Sample Category Title

EURUSD Intraday Analysis

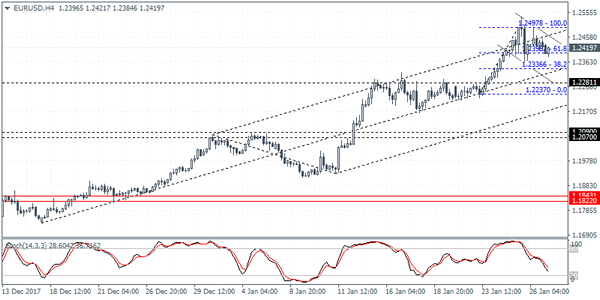

EURUSD (1.2419): The EURUSD rallied briefly to post a fresh 4-year high at 1.2537 on Thursday but eased back towards the weekend. The gradual decline is seen with the euro attempting to rebound off the previous lows formed at 1.2393 where minor support can be seen. As long as this support holds, EURUSD could be poised to make further gains to the upside. This is also seen by the bullish flag pattern that has formed. The next target to the upside comes in at 1.2660 provided that the EURUSD can breakout above 1.2497. To the downside, a break down below 1.2398 could signal a correction towards 1.2281.

U.S. GDP Weaker Than Expected. Core PCE Data Awaited

The U.S. dollar closed last week on a volatile note with the dollar index losing 0.3% on Friday. The decline also marked the biggest weekly loss since June 2017. On Thursday, President Trump clarified on the comments made earlier by the Treasury Secretary Steven Mnuchin about his preference for a weaker dollar. Trump said that Mnuchin's comments were taken out of context. This sent the USD to rise briefly but the currency gave up those gains by Friday's close.

The preliminary GDP data from the U.S. was released on Friday. The fourth quarter GDP was seen rising 2.6% which was weaker than expected. In the UK, the advance GDP report showed that the UK's economy rose 0.5% on the quarter.

Looking ahead, the economic data today will include the German import prices while in the NY trading session, the core PCE price index data will be released. Economists expect core PCE to rise 0.2% on the month. Personal income and spending data will also be released.

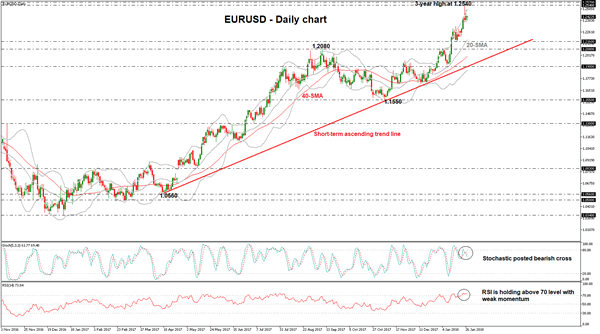

EURUSD Maintains Weak Upside Bias, Bearish Correction Is Expected

EURUSD has been underperforming in the previous couple trading days, creating a pullback on the 3-year high, the 1.2540 resistance level. When looking at the bigger picture the pair holds a clear trend to the upside as it recorded the sixth bullish week in a row.

However, the short-term technical indicators are pointing for a correction to the downside. The RSI is above the 70-overbought level at 73, suggesting that the latest upswing may be running out of steam and that the risk of a near-term correction is high. Moreover, the stochastic oscillator posted a bearish crossover within the %K and %D moving averages, indicating bearish movement. The price hit the upper boundary of the Bollinger Band and failed to end a day above it.

Should price reverse lower, immediate support could come at 1.2160, which is near to the mid-level of the Bollinger Band. Below that, 1.2080 is another major support and is holding above the 9-month ascending trend line.

Conversely, to the upside, the next level to have in mind is the 1.2540 key level, while slightly above it, the next significant resistance is the 1.2570 taken from the high in December 2014.

