Sample Category Title

GBPUSD Direction Centered Around 1.4262 Level

The British pound has corrected lower against the U.S dollar during the European trading session, hitting 1.4231, as GBPUSD buyers take profit from overstretched levels. The pair faces strong technical resistance at the 1.4350 level, which represents the 76.4 Fibonacci retracement of the Brexit spike high, to the 2017 swing-price-low. Price-action is currently consolidating around the pivotal 1.4262 level, as sterling traders await the ECB Policy Meeting and UK Prime Minister Theresa May's speech at the World Economic Forum.

The GBPUSD pair remains intraday bullish while trading above the 1.4262 level, further upside towards 1.4300 and 1.4350 appears likely.

Should price-action on the GBPUSD pair start to move below the 1.4262 level, a deeper correction towards the 1.4231 and 1.4200 support levels may ensue.

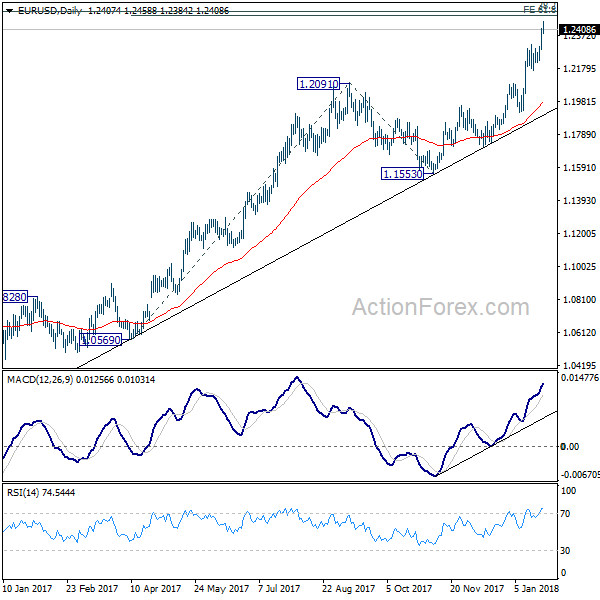

EURUSD Intraday Bullish Above 1.2376

The euro currency has moved to yet another new 2018 trading-high against the U.S dollar, hitting 1.2458, as the greenback faced a wave on new selling interest. Price-action is currently holding around the 1.2420 level, with the EURUSD pairs key 200-month moving average located just above, at the 1.2432 level. Traders and investors now await the European Central Bank Policy Meeting, with financial markets looking for ECB President Mario Draghi's comments on the rapid appreciation of the EURUSD exchange rate.

The EURUSD pair remains strongly bullish while trading above the 1.2376 level, upside targets remain 1.2470 and 1.2500 for buyers.

Should the EURUSD pair move below the 1.2376 level, sellers may push price-action towards the 1.2332 and 1.2396 support levels.

Euro Stalls ahead of ECB Policy Meeting; Oil Hits Fresh 3-Year Highs

Here are the latest developments in global markets:

FOREX: The dollar stalled its downtrend near today's 4 ½ -month lows versus the yen, last seen at 108.97 (-0.16%), and remained flat close to 3-year lows of 89.06 against a basket of currencies as traders continued to digest the comments made by the US Treasury Secretary who said that a weaker dollar is more attractive for trade purposes. Pound/dollar slipped to 1.4252 (+0.08%) during early European trading hours after breaking 1.4327 – a level it last saw before the Brexit referendum –, while euro/dollar erased earlier gains, falling back to 1.2400 (-0.05%). Aussie/dollar eased to 0.8042 and kiwi/dollar managed to pick up to 0.7391 following a deep fall towards 0.7324 attributed to worse than expected inflation readings. Dollar/loonie changed hands at 1.2323 (-0.20%).

STOCKS: The European stocks were mixed ahead of the ECB meeting. The pan-European STOXX 600 was flat and the blue-chip Euro STOXX 50 was up by 0.23% at 1100 GMT with telecommunication services being the best performers. The German DAX 30 was weaker by 0.12%, weighed by losses in industrials, while the French CAC 40 increased by 0.48% with all its sectors being in the green. The British FTSE 100 inched up by 0.11% affected mainly by changes in stock ratings.

COMMODITIES: Oil prices reached fresh 3-year tops during the European afternoon as a falling dollar, declining US oil stockpiles and OPEC-led supply cuts continued to underpin the market. WTI crude peaked at $66.44 per barrel before it fell back to $66.00 (+0.72%) and Brent hit a high at $71.20 before it edged down to $70.68 (+0.44%). Gold moved lower to $1359 (+0.04%) per ounce after reaching a 1 ½-year high at $1365.89.

