Sample Category Title

America First, Dollar Last – Let the Trade Wars Commence

Four days after the US government was shut down due to immigration-driven disagreement over extending Federal funding, the US dollar sustained a major blow resulting from protectionist remarks by US Secretary Steven Mnuchin and Commerce Secretary Wilbur Ross.

Shutdown & Protectionism

Resurfacing political dissent is nothing new. Yet, when it threatens the functioning of more than 25 Federal departmental agencies and forces hundreds of thousands of Federal workers into unpaid leave, then it's a serious problem, especially during a mid-term election year.

Remarks by politicians expressing support for domestic industries are also nothing new. So the occasional expression of economic realities by the Treasury chief, that a weak currency helps exports (even if it goes against the supposed official tag line that a strong USD is in the economic interest). However, when the Commerce secretary embarks on an elaborate explanation justifying measures at trade wars on the grounds that: "… trade wars have been in place for quite a little while; the difference is the US troops are now coming to the ramparts", then it's a problem. Not only for the global economy, but especially for the US currency.

Since the 1990s, currency traders have consistently punished the US dollar on each occasion where the US administration adopted protectionist measures (Ronal Reagan vs Japan in 1983-84 and George W Bush with foreign steel in 2002).

Trump fires the first shot

Trump's first trade action is a 30% tariff on imported solar panels and 50% tariffs on large residential washing machines. China will be the target of the tax on solar panels, while South Korea and Mexico will be affected by the tax on washing machines. I will neither focus on the fact that higher tariffs will drive up prices on US consumers, nor tens of thousands of US jobs related to installing solar panels that will be lost as collateral in the trade wars.

Woe from China retaliation

Interestingly, the aforementioned trade tariffs are not so much of a threat to China's industry as they would be a danger to US companies seeking to benefit from the rise of China's consumers. China could begin their own efforts at trade wars by threatening the US to move away from Boeing towards Europe's Airbus, slash its purchases of Apple's products and reduce its demand for US grains.

Mid-Term Trap

Most Democrats opposed the bill to extend government funding because their efforts to preserve protections for over half a million of mostly young immigrants, known as Dreamers. These efforts were rejected by President Trump and Republican leaders. The shutdown ended on Monday, after Senate majority leader Mitch McConnell assured the Democrats that they would hold a debate and a vote on immigration in return for ending the filibuster of a short-term funding deal until February 8.

But, unlike previous battles with Democrats on tax reform and Obamacare, the impasse over Dreamers does involve trump going against sectors of the Republican base.

Trump faces the predicament of having to choose between avoiding upsetting his base and doing what is "right" for immigrants seeking sanctuary in the US. Democrats are not only aware of this, but also of Trump's -40% approval rating during a midterm-election year. This should spur them into playing hardball ahead of the February 8 deadline and raises the possibility of Republicans losing Senate majority in November, not a helpful outcome for markets or the US dollar.

As for trade action, Trump's tariffs in a mid-term election are a blatant parallel to George W. Bush's trade wars declaration on foreign steel in late 2001 aimed at securing victory in the bankrupt Rust Belt states ahead of the 2002 mid-term elections. The US dollar peaked in February 2002. By the time the World Trade Organisation punished the US with $2bn in sanctions, the US dollar had lost 12%, before falling into a 7-year bear market. And, unlike the China of 16 years ago, the China of today will not take things sitting down. Stay tuned.