Forex Analysis: Markets Settle Post Davos

There was a general increase in volatility last week across the board due to Davos and a busy economic calendar. On Friday, BOJ's Kuroda made comments in Davos concerning the Japanese economy, saying the contrast between recovery and inflation stands out more than anywhere else and the economy is expanding moderately and will continue. It's the second largest expansion post-war. Medium to long-term inflation expectations is expected to rise. The deflationary mindset has been more tenacious than expected. He said that the output gap is closing and that the BOJ will continue aggressive easing. Most risks, from his perspective, were external and there were some indications that wages were rising. This last comment about wages sent USDJPY lower from 109.542 to 108.360.

Bank of England Governor Mark Carney also made comments at the same event, saying 80% of the G7 recovery is led by investment and trade. The probability of adjustment in asset prices has risen. We have not fully solved too big to fail. The market will decide where asset prices should be and the financial system is unlikely to amplify asset price moves. He also said that higher capital standards would help if there was a disorderly Brexit. EURGBP moved higher from 0.87323 before his comments, to finish at 0.87798 afterwards.

UK Gross Domestic Product (QoQ) (Q4) was 0.5% v an expected 0.4%, from 0.4% previously. Gross Domestic Product (YoY) (Q4) was 1.5% v an expected 1.4%, compared to 1.7% previously. GBPUSD went to a high of 1.42853, before selling off to 1.42390 following the data release.

Canadian Consumer Price Index (MoM) (Dec) was -0.4% v an expected -0.3%, from 0.3% previously. BOC Consumer Price Index Core (YoY) (Dec) was 1.2% v an expected 1.5%, from 1.3% previously. BOC Consumer Price Index Core (MoM) (Dec) was -0.5% v an expected -0.6%, from a prior -0.1%. Consumer Price Index (YoY) (Dec) was unchanged at 1.9%, from 2.1% previously. CAD crosses can be affected by this release. USDCAD moved higher, from a low of 1.22960 to 1.23588 following the data becoming public.

US GDP Annualized (Q4) was 2.6% v an expected 3.0%, from 3.2% previously, which was revised down to 2.6%. GDP Price Index (Q4) was 2.4% v an expected 2.3%, from 2.1% previously. Durable Goods Orders Ex-Transportation was 0.6% v an expected 0.5%, from -0.1% previously, which was revised up to 0.3%. Durable Goods Orders (Dec) was 2.9% v an expected 0.8%, from 1.3% previously, which was revised up to 1.7%. USDJPY sold off from 109.298 to 109.108 after the data release.

At 18:00 GMT, Baker Hughes US Rig Count numbers were released coming in at 759. The prior number last Friday showed that there were 747 Oil rigs in operation.

EURUSD is down -0.11% overnight, trading around 1.24146.

USDJPY is up 0.17% in early session trading at around 108.774.

GBPUSD is down 0.23% to trade around 1.41299.

USDCAD is up 0.17%, trading around 1.23351.

Gold is down -0.07% in early morning trading at around $1,348.35.

WTI is up 0.12% this morning, trading around $66.22.

Major data releases for today:

At 13:30 GMT, US Personal Consumption Expenditures – Price Index (YoY) (Dec) is expected to be 1.9% from 1.8% previously. Core Personal Consumption Expenditures – Price Index (MoM) (Dec) is expected to be 0.2% from 0.1% previously. Personal Consumption Expenditures – Price Index (MoM) (Dec) is expected to come in at 0.0% from 0.2% previously. Personal Income (MoM) (Dec) is expected unchanged at 0.3%. Personal Spending (Dec) is expected at 0.4% v 0.6% previously. Core Personal Consumption Expenditures – Price Index (YoY) (Dec) is expected unchanged at 1.5%. USD crosses may be heavily traded as a result of this data.

At 15:30 GMT, US Dallas Fed Manufacturing Business Index (Jan) is expected to be released, with a number of 14.6, from 29.7 previously. Firms are asked by the Federal Reserve Bank of Dallas whether output, employment, orders, prices and other indicators increased, decreased or remained unchanged over the previous month.