Day ahead: ECB decides on monetary policy; Japanese inflation pending in Asia session

The ECB's monetary policy meeting at 1245 GMT will be closely watched by investors during the European afternoon, with the potential to bring fresh volatility to the euro. ECB policymakers are widely expected to keep rates unchanged, though, the press conference following the decision at 1330 GMT could be of greater importance. Particularly, analysts will be eager to hear comments on the central bank's quantitative easing program and any changes to its intention to reduce monetary stimulus. Any remarks on the strengthening euro are expected to attract attention as well.

In Canada, monthly retail sales due at 1330 GMT are said to lose speed in November, growing by 0.8% m/m compared to a rise of 1.5% in the previous month, while, excluding automobiles, the measure is forecasted to grow at October's pace of 0.8%.

Meanwhile out of the US, initial jobless claims are seen slightly higher by 16,000 at 240,000 in the week ending January 19. New home sales will follow at 1500 GMT, with analysts forecasting a large decline of -7.9% m/m in December. Recall that in November the gauge posted the biggest expansion rate since 2013, jumping by 17.5% m/m.

Late in the day, Japan will report on inflation for the month of December at 2330 GMT, with the potential to extend or reverse the yen's recent rally if the results deviate far from the forecasts. According to Reuters, the core CPI which is closely watched by the BoJ is projected to remain flat at 0.9% y/y, while based on other sources, the headline inflation rate might nearly double to 1.1% y/y from 0.6% in November.

In stock markets, Caterpillar, 3M Company and Union Pacific Corporation are among companies to report on quarterly earnings prior to the US market open.

Canadian Dollar Edges Higher, Retail Sales Next

The Canadian dollar has posted slight gains in the Thursday session. Currently, the pair is trading at 1.2328, down 0.15% on the day. On the release front, it's a busy day on both sides of the border. Canada will release retail sales reports, while the US publishes unemployment claims and New Home Sales. On Friday, Canada publishes CPI and the US releases Advance GDP and durable goods reports.

The Canadian economy has been performing fairly well, but there is a dark cloud on the horizon regarding NAFTA. The free trade agreement is critical for the Canadian economy, so threats by US President Trump to blow up the agreement are causing genuine concern for the government and the Bank of Canada. Negotiations between Canada, Mexico and the US have not yielded much progress, and a sixth round of negotiations started on Tuesday in Montreal. Trump has repeatedly said he is unhappy with the deal, and would prefer a new bilateral agreement between the US and Canada. Still, Trump is unpredictable, and there are also many US companies that benefit from the current deal and are opposed to the US pulling the plug. If NAFTA is terminated, it's a good bet that the Canadian dollar will take a tumble.

It should be a smooth transition for the Federal Reserve, as Jerome Powell is set to replace Janet Yellen as chair of the powerful central bank. On Tuesday the Senate confirmed Jerome Powell as the next head of the powerful Federal Reserve on Tuesday. The vote of 84-13 was a cakewalk, reflecting strong bipartisan support for Powell. The new chair is expected to continue Yellen's monetary stance, which was marked by small, incremental rate hikes during a period of economic expansion. The Fed has started to trim its massive balance sheet, another vote of confidence in the strength of the economy. At the same time, Fed policymakers are divided over how to approach inflation, which remains below the Fed target of 2 percent, despite a strong economy and a red-hot labor market. Another unknown is how the recent tax reform legislation will impact the US economy, and investors will be looking at the Fed as one of the sources for guidance.

The US Senate confirmed Jerome Powell as the next head of the powerful Federal Reserve on Tuesday. The vote of 84-13 was a cakewalk, reflecting strong bipartisan support for Powell. The new chair is expected to continue Janet Powell's monetary stance, which was marked by small, incremental rate hikes during a period of economic expansion. The Fed has started to trim its massive balance sheet, another vote of confidence in the strength of the economy. At the same time, Fed policymakers are divided over how to approach inflation, which remains below the Fed target of 2.0%, despite a strong economy and a red-hot labor market. Another unknown is how the recent tax reform legislation will impact the US economy, and investors will be looking at the Fed as one source for guidance.