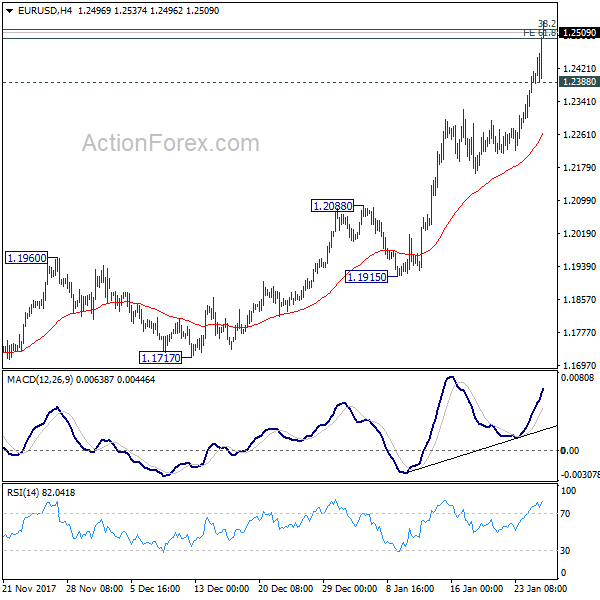

EURUSD Spiked above 1.25 on Draghi But Without Clear Break so Far

The Euro was higher across the board in reaction to ECB President Mario Draghi's press conference after the central bank kept its policy unchanged as expected. Nothing new or surprising from Draghi today, as he pointed on robust pace of economic expansion; underlying inflation remains subdued and is expected to hover around current levels in coming months before increasing as strong cyclical momentum strengthens the confidence that inflation will converge to its target. Draghi said that recent volatility in the FX market is source of uncertainty, with little chances for interest rate hike this year.

The single currency spiked to new high at 1.2537 (the highest since Dec 2014) before easing back below 1.25 handle.

Euro showed impressive rally in January, extending rally of previous two months, with signs of further advance after Mario Draghi failed to at least reduce the pace of recent strong bullish acceleration.

Strong bullish signal could be expected on close above 1.25 handle which would lead for extension towards next pivotal point at 1.2597 (Fibo 61.8% of larger 1.3992/1.0340 descend).

Sentiment remains firmly bullish, but overextended daily studies could lead towards further easing, if the pair dips and closes below 1.2400 handle, which is needed for initial bearish signal.

However, current action was so far insufficient to signal buy the rumors – sell the facts scenario, keeping bias with bulls for now.

Res: 1.2500; 1.2537; 1.2567; 1.2597

Sup: 1.2459; 1.2400; 1.2384; 1.2351

Canadian Retail Spending up in November

Highlights:

- November retail sales increased 0.2% in nominal terms, and 0.3% controlling for the impact of prices.

- Volume sales were boosted by a sharp 12.6% rise in sales at electronic stores.

- E-commerce sales (not all of which are included in the retail sales totals) were up 25.5% over the past year ending in November. That was up from an 18.5% rate in October but still below the 40%+ year-over-year average increase over the first 8 months of 2017.

Our Take:

Retail sales inched up 0.2% in November to build on a 1.6% jump in October. Part of the increase was due to sharp jump in gasoline prices that was responsible for most of a 6% jump in sales at the pump. Sales nonetheless rose a somewhat stronger 0.3% excluding the impact of prices — boosted by a 13% surge in sales at electronic & appliance stores. Statistics Canada noted that the increase in electronics sales in particular looked to have been boosted by new product launches and promotions like 'Black Friday' sales. That means some of the sales increase in November may prove to have been at the expense of sales in December and/or January. Nonetheless, with labour markets continuing to improve at a rapid pace through the end of the year, there are also good reasons to think current underlying trends in retail demand — and indeed, the rest of the economy — remain solid. The retail numbers follow earlier reported sales gains in the manufacturing and wholesale sectors in November. Combined with the potential for a bounce-back from what was likely transitory weakness in oil production in October and still-solid labour market data, that suggests GDP potentially posted a 0.3% or 0.4% increase in November following the surprisingly soft flat reading the prior month. That would remain supportive of the Bank of Canada's, and our own, view that the Canadian economic backdrop continues to improve, if not at the outsized pace seen from mid-2016 to mid-2017.

Canadian Retail Sales Extend Gains in November

Retail sales rose 0.2% in November, marking the third straight month of gains. In real terms, sales were up 0.3%.

Sales were up in about half of the major industries, led by electronics and appliance stores (+13%) and gasoline stations (+6%), the latter of which was driven by higher prices. On the flip side, sales at motor vehicle and parts dealers (-3.6%) provided some offset.