At 21:45 GMT, New Zealand Trade Balance (MoM) (Dec) numbers will be released and are expected to be $-125M. The prior number was $-1,193M. Imports (Dec) were $5.82B previously. Trade Balance (YoY) (Dec) was $-3.444B previously. Exports (Dec) were $4.63B previously. This data can affect NZD crosses.

At 23.30 GMT, Japanese Job/Applications Ratio (Dec) is expected at 1.57 from 1.56 previously. Unemployment Rate (Dec) is expected unchanged at 2.7%. Overall Household Spending (YoY) (Dec) is expected unchanged at 1.7%. Large Retailer's Sales (Dec) is expected at -0.6% from 1.4% prior. Retail Trade s.a. (MoM) (Dec) is expected at 0.1% from 1.9% prior. Retail Trade (YoY) (Dec) is expected at 1.8% from 2.1% previously, which has been revised up to 2.2%. JPY pairs could be moved by this data release.

Major data releases for this week:

On Tuesday at 10:00 GMT, Eurozone Gross Domestic Product QoQ and YoY for Q4 will be released.

On Wednesday at 19:00 GMT, the US Fed Interest Rate Decision and Monetary Policy Statement will be released.

On Friday at 13:30, US Nonfarm Payrolls and the Unemployment Rate for January will be released.

Currencies: Dollar Decline Halts, At Last For Now

Sunrise Market Commentary

- Rates: US yields clear technical hurdles

US yields cleared technical resistance at the 5- and 10-yr tenors last week, suggesting more upward potential medium term. Today's PCE inflation data are less important than usual as they could be derived from Friday's GDP release. The eco calendar heats up later this week with the Fed meeting, Trump's State of the Union and payrolls. - Currencies: Dollar decline halts, at least for now

The USD sell-off eased at the end of last week as US president Trump in some way ‘confirmed' the US strong dollar policy. This week the focus turns, amongst others, to the Fed policy decision. The Fed turning more optimistic on growth or on inflation, might help to put a floor for the dollar. For now there is no sign of a trend reversal in the USD yet.

The Sunrise Headlines

- US stock markets set another round of record highs on Friday (+1%) and are heading for their best month in over two years as earnings from corporate America continue to impress. China underperforms in Asia overnight.

- Britain is seeking powers to vet new EU laws agreed by the rest of the bloc during the transition period after Brexit day, in a demand that risks setting the UK on a collision course with Brussels.

- There are a number of factors preventing the BoJ from reaching its 2% inflation target but wages and prices are gradually rising and it is getting closer, the governor of the central bank Kuroda said on Friday.

- China's economic growth will likely slow to 6.5-6.8% this year, a senior official at the country's top economic planner wrote in the Beijing Daily, while warning about the risks of "Black Swan" and "Gray Rhino" events.

- The ECB has to end its quantitative easing as soon as possible, according to ECB Governing Council member Knot, who said there's not a single reason anymore to continue with the program.

- Miloš Zeman will serve a second and final term as Czech president, after defeating his pro-EU rival Drahoš in an election that underscored the strength of the backlash against the EU's multi-cultural and liberal values in central Europe.

- Today's eco calendar contains US personal income & spending data and PCE inflation numbers. ECB's Lautenschlaeger and Coeure are scheduled to speak

Currencies: Dollar Decline Halts, At Last For Now

Dollar decline slows going into Fed decision

The dollar entered calmer waters on Friday. US president Trump's address at the WEF on Friday brought little news on international trade or for the dollar. US data, including Q4 GDP were OK, but failed to inspire trading. EUR/USD drifted back lower in the 1.24 big figure. The yen remained well bid as markets saw a hawkish spin in comments from BOJ's Kuroda. USD/JPY rebounded off the intraday lows as the BOJ indicated that there was no change in its inflation assessment. USD/JPY finished the day at 108.58 (109.41 on Thursday).

