from 1.4% prior. Retail Trade s.a. (MoM) (Dec) was 0.9% against an expected 0.1%, from 1.9% prior, which was revised down to 1.8%. Retail Trade (YoY) (Dec) was 3.6% against an expected 1.8%, from 2.2% previously, which has been revised down to 2.1%.

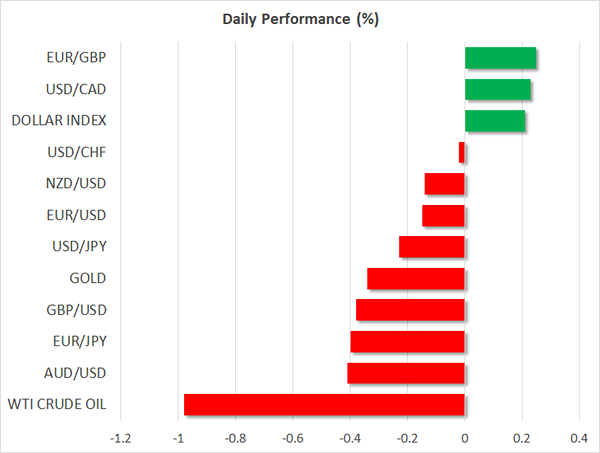

EURUSD is down -0.24% overnight, trading around 1.23552.

USDJPY is down -0.17% in early trading at around 108.773.

GBPUSD is down 0.38% to trade around 1.40205.

USDCAD is up 0.21%, trading around 1.23636.

Gold is down -0.38% in early trading at around $1,334.80.

WTI is down -1.02% this morning, trading around $64.82.

Major data releases for today:

At 09:30 GMT, UK Consumer Credit (Dec) is expected to be £1.3B from £1.4B previously. Mortgage Approvals (Dec) is expected at 63.500K from 65.139K prior. GBP crosses could be affected by this data.

At 10:00 GMT, Eurozone Gross Domestic Product s.a. (QoQ) (Q4) is expected to be unchanged at 0.6%. Gross Domestic Product s.a. (YoY) (Q4) is expected to be 2.7% from 2.6% previously. Services Sentiment (Jan) is expected to be 18.6 from 18.4 previously. Consumer Confidence (Jan) is expected to be unchanged at 1.3. Industrial Confidence (Jan) is expected to be 9.0 from 9.1 previously. Economic Sentiment Indicator (Jan) is expected to be 116.3 from 116.0 previously. Business Climate (Jan) is expected to come in at 1.69 from 1.66 prior. EUR pairs may be moved by this release, especially the GDP data.

At 13:00 GMT, German Harmonised Index of Consumer Prices (YoY) (Jan) is expected to come in unchanged at 1.6%.

At 14:00 GMT, US S&P/Case-Shiller Home Price Indices (YoY) (Nov) is expected to be unchanged at 6.4%.

At 15:30 GMT, Bank of England Governor Mark Carney will testify before the House of Lords Economic Affairs Committee in London. GBP crosses may experience volatility during this time.

At 02:00 GMT, Wednesday 31st January, we will see the US State of the Union address by President Trump.