Regionally, the picture was also mixed, with sales up in half the provinces. Quebec (+0.9%) led the way, followed by Manitoba (+0.4%) and Ontario (+0.3%). Sales in Alberta and Saskatchewan were down 0.3%, while B.C.'s were relatively unchanged during the month.

Key Implications

The gains in retail sales volumes in October and November suggest that sales will be up in the fourth quarter as a whole. This bodes well for overall consumer spending and by extension, economic growth during the quarter – the latter of which is currently tracking around 2.5% annualized.

Going forward, we expect consumer spending to remain a key source of strength for the Canadian economy, particularly in light of the recent gains in employment and wages. Recent interest rate increases, however, will likely serve to keep consumer spending in check.

Today's report adds to the economic picture that the data dependent Bank of Canada is watching as it determines its next move. While it is supportive of higher interest rates, the tightening cycle is likely to be slow and gradual, giving the Bank time to assess the impact of higher rates and other uncertainties such as the new B-20 guidelines and any changes to NAFTA.

ECB Stands Pat as Widely Expected, Confident Draghi Shoots Up Euro

Quick updates: Euro surges as being boosted by ECB President Mario Draghi's comment. In his remarks, Draghi said that "incoming information confirms a robust pace of economic expansion, which accelerated more than expected in the second half of 2017." And, "the strong cyclical momentum, the ongoing reduction of economic slack and increasing capacity utilisation strengthen further our confidence that inflation will converge towards our inflation aim of below, but close to, 2%".

Euro remains steady in range after ECB delivers no surprise to the markets. ECB left monetary policies unchanged as widely expected. The main refinancing rate is held at 0.00%, marginal lending facility rate and deposit facility rate at 0.25% and -0.40% respectively. Regarding the EUR 30b per month asset purchase program, the Governing Council confirms that it's intended to "run until the end of September 2018, or beyond, if necessary". Also, that will be "until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim." ECB also left the door open to "increase the asset purchase programme (APP) in terms of size and/or duration" if "outlook becomes less favorable".

German Ifo business climate hit record high

German Ifo business climate rose to 117.6 in January, up from 117.2 and beat expectation of 117.0. That's also the highest reading on record, same as that in last November. Expectations gauge dropped to 108.4, down from 109.4, below consensus of 109.2. Current assessment gauge rose to 127.7, up from 125.5, above consensus of 125.3. Ifo President Clemens Fuest noted in the release that "the German economy made a dynamic start to the year." The expectations gauge did slip. But Fuest said "fewer manufacturers expect to see any further short-term improvement in their very good business situation".

IMF Lagarde urged Mnuchin to clarify his stance on Dollar

IMF managing director Christine Lagarde said that the world economy is at a sweet spot and international trade is growing even faster than economic growth. Meanwhile, she also urged US Treasury Secretary Steven Mnuchin to "clarify exactly what he said" regarding Dollar's exchange rate. She emphasized "the dollar is of all currencies a floating currency and one where value is determined by markets and geared by the fundamentals of US policy."

Mnuchin said his comments were "balanced and consistent".

Dollar's selloff accelerated yesterday after Mnuchin said that a weak dollar is "good for us as it relates to trade and opportunities". He defended that the comments was " balanced and consistent" and, he's "not concerned with where the dollar is in the short term". He further clarified today that it's "perhaps slightly different from previous treasury secretaries" but "it's not a shift in my position". He emphasized that "we do support free and floating currencies reflective of the market". He claimed that "we're not looking to get into trade wars".

EUR/USD Mid-Day Outlook (Update)

Daily Pivots: (S1) 1.2326; (P) 1.2370 (R1) 1.2452; More....

