Sample Category Title

CAD/JPY 4H Chart: Waving Flag

After reaching the highest mark since early January at 91.58, the Canadian Dollar continued to lose ground against the Japanese Yen.

In the 4H chart, the pair reached the 50.00% Fibonacci retracement level and continued moving south. The retracement can be measured by connecting the high level of 91.58 touched within the first week of January and with the mid – December low level of 87.34, where the 0.00% level is the high and 100% is the December low.

In regards to future trading, the pair is likely to continue trading south until it breaches the weekly PP level at 87.56. A breakout from the rectangle south or north is a likely option.

Will ECB Provide More Hawkish Guidance?

- WEF Event Eyed Ahead of Trump Speech Friday;

- Will ECB Provide More Hawkish Guidance?

- Mnuchin Plays Down USD Comments After Sell-Off.

WEF Event Eyed Ahead of Trump Speech Friday

US equity markets are currently eyeing a slightly higher open on Thursday, following a fairly volatile session on Wednesday after which indices ended relatively flat.

Investors have plenty to focus on today, with the World Economic Forum in Davos grabbing much of the attention, while 26 S&P 500 companies will report fourth quarter earnings. Meanwhile we’ll also get more economic data from the US and Canada, with jobless claims and new homes sales coming from the former and retail sales the latter. This comes following a morning in which another survey in Germany showed record high business confidence in another boost to the entire regions recovery.

The WEF will undoubtedly grab investors’ attention on Thursday, with some of the world’s most important politicians and business leaders in attendance and making speeches. Naturally, it’s US President Donald Trump’s speech on Friday that is most hotly anticipated given growing concerns globally about protectionism, with many other leaders having warned against it already at the event.

Will ECB Provide More Hawkish Guidance?

The ECB will take some attention away from Davos on Thursday, as the central bank releases its latest monetary policy statement and holds its usual post-meeting press conference. With no change in monetary policy expected, the focus will primarily be on President Mario Draghi’s press conference and particularly what the ECB plans to do once the asset purchase program expires in September.

The ECB in its December meeting minutes alluded to the fact that forward guidance could be revisited early this year and that it will need to evolve gradually, which has driven speculation that the message could become more hawkish earlier than expected. Combined with the improved economic climate in the eurozone and the increasing confidence that inflation will rise, investors are bracing themselves for warnings that bond buying will not be extended past September and even conversations around interest rate hikes next year.

With the euro having rallied strongly over the last couple of months following a brief correction after quantitative easing was last extended, I wonder how priced in a more hawkish ECB is and whether the lack of a hawkish shift today may weaken the single currency. Of course, the euro has been particularly strong against the dollar, the depreciation of which has played a major role in the move.

Mnuchin Plays Down USD Comments After Sell-Off

US Treasury Secretary Steve Mnuchin – who’s comments on Wednesday were blamed for driving the currency lower again – played down these remarks which has failed to sustainably reverse the greenback’s declines. Mnuchin provided balance to his comments insisting that while a weaker dollar has its benefits for trade, a strong dollar has benefits in other areas and that the US isn’t focused on its levels. It seems that traders are only really interested in negative dollar news which isn’t uncommon in bearish markets.

Dollars Downfall Remains Intact, ECB Next

Thursday October 25: Five things the markets are talking about

It was another mixed picture overnight, as capital markets digested the weakening dollar and a protectionist push from the U.S. The greenback has slipped against most G20 currency pairs, while most commodity prices gained.

The EUR has edged higher ahead of today's European Central Bank (ECB) rate decision (07:45 am EDT) and Draghi's highly anticipated press conference (08:30 am EDT). The market is looking for further clues on policy makers' appetite for rolling back stimulus, and their thoughts on a strengthening EUR currency.

What to expect?

In order for traders to stop buying EUR's (€1.2461), President Draghi needs to combine currency worries with downplaying the chance of a guidance change. If he does, the EUR could fall back below the psychological €1.2300 level if Draghi insists that rate increases won't come until QE ends – basically diminishing the ‘hawkishness' of the last ECB minutes.

Will the market buy Draghi's downplaying early ECB exit speculation?

The bond market will find it difficult; yields in Germany and the rest of Europe are not expected to go that much lower now that the market is seriously talking about ‘rate normalization' supported by the global growth story.

The ‘single' unit should find a bid and rise through the €1.25 handle (three-year high) if Draghi focuses on the improvements in the eurozone economy and “acknowledges the possibility of early guidance changes,' even if he expresses concerns about EUR's strength.