Asian equities opened strong this morning, but the rally loses momentum throughout the session. USD/JPY moves in the upper half of 108. EUR/USD trades close to and mostly just north of 1.24.

US spending and income data will be published today. The data are less relevant for markets as the US Q4 GDP report is already published. Investors will look forward to US president Trump's State of the Union and Fed's policy decision on Wednesday and to the early month US eco data, including the payrolls on Friday. Will the Fed upgrade its assessment on growth or on inflation? The tone of US president Trump's speech might again be a bit more protectionist than in Davos.

The dollar decline slowed at the end of last week. This process can continue going into the Fed meeting. A modest USD comeback is possible if the Fed turns more optimistic and the US data remain strong. There is no clear technical sign of a sustained USD rebound yet. EUR/USD 1.2537/1.2596 remains the first topside reference. A return below 1.2323 would indicate that the pressure on the USD is easing. A sustained return below 1.2165 would call off the ST alert on the USD.

On Friday, sterling received temporary support from better than expected Q4 growth, but the gain could not be sustained. EUR/GBP finished the session at 0.8780. Today, the EU27 ministers meet to finalize the directives for the Brexit negotiations. There is again more political noise on Brexit in the UK. The sterling rebound lost momentum at the end of last week. The downside test of EUR/GBP was rejected. We put the risk for EUR/GBP to return back higher in the 0.8690/0.9033 range. Intermediate resistance comes in at 0.8928

EUR/USD: rally halted, but no technical sign of a trend reversal

Market Update – Asian Session: USD Rises Slightly After Weakening On Comments From Davos, Equities Shore Up Ahead Of...

Headlines/Economic Data

General Trend:

Asia markets open generally higher, tracking Friday’s rally in US equities

Energy shares outperform

Markets in Hong Kong and Shanghai underperform

US dollar (USD) trades generally firmer

Busy week in terms of corporate earnings and macro events (including Australia Q4 CPI, China PMIs, Fed meeting, Germany prelim CPI, US monthly nonfarm payrolls)

Apple due to report quarterly results after the close on Thursday, Feb 1st

Japan Telecoms to report earnings this week (KDDI, Sharp, NTT Docomo)

PBoC skipped open market operation (OMO) for third straight session

PBoC sets yuan at multi-year high for 7th straight session

Japan

Nikkei 225 opened +0.8%; closed flat

Shin-Etsu Chemical: Trades higher by over 4% (Q3 results above ests)

Fanuc [6954.JP]: Gains over 2% (Reported Q3 Net profit ¥50.5B v ¥41.8Be, Op profit ¥61.8B v ¥52.4Be, Rev ¥188.4B v ¥133.2B y/y; Raises FY18 guidance)

Fuji Electric [6504.JP]: Gains over 2% ahead of expected earnings report

Sharp [6753.JP]: +1.5% (Expected to report earnings on Jan 31st) - Auto components firm Koito Mfg: Declines over 5% (FY op profit guidance below consensus)

(JP) Japan's cryptocurrency exchange Coincheck has confirmed that ~¥58B ($534M) in customers' virtual currency holdings were taken from its wallets Friday (appears to be the biggest virtual currency heist to date) – Nikkei

(JP) Japan Cabinet Office white paper: consumer prices show signs of picking up – Nikkei

(JP) Japan MOF, BoJ and FSA officials expected to discuss markets during Monday afternoon - financial press

(JP) Bank of Japan: Gov Kuroda did not revise the inflation outlook in his Davos comments (from Friday, Jan 26th):[ ** NOTE: Earlier on Friday: (JP) BoJ Gov Kuroda: Reiterated that medium to long term inflation expectations are projected to rise; Seeing relatively weak prices in Japan; see some indication of rising wages and prices in Japan; we are finally close to our 2% inflation target] Looking Ahead: Japan Dec Household Spending, Unemployment Rate, Retail Sales due for release on Tuesday

