Sample Category Title

USD/CHF Dizzy Fall

USD/CHF is trading lower. Support at 0.9533 (19/01/2017) is now broken. Hourly resistance at 0.9668 (17/01/2017 high) moves away. Expected to show further short-term downside move.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found at 0.9072 (07/05/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Heading Lower

USD/JPY is trading below the 110 mark. The resistance at 111.50 (18/01/2018) is distanced. The technical structure suggests further shortterm downside moves.

We favor a long-term bearish bias. Support is now given at 101.20 (09/11/2016 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Steep Rise

GBP/USD keeps trading higher. The technicals is positive. Hourly support is given at 1.3742 (16/01/2018 low).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is now moving up to 2016 highs. A long-term support given at 1.1841 (07/10/2017 low) and a strong resistance at 1.5018 (24/06/2016 high) are identified.

EUR/USD Trading Around 1.2415

EUR/USD keeps on increasing. The pair has strongly bounced back. Hourly support is given at 1.2165 (17/01/2017 low). The technical structure suggests further short-term upside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2856 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Market Update – European Session: Attention Turns To ECB Meeting

Notes/Observations

US dollar (USD) maintained a soft tone amid comments from US officials and trade concerns; global leaders ask US to clarify weak dollar comments

German GFK Consumer mood at highest level since Oct 2001

German Jan IFO Business Climate Survey matched its highest level since reunification (1991)

ECB rate decision and press conference in focus; Given current level of Euro will Draghi diminish the hawkishness of the last ECB minutes?

Asia:

New Zealand Q4 CPI misses expectations with the annual pace within RBNZ target range for the 5th straight quarter Q/Q: 0.1% v 0.4%e; Y/Y:1,6% v 1.9%e

South Korea Q4 Preliminary GDP registers its first contraction since 2008 (Q/Q: -0.2% v +0.1%e; Y/Y: 3.0% v 3.4%e

S&P affirmed Australia sovereign AAA rating; Outlook negative

China Commerce Ministry (MOFCOM) Spokes; Cooperation is only correct direction for China-US trade relationship, does not want escalation of trade 'spats' with the US. person Gao Feng: "strongly" opposes USTR report; trade frictions outlook still severe in 2018

China PBOC Gov Zhou was not re-elected to CPPCC National Committee; Vice Premier Wang Yang is in the new national committee (**Note: Zhou was expected to retire ‘soon’)

PBOC: skipped OMOs as liquidity levels in banking system were “appropriate and stable” (1st skip since Jan 9th)

Europe:

France President Macron commented at Davos that globalization was going through major crisis and that the race to the bottom on taxes was not the right answer to globalization

UK Office for Budget Responsibility's Chote: UK economy is 'weak and stable' with 50% chance of another recession in five years

Americas:

President Trump stated that he would answer questions from Special Counsel Mueller under oath, would tell him there was no collusion with Russia; wanted $25B fund to build the wall; open to the concept of giving DACA recipients citizenship in 10-12 years

President Trump to outline $1.7T infrastructure plan in State of the Union address scheduled for Tuesday, Jan 30th

All three appeal judges in Former Brazil President Lula corruption case voted to uphold the conviction conviction

Energy:

Saudi Oil Min al-Falih:Highly unlikely OPEC would change course in June. US oil boom was a threat as Mexican and Venezuelan output was declining; did not see signs of a significant oil demand slowdown

Economic Data:

(DE) Germany Feb GfK Consumer Confidence: 11.0 v 10.8e (highest reading since 2001)

(MY) Malaysia Central Bank (BNM) raised Overnight Policy Rate by 25bps to 3.25%; as expected

(FI) Finland Dec Unemployment Rate: 8.4% v 7.1% prior

(NO) Norway Nov AKU Unemployment Rate: 4.1% v 4.0%e

(ES) Spain Q4 Unemployment Rate: 16.6% v 16.1%e

(SE) Sweden Jan Consumer Confidence: 107.2 v 107.0e; Manufacturing Confidence:113.8 v 117.5e, Economic Tendency Survey: 110.2 v 112.0 prior

(SE) Sweden Dec Unemployment Rate: 6.0% v 6.1%e, Unemployment Rate (seasonally adj): 6.5% v 6.5%

(HK) Hong Kong Dec Trade Balance (HKD): -59.9B v -45.9Be; Exports Y/Y: 6.0% v 7.3%e; Imports Y/Y: 9.0% v 7.2%e

(DE) Germany Jan IFO Business Climate: 117.6 v 117.0e (matches record high); Current Assessment: 127.7 v 125.3e, Expectations Survey: 108.4 v 109.3e

(NO) Norway Central Bank (Norges) left its Deposit Rates unchanged at 0.50% (as expected)