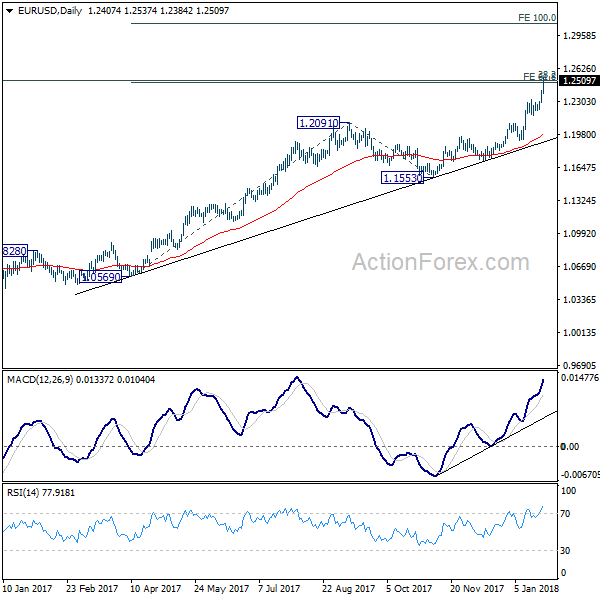

EUR/USD picks up upside momentum again as lifted by ECB Draghi. key fibonacci cluster level at 1.2494/2516 is already met but there is no sign of topping yet. Intraday bias stays on the upside. Sustained break of 1.2494.2516 will target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. On the downside, below 1.2388 minor support will turn intraday bias neutral first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.10% | 0.40% | 0.50% | |

| 21:45 | NZD | CPI Y/Y Q4 | 1.60% | 1.90% | 1.90% | |

| 07:00 | EUR | German GfK Consumer Confidence Feb | 11 | 10.8 | 10.8 | |

| 09:00 | EUR | German IFO Business Climate Jan | 117.6 | 117 | 117.2 | |

| 09:00 | EUR | German IFO Expectations Jan | 108.4 | 109.2 | 109.5 | 109.4 |

| 09:00 | EUR | German IFO Current Assessment Jan | 127.7 | 125.3 | 125.4 | 125.5 |

| 09:30 | GBP | BBA Loans for House Purchase Dec | 36.1K | 39.7K | 39.5K | 39.0K |

| 11:00 | GBP | CBI Reported Sales Jan | 12 | 13 | 20 | |

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Initial Jobless Claims (JAN 20) | 233K | 236K | 220K | 216K |

| 13:30 | CAD | Retail Sales M/M Nov | 0.20% | 0.80% | 1.50% | 1.60% |

| 13:30 | CAD | Retail Sales Ex Auto M/M Nov | 1.60% | 0.90% | 0.80% | |

| 15:00 | USD | New Home Sales Dec | 676K | 733K | ||

| 15:00 | USD | Leading Index Dec | 0.50% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -183B |

EUR/USD Mid-Day Outlook (Update)

Daily Pivots: (S1) 1.2326; (P) 1.2370 (R1) 1.2452; More....

EUR/USD picks up upside momentum again as lifted by ECB Draghi. key fibonacci cluster level at 1.2494/2516 is already met but there is no sign of topping yet. Intraday bias stays on the upside. Sustained break of 1.2494.2516 will target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. On the downside, below 1.2388 minor support will turn intraday bias neutral first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 25 January 2018

INTRODUCTORY STATEMENT

Ladies and gentlemen, first of all let me wish you a Happy New Year. The Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council, which was also attended by the Commission Vice-President, Mr Dombrovskis.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.

Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the new monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase the asset purchase programme (APP) in terms of size and/or duration. The Eurosystem will reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

Incoming information confirms a robust pace of economic expansion, which accelerated more than expected in the second half of 2017. The strong cyclical momentum, the ongoing reduction of economic slack and increasing capacity utilisation strengthen further our confidence that inflation will converge towards our inflation aim of below, but close to, 2%. At the same time, domestic price pressures remain muted overall and have yet to show convincing signs of a sustained upward trend. Against this background, the recent volatility in the exchange rate represents a source of uncertainty which requires monitoring with regard to its possible implications for the medium-term outlook for price stability. Overall, an ample degree of monetary stimulus remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term. This continued monetary support is provided by the net asset purchases, by the sizeable stock of acquired assets and the forthcoming reinvestments, and by our forward guidance on interest rates.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP increased by 0.7%, quarter on quarter, in the third quarter of 2017, following similar growth in the second quarter. The latest economic data and survey results indicate continued strong and broad-based growth momentum at the turn of the year. Our monetary policy measures, which have facilitated the deleveraging process, continue to underpin domestic demand. Private consumption is supported by rising employment, which is also benefiting from past labour market reforms, and by growing household wealth. Business investment continues to strengthen on the back of very favourable financing conditions, rising corporate profitability and solid demand. Housing investment has improved further over recent quarters. In addition, the broad-based global expansion is providing impetus to euro area exports.