The eurozone growth story is already mostly priced into the EUR. Perhaps the next trigger for the common currency's rally is likely to come from politics? Further hints on the progress of eurozone integration would likely give the market confidence to buy the EUR – remember, it was fears of eurozone disintegration that initially pressured the EUR years ago.

1. Stocks under pressure from currency strength

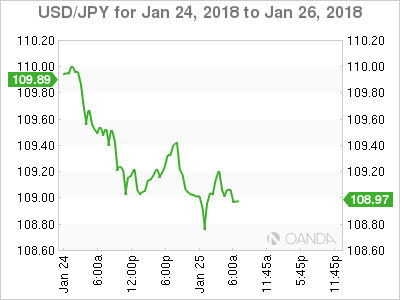

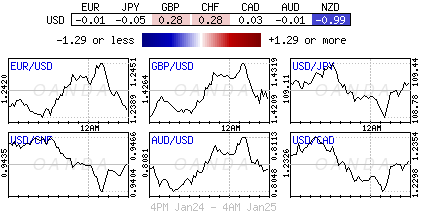

In Japan, the Nikkei share average dropped to a near two-week low overnight as a stronger yen (¥109.08) hurt exporters. The Nikkei ended -1.1% lower, the weakest closing level since Jan. 12. The broader Topix fell -0.9%.

Down-under, Aussie shares recouped some of their losses overnight to end the week in the black as a rally in top material firms partially offset falls in financials. The S&P/ASX 200 index closed lower -0.1%.

In Hong Kong, stocks snapped a seven-day winning streak. The Hang Seng index ended down -0.9%, while the China Enterprises index fell -1.7%.

In China, stocks weakened from two-year highs, with the benchmark Shanghai index snapping a seven-session winning streak, led down by property and healthcare firms. At the close, the Shanghai Composite index was down -0.31%, while the blue-chip CSI300 index was down -0.57%.

In Europe, regional indices trade mixed as the Eurostoxx 600 trades fractionally lower, with strength in the CAC and Ibex offset by weakness in the DAX and Swiss SMI. Market is looking ahead to ECB's press conference.

U.S stocks are set to open in the ‘black' (+0.1%).

Indices: Stoxx600 flat at 401.0, FTSE +0.1% at 7653, DAX -0.1% at 13395, CAC-40 +0.4% at 5515, IBEX-35 +0.5% at 10618, FTSE MIB +0.4% at 23714, SMI -0.1% at 9537, S&P 500 Futures +0.1%

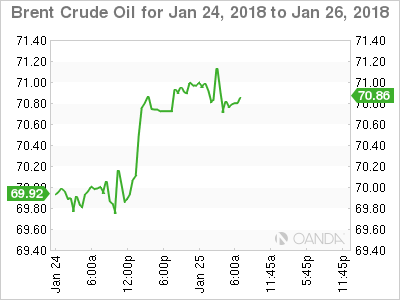

2. Oil rallies on tighter supply and weaker dollar

Brent crude oil hit +$71 a barrel overnight for the first time in three-years, supported by an OPEC-led supply curbs and a record-breaking run of declines in U.S crude inventories coupled with a weaker USD.

OPEC and its allies, including Russia, began to curb supplies in 2017. An involuntary drop in Venezuela's output in recent months has deepened the impact of the curbs.

Brent crude prices have hit +$71.20 a barrel, the highest since early December 2014, while U.S crude has climbed to +$66.44, also the highest since early December 2014, before dipping to +$66.05, up +44c.

Casting a shadow over the oil rally is the presence of growing output of U.S shale oil, as higher prices encourage more investment in expanding supplies.

Note: U.S crude oil production is expected to surpass +10m bpd next month, and on the way to a record ahead of previous forecasts according to the U.S government's EIA.

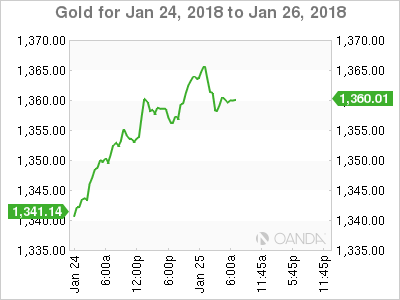

Ahead of the U.S open, gold prices have rallied to their 18-month high, buoyed as the U.S dollar hit three-year lows after ‘weaker currency' comments from U.S Treasury secretary Mnuchin. Spot gold has rallied +0.2% to +$1,360.56 per ounce, after hitting its highest since Aug. 3, 2016 at +$1,366.07.

