Sample Category Title

GBP/USD Retracement In Uptrend

The GBP/USD is still in uptrend but at this point we see a retracement towards weekly camarilla levels. If the price drops at the POC zone, we might see a bounce towards W H1 - 1.4202. The POC zone ( W L3, ascending trend line, 78.6, historical buyers) 1.4023-1.4067 could show now moment buyers ant the price might bounce to 1.4202. The zone is wider due to much higher ATR in the previous week. Continuation of the uptrend is possible only if we see a clear close above 1.4202. Below 1.4200 the price could drop to 1.3966, 1.3916 and 1.3890. Have in mind that this is the intra week analysis.

W H1 - Weekly Camarilla Pivot (Interim resistance - Weak)

W H2 - Weekly Camarilla Pivot (Weekly resistance)

W H3 - Weekly Camarilla Pivot (Weekly resistance - main)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

W L4 - Weekly Camarilla Pivot (Interim support - Strong)

W L3 – Weekly Camarilla Pivot (Interim support - Main)

W L2 – Weekly Camarilla Pivot (Interim support)

W L1 - Weekly Camarilla Pivot (Interim support - Weak)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Technical Outlook: USDJPY – Broken Weekly Cloud Base Caps Consolidation For Now

The pair is consolidating above last Friday,s fresh low at 108.28 on Monday, with the action being so far capped by broken supports at 109.06/10 (Fibo 76.4% / weekly cloud base) now acting as solid resistances.

Friday,s close below these levels was strong bearish signal for further weakness, but oversold daily studies may delay bears.

Limited upside action is seen preceding fresh weakness as bears eye targets at 107.80 (bull-trendline drawn off 2012 low at 77.12) and key m/t support at 107.31 (2017 low, posted on 08 Sep).

Recovery should ideally hold below weekly cloud base, with stronger upticks to be capped by 110.00 resistance (psychological barrier / falling 10SMA).

Res: 109.10, 109.76, 110.00, 110.20

Sup: 108.50, 108.26, 107.80, 107.31

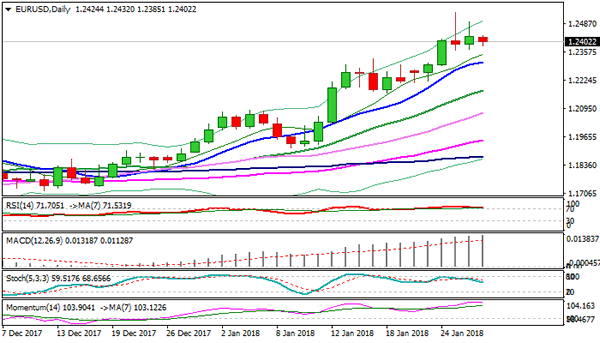

EURUSD Likely To Correct Below 1.2432

The euro is starting to correct lower against the greenback in early Monday trading, as the U.S dollar index starts to recover against a basket of major currencies. The EURUSD pair is currently hovering around the 1.2400 level, with downside pressure gathering while price trades below the key 1.2432 technical level. Euro traders now look to the release of the Federal Reserves preferred measure of domestic inflation in the U.S economy, the Core PCE Index.

The EURUSD pair may correct lower while trading below the 1.2432 level, downside support is found at 1.2385 and 1.2323.

Should the EURUSD pair move above the 1.2432 level, we may see further buying towards 1.2493 and 1.2537.

GBPUSD Intraday Bearish Below 1.4171 Level

The British pound has started the new trading week on the backfoot against the U.S dollar, as UK political uncertainty weighs on pound sentiment. After suffering heavy losses on Friday, the GBPUSD pair continues to remain under selling pressure, as speculation mounts that UK PM Theresa May could face a leadership challenge. UK politics aside, traders will now focus on the next move in the U.S dollar, and the release of the CORE PCE Index from the United States.

The GBPUSD pair is likely to remain under selling pressure while trading below the 1.4171 level, key intraday support is found at 1.4082 and 1.4041.

Should price-action on the GBPUSD pair move above the 1.4171 level, buyers may test towards the 1.4211 and 1.4284 levels.

US DataTake Centre Stage On Monday

The global financial markets will be off to a busy start this week, with attention fixated on the US economic calendar.

Investors can expect a sparse release schedule from the European market on Monday. The Spanish government will report on retail sales at 08:00 GMT, followed by a report on Italian producer inflation two hours later.