Korea

Kospi opened +0.5%

Banks trade broadly higher: Shinhan Financial +2.3%, Woori +1% - Chip makers gain: Samsung Electronics and Hynix trade higher by over 1%

Samsung Biologics [207940.KR] +5.5% (may report earnings on Jan 31st)

Lotte Chemical: Gains over 3% (may report earnings on Feb 1st)

E-Mart: Has gained over 2% (gained over 15% on Friday amid investment in online unit)

(KR) South Korea to layoff 200 public employees (inlc executives), they will be referred to prosecutors over job favor cases - Korean press

(KR) Bank of Korea (BOK) economic focus report: The United States is expected to ramp up protectionist trade policies going forward, which could pose challenges for South Korea - Korean press

(KR) South Korea not excluding possibility of foreigner tax delay - Korean press

(KR) Bank of Korea (BoK) sells KRW800B in 1-year monetary stabilization bonds (MSB): yield 1.88%

(KR) South Korea sells KRW700B 20-year bonds: avg yield 2.65% v 2.405% prior

China/Hong Kong

Hang Seng opened +0.6%, Shanghai Composite +0.2%; Indices later pare gains

Hang Seng Property Index -1%, Information Tech -1%, Consumer Goods -0.9%, Financials -0.5%; Energy +1.5%

Chongqing Iron & Steel [1053.HK]: Higher by over 9% (expects to turn profit in FY17)

Great Wall Motor [2333.HK] Gains over 2% (receives some positive broker commentary despite FY profit warning)

Wynn Macau [1128.HK] Shares declines over 4%, bonds also decline (Shares of Wynn Resorts closed down by over 10% on Friday amid reports of sexual misconduct allegations related to CEO Steve Wynn)

Leshi Internet, 300104.CN Trades down by 10% daily limit for the 4th consecutive day

(KR) South Korea think tank HRI: South Korean companies need to shift their strategies in China as Beijing strives to boost domestic spending by attracting foreign investment and offering higher wages – Korean press

(CN) China NDRC sees 2018 GDP at 6.5-6.8%

(CN) PBoC: Skips OMO (3rd straight session) v skipped prior; Net drain CNY140B v CNY270B drain prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.3267 v 6.3436 PRIOR (strongest level since Nov 2nd, 2015)

(CN) China and South Korea economic chiefs to meet in China this week to discuss issues including increasing economic cooperation - Korean press

(HK) CNY 1-month HIBOR 4.70983% (highest level since Sept); 1-week HIBOR 4.17154% (highest level since Nov)

Australia/New Zealand

ASX 200 opened -0.1%; closed +0.4%

ASX 200 Energy Index +1.1%, Utilities +1%, Telecom +0.5%, Consumer Discretionary +0.5%, Financials +0.4%; REIT -0.7%

Energy firm AWE [AWE.AU]: Gains over 16% (Receives bid from Japan's Mitsui for A$0.95/shr cash or A$602M)

CBA.AU Names retail banking chief Matt Comyn as CEO, effective, April 9th

Iluka Resources [ILU.AU] Gains over 5%: Reports Q4 Mineral Sands Production 298.3Kt 217.5Kt y/y; Total Mineral Sands Rev A$245.4M v A$253.7M y/y

AUD/USD St George Bank raises year-end target for A$ to $0.84 (prior $0.82)

(AU) Australia PM Turnbull: To spend $3.1B to increase stake in global arms exports

SML.NZ Affirms 2017/18 milk price forecast of NZ$6.50 kgMS

AAC.AU Australia farmland values are expected to rise for a 5th consecutive year in 2018 fueled by low interest rates, rising commodity prices, favourable growing conditions and more profitable farmers looking to expand

Australian Agricultural Looking Ahead: New Zealand Dec Trade Balance and Australia Dec NAB Business Confidence due for release on Tuesday