3. Sovereign yields wait for ECB press conference

Consensus expects ECB President Draghi will likely try to downplay all early ECB exit speculations in a few hours, but will the market buy it? With monetary policy normalization, a primary 2018 trading theme, lower sovereign yields are not expected to be the norm.

Elsewhere, Norway Central bank (Norges) policy statement this morning noted that the decision to keep policy steady was unanimous and that there were no substantial changes to outlook since December. Inflation is to remain below the +2.5% target in coming years – domestic inflation is low, but has moved up as expected.

Note: Previous comments from Norges Bank's Governor Olsen in December indicated that policy makers might decide to follow in the footsteps of the Fed and increase its key interest rates toward the end of 2018.

In Japan, JGB yields edged higher overnight, following U.S Treasury movements, even as a sharply stronger yen sends Japan equities lower. Yields on the benchmark 10-year and newest 30-year JGB's are both higher by +0.05% each at +0.080% and +0.825%.

The yield on 10-year Treasuries decreased -1 bps to +2.64%, while Germany's 10-year Bund yield declined -1 bps to +0.59%.

4. Dollars downfall remains intact

The ‘mighty' USD weakness continues to be the focus, but the dollar is off its worst levels heading into the N. America trading session. The latest U.S dollar weakness came amid Treasury secretary Mnuchin ‘weaker' comments and trade concerns – global leaders have asked the U.S to clarify weak dollar comments.

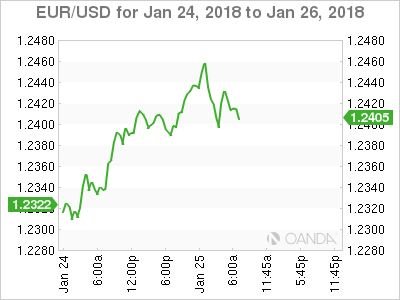

The EUR/USD has tested its three-year highs atop of €1.2459 and have since come off its best levels ahead of the ECB rate decision as participants moved to the sidelines from recent longs. Will Draghi continue to strike a ‘dovish' tone especially given the level of the EUR? Expect the ECB to show some concern on its inflation outlook if the EUR breaks above €1.26. A stronger currency would provide headwinds of achieving the ECB's inflation target.

Elsewhere, sterling tested £1.4328 overnight for its best level in the aftermath of the Jun 2016 Brexit referendum, while USD/JPY is holding atop of ¥109 level after testing ¥108.74 earlier in the session

5. German business sentiment ties record-high

Data this morning showed that German business sentiment in January tied November's record high amid strong order books in the manufacturing sector.

The Ifo Institute for Economic Research said that its business climate index rose to 117.6 points in January from 117.2 points in December, beating economists' expectations for a slight decline to 117.0.

“The German economy has had a dynamic start to the year,' said Ifo president Clemens Fuest.

Capacity utilization in the important manufacturing sector rose further from an already elevated level, bolstering businesses mood about their current business situation, which they assessed as “better than ever,' the Ifo said.

Yet despite the excellent current situation, the roughly 7,000 businesses polled by the Ifo in January trimmed their expectations for the next six months, the think tank said.

Euro Punches Past After 1.24 After Mnuchin Comments, ECB Decision Next

The euro has ticked higher in the Thursday session. Currently, EUR/USD is trading at 1.2418, up 0.08% on the day. The euro is currently at its highest level since December 2014. On the release front, German indicators beat the forecasts. GfK Consumer Climate rose to 11.0, above the estimate of 10.8 points. As well, Ifo Business Climate improved to 117.6, beating the estimate of 117.1 points. Later in the day, the ECB will issue a monetary policy statement and is expected to maintain rates at a flat 0.00%. Over in the US, today’s key indicators are unemployment claims and New Home Sales. On Friday, the US releases Advance GDP for the fourth quarter of 2016, as well as durable goods reports.

With the eurozone economy in rebound mode, there is increasing talk of the ECB shifting to a normative monetary policy, after years of massive stimulus. Still, we’re unlikely to see any dramatics at the first policy meeting of 2018, as the ECB is likely to retain its pledge to continue buying bonds under its asset-purchase program (QE). The ECB has trimmed QE from EUR 60 billion to 3o billion/mth, and ECB policymakers have hinted that the Bank could wind up QE in September, and this has pushed the euro higher in recent weeks. ECB President Mario Draghi will speak after the statement, and any hints that QE will not be extended could send the euro to higher ground. However, Draghi may prefer to keep a low profile until the March policy meeting, when policymakers will have had a chance to review updated economic forecasts.