The risks surrounding the euro area growth outlook are assessed as broadly balanced. On the one hand, the prevailing strong cyclical momentum could lead to further positive growth surprises in the near term. On the other hand, downside risks continue to relate primarily to global factors, including developments in foreign exchange markets.

Euro area annual HICP inflation was 1.4% in December 2017, down from 1.5% in November. This reflected mainly developments in energy prices. Looking ahead, on the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around current levels in the coming months. For their part, measures of underlying inflation remain subdued – in part owing to special factors – and have yet to show convincing signs of a sustained upward trend. Yet, looking forward, they are expected to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual rate of growth of 4.9% in November 2017, after 5.0% in October, reflecting the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 continued to be the main contributor to broad money growth, expanding at an annual rate of 9.1% in November, after 9.4% in October.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations increased to 3.1% in November 2017, after 2.9% in October, while the annual growth rate of loans to households stood at 2.8% in November, compared with 2.7% in October. The euro area bank lending survey for the fourth quarter of 2017 indicates that loan growth continues to be supported by increasing demand and a further easing in overall lending conditions.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for an ample degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2%.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to strengthening the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the increasingly solid and broad-based expansion strengthens the case for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Strengthening Economic and Monetary Union remains a priority. The Governing Council welcomes the ongoing discussions on completing the banking union and the capital markets union, and on further deepening Economic and Monetary Union.

We are now at your disposal for questions.

NZDUSD Holds in Upward Sloping Channel; Reached 5-Month High

NZDUSD has been developing in an upward sloping channel since December 2017 and during yesterday's trading session it reached a fresh five-month high of 0.7436, though it ended the day in the red. However, it regained some ground over today's European session.

Short-term momentum indicators are signaling for opposite scenarios. The RSI indicator is pointing north in the positive territory, whilst the MACD oscillator slipped below its trigger line but remains in the bullish area. Moreover, in the 4-hour chart, the 20 and 40 simple moving averages are following the price, suggesting further gains.

To the upside, the next resistance level to watch is the 5-month high of 0.7436, while above it the next major barrier is the 0.7460 obstacle taken from the bottom of July 2017.

If prices reverse lower, immediate support could come at 0.7325, which is near the lower band of the sloping channel. Below that, the 23.6% Fibonacci retracement level with the low at 0.6820 and the high at 0.7436, is another major support around 0.7290.

Elliott Wave Analysis: USD Index and EURUSD

Good day traders!

Regarding the overall USD trend, we see prices bearish in wave five on USD Index daily chart, a leg that must contain five subwaves.

USD Index, Daily

Based on latest price move on EURUSD, we think that wave four can be coming soon, as market unfolded five subwaves up from a triangle. Today's close below 1.2383 can be a temporary trend changer.

EURUSD, 1h

EURUSD: Caps Gain, Threatens Pullback

EURUSD: Caps Gain, Threatens Pullback EURUSD: The pair saw a price rejection during Thursday trading session. This leaves the risk of a correction. On the upside, resistance comes in at 1.2400 level with a cut through here opening the door for more upside towards the 1.2450 level. Further up, resistance lies at the 1.2500 level where a break will expose the 1.2550 level. Its daily RSI is bullish and pointing higher suggesting more strength. Conversely, support lies at the 1.2300 level where a violation will aim at the 1.2250 level. A break of here will aim at the 1.2200 level. Below here will open the door for more weakness towards the 1.2150. All in all, EURUSD faces further upside move on bullish offensive