(UK) Dec BBA Loans for House Purchases: 36.1K v 39.8Ke

(ZA) South Africa Dec PPI M/M: 0.6% v 0.6%e; Y/Y: 5.2% v 5.2%

Fixed Income Issuance:

(CL) Chile opened its book to sell EUR-denominated Feb 2029 notes; guidance seen +50-55bps to mid-swaps

(IN) India sold total INR110B vs. INR110B indicated in 2024 and 2028 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 401.0, FTSE +0.1% at 7653, DAX -0.1% at 13395, CAC-40 +0.4% at 5515 , IBEX-35 +0.5% at 10618, FTSE MIB +0.4% at 23714 , SMI -0.1% at 9537, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade mixed as the Eurostoxx 600 trades fractionally lower, with strength in the CAC and Ibex offset by weakness in the Dax and Swiss SMI.

Earnings continued to be the dominant theme this morning, with notable earners including Diageo, Sky, ST Micro and Asos. Notable decliners this morning include Zumtobel, Fingerprint Cards, Aryzta following profit warnings, while an upbear trading strament from Daily Mail Group, and earnings from Elior helped push shares higher.

In other news Clariant shares fall over 7% after Sabic took a 25% stake.

Looking ahead notable earners include Dow components 3M and Caterpillar, as well as Airlines, Jetblue, Southwest and American Airlines. Other notable earners include Fiat Chrysler, Northrop and Raytheon.

Movers

Consumer Discretionary [Diageo [DGE.UK] +1% (Earnings), Aryzta [ARYN-CH] -20% (Cuts outlook), Daily Mail General Trust [DMGT.UK] +4% (Trading update), Elior [ELIOR.FR]+3.0% (Earnings), Hornby [HRN.UK] -13% (Trading update), Asos [ASC.UK] -0.4% (Trading update), Zumtobel [ZUM.AT] -16% (Profit warning), Sky Plc [SKY.UK] +1% (Earnings)]

Materials [Clariant [CLN.CH] -10% (Sabic takes stake)

Technology [Software AG [SOW.DE] -4.6% (Earnings), Fingerprint Cards [FINGB.SE] -24% (Prelim Q4), Accesso Tech [ACSO.UK] +5% (Trading update)]

Speakers

Norway Central bank (Norges) policy statement noted that the decision to keep policy steady was unanimous. No substantial changes to outlook since December. Inflation to remain below the 2.5% target in coming years. Inflation was low but had moved up as expected

IMF's Lagarde: Trade is a very significant engine of growth. Stated that the USD value was determined by markets but called upon US Treasury Sec Mnuchin to clarify comments on a weak USD currency

UK Chancellor of Exchequer Hammond (Fin Min): Brexit transition deal would likely be around two years. Satisfied with current level of GBP currency

EU Official: UK trade deals only applicable after transition

Treasury Sec Mnuchin: Earlier comments on USD was consistent and quite clear; believed in free currencies (markets determine the rates). Long-term USD level was determined by economic strength. Did not want to enter trade wars. Had a very good and open dialogue with China; discussed possible trip[ to China later in 2018

US Commerce Sec Ross stated at Davos that President Trump was more interested in bilateral accords as they had fewer moving parts. Hard to say when the NAFTA talks would end; needed to get a proper deal; mindful of the upcoming Mexican election. Would not give previews on what will happen on steel

S&P Report: Strong Euro could delay QE tapering as dovish Council members would set the tone. Draghi likely to strike a dovish tone at the Jan policy meeting

German IFO Economists: noted that the domestic economy had a dynamic start to 2018 and was in excellent condition despite the lack of a new govt and saw no dampening effect from the Euro currency strength

Malaysia Central Bank Policy Statement noted that it decided to normalize the degree of monetary accommodation as the domestic economy was firmly on a steady growth path. Current level of Overnight rate and stance of monetary policy remained accommodative. Strong economic growth momentum was expected to continue and be sustained by stronger global growth and positive spillovers from external sector. Inflation was expected to average lower in 2018

Currencies

The USD weakness continued to be in focus but the greenback was off its worst levels coming into the NY morning. .

EUR/USD tested the 1.2459 during the Asian session for fresh 3-year highs. The pair came off its best levels ahead of the ECB rate decision as participants moved to the sidelines from recent longs. Markets expected ECB President Draghi to continue to strike a dovish tone especially given the level of the Euro. Analysts noted that ECB would likely show some concern on its inflation outlook if EUR/USD gains broke above 1.26. A strengthening exchange rate would provide headwinds of achieving the inflation target. Back in July the ECB noted that Euro exchange rate (re-pricing) had received some attention

GBP/USD tested 1.4328 overnight for its best level in the aftermath of the Jun 2016 Brexit referendum.