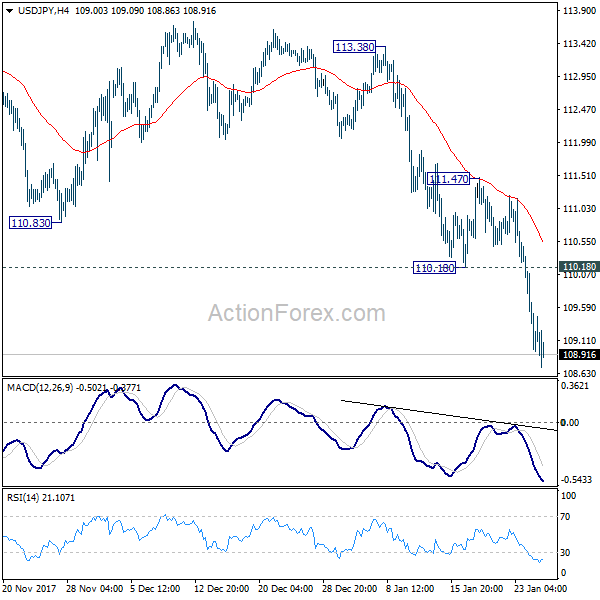

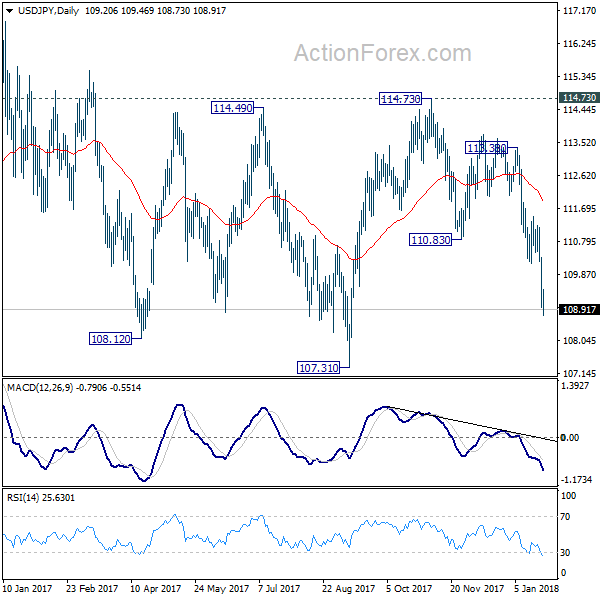

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.67; (P) 109.50; (R1) 110.04; More...

Intraday bias in USD/JPY remains on the downside for 107.31 low. Break will target next fibonacci support at 106.48. On the upside, break of 110.18 support turned resistance will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD?JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9393; (P) 0.9486; (R1) 0.9547; More...

USD/CHF's decline continues today and breaks 0.9420 key support. There is no clear sign of bottoming yet. Intraday bias remains on the downside. Sustained trading below 0.9420 will carry larger bearish implication and pave the way to next key fibonacci level at 0.9115. On the upside, above 0.9535 minor résistance will turn bias back to the upside for rebound.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore,we don't expect a firm break of this level. However, firm break of 0.9420 will confirm that fall from 1.0342 is developing into a long term down trend. And in that case, next downside target will be 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115.

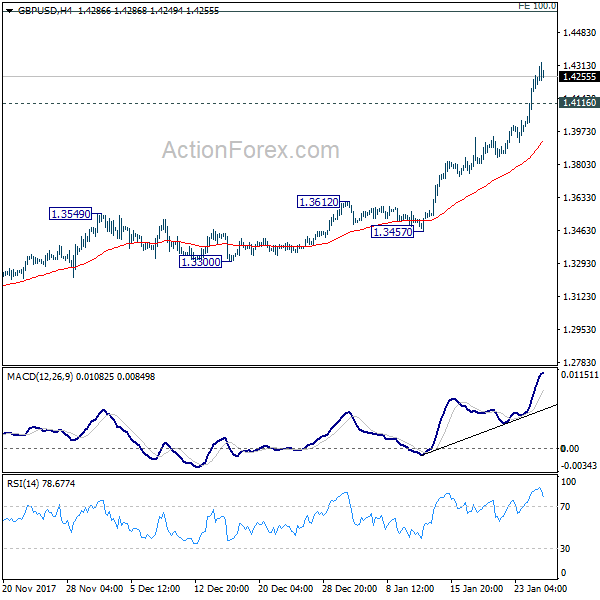

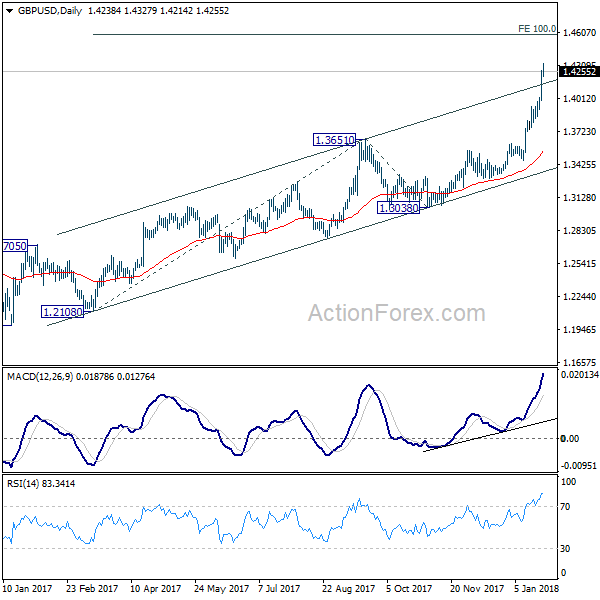

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4067; (P) 1.4164; (R1) 1.4333; More.....