North America

Avon [AVP] Activists investors expected to call for the company to examine options - US financial press

Wynn Resorts [WYNN]: Steve Wynn resigns from post as Republican National Committee (RNC) finance chair amid sexual misconduct allegations – press

Wynn Resorts [WYNN]: Following allegations related to CEO Wynn board said to create special committee – US financial press

Ford [F]: China chief Jason Luo has resigned, effective immediately, new chief to be named in future announcement

(US) Trump team considers nationalizing 5G network in order to counter China – Axios

(US) President Trump will use his State of the Union address to build momentum for legislation on infrastructure and immigration - financial press Looking Ahead: Corporate earnings are expected from companies including Lockheed Martin, Seagate Technology

Europe

(EU) ECB's Knot (Netherlands): central bank has to end its QE program as soon as possible, arguing that there’s not a single reason anymore to continue with it - Buitenhof

(ES) Spain’s Constitutional Court on Saturday blocked Catalonia’s Puigdemont from returning to power in the region (as expected); The Catalonia regional parliament is expected to vote for a new leader on Tuesday in Barcelona – financial press

(UK) PM May facing Conservative party demands to fire Chancellor Hammond over over his push last week for a “very modest” Brexit – FT [**Note: On Friday, Jan 26th a UK government spokesperson said PM May has full confidence in Chancellor Hammond (Fin Min)]

(UK) Govt officials from both China and UK have declared the “golden era” in bilateral ties between China and the UK is in jeopardy ahead of British Prime Minister May’s visit to Beijing next week amid disagreements over China’s overseas investment drive

(IE) Ireland Jan Bank of Ireland Economic Pulse: 92.8 v 88.9 prior

(AT) Fitch affirms Austria sovereign debt at AA+; outlook Stable (from Jan 26th)

(FR) Fitch affirms France sovereign rating at AA; outlook Stable (from Jan 26th)

Temenos [TEMN.CH]: Responds to recent press speculation and says it has not been approached to be acquired nor is it in discussion to do so

Levels as of 01:00ET

Nikkei225 flat, Hang Seng -0.2%; Shanghai Composite -0.3%; ASX200 +0.4%, Kospi +0.9%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.0%, Dax -0.1%; FTSE100 -0.2%

EUR 1.2434-1.2385; JPY 108.99-108.51; AUD 0.8118-0.8079;NZD 0.7364-0.7318

Feb Gold -0.4% at $1,346/oz; Mar Crude Oil +0.3% at $66.31/brl; Mar Copper +0.8% at $3.23/lb

Today Will Be Fairly Quiet With No Global Market Movers Released

Market movers today

Today will be fairly quiet with no global market movers being released. Later in the week, focus is on Donald Trump’s State of the Union speech (Tuesday), the Fed meeting (Wednesday), euro area HICP figures for January (Wednesday), and not least Chinese PMI data (Thursday).

In the US, PCE headline and core inflation as well as personal spending data for December are due to be released.

EU27 ministers will meet in Brussels today to finalise a set of negotiating directives for the Brexit negotiations, which could give new det ails on the EU’s position in the transition period.

Selected market news

On Friday, EUR fixed income markets continued to be under pressure following Thursday’s ECB meeting (see ECB Review – Language to be revisited in March, 25 January 2018). Once again, the 5Y segment on the yield curve was the catalyst point for the move higher in yields, climbing around 4bp higher. Meanwhile, further out on the curve, the 30Y segment dropped a couple of basis points (out right ) leading to a further curve flat tening of the 5Y-30Y. Over the weekend ECB, GC member Klas Knot (hawkish) said that the ECB QE programme has to end ‘as soon as possible’ also saying that ‘the program is fixed until September’ (see Bloomberg).