USD/JPY holding just above the 109 level after testing 108.74 overnight

Fixed Income

Bund Futures trades down 7 ticks at 160.50 with the sub-160 area in focus ahead of the ECB rate decision. Continued upside targets 162.00, while a move lower targets the159.56 low.

Gilt futures trade at 122.93 down 2 ticks standing below its declining 50-period moving average. Support continues to stand at 123.02 then 122.55, with upside resistance at 123.75 then 124.33.

Thursday’s liquidity report showed Wednesday’s excess liquidity rose to €1.870T from €1.867T prior. Use of the marginal lending facility fell to €45M from €524M prior.

Corporate issuance saw no deals priced in the primary market

Looking Ahead

(CA) Canada Jan CFIB Business Barometer: No est v 59.7 prior

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

06:00 (UK) Jan CBI Retailing Reported Sales: 13e v 20 prior, Total Distribution: No est v 24 prior

06:00 (CZ) Czech Republic to sell Bills

06:30 (TR) Turkey Jan Capacity Utilization: 78.8%e v 79.0% prior

06:30 (TR) Turkey Jan Real Sector Confidence (Seasonally Adj): No est v 109.2 prior; Real Sector Confidence (unadj): No est v 103.3 prior

06:30 (IS) Iceland to sell Bills

06:45 (US) Daily Libor Fixing

07:00 (RO) Romania to sell 2.3% 2020 Bonds

07:00 (UR) Ukraine Central Bank Interest Rate Decision: Expected to leave Key Rate unchanged at 14.50%

07:00 (BR) Brazil Dec Total Federal Debt (BRL): No est v 3.493T prior

07:45 (EU) ECB Interest Rate Decision: Expected to leave Main Refinancing Rate unchanged at 0.00%

08:00 (RU) Russia Dec Unemployment Rate: 5.2%e v 5.1% prior

08:00 (RU) Russia Dec Real Retail Sales M/M: No est v -1.4% prior; Y/Y: 3.5%e v 2.7% prior

08:00 (RU) Russia Dec PPI M/M: 1.3%e v 0.9% prior; Y/Y: 7.7%e v 8.0% prior

08:00 (RU) Russia Gold and Forex Reserve w/e Jan 19th: No est v $437.9B prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 257Ke v 220K prior; Continuing Claims: 1.93Me v 1.952M prior

08:30 (US) Dec Preliminary Wholesale Inventories M/M: 0.4%e v 0.8% prior, Retail Inventories M/M: No est v 0.1% prior

08:30 (CA) Canada Nov Retail Sales M/M: 0.8%e v 1.5% prior; Retail Sales Ex Auto M/M: 0.9%e v 0.8% prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (EU) ECB’s Draghi post rate decision press conference

09:00 (BE) Belgium Jan Business Confidence: 0.4e v 0.1 prior

09:00 (MX) Mexico Nov Retail Sales M/M: 0.4%e v 1.0% prior; Y/Y: -0.9%e v -0.1% prior

10:00 (US) Dec Leading Index: 0.5%e v 0.4% prior

10:00 (US) Dec New Home Sales: 675Ke v 733K prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Jan Kansas City Fed Manufacturing Activity: 15e v 14 prior

13:00 (US) Treasury to sell 7-Year Notes

(IT) Italy Debt Agency (Tesoro) announces upcoming BTP auctions details for Tues, Jan 30th

16:00 (KR) South Korea Jan Consumer Confidence: No est v 110.9 prior

18:30 (JP) Japan Dec National CPI Y/Y: 1.1%e v 0.6% prior; CPI Ex Fresh Food (core) Y/Y: 0.9%e v 0.9% prior, CPI Ex Fresh Food, Energy (core-core) Y/Y: 0.4%e v 0.3% prior

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

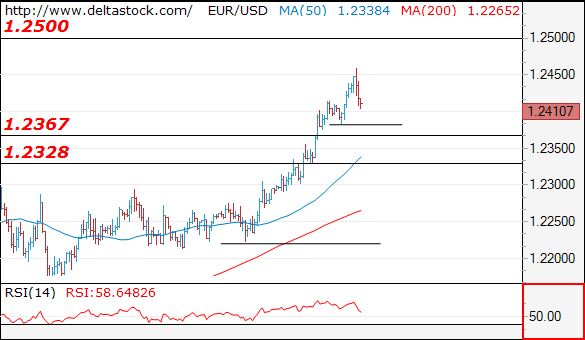

Current level - 1.2410

I think, that today's high at 1.2460 sets the beginning of a corrective pullback towards 1.2367 and even 1.2330. Trigger on the downside is 1.2385.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2440 | 1.2500 | 1.2367 | 1.2330 |

| 1.2460 | 1.2500 | 1.2330 | 1.2220 |

USD/JPY

Current level - 109.10

My outlook is counter-trend against 108.50, for a break through the crucial 109.47, towards 110.20 resistance.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.47 | 110.20 | 108.50 | 108.50 |

| 110.20 | 112.00 | 108.50 | 107.30 |

GBP/USD

Current level - 1.4260

My outlook here switched to counter-trend after the recent peak below 1.4340 area, for a break through the crucial 1.4215, towards 1.4120 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4295 | 1.4340 | 1.4215 | 1.3940 |

| 1.4340 | 1.4620 | 1.4120 | 1.3730 |

Technical Outlook: AUDUSD – Bulls Are Consolidating Ahead Of Final Push Trough 0.8124 Target, Rising 10 SMA To Hold...