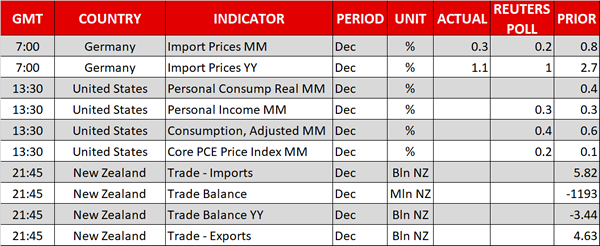

In the United States, the Department of Commerce will issue its monthly personal income and outlays report at 1:30 GMT. The report is expected to show a 0.3% increase in personal income last month, accompanied by a 0.4% uptick in consumer spending.

Market participants are also looking at the personal income and outlays report for another reason: it contains the latest data on core personal consumption expenditures (PCE), which is the Federal Reserve’s preferred measure of inflation. The core PCE index is projected to rise 0.2% month-on-month, which translates into an annualized rate of 1.6%. The US central bank targets inflation at 2% annually. Although inflation remains below that level, the Fed has been slowly removing policy accommodation in response to a stronger economy.

Later in the morning, the Federal Reserve Bank of Dallas will report on the manufacturing business index for January. The monthly report is expected to show a sharp slowdown in regional factory activity.

Several high-profile US releases are scheduled throughout the week, culminating in Friday’s nonfarm payrolls report. The release is expected to show another month of solid hiring for the world’s largest economy, boosting optimism about the nation’s prospects. Other US data releases this week include factory orders and manufacturing PMI.

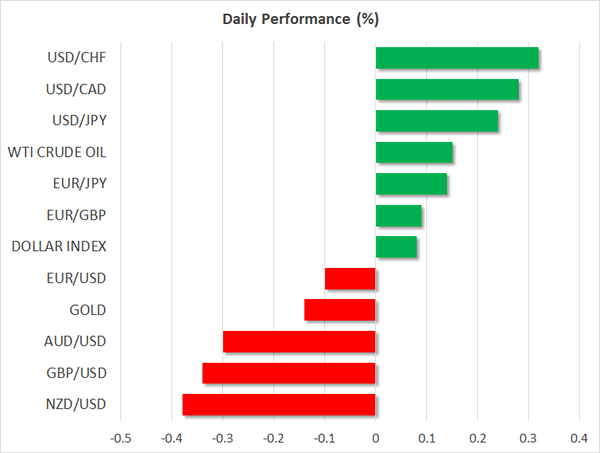

In the currency markets, all eyes will be on the US dollar, which is coming off the worst start to a year in decades. The US dollar index (DXY), which tracks the performance of the greenback against a basket of six competitors, fell below 90.00 last week. It was last seen trading at 89.22, having gained 0.2% from the previous close.

EUR/USD

Europe’s common currency is coming off another week of solid gains. The EUR/USD closed firmly above 1.2400 on Friday and continues to trade above those levels at the start of Monday’s Asian session. The pair will continue to be supported so long as the dollar’s woes continue.

GBP/USD

Like the euro, the British pound scored huge gains against the dollar last week, with cable rising above 1.4100 for the first time since the Brexit debacle. The GBP/USD was last seen trading at 1.4132. Its short-term outlook will be dictated by the US dollar and its response to high-profile economic data.

USD/JPY

The Japanese yen backtracked slightly against the dollar on Monday but remains in a firm uptrend. The USD/JPY exchange rate was last seen trading at 108.76. The bears are eyeing fresh lows so long as the pair trades near the 108.50 mark.

Technical Outlook: GBPUSD – Risk Of Deeper Pullback Towards Strong 1.40 Support Exists

Cable eases in early Monday's trading and pressures 1.41 support, following last week's double upside rejection at 1.43 zone. Friday's candle with long upper shadow, left after strong rejection ticks under 1.4300 barrier weighs on near-term action for deeper pullback after last week's action stalled on approach to weekly 200SMA (1.4384). Weak hourly structure supports further easing for test of Thursday's low at 1.4082 and daily Tenkan-sen (1.4050), violation of which would expose strong support at 1.4000 (psychological support/Fibo 38.2% of 1.3457/1.4344/rising 10SMA). Overall bulls favor shallow correction which should be ideally contained above 1.40 support before fresh attempts higher, however, risk of deeper correction on loss of 1.40 handle, cannot be ruled out as studies on daily and weekly charts are overbought. Bearish scenario will be activated on firm break below 1.40 and would risk extension towards next key support at 1.3800 (Fibo 61.8%/rising 20SMA).

Res: 1.4158, 1.4182, 1.4218, 1.4286

Sup: 1.4100, 1.4082, 1.4050, 1.4000

Yen Gains On Kuroda’s Comments, US Consumption And PCE Data Due

Here are the latest developments in global markets:

FOREX: The dollar index traded marginally higher on Monday, recouping some of the losses it posted on Friday. Meanwhile, the yen remained relatively elevated after shooting up on Friday, following some remarks from BoJ Governor Kuroda.