On Friday, the Bank of Japan (BoJ) clarified that Governor Haruhiko Kuroda was not revising the inflation outlook when he said in Davos that inflation was finally moving close to the 2% target (see Bloomberg). After Kuroda’s remarks on Friday , the USD/JPY dropped nearly 1% and has since regained some of the initial fall.

In the US today, focus will be on the PCE inflation print, which is expected to increase to 1.6% y/y. After the higher-than-expected US CPI inflation print in December the marketimplied probability of a Fed March hike has edged higher. Currently, markets have priced in a March Fed hike with an 85% probability and a total of two and a half hikes in 2018.

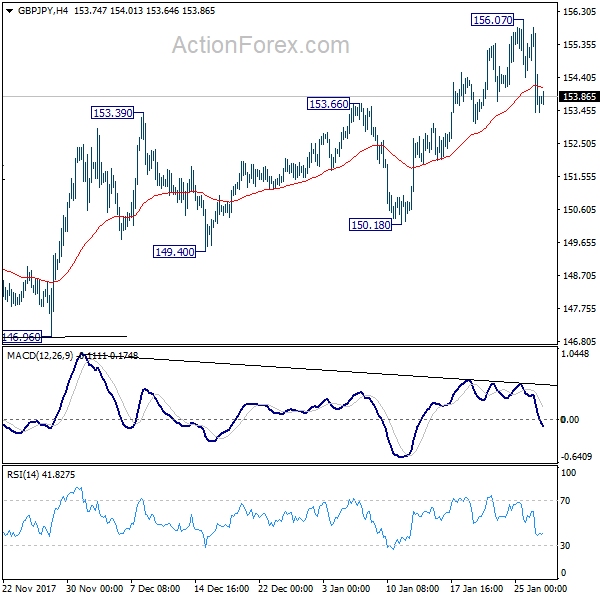

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.84; (P) 154.34; (R1) 155.26; More...

Intraday bias in GBP/JPY is mildly on the downside. Fall from 156.07 short term top would extend to 150.18 support first. Break there will target a test on 146.96 key support level. Nonetheless, break of 156.07 will resume medium term rally.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 134.29; (P) 135.21; (R1) 135.89; More....

Intraday bias in EUR/JPY remains neutral but outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

Will The U.S. Dollar Find Support This Week?

The U.S. dollar's worst start in 21 years has reminded many investors of trade wars, particularly after U.S. Treasury Secretary Mnuchin commented about the benefits of a weaker dollar and the decision by President Trump to impose tariffs on imported solar panels and washing machines.

However, these aren't the only factors that have contributed to the dollar's weakness. Traders across the globe are highly anticipating the end of stimulus from major central banks, including the BoJ and ECB. This has been reflected in sovereign and corporate bond markets where yields on more than $800 billion of debt moved into positive territory.

The rise in U.S. bonds yields are doing little to support the greenback, simply because yields elsewhere are also moving higher, but if spreads continue to widen, the dollar should begin attracting some inflows.

The week ahead will be a busy one, and focus will remain on the U.S. dollar. Mr. Trump will deliver his first State of the Union address to Congress on Tuesday. Although he is highly likely to declare a victory over the tax overhaul, and how his actions boosted the American economy and stock returns, investors will be focused on any details surrounding the infrastructure bill, trade tensions, and border wall funding. So expect some volatility as he speaks.

The Federal Reserve is expected to leave policy unchanged when it announces the rate decision on Wednesday. Given this is the last meeting Chaired by Janet Yellen, I don't expect much out of it. However, any tweaks in the statement may be slightly hawkish given that inflation expectations has risen to its highest levels since 2014.

If neither of these two events support the dollar, Friday's jobs report will be given a chance to do so. After a disappointing figure in December, markets are anticipating 175,000 non-farm payrolls have been added in January. Moreover, since the return of inflation is becoming a hot topic, wage growth will be under the traders' microscope once again. This is where we might see a surprise- driven by increased bonuses following the tax reforms.