The Aussie hit new high at 0.8118 on Thursday, in extension of previous day’s strong rally and took 0.8102 barrier (20 Sep spike high) which marks the last obstacle ahead of key resistance at 0.8124 (08 Sep peak).

Subsequent easing to 0.8062 signaled hesitation at key 0.8124 barrier, with consolidative action expected to precede final push higher for attack at 0.8124.

Bullish structure remains intact and favors further upside, with break above 0.8124 to open way for test of another significant barrier at 0.8161 (14 May 2015 high / 50% retracement of larger 0.9503/0.6826 fall).

Sideways-moving daily RSI (in overbought territory) and slow stochastic (holding under overbought zone boundary) support scenario of consolidation.

The downside attempts should be limited at 0.8000 zone (psychological support, reinforced by rising daily Tenkan-sen / 10SMA) to keep immediate bulls intact.

Conversely, break here could be initial signal of pullback.

Res: 0.8124, 0.8161, 0.8200, 0.8242

Sup: 0.8042, 0.8000, 0.7956, 0.7936

Technical Outlook: USDJPY – Bears Extend Below Strong Supports At 109.10/06 But Corrective Action May Precede Fresh Weakness

The pair remains firmly in red on Thursday, extending steep fall into third straight day and probing below strong supports at 109.10/06 (weekly cloud base /Fibo 76.4% of 107.31/114.73).

Fresh weakness extended to 108.73 so far (the lowest since 11 Sep) with close below 109.06 to generate strong bearish signal for further easing and expose next targets at 108.26 (29 Aug spike low) and 108.12 (11 Sep low).

Meanwhile, bears may take a breather on oversold daily studies (no firmer bullish signals so far), with corrective upticks seen as selling opportunities and ideally capped by former key supports now reverted to resistances at 110.00/15 (psychological barrier / broken Fibo 61.8% of 107.31/114.73, reinforced by falling daily Tenkan-sen).

Res: 109.47, 110.00, 110.15, 110.46

Sup: 108.73, 108.26, 108.12, 107.50

Technical Outlook: GBPUSD – It’s Dangerous To Play Against The Trend But Risk Of Pullback Exists

Cable hit new high at 1.4328 on Thursday, in extension of previous day's 1.7% rally, after pound rallied on weaker dollar.

Important barriers at 1.4288 (Fibo 76.4% of post-Brexit vote 1.5016/1.1930 fall) and 1.4317 (FE 200% of the wave C from 1.3301 trough) were cracked on today's spike but gains were so far short-lived as the pair eased to 1.4232.

No firmer signs of correction so far, despite overextended daily studies, as steep bull-leg from 1.3457 (11 Jan trough), part of broader recovery rally from 1.1930, could extend further of strong bullish sentiment on positive Brexit talks environment, strong signals of strengthening UK economy and significantly weaker US dollar.

Bullish scenario sees firm break above 1.4317 Fibo barrier for extension towards next target at 1.4511 (FE 238.2%).

Conversely, stronger reversal signal requires return below 1.4200 handle and retracement of at least 50% of Wednesday's 1.3996/1.4262 rally to expose strong supports at 1.4026/00 zone (rising daily Tenkan-sen / psychological support / Wednesday's low), break of which would generate stronger bearish signal.

Res: 1.4317, 1.4328, 1.4350, 1.4400

Sup: 1.4232, 1.4200, 1.4163, 1.4124

GBPUSD Rally Set To Continus Above 1.4262

The British pound continues to rally against the U.S dollar, with the pair now starting to trade well above the 1.4300 level, as broad-based selling in U.S dollar index accelerates. The GBPUSD pair has so far traded as high as 1.4324, with buying interests in sterling increasing after solid December Wage Earnings and Employment figures from the United Kingdom economy. GBPUSD traders now look to a scheduled speech from UK PM Theresa May, at the World Economic Forum, and the European Central Bank Policy Meeting later today.

The GBPUSD pair remains strongly bullish while trading above the 1.4262 level, further gains towards 1.4350 and 1.4400 appear possible.

Should price-action on the GBPUSD pair start to decline below the 1.4262 level, the 1.4200 and 1.4127 levels now act as intraday support.