STOCKS: Asian markets were mixed. In Japan, the Nikkei 225 closed marginally lower, while the Topix was less than 0.1% higher. In Hong Kong, the Hang Seng declined 0.3%, though the index still lies very close to all-time high levels. In Europe, futures tracking the Euro STOXX 50 were 0.3% up, suggesting the index could open higher. Over in the US, Friday marked another spectacular day for the major indices, with the S&P 500, Dow Jones and Nasdaq Composite all closing at record highs. The Nasdaq led the charge, gaining an astonishing 1.3%, while the S&P tracked closely behind that, up by almost 1.2%. Futures tracking the S&P, Dow and Nasdaq 100 are all currently very close to neutral territory, thus providing no clear indication of how these indices might open today.

COMMODITIES: Oil prices did not give a clear direction on Monday, with WTI trading slightly higher, but Brent crude being somewhat lower. Both benchmarks continue to hover near multi-year highs, buoyed by the broader plunge in the US dollar, as well as optimism that the market is rapidly rebalancing itself. That said, the sentiment surrounding the energy market may be on thin ice right now, amid tentative signs that US production has begun to rise again, following the surge in the US Baker Hughes oil rig count released on Friday. In precious metals, gold corrected a little lower on Monday, last trading near the $1347/ounce level.

Major movers: Yen spikes up on 'optimistic' BoJ remarks

The Japanese yen gained ground on Friday, following some comments from Bank of Japan (BoJ) Governor Haruhiko Kuroda at Davos. In an uncharacteristically optimistic tone, he said there are some indications that Japanese wages are rising, and that the BoJ is finally close to achieving its 2% inflation target. Even though these comments are far from ground breaking, they come from a notorious policy dove, and amidst heightened speculation that the BoJ may be setting up to scale back its massive stimulus program.

That said though, one has to reiterate that any change in the BoJ's language will likely be motivated by a substantial pick-up in wages and inflation, something that is not evident in the data yet. Indeed, the BoJ quickly backpedaled on these remarks, with a spokesperson for the Bank clarifying a few hours later that the Governor did not signal any change to the inflation outlook, causing the JPY to give back some of its Kuroda-induced gains.

Sterling/dollar corrected lower 0.3% today, perhaps due to some profit-taking ahead of a meeting in Brussels between EU27 ministers. The officials are expected to approve a set of directives that will allow their chief negotiator to broker a transitional agreement with the UK.

As for the commodity-linked currencies, dollar/loonie was up nearly 0.3%. In the near-term, the pair will likely continue to respond to any moves in oil prices, as well as any developments in the ongoing NAFTA negotiations. In this respect, the sixth round of talks (out of seven) is scheduled to conclude today, amid no signs of material progress. Any comments from the senior negotiators will be closely watched. Elsewhere, kiwi/dollar was down almost 0.4%, while aussie/dollar fell 0.3%.

Day ahead: US consumption & core PCE due; New Zealand trade data could also attract attention

Market participants will be paying close attention to US consumption data for the month of December due at 1330 GMT. Consumer spending during the month is expected to ease after growing beyond forecasts in November, overall giving signs of positive momentum in the economy. The December core personal consumption expenditures (PCE) price index – the Federal Reserve's preferred inflation measure – will be made public at the same time. It is expected to grow by 0.2% m/m in December, up from November's 0.1%, while year-on-year growth for the measure is expected to remain at 1.5%; this compares to the Fed's target for inflation of 2%. Following the surprising uptick in the core CPI rate for the month, market participants may be looking for a similar reaction in the core PCE print as well. An upside surprise could lead markets to price in a more aggressive tightening cycle by the US central bank, thus lending support to the greenback. Data on personal consumption and income will also be released at 1330 GMT.

Beyond the above releases, the economic calendar is relatively light today with New Zealand's trade data for December gaining some interest. Those are scheduled for release at 2145 GMT.

European Central Bank board member Sabine Lautenschläger will be speaking at a Frankfurt conference on banking reforms at 1045 GMT.

In equity markets, corporate earnings releases will continue to keep investors busy.