Intraday bias in GBP/USD remains on the upside. Current rally is targeting 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. On the downside, below 1.4116 minor support will turn intraday bias neutral first. But retreat should be contained well above 1.3612 resistance turned support to bring another rise.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

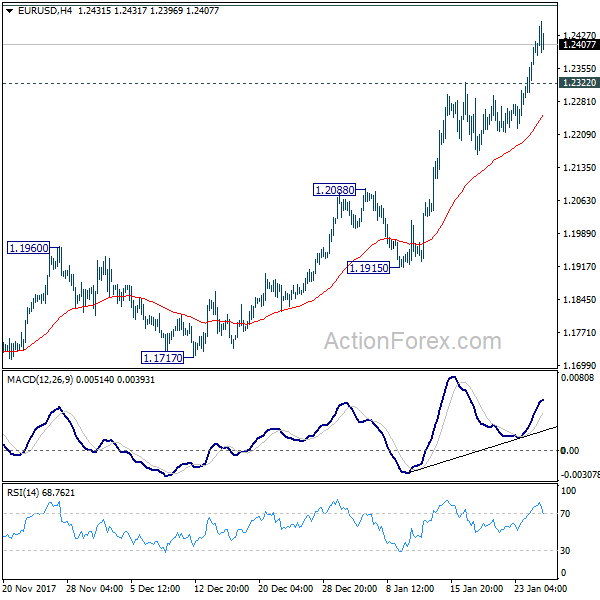

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2326; (P) 1.2370 (R1) 1.2452; More....

With 1.2322 minor support intact, intraday bias in EUR/USD remains on the upside. Current rally should target next key fibonacci cluster level at 1.2494/2516. At this point, we'd still expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2322 minor support will turn intraday bias neutral first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of further rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

DAX – Investors on Sidelines Ahead of ECB Meeting

The DAX is almost unchanged in the Thursday session. Currently, the index is trading at 13,422.50, down 0.06% on the day. On the release front, GfK Consumer Climate rose to 11.0, above the estimate of 10.8 points. As well, Ifo Business Climate improved to 117.6, beating the estimate of 117.1 points. Later in the day, the ECB will issue a monetary policy statement and is expected to maintain rates at a flat 0.00%. On Friday, the US releases Advance GDP for the fourth quarter of 2016, with an estimate of 3.0%.

With the German economy firing on all cylinders, there was no surprise that business and confidence levels rose in January. Consumer confidence improved to 11.0, pointing to an optimistic consumer early in 2018. Business confidence also moved higher, as Ifo Business Climate improved to 117.6, up from 117.1 in the previous release. The German Office of Statistics recently released preliminary data for GDP, and the reading of 2.2% for 2017 improved on the 2016 figure of 1.9%.

With the eurozone economy in rebound mode, there is increasing talk of the ECB shifting to a normative monetary policy, after years of massive stimulus. Still, we're unlikely to see any dramatics at the first policy meeting of 2018, as the ECB is likely to retain its pledge to continue buying bonds under its asset-purchase program (QE). The ECB has trimmed QE from EUR 60 billion to 3o billion/mth, and ECB policymakers have hinted that the Bank could wind up QE in September, and this has pushed the euro higher in recent weeks. ECB President Mario Draghi will speak after the statement, and any hints that QE will not be extended could send the euro to higher ground. However, Draghi may prefer to keep a low profile until the March policy meeting, when policymakers will have had a chance to review updated economic forecasts.

The US Senate confirmed Jerome Powell as the next head of the powerful Federal Reserve on Tuesday. The vote of 84-13 was a cakewalk, reflecting strong bipartisan support for Powell. The new chair is expected to continue Janet Powell's monetary stance, which was marked by small, incremental rate hikes during a period of economic expansion. The Fed has started to trim its massive balance sheet, another vote of confidence in the strength of the economy. At the same time, Fed policymakers are divided over how to approach inflation, which remains below the Fed target of 2.0%, despite a strong economy and a red-hot labor market. Another unknown is how the recent tax reform legislation will impact the US economy, and investors will be looking at the Fed as one source for guidance.

GBP/CAD 4H Chart: The Bull Market

After reaching the monthly pivot point at 1.6777 formed during the first week of January 2018, the British Pound continued to gain strength against the Canadian Dollar.

The pair broke the previous channel down and continued to form a new high. A new junior channel has been mapped to trail the market movement.

The pair is likely to continue trading north until it finds resistance at 1.7854, which is the highest level since early May, 2017. When or if it happens, the pair might make a temporary retracement south.