The US Senate confirmed Jerome Powell as the next head of the powerful Federal Reserve on Tuesday. The vote of 84-13 was a cakewalk, reflecting strong bipartisan support for Powell. The new chair is expected to continue Janet Powell’s monetary stance, which was marked by small, incremental rate hikes during a period of economic expansion. The Fed has started to trim its massive balance sheet, another vote of confidence in the strength of the economy. At the same time, Fed policymakers are divided over how to approach inflation, which remains below the Fed target of 2.0%, despite a strong economy and a red-hot labor market. Another unknown is how the recent tax reform legislation will impact the US economy, and investors will be looking at the Fed as one source for guidance.

EUR/USD Analysis: Awaits Information From ECB

The common European currency surged against the Greenback during the first part of Wednesday. The upper channel line of the senior channel failed to limit the pair, thus allowing further appreciation towards the weekly R3.

This upward momentum which was mainly driven by Mnuchin's comments should allay in the nearest hours, thus allowing bears to dominate this session.

However, the ECB is to release its Minimum Bid Rate and have a conference at 1245GMT and 1330GMT, respectively. In case of any positive surprise, the rate could briefly trade above the 1.25 mark. Investors are waiting for some information on whether and/or how the Bank is to curb the Euro's strong appreciation which has pushed the rate up to its highest level sine late 2014.

Downside target could be 1.23.

GBP/USD Analysis: Reluctant To Breach 1.43

Upside risks have dominated the GBP/USD exchange rate for the third consecutive session. Contrary to expectations, the Pound did not return back to the breach senior channel circa 1.40, but moved confidently towards a new 1,5-year high at 1.43.

Similarly to other major pairs trading against the Greenback, technical indicators of this pair are pointing to a soon decline. This assumption is likewise reinforced by the fact that the bullish sentiment allayed considerably starting from late Wednesday.

In case a reversal is to occur in the nearest hours, this would re-confirm the existence of a three-week ascending channel. In line with this pattern, a strong southern barrier could be provided by the 1.4150 mark; the 55-hour SMA could likewise be located near this area.

USD/JPY Analysis: Falls To 109.00

The bearish momentum that prevailed on Tuesday continued to dominate the market on the following day, as well. As a result, the US Dollar experienced a considerable 0.98% fall against the Yen on Wednesday.

It seems that this session might finally mark a change in the previous sentiment. The pair reached the weekly S3 near the 108.90, but was rather reluctant to edge lower. This mark coincides with the bottom boundary of a five-week descending channel.

Thus, the base scenario favours a period of appreciation towards the 110.20 area where the weekly S1, the monthly S2 and the 55– and 100-hour SMAs are located.

In case high volatility is not apparent in this session, the Greenback might remain near the breached senior channel circa 109.60.

XAUUSD Analysis: Climbs To Highest Level Since Mid-2016

Gold continues to appreciate against the US Dollar for the second consecutive session. The pair's surge late on Wednesday was attributed primarily to fundamental events as a result of which the yellow metal had already reached its highest mark since mid-2016 circa 1,365.00 by Thursday morning.

Technical indicators are located near their historic highs and are starting to converge. These factors suggest that downside risks are likely to prevail in the market today.

The expected fall is likely to be hindered near the 1,355.00 mark which is reinforced by the weekly and monthly R2s. The pair, however, should gather strength and push even lower.

The ultimate low for today should be the 55-hour SMA and the weekly R1 near 1,345.00.

GBP/USD: UK Average Earning Index

The British Pound appreciated against the US Dollar on the official UK labour market data. The GBP/USD currency pair added 22 base points or 0.16%, touching the 1.4116 mark, and managed to sustain the upmove.

The number of working people in the UK rose surprisingly in the three month period to November, while regular wages increase at the strongest rate in a year, the official report indicated on Wednesday. The Office for National Statistics stated that the Average Earnings Index was unchanged at 2.5%, while earnings without bonuses grew 2.4% year-over-tear in the reported period. Statisticians said that with the amount of vacancies at a new record and strong employment, demand for labour remained solid.

NZD/USD: NZ Consumer Price Index

The Kiwi lost its ground against the US Dollar, following disappointing inflation report for New Zealand. The NZD/USD exchange rate dropped 83 base points or 1.12% to be seen trading below the 0.7350 level.

Statistics New Zealand stated that the country's Consumer Price Index increased just 0.1% in the December quarter, missing expectations dramatically and causing a sell-off in the domestic currency. The result pressed yearly inflation growth pace to 1.6%, compared with expectations for 1.9%. The weak CPI figure would exacerbate the determination of the Reserve Bank of New Zealand to keep rates unchanged for years, ahead of the next monetary policy decision announcement on February 8.