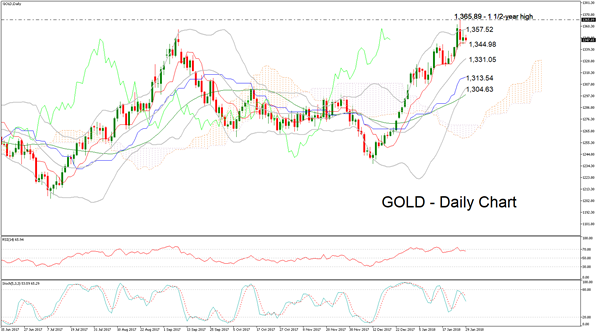

Technical Analysis: Gold bullish bias potentially loses steam

Gold has eased a bit after hitting a one-and-a-half year high of 1,365.89 last week. The Tenkan- and Kijun-sen lines remain positively aligned and the RSI indicator is in bullish territory above 50. However, the RSI moving sideways might be an indication of the bullish short-term momentum losing steam. Also, the stochastics are giving a bearish signal in the very-short-term: the %K line has moved below the slow %D one and both lines are heading lower.

The dollar-denominated precious metal tends to lose ground when the greenback strengthens. Stronger-than-anticipated US data on consumption and PCE later on Monday are expected to boost the dollar and likely push gold lower. In this case, gold might find support around the Tenkan-sen at 1,344.98, with steeper declines shifting the focus to the current level of the middle Bollinger line – a 20-day moving average line – at 1,331.05.

A US data miss that weakens the dollar could see the yellow metal advancing. In such a scenario, resistance could be met around the upper Bollinger band at 1,357.52 and further above at around last week's high of 1,365.89.

Technical Outlook: EURUSD May Ease Further As Dollar Regains Traction, Overall Bulls Favor Further Upside After Correction

The Euro stands at the back foot at the beginning of the week and tested supports at 1.2400 zone on Monday, as dollar ticked higher against the basket of major currencies, boosted by overall solid US GDP data last Friday. This signals a breather in larger EURUSD uptrend, with repeated failures to clear 1.25 barrier also seen as negative signal which could lead into deeper correction, as bulls show signs of fatigue. Thursday’s bearish candle with long upper shadow which was formed after strong upside rejection at 1.2537, continues to weigh and signal further easing. Near-term action stays capped under hourly cloud (1.2420/1.2445) keeping immediate focus at the downside and test of Friday’s low at 1.2370, break of which will unmask strong support at 1.2300 (Fibo 38.2% of 1.1915/1.2537 upleg, reinforced by rising 10SMA). Corrective action should be ideally contained at 1.2300 zone as overall bullish structure favors further advance. Conversely, loss of 1.2300 handle would signal deeper correction and risk test of key 1.2160 support zone (18 Jan trough/Fibo 61.8% of 1.1915/1.2537/rising 20SMA).

Res: 1.2432, 1.2493, 1.2537, 1.2597

Sup: 1.2370, 1.2351, 1.2300, 1.2226

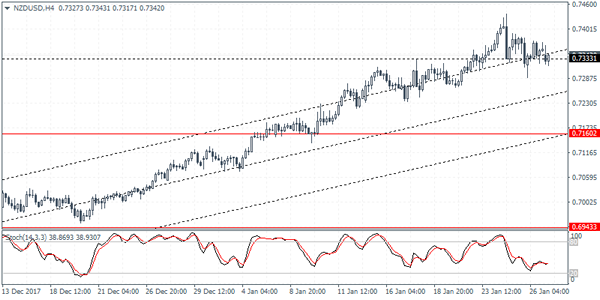

NZDUSD Intraday Analysis

NZDUSD (0.7342): The new Zealand dollar has stalled near the top end of the rally with price settling above 0.7333. As long as this support holds, NZDUSD could be seen attempting to post further gains above the previous highs at 0.7407. The downside risks could start to build in the event that NZDUSD breaks down below 0.7333. This would mark a potential correction towards the next main support at 0.7160.

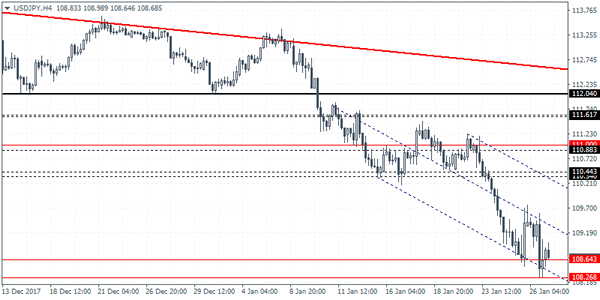

USDJPY Intraday Analysis

USDJPY (108.68): The USDJPY extended declines to briefly test the lower support near 108.26. However, the quick pullback off this level indicates a further test of support. On the 4-hour chart, USDJPY was seen consolidating near the minor support level of 108.64 - 108.26. A rebound off this level can be expected only on a higher low being formed. To the upside, resistance at 110.44 - 110.34 could be tested in the near term. The USDJPY currency pair could be seen remaining range bound within these levels in the near term with a breakout from the resistance or support likely to see further direction in